Tantalus Systems (TSX:GRID) (OTC:TGMPF) – Q2 2025 Earnings

Tantalus Systems (TSX:GRID) (OTC:TGMPF) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $3.05

Market Cap: $165.8 million

Q2 2025 sales of $13.1 million vs $10.7 million in the prior year

Q2 2025 loss per share of ($0.02) vs ($0.02) in the prior year

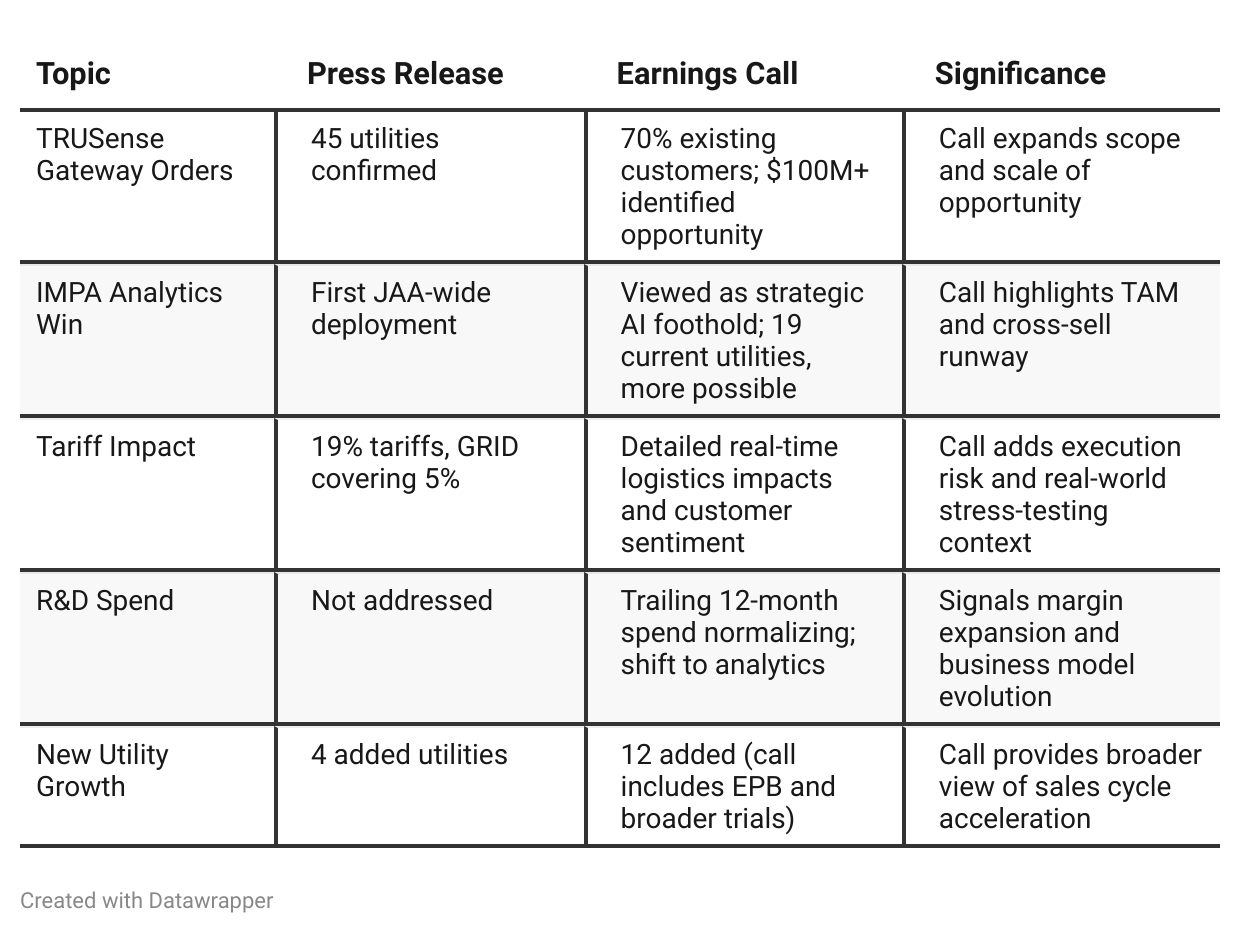

Press Release vs Call Transcript Comparison

The press release provides a strong snapshot of headline metrics and achievements, but the earnings call surfaces critical details that could meaningfully influence an investor’s view—especially around customer adoption behavior, tariff fallout, and the expanding software/data analytics strategy. The contrast in depth between the two documents highlights why call commentary is essential for understanding how a seemingly hardware-centric story is evolving into a platform-plus-analytics model with much greater margin potential and strategic value.

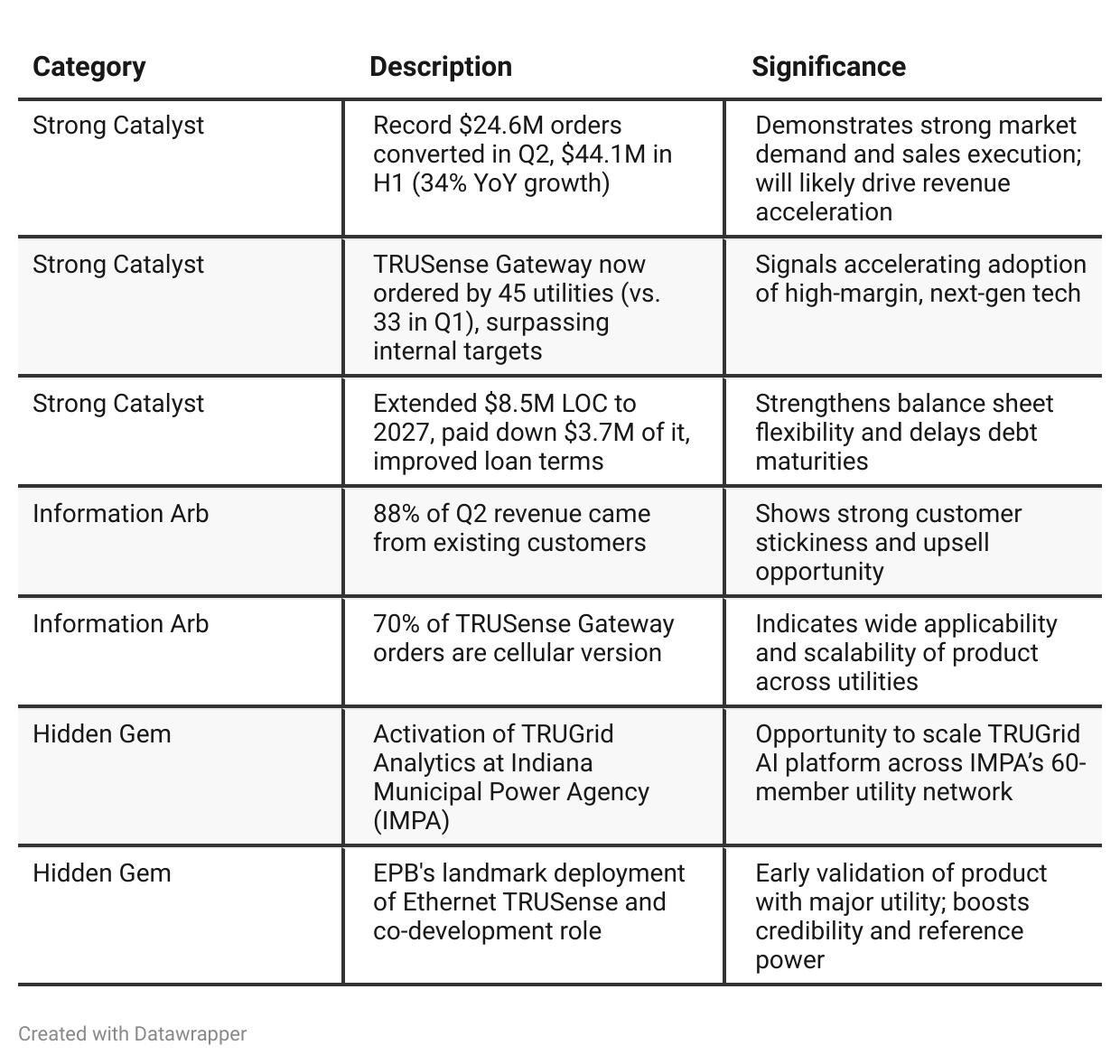

Positive Insights

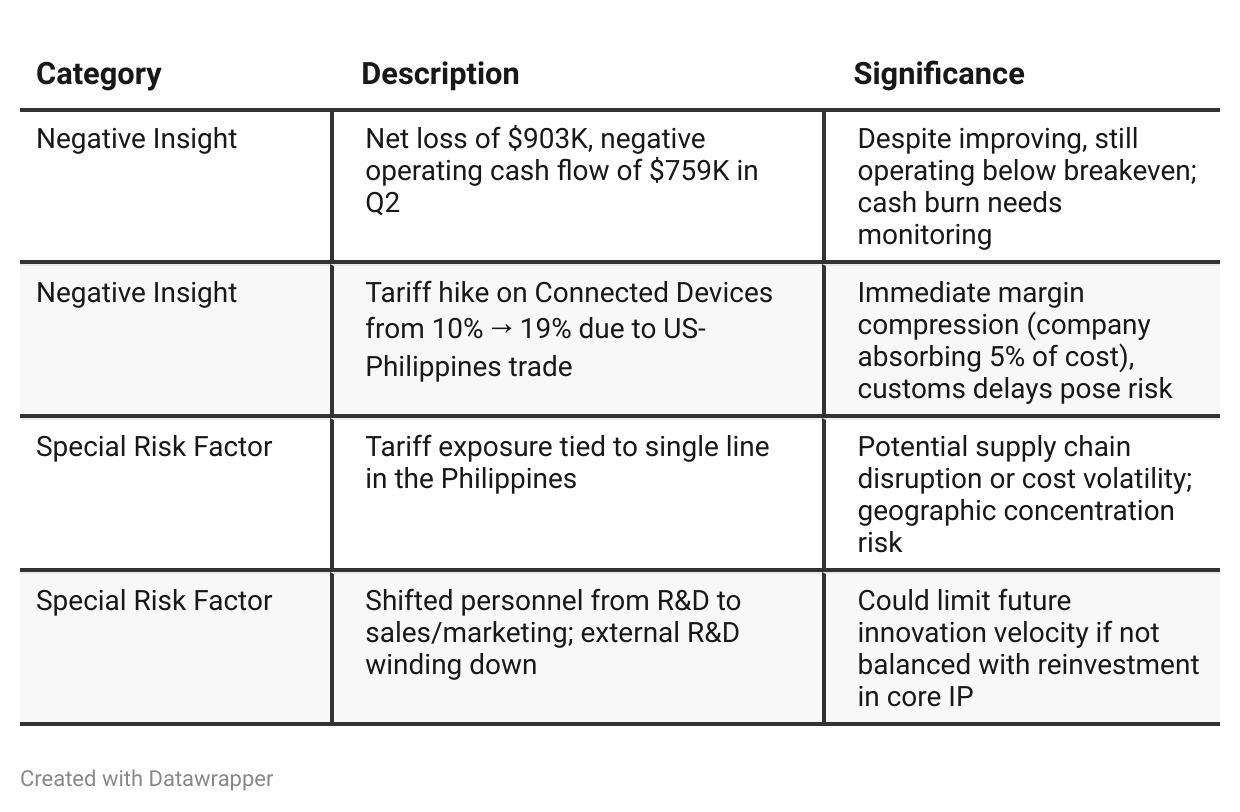

Negative Insights

Tariff Risk

Impact Summary:

Tariffs increased from 10% to 19% on Connected Devices imported from the Philippines (effective July 22).

Tantalus is absorbing 5% of the cost to support customers—near-term margin headwind.

Delays at customs due to logistical adjustments post-tariff.

Company evaluating second manufacturing location outside the Philippines, potentially in the U.S., to mitigate tariff risk and ensure supply chain resilience.

Strategic Mitigation:

Absorbing partial cost to retain long-term customers.

Highlighting TRUSense and TRUGrid as software-driven alternatives to expensive infrastructure deployments.

Tariff pressure may actually accelerate analytics adoption if utilities delay new hardware purchases.

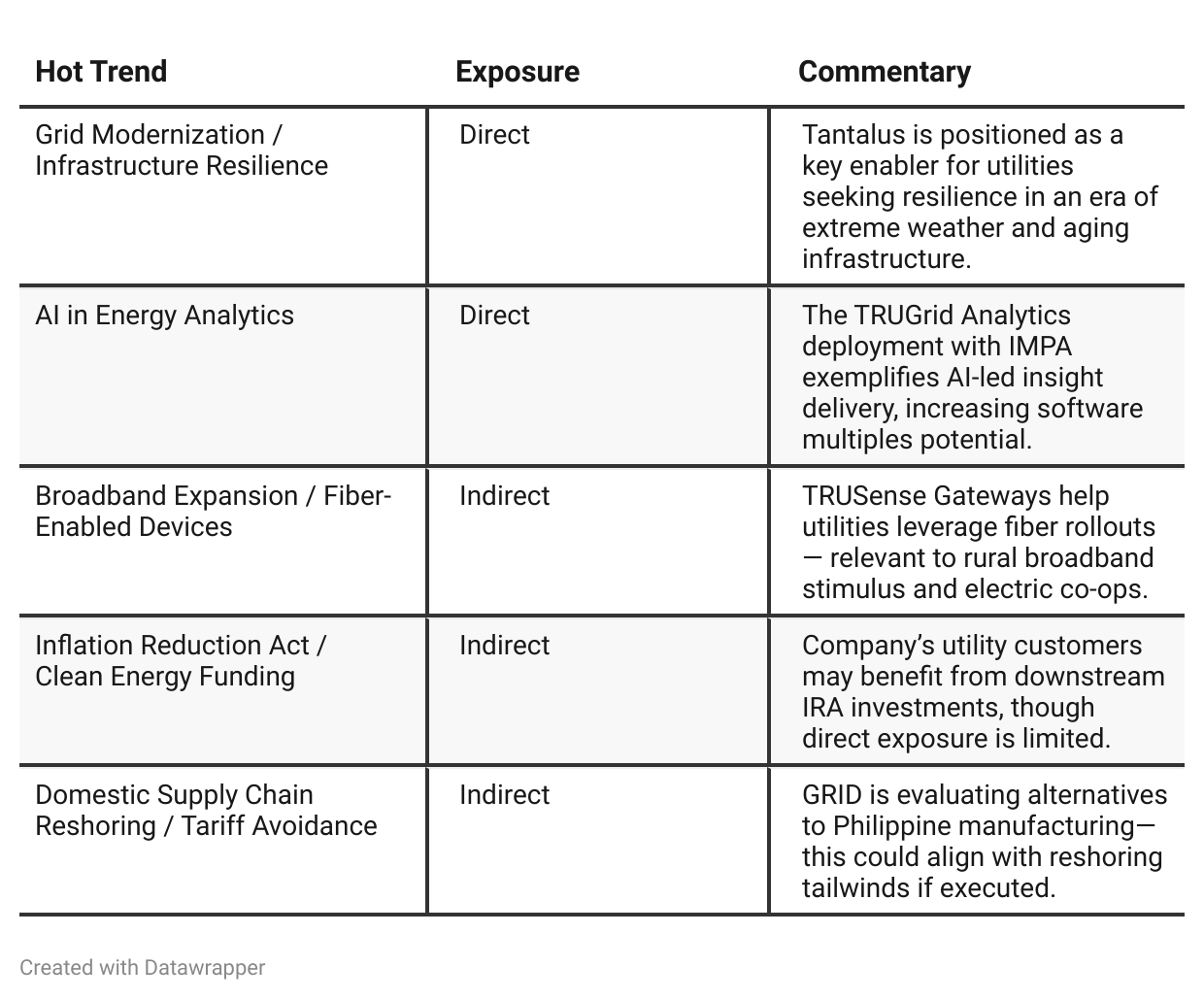

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison

Tantalus has transitioned from a company laying the groundwork for its flagship TRUSense Gateway in Q1 2025 to one entering a commercialization and scaling phase by Q2 2025. The narrative evolved from cautious optimism around pilot programs and macro tailwinds to execution-focused momentum—bolstered by record sales orders, expanded customer footprint, and a landmark deal with EPB.

Tariffs became more acute (increasing to 19%), but instead of derailing progress, Tantalus is using its absorption strategy as a competitive differentiator. Financially, the company remains disciplined, achieving recurring revenue growth and improving EBITDA.

The evolving message is clear: Tantalus is no longer just preparing for grid modernization—it is executing on it at scale.Year-over-year comparison

Tantalus Systems’ narrative shifted meaningfully from Q2 2024 to Q2 2025—from a company laying groundwork for a new flagship product (TRUSense Gateway) and navigating supply chain constraints, to one that is actively scaling that product across a broadening customer base and securing repeatable revenue streams.

In Q2 2024, management emphasized strategic investment and market readiness; by Q2 2025, the focus had transitioned to operational execution, commercial adoption, and resilience in the face of external shocks (e.g., tariffs).

The tone is more confident, supported by record sales, expanding recurring revenue, and early signs of customer-led network effects.

Final Takeaway

Tantalus Systems is in a growth phase, aggressively expanding its smart grid platform through TRUSense Gateway deployments and AI-driven analytics. While tariff-driven cost pressures pose short-term risks, management’s customer-first pricing strategy is reinforcing long-term relationships and helping drive record sales conversions.

Execution on TRUSense revenue realization, margin recovery, and geographic diversification of manufacturing will be key for sustaining momentum.

Verdict: BUY, with upside dependent on continued ARR growth and margin stabilization post-tariff absorption.