T2 Biosystems, Inc. (OTCMKTS: TTOO) – Q3 2024 Earnings

T2 Biosystems, Inc. (OTCMKTS: TTOO) – Q3 2024 Earnings

Earnings Release Date: Nov. 14, 2024

Stock Price: $0.55

Market Cap: $9.8 million

Q3 2024 sales of $2.0 million vs $1.4 million in the prior year

Q3 2024 EPS of ($0.57) vs ($3.45) in the prior year

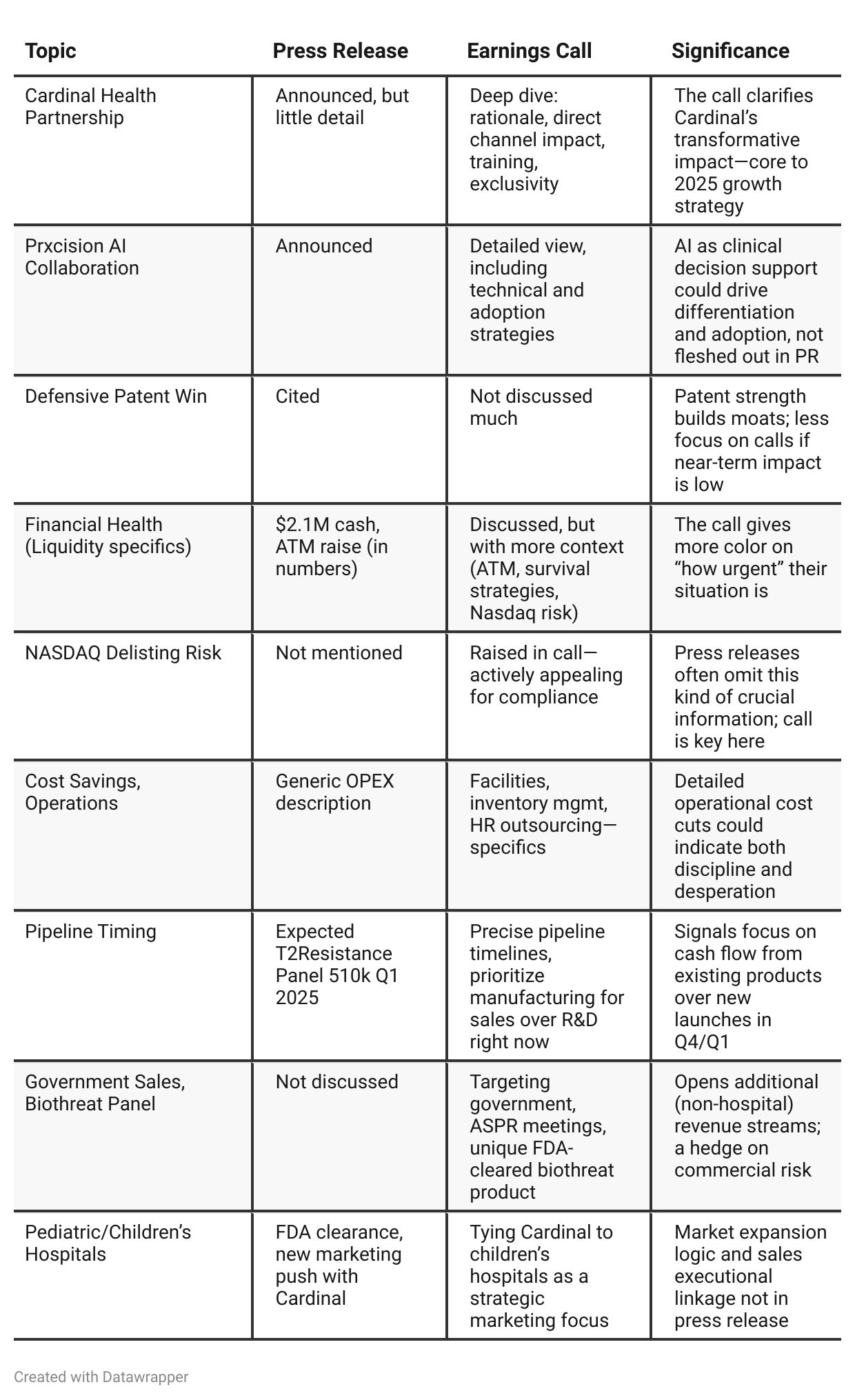

Press Release vs Call Transcript Comparison

The biggest difference is context and urgency: The earnings call provides far more nuance about why channel and partnership deals are so critical right now for T2’s business model and survival.

The pipeline is robust, but execution is now front and center: Management’s risk seems less about innovation and more about reaching scale before financing options close off.

Investors should pay close attention to the actual near-term sales ramp with Cardinal and Prxcision, not just the existence of those deals.

Real estate and HR cost-cutting moves demonstrate discipline, but also underscore that the company is seeking every dollar of savings to extend runway.

The press release gives strong headline numbers, but only the call discusses the extent and risk of the NASDAQ listing threat and the potentially dilutive or existential financial challenges.

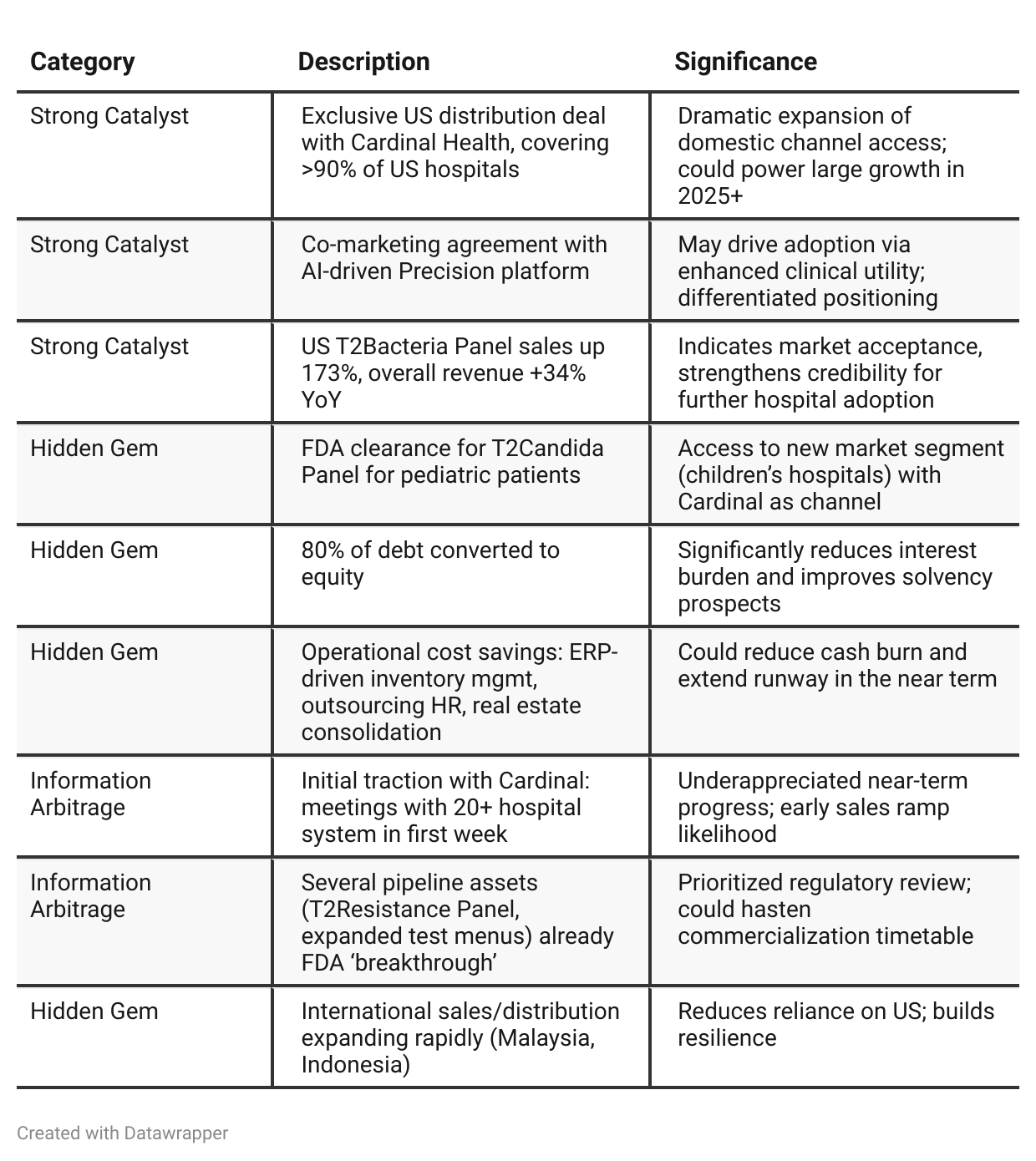

Positive Insights

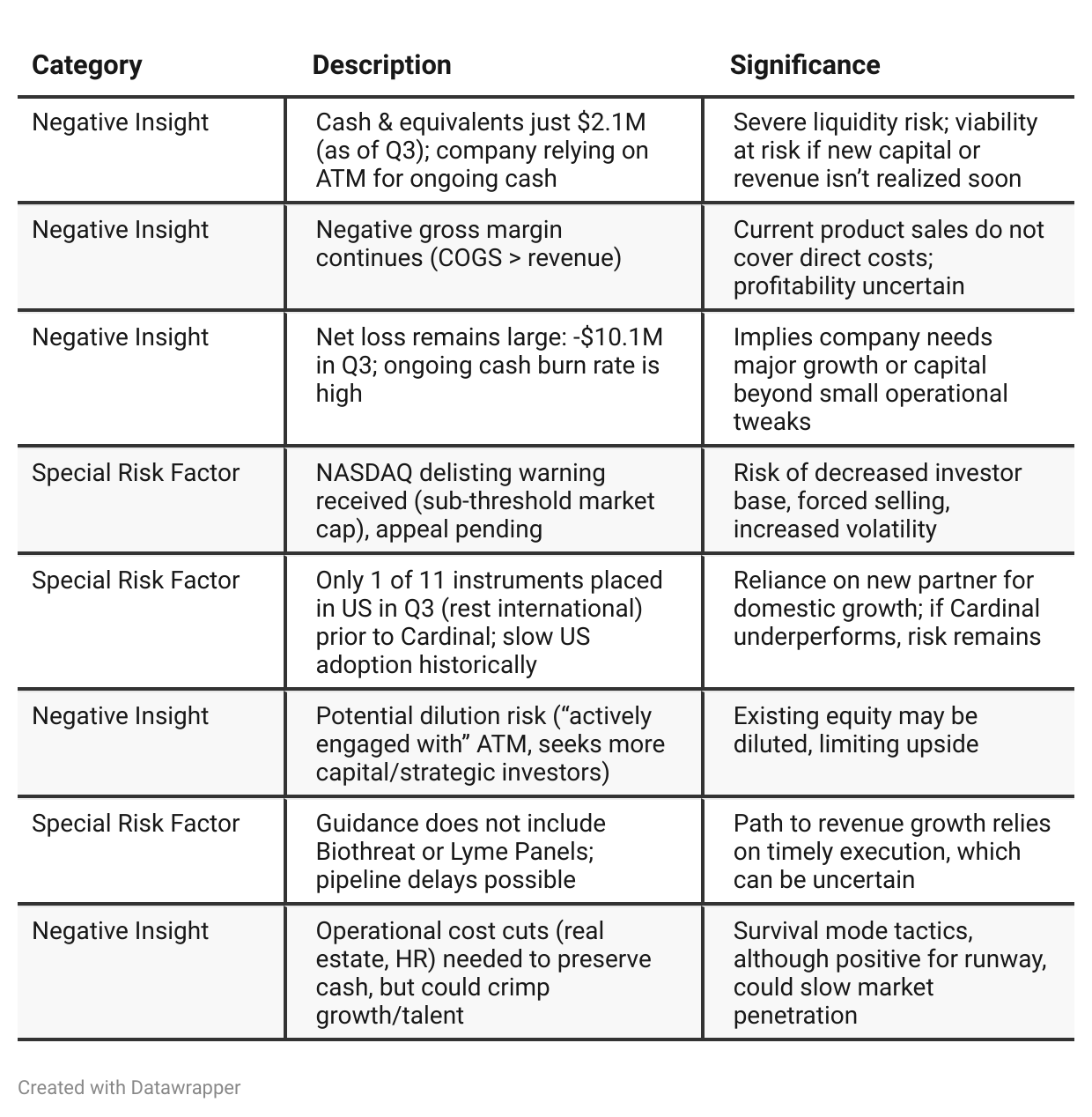

Negative Insights

Tariff Risk

No mention of US tariffs or trade policies in the transcript. The company neither highlighted tariff-related risks nor any mitigation strategies. Its supply chain, revenue, and profitability outlook are described without reference to tariffs or trade policy impacts. Investors should nonetheless remain alert for any future commentary, particularly if international sales or sourcing increases.

Sentiment Analysis

The overall sentiment toward T2 Biosystems (TTOO) is bearish. Most comments are negative, focusing on the stock’s poor performance, doubts about the company’s future prospects, and comparisons to failed companies. While there are a couple of isolated bullish opinions about potential acquisitions or price surges, the prevailing tone is skeptical and highly critical, suggesting that investors generally expect further declines or have little confidence in a turnaround.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q2 and Q3 2024, T2 Biosystems has shifted from a phase of cautious groundwork and cost discipline, focused on surviving and building optionality, to one of more ambitious scaling efforts, unlocked by a transformative distribution agreement with Cardinal Health. While the company’s core themes remain—sepsis as a massive, underdiagnosed burden and the inadequacy of blood culture diagnostics—its narrative has evolved. In Q2, the discussion revolved around navigating uncertainty, capital discipline, and pipeline preparation, with a commercial partnership still hypothetical. By Q3, the conversation becomes more outward-facing and opportunistic: the partnership is real, the market access is immediate, and the company speaks about revenue acceleration and scaling across new hospital segments. Financial caution and risk management persist, but the message is now about execution, adoption, and inflection, not just survival.Year-over-year comparison

In Q3 2023, T2 Biosystems was in “diagnostic survival mode.” The company was focused on operational fixes, clearing product backlogs, and defending its NASDAQ listing through a reverse split, while touting a few regulatory and customer-driven wins. The tone was pragmatic and resilient, with innovation ambitions balanced against the pressing need to overcome manufacturing and revenue headwinds.

By Q3 2024, the narrative shifts to one of “strategic inflection.” Armed with an exclusive, large-scale US distribution partnership (Cardinal Health) and new product extensions (AI platform, pediatric, pipeline trials), T2 is more growth-oriented and opportunistic. While financial and capital risks remain high, management’s messaging has moved from incremental improvement and maintenance to seizing large channel and portfolio opportunities, emphasizing the pathway to an eventual scaling story—if execution on recent partnerships and cash management succeeds.

Final Takeaway

T2 Biosystems is in a high-risk turnaround phase, betting on channel expansion (Cardinal Health) and new product launches to break out of survival mode. While catalysts are significant—including potential game-changing US hospital access and AI-driven adoption—liquidity risks, negative margins, and delisting overhangs are immediate. Investors should closely watch for Cardinal-driven revenue ramp and capital raises. Execution over the next two quarters will define the company’s path. Verdict: HOLD (Speculative); trajectory highly dependent on external partner performance and funding solutions.