TechPrecision Corporation (NASDAQ: TPCS) – Q1 2026 Earnings

TechPrecision Corporation (NASDAQ: TPCS) – Q1 2026 Earnings

Earnings Release Date: Aug. 21, 2025

Stock Price: $5.32

Market Cap: $51.9 million

Q1 2026 sales of $7.4 million vs $8.0 million in the prior year

Q1 2026 loss per share of ($0.06) vs ($0.16) in the prior year

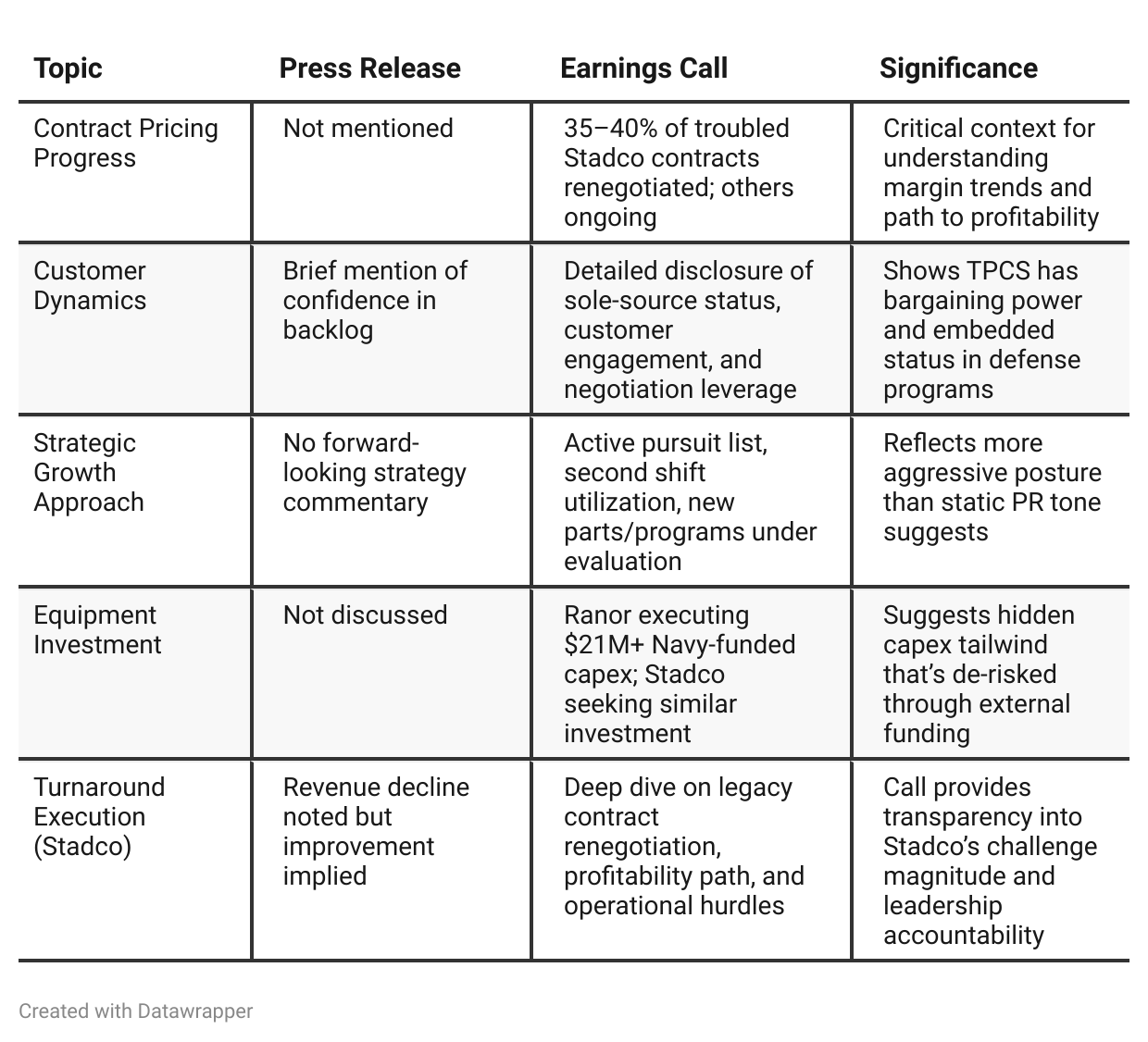

Press Release vs Call Transcript Comparison

While the press release paints a picture of gradual improvement anchored by margin expansion and a record backlog, the earnings call revealed a more nuanced reality: TechPrecision is still dealing with the fallout from its Stadco acquisition, fighting to renegotiate underpriced legacy contracts and working to stabilize cash burn. However, the call also introduced credible signs of forward momentum—namely, high-value sole-source contracts, pursuit of new business, and Ranor’s grant-funded capex build-out.

These disclosures, absent from the press release, provide greater investor clarity into both upside optionality and execution risks. For investors, the earnings call offered significantly more insight into the operational levers, culture shift, and real challenges than the press release alone.

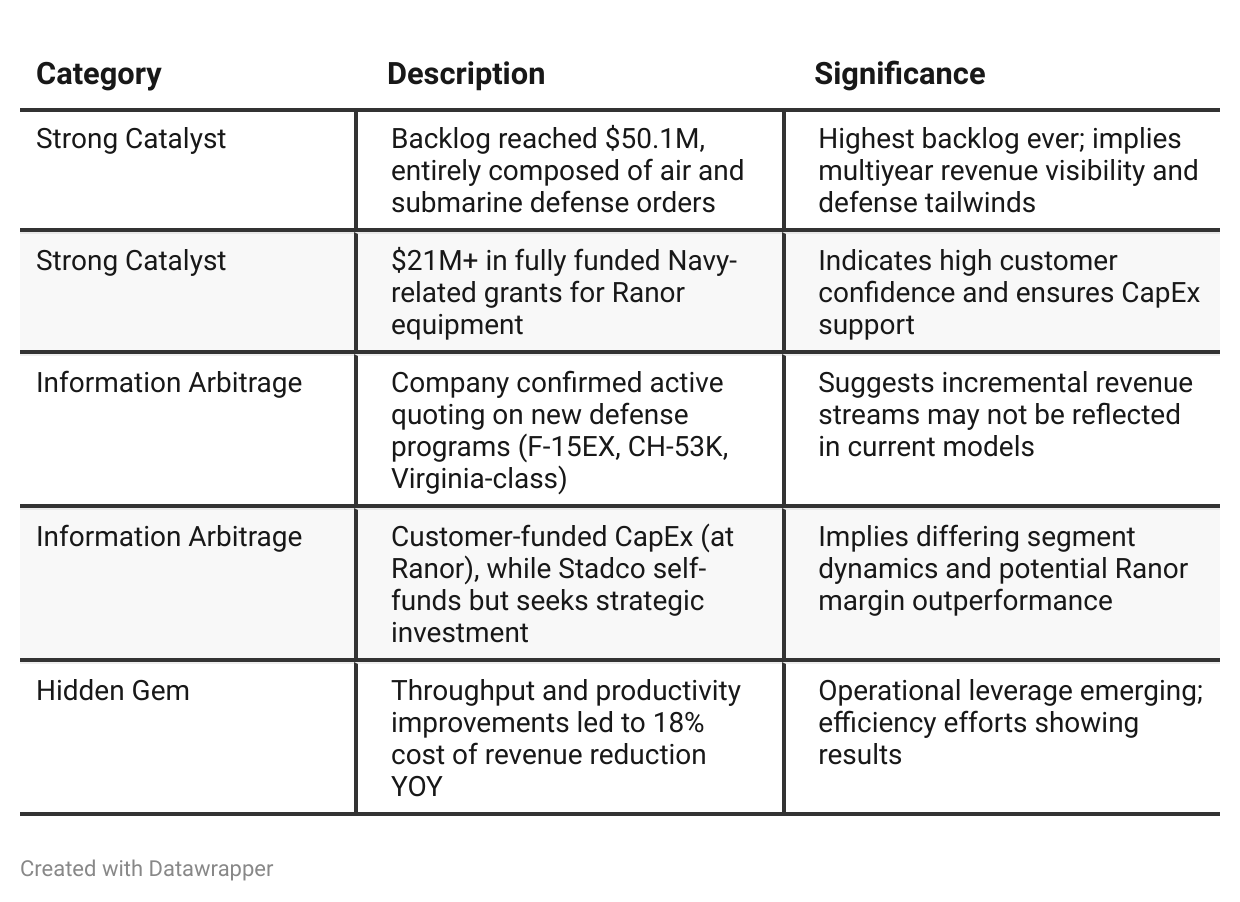

Positive Insights

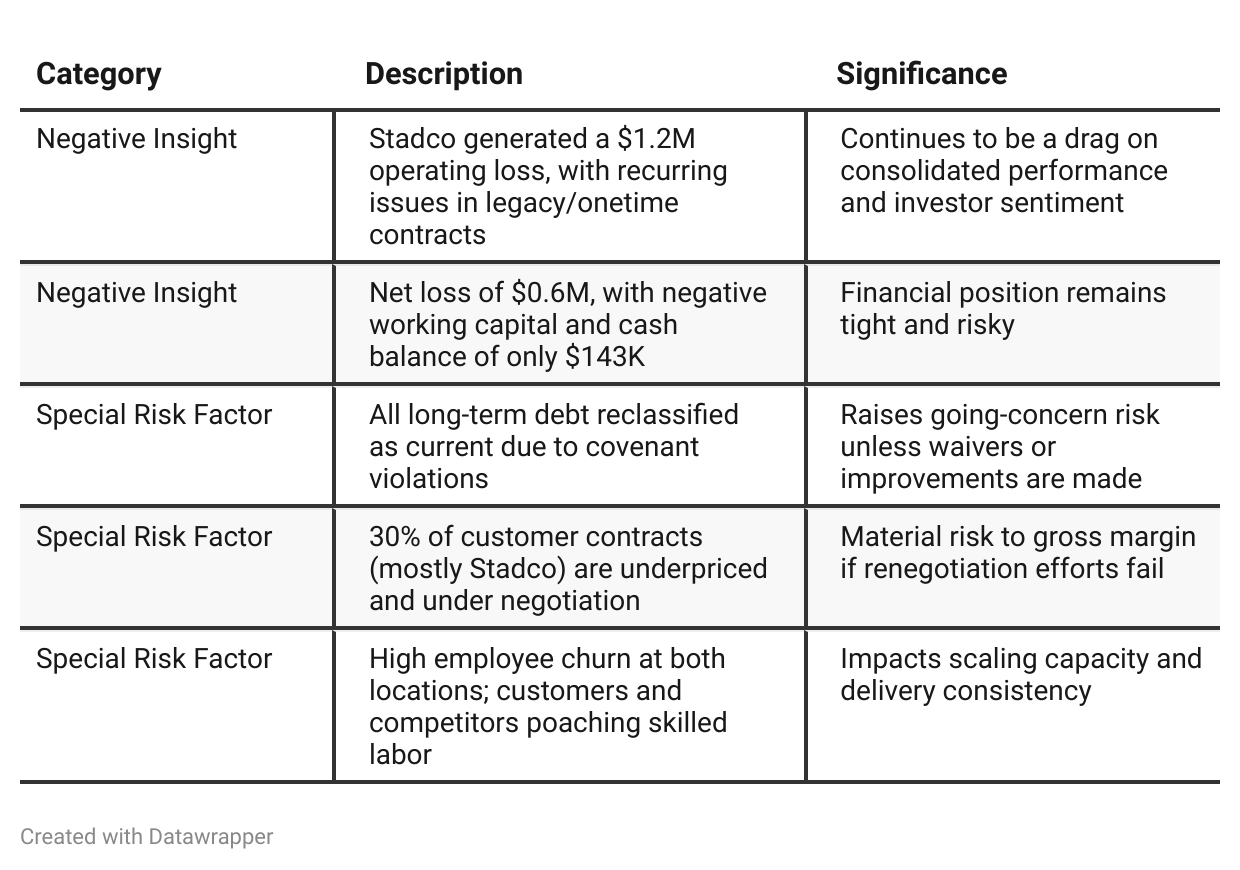

Negative Insights

Tariff Risk

No explicit mentions of tariffs or U.S. trade policy were made in the Q1 2026 call. However, given TPCS’s deep entrenchment in U.S. Navy and defense aerospace programs, it is insulated from international trade exposure. All strategic commentary centered on domestic defense manufacturing and supply chain bottlenecks related to customer-furnished materials (CFM). Thus, tariff risks are not material at this time.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q4 FY2025 and Q1 FY2026, TechPrecision’s narrative has shifted from cautiously celebrating an inflection point to engaging more deeply with the complexity of sustaining and scaling improvement—especially at Stadco. While the Q4 call was a milestone with its first Stadco profit and strong Ranor performance, the Q1 call reflected a more mature, transparent, and execution-focused tone.Management is now more open about the scope of Stadco’s issues (~30% problematic revenue), the risk of walking away from certain contracts, and the structural bottlenecks (labor, second shift capacity, CAPEX needs). However, customer trust, backlog momentum, and new quoting opportunities in defense offer clear tailwinds. The presence and influence of new CFO Phil Podgorski is notable—bringing pricing rigor, operational discipline, and improved communication with the Street.

In essence, Q4 was a proof-of-concept; Q1 reveals a leadership team determined to professionalize the business, break the $7–$8M quarterly revenue ceiling, and rebuild investor credibility with results, not promises.

Year-over-year comparison

In Q1 2025, TechPrecision was in defensive mode—reeling from the failed Votaw acquisition, dealing with broken Stadco equipment, and facing shareholder pressure. The messaging focused on damage control, limited disclosure, and no Q&A.

By Q1 2026, the company had shifted meaningfully toward recovery and transparency. Leadership acknowledged past missteps, gave concrete updates on contract renegotiations, and outlined a disciplined operational path forward. The CFO played a more prominent and professional role. Management demonstrated awareness of structural weaknesses (e.g., labor challenges, underutilized facilities), but also shared a tangible plan to unlock value through backlog execution, pricing corrections, and capacity expansion.

The overarching shift: From a company in triage to a company aiming to become operationally sound and investor-relevant.

Final Takeaway

TechPrecision is in a transition phase, stabilizing Ranor while restructuring Stadco. Management demonstrated improving operational rigor and backlog momentum—particularly in Navy and aerospace defense. However, Stadco remains an unresolved margin drag, and liquidity constraints limit near-term flexibility.

Execution on Stadco turnarounds and maintaining customer trust during contract renegotiations will determine the pace of earnings recovery.

Verdict: HOLD, with potential upside if gross margin recovery and top-line acceleration materialize in subsequent quarters.