Trex Company, Inc. (NYSE: TREX) – Q2 2025 Earnings

Trex Company, Inc. (NYSE: TREX) – Q2 2025 Earnings

Earnings Release Date: Aug. 4, 2025

Stock Price: $63.42

Market Cap: $6800.3 million

Q2 2025 sales of $$388 million vs $376 million in the prior year

Q2 2025 EPS of $0.73 vs $0.80 in the prior year

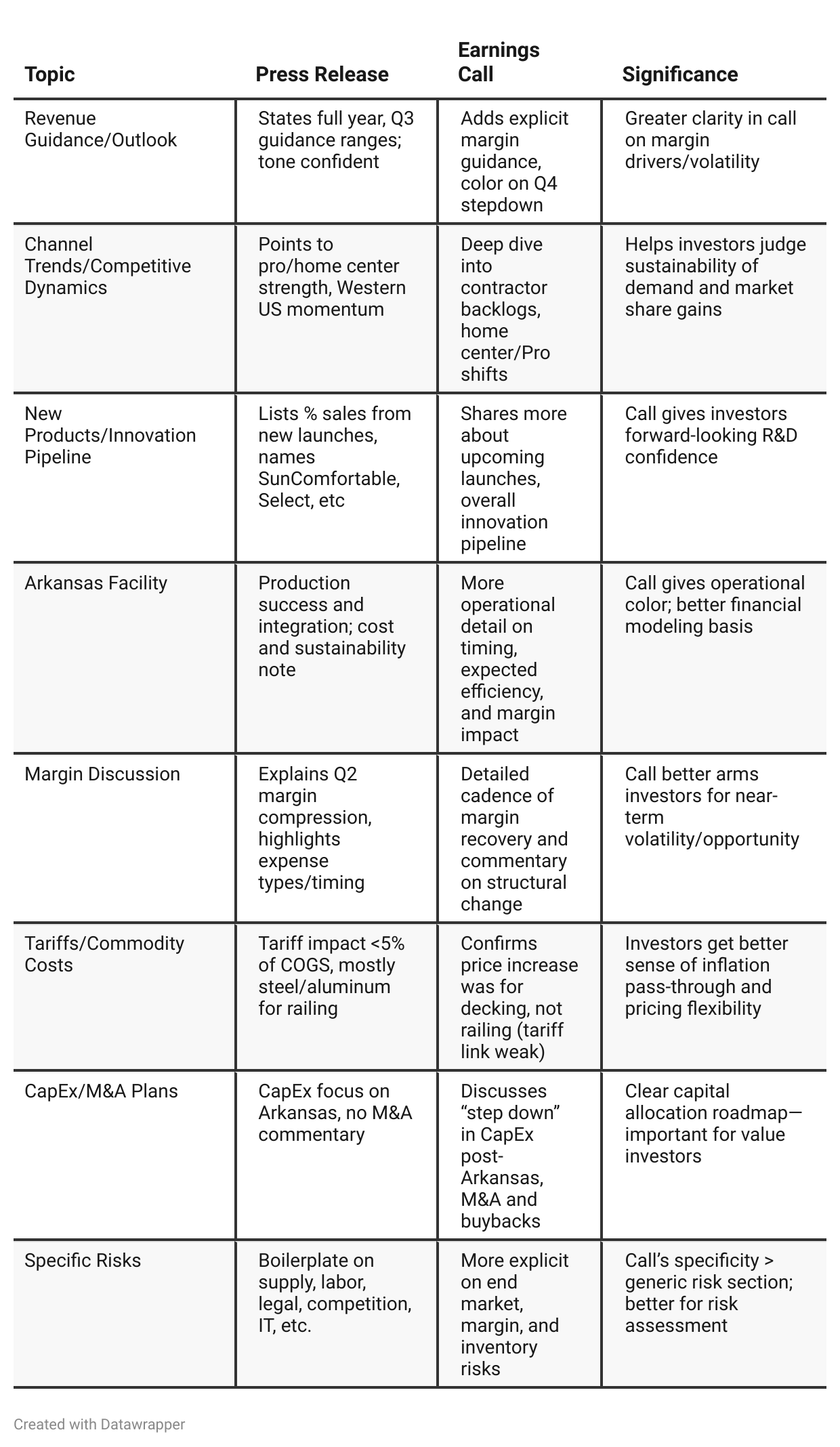

Press Release vs Call Transcript Comparison

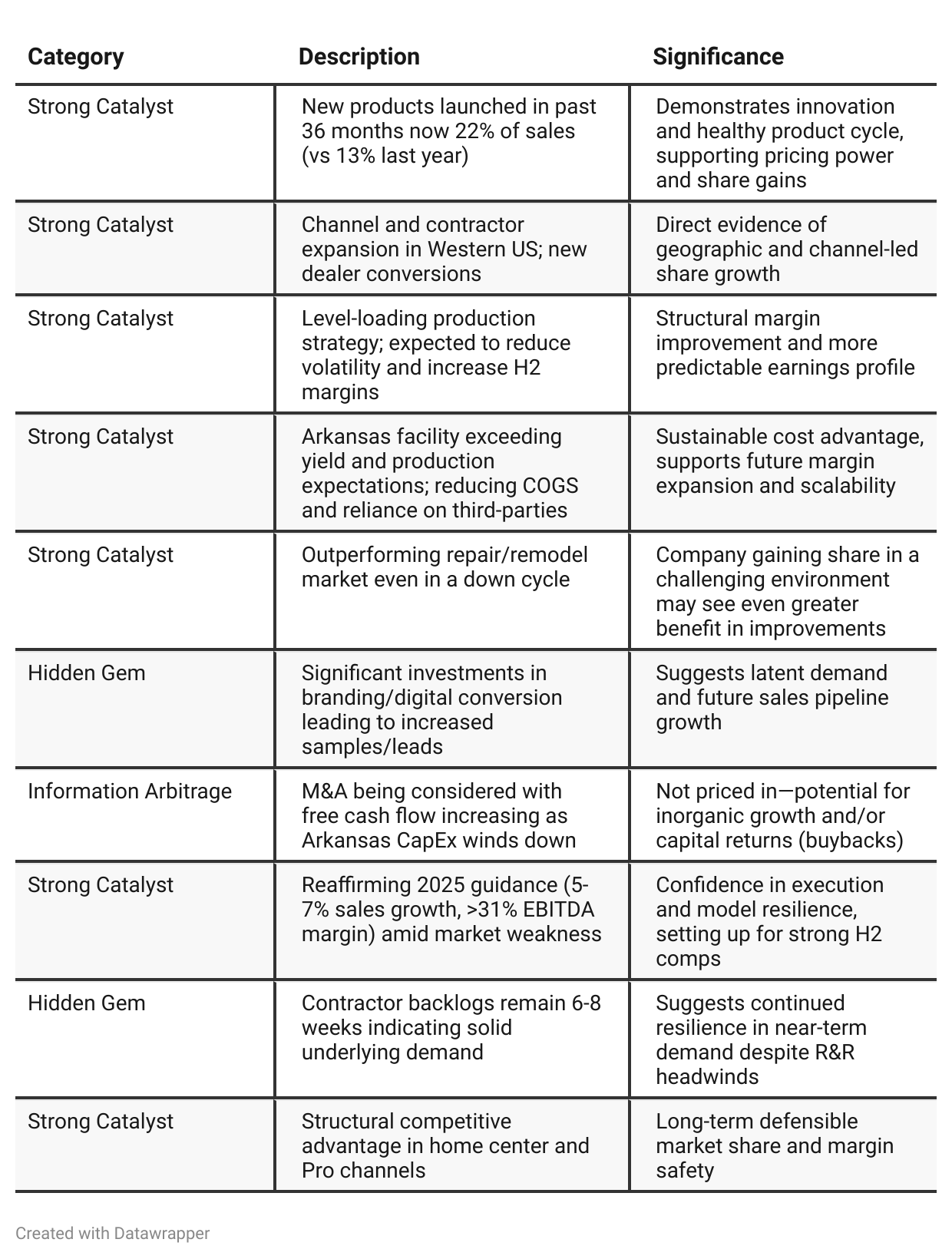

Call delivers more insight about capital allocation: Declining Arkansas-related CapEx in 2026+ should free up cash for share buybacks and potential M&A.

Multiple analysts probed margin cadence and end-market risk, underscoring investor concern about operational execution vs. topline optimism.

Market share gains from wood (170 bps last 18 months) are a major pillar of the growth story, and these trends are explained with more detail (including cyclicality at the low-end) in the call.

Management teams that describe specific execution strategies and demand drivers (channel conversion, operational efficiency) often enjoy more investor confidence.

Press release, by nature, is highly promotional; the call transcript is more "warts and all", revealing both tailwinds and headwinds.

Positive Insights

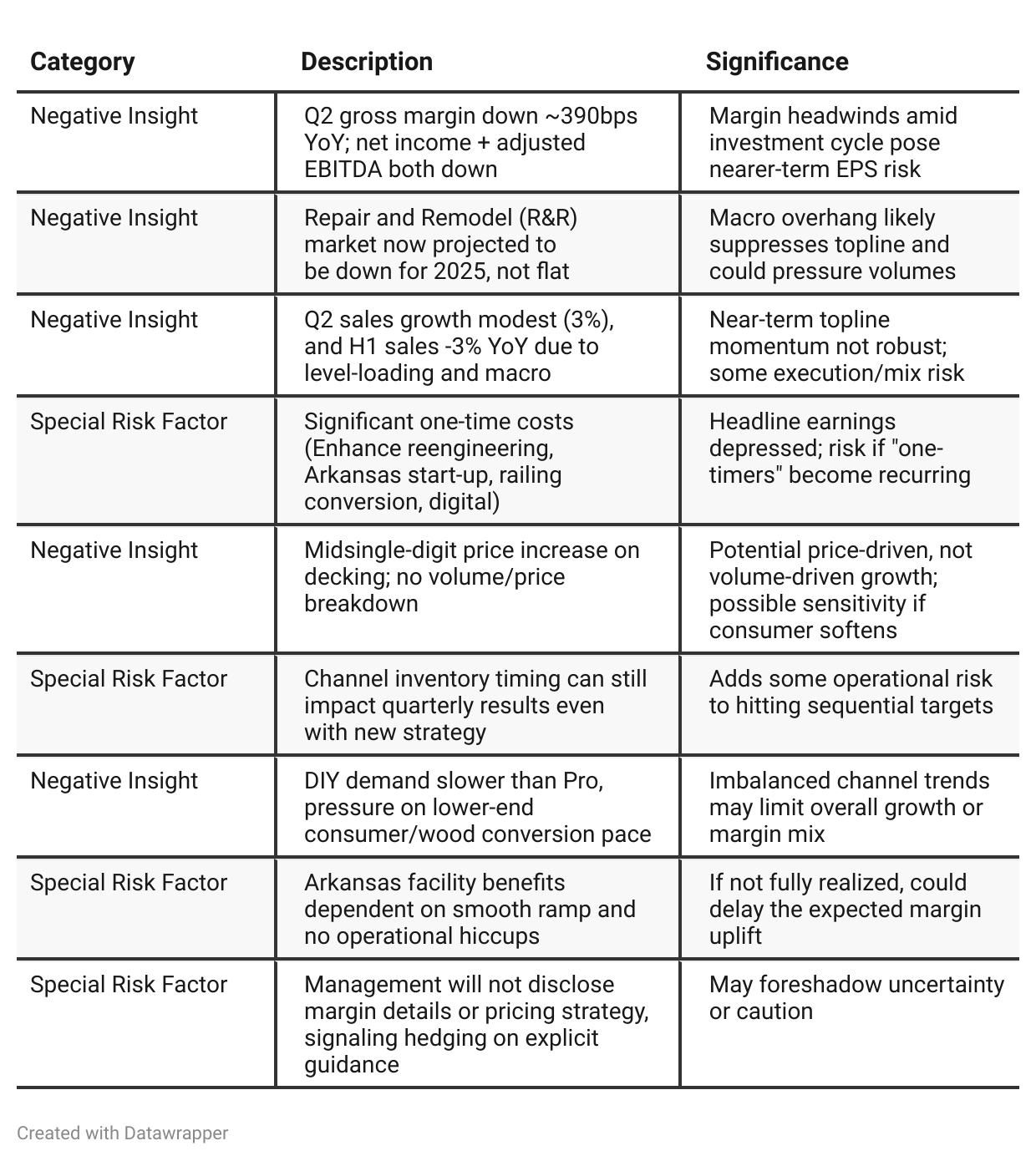

Negative Insights

Tariff Risk

Tariffs affect less than 5% of Trex’s cost of goods, mainly aluminum and steel for railing/fasteners—not core decking.

Trex raised prices on decking (not railing), using selective pricing to offset some cost pressures.

Additional mitigation: pre-buying materials, supplier negotiations, and operational shifts.

Management believes tariff impacts are “meaningfully mitigated”; no warning of major risk to margins, competitiveness, or innovation.

Bottom line: Tariff exposure is well-controlled and not a material risk to Trex’s outlook at this time. Investors should monitor, but current impact is minimal.

Previous Earnings Call

Quarter-over-quarter comparison

In Q1 2025, Trex’s narrative was one of tactical adaptation: explaining softer year-over-year comparisons due to channel and production normalization, and heavily emphasizing innovation and new product launches to fuel an expected second-half rebound. The company highlighted operational investments and strategic inventory management plans that had not yet fully materialized. There was a clear, if guarded, optimism: management saw “pent-up R&R demand” returning by 2027 and firmed up confidence in their channel presence and premium product focus.By Q2 2025, the narrative shifted to execution and resilience. Trex demonstrated its ability to outperform amid worsening end-market conditions and adverse weather, validating its strategic bets: level-loading production yielded operational benefits, contractor/channel strategies paid off with continued share gains, and the Arkansas facility exceeded internal targets. The tone is more measured—management is upfront about market contraction, but shows conviction that structural improvements and innovation will enable Trex to deliver on its guidance and position for margin/cash flow expansion.

Over this half-year, Trex moved from promising operational transformation to demonstrating early results, all while adjusting for a tougher market. The story is now about durable outperformance, visible margin levers, and post-capex capital flexibility, balanced by transparency on persistent macro risk and tempered near-term execution.

Year-over-year comparison

In Q2 2024, Trex’s narrative was about managing through broad-based consumer softness, inventory normalization, and executing on cost controls, with optimism pinned to the resilience of the premium buyer and faith in innovation and branding driving future growth. The message was: “The market is tough, but we’re investing and positioning for a rebound, staying ahead through innovation and efficiency.”

By Q2 2025, the company’s message is notably more mature and grounded. Trex acknowledges the market has worsened further, yet points to proven execution, citing record sales despite macro adversity. The narrative pivots to “results over promises,” with operational strategies (Arkansas, level-loading) demonstrating tangible payback, new products capturing a much larger sales mix, and smarter capital allocation setting up the next phase. The posture is less about weathering storms and more about structurally out-executing both the market and competitors, with an eye toward leveraging this position for future growth (M&A, buybacks) once macro turns. The tone is more self-assured but also refreshingly transparent about the magnitude and reality of headwinds.

Final Takeaway

Trex Company is in a transitional phase, pivoting from investment-heavy operations and macro headwinds to an anticipated margin and free cash flow expansion in the second half of 2025 and beyond. Key growth drivers—new product innovation, share gains, and improved manufacturing efficiency—are balanced by real risks from ongoing R&R market softness and legacy cost pressures. Investors should focus on the realization of margin leverage, demand durability as R&R stabilizes, and evidence that new channel/product strategies drive sustainable growth. Verdict: Hold—potential upside if execution on margin expansion and demand proves out, but wait for greater visibility/confirmation in the second half.