Tetra Tech, Inc. (NASDAQ: TTEK) – Q3 2025 Earnings

Tetra Tech, Inc. (NASDAQ: TTEK) – Q3 2025 Earnings

Earnings Release Date: Jul. 30, 2025

Stock Price: $37.54

Market Cap: $9970.2 million

Q3 2025 sales of $1,370 million vs $1,344.3 million in the prior year

Q3 2025 EPS of $0.43 vs $0.32 in the prior year

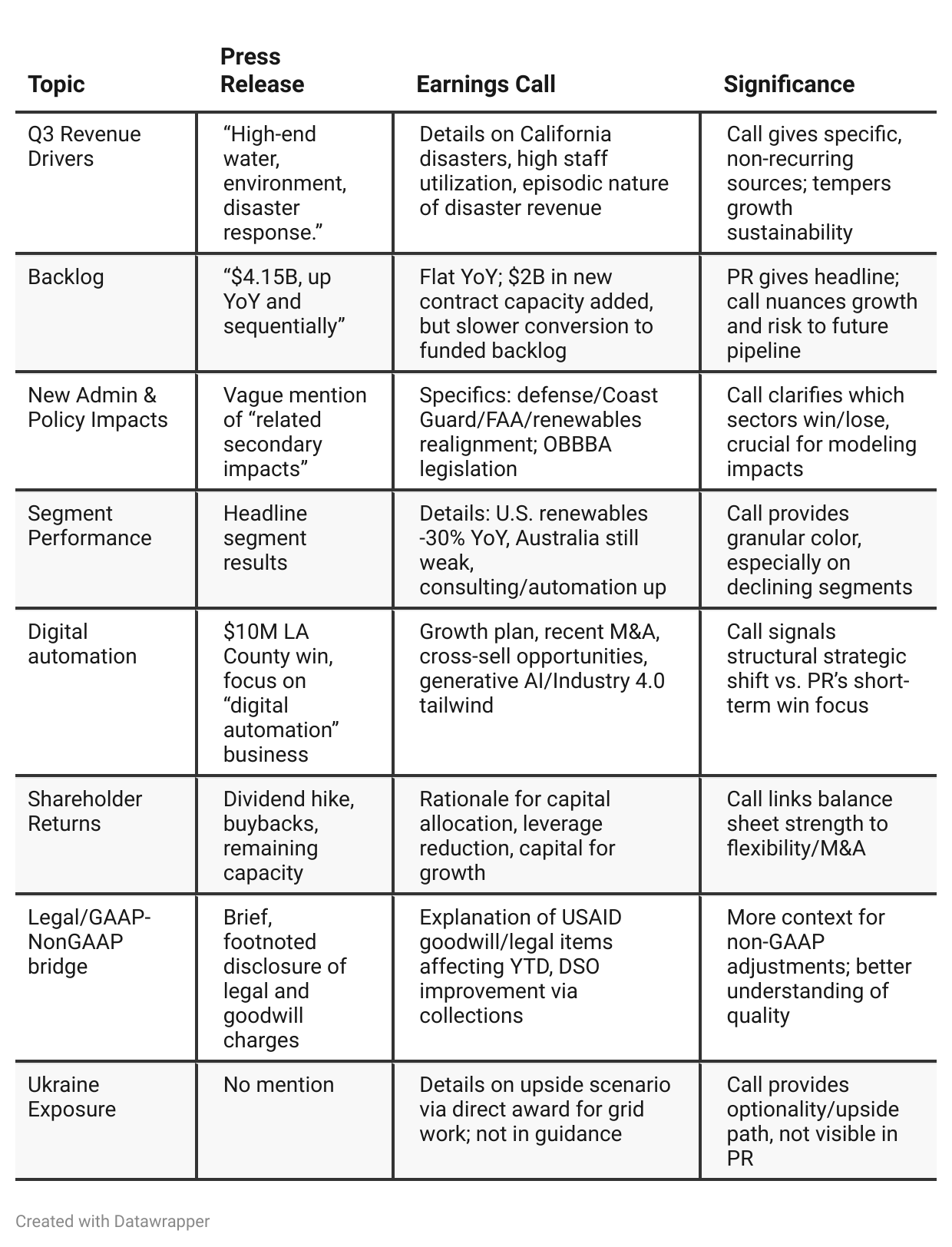

Press Release vs Call Transcript Comparison

The call emphasizes management’s confidence in navigating volatile policy environments and their ability to pivot resources.

“Higher margin” focus (consulting, digital, fixed price) is a major positive, but sustainability needs monitoring as episodic work normalizes.

Book-and-burn dynamic means investors may need to be comfortable with less “backlog visibility,” even as near-term revenue flows.

New U.S. administration’s policies are acknowledged as both challenge (renewable headwinds, funding bureaucratic friction) and opportunity (defense, automation).

International growth is nuanced—region-by-region divergence: UK/Ireland/Canada are strong (water focus); Australia is a continued drag.

Shareholder returns (dividends, buybacks) are explicitly linked to improved cash conversion, margin progress, and leverage reduction, providing some buffer for investors.

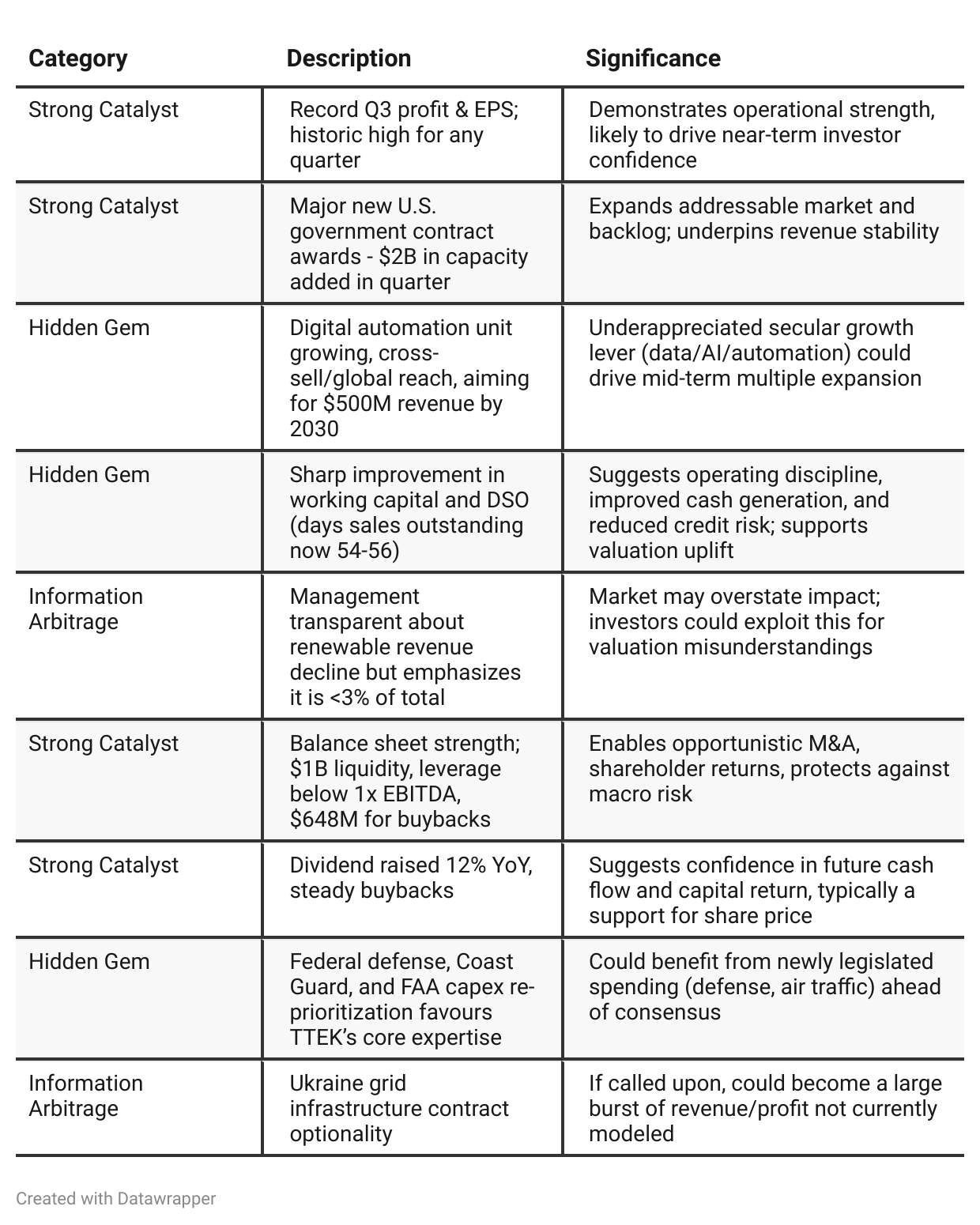

Positive Insights

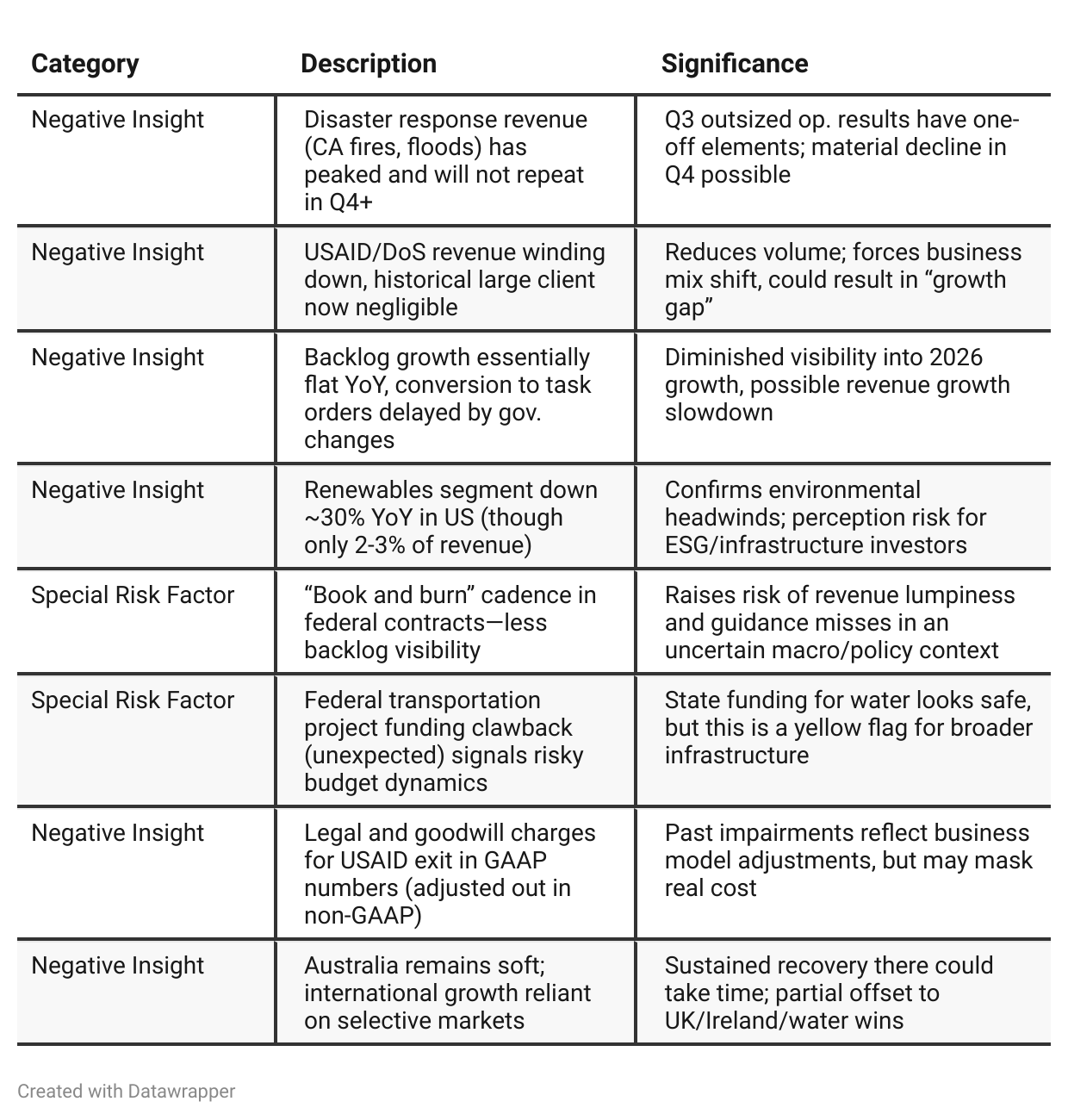

Negative Insights

Tariff Risk

No discussion of tariffs or trade policy impacts in the call.

Tetra Tech’s business—driven by U.S. government and allied country contracts—shows no current exposure to U.S. tariffs or international trade disruptions per management’s commentary.

No supply chain adjustments, pricing changes, or loss of competitive position due to tariffs were mentioned.

No forward-looking statements about tariffs or global trade obstacles.

Previous Earnings Call

Quarter-over-quarter comparison

Q2 2025 Story: Tetra Tech faced a “shock test” with the near-total loss of its largest historical client (USAID). Rather than retrench, the company delivered record revenue and profits due to service diversity, strong state/local and defense wins, and an uptick in digital/data center growth. Management focused on transparency, structural margin improvement, and capital return (buybacks, dividends), aiming to reassure investors their business model is durable and poised for growth—even after losing a legacy revenue source.Q3 2025 Story: The shock phase has passed; execution has been proven. Management is now more focused on explaining the new phase: sustaining margin, managing one-off windfalls (like disaster response), and preparing for a volatile federal contract market where visibility is lower and backlog conversion is less predictable. Strategic focus is shifting toward aligning with new government priorities (defense/FAA/Coast Guard), expanding digital automation, and maintaining capital discipline. While underlying demand for water/infrastructure remains, TTEK is no longer simply “proving resilience”—the message is now, “we’re capable, but so is the external environment, so manage your expectations accordingly.”

Year-over-year comparison

In Q3 2024, Tetra Tech’s narrative was of outperformance and multi-pronged growth, driven by robust demand for water, environmental, and high-tech infrastructure consulting. Management stressed strategy, high-margin service mix, and conservative discipline in reporting. Risks were framed as manageable or exploitable.

By Q3 2025, the story is one of transition. The company is coming off a record (but partly one-time) quarter, forced to navigate a dramatically changed U.S. government contracting environment. Messaging pivots to explaining the nonrecurring nature of some wins, managing for less predictable revenue visibility, and focusing on margin/cash discipline. Core strengths remain—particularly in water, public infrastructure, digital automation, and capital allocation discipline—but management signals to investors that coming quarters may bring more uneven results as secular drivers eventually replace episodic windfalls.

Final Takeaway

Tetra Tech is in a transitional phase, shifting from one-off government windfall work (disaster, USAID) toward higher-margin consulting and digital automation, supported by a fortress balance sheet and substantial new contract wins. While secular demand (water, infrastructure, automation) is robust and new US policy presents opportunities, near-term comparables will soften as episodic disaster/USAID revenue fades. Consistent execution on core margin improvement, conversion of new contract capacity, and visibility into post-2025 growth are pivotal for re-rating. Verdict: HOLD, with upside contingent on confirming durable growth beyond one-off revenue sources.