Ultralife Corporation (NASDAQ: ULBI) – Q2 2025 Earnings

Ultralife Corporation (NASDAQ: ULBI) – Q2 2025 Earnings

Earnings Release Date: Aug. 7, 2025

Stock Price: $8.16

Market Cap: $135.7 million

Q2 2025 sales of $48.6 million vs $43.0 million in the prior year

Q2 2025 EPS of $0.07 vs $0.22 in the prior year

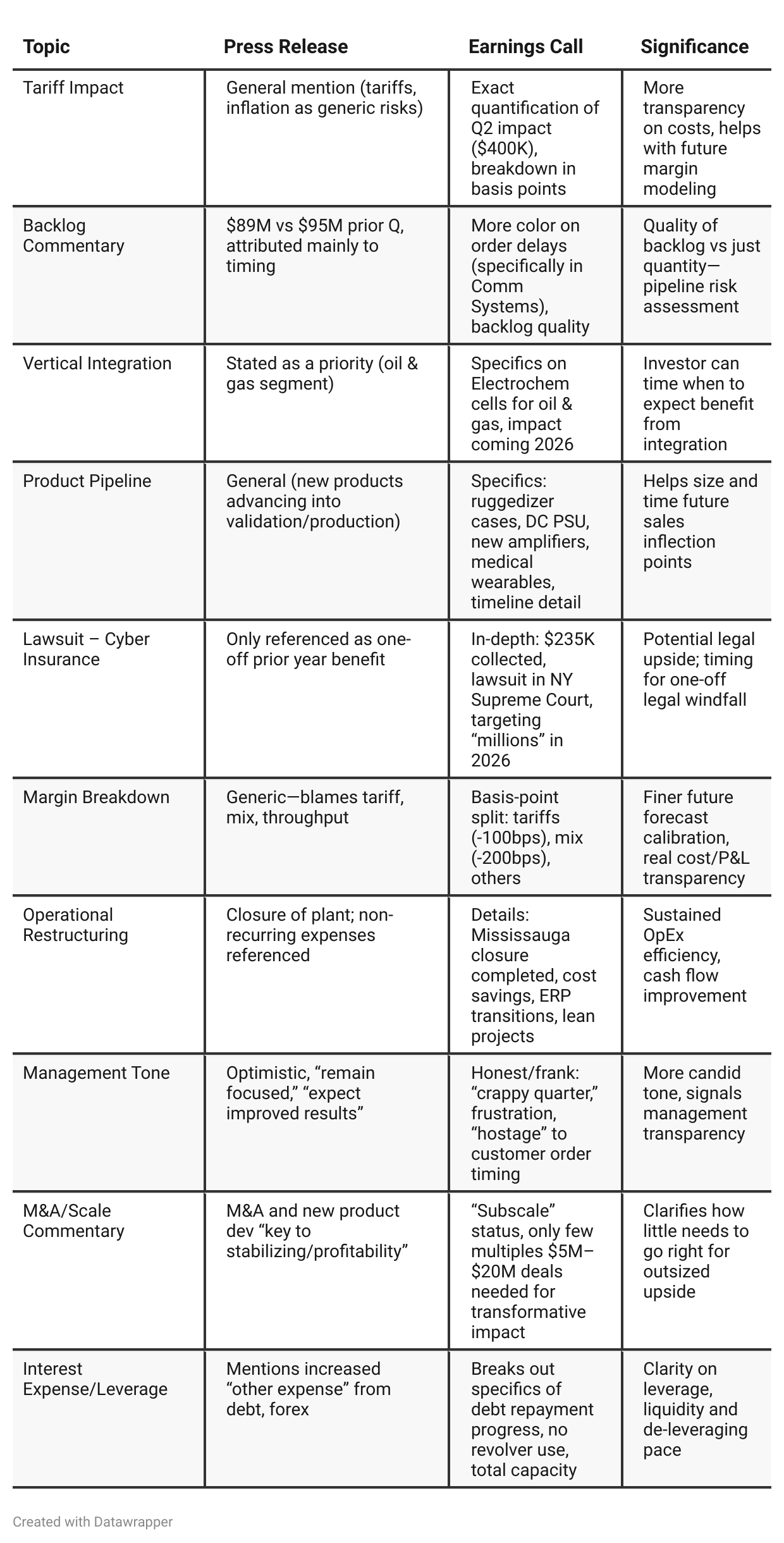

Press Release vs Call Transcript Comparison

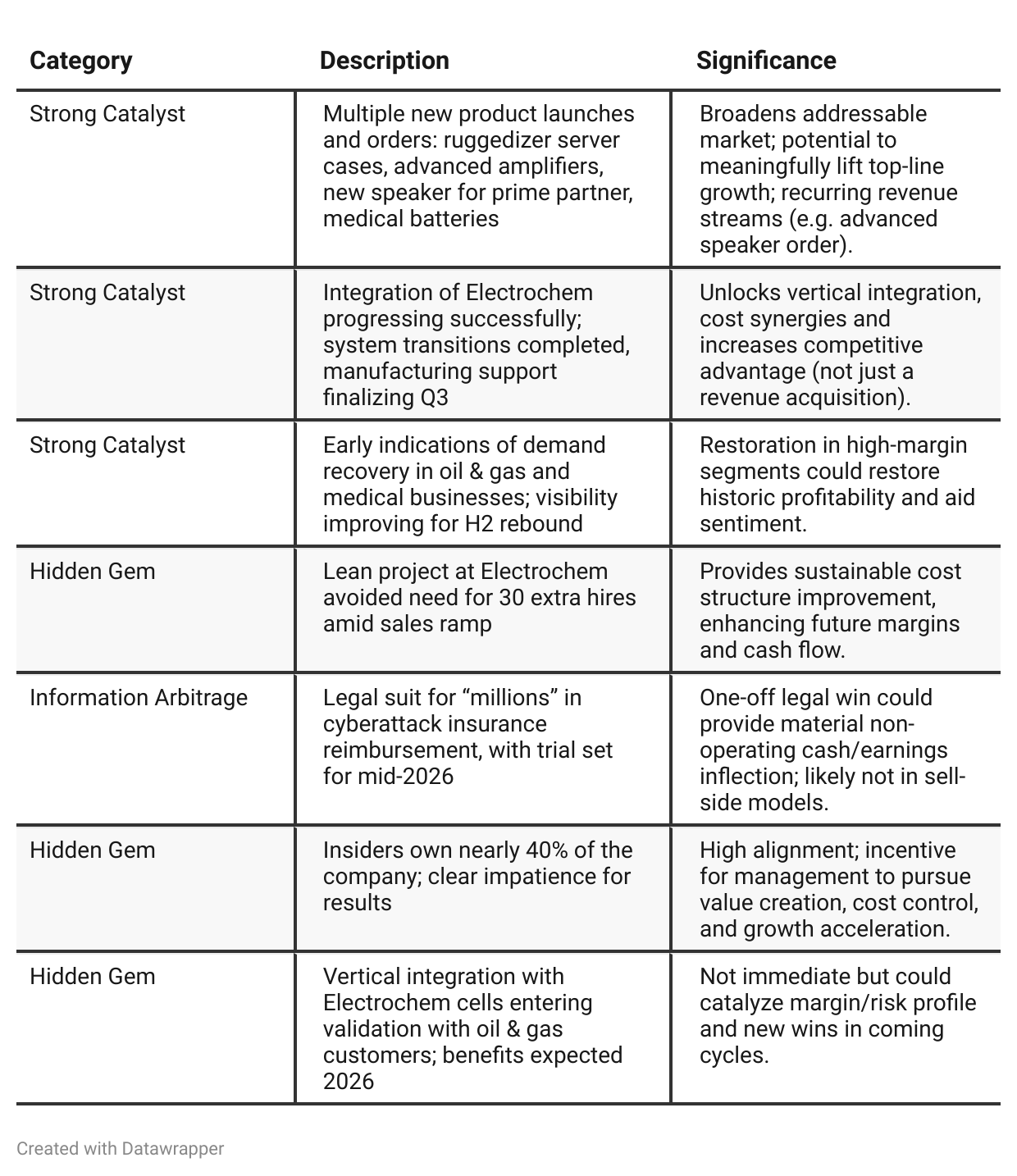

Working capital and liquidity remain strong; paid down more debt than required in H1 2025—a positive for financial resilience.

Management is passing tariff surcharges to customers where possible; suggests some pricing power and customer stickiness.

Several product development cycles still in pre-revenue qualification; risk of continued lag, but consistent pipeline filling.

Company’s insider shareholders own close to 40%—alignment with outside investors.

Enhanced focus on targeted marketing and digital lead-gen for funnel building; early positive feedback.

The pace of converting R&D investment and customer qualifications into recurring revenue will determine valuation sensitivity.

Legal risk/upside: material, but with long lead time before resolution (2026).

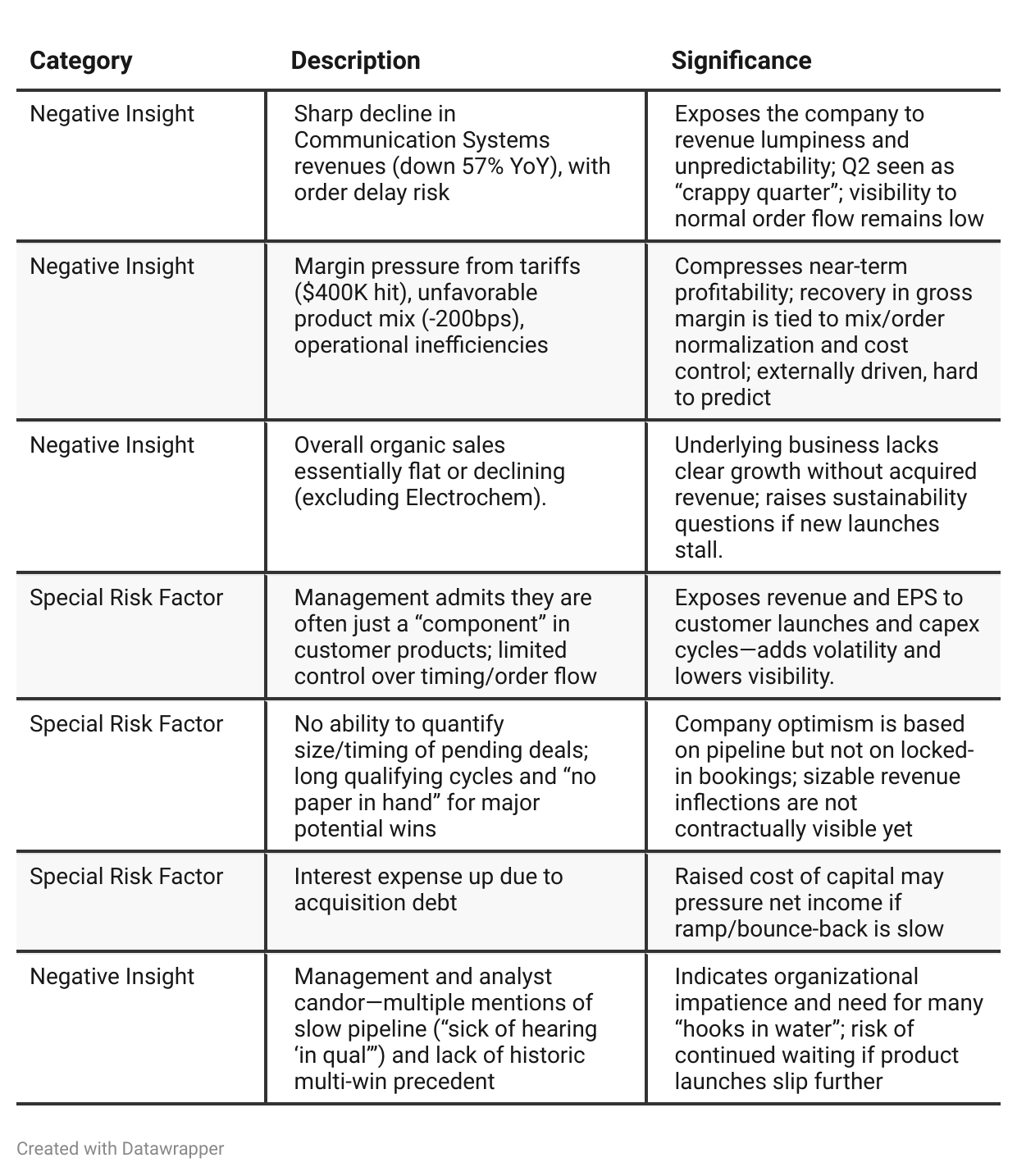

The business is highly leveraged to volume and mix; relatively small shifts in customer order timing or wins can result in sharp EPS swings.

Positive Insights

Negative Insights

Tariff Risk

Tariffs had a direct $400,000 hit to Q2, costing ~100bps of margin, with the brunt due to bad timing of peak China import rates.

Management reports these impacts are “fluid,” and while not expecting another Q2-like spike, there is ongoing risk as tariff regimes can change unpredictably.

The company is passing surcharge costs to customers where possible, but notes that not all surcharge can be recovered, and some customer cash flow is stretched by tariffs, raising risk of customer order hesitancy.

The impact of tariffs is notably visible in the margin and order flow, particularly for components needed on fixed delivery schedules.

Sentiment Analysis

The overall sentiment for Ultralife Corporation is cautiously bullish. Investors acknowledge the recent weak earnings report, highlighting concerns over margins, product mix, and lack of organic growth, and some express diminished confidence in management's visibility. However, there is also notable optimism: director insider buying is repeatedly highlighted, the stock has rebounded sharply, and several investors mention holding or adding to positions, expecting a second-half rebound fueled by sector recovery and new product contributions. Technical chart watchers and sector momentum add to the positive tone, with some seeing post-earnings weakness as a buying opportunity. Thus, sentiment leans bullish, tempered by awareness of near-term risks.

Previous Earnings Call

Quarter-over-quarter comparison

Ultralife began 2025 on the front foot following the full incorporation of Electrochem, expressing confidence in organic and acquired growth, product launches, and margin enhancements through cost control and integration. Management maintained an optimistic tone, expecting short-term medical sales softness to rebound and seeing stable defense demand and a robust backlog. As the year advanced into Q2, however, hopes ran into tangible macro and micro headwinds: sharp declines in key segment sales, significant margin pressure from tariffs and product mix, and a blunt admission that order and revenue timing hinged heavily on customer cycles beyond their control. The tone shifted from confident and constructive to candid and somewhat frustrated—while the pipeline remains substantial and the long-term opportunity set is broad, management acknowledged the wait for material wins is dragging on, patience within the company is wearing thin, and visibility is low despite a focus on operational discipline. The result is a narrative transition: from a story of robust operational progress poised to unlock scalable growth to one of resilience and realism about near-term volatility, external dependency, and the need for patient execution before upside can be realized.Year-over-year comparison

Q2 2024: Ultralife emerges from a period of transformation with strong operational momentum: improving margins, growing diversified sales, focused cost discipline, and prudent debt reduction. Excitement builds around a growing product pipeline—in particular, medical and oil & gas opportunities. The company projects optimism, seeing successful execution on key priorities as a proof point for further growth and margin expansion.

Q2 2025: Despite increased sales (due to acquisition), the company faces meaningful, largely external setbacks. Tariffs, unfavorable product mix, and timing of major orders (in medical, oil & gas, and defense) compress profits and margins. Leadership is candid about the quarter's disappointment but reiterates confidence in their long-term strategy—emphasizing continued investment in new products, deeper vertical integration, and building a robust pipeline of large, diversified growth opportunities. The narrative shifts from celebrating sequential gains to explaining near-term setbacks and reinforcing the rationale for patience: “We’ve done the right things, invested for the future; some things take longer, but big wins are feasible if even a few of these bets land.”

Final Takeaway

Ultralife Corporation is in a transitional phase, balancing operational streamlining and new product launches with near-term margin/revenue volatility after a difficult Q2. Management is focused on growth, cost controls, and extracting value from recent acquisitions—yet, substantive upside depends on multiple customer wins and improvements in product mix and margin. Investors should watch for concrete evidence of commercial wins and backlog expansion in the coming quarters. Verdict: Hold, with potential upside if and when new business milestones materialize.