TransAlta Corporation (NYSE: TAC) – Q2 2025 Earnings

TransAlta Corporation (NYSE: TAC) – Q2 2025 Earnings

Earnings Release Date: Aug. 1, 2025

Stock Price: $12.05

Market Cap: $3590.9 million

Q2 2025 sales of $433 million vs $582 million in the prior year

Q2 2025 EPS of ($0.38) vs $0.18 in the prior year

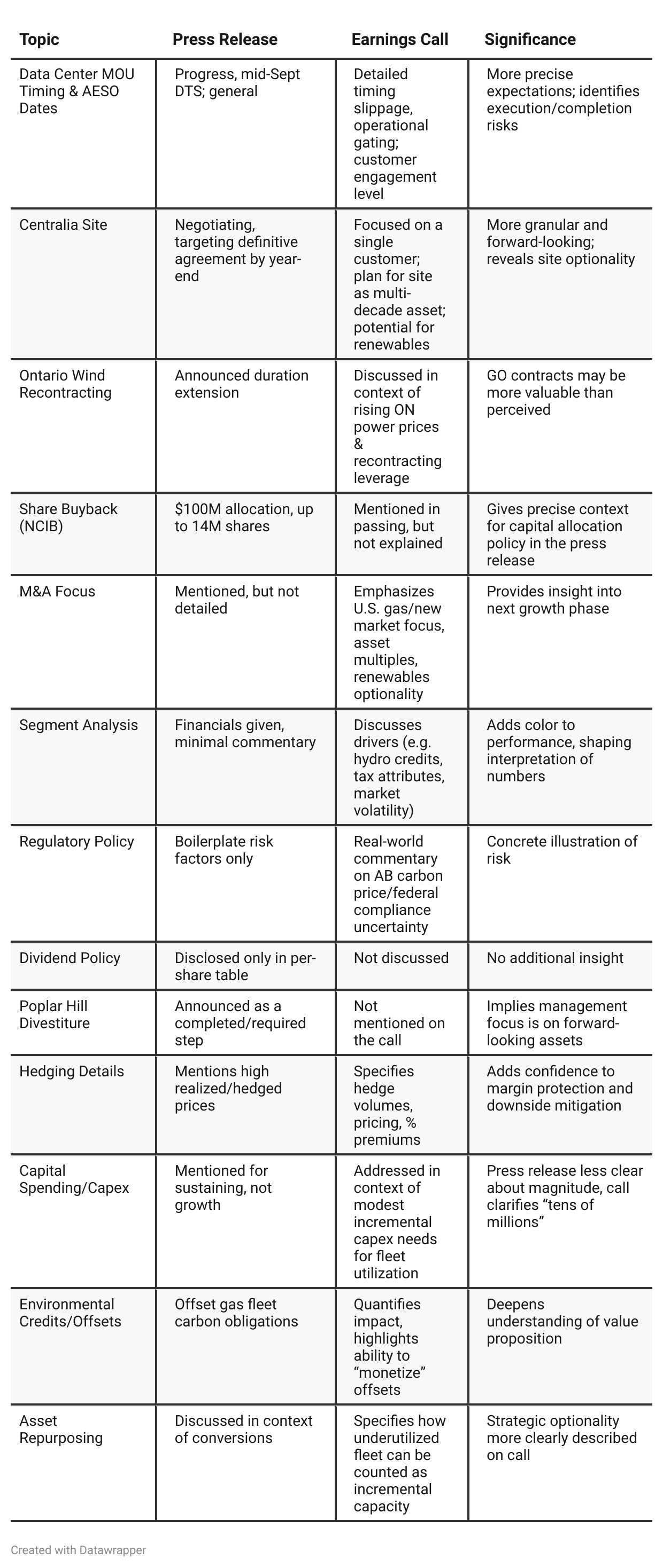

Press Release vs Call Transcript Comparison

Management Tone: The earnings call reveals visible confidence in multi-year growth (data centers, M&A, asset repurposing); the press release is more “to script.”

Execution Risk: The call gives insight into gating factors and process slippage (e.g., data center MOUs, regulatory timing)—critical for those trading on timing/announcements.

Clean Energy Positioning: The press release highlights “70% reduction in GHG emissions” and an “MSCI ESG AA rating,” while the call contextualizes how actual financial benefits flow through hydro/wind credit monetization.

Liquidity & Leverage: Press release details new credit agreements, supporting claims (in the call) that the firm retains “ample liquidity” for buybacks or M&A.

Merchant Market Exposure: Only the call spells out the realized prices across Alberta’s hedged, merchant, and ancillary lines, exposing real margin sustainability versus market volatility.

Disclosure Quality: The press release provides comprehensive financial tables and reconciliations, while the call translates numbers into strategic interpretation.

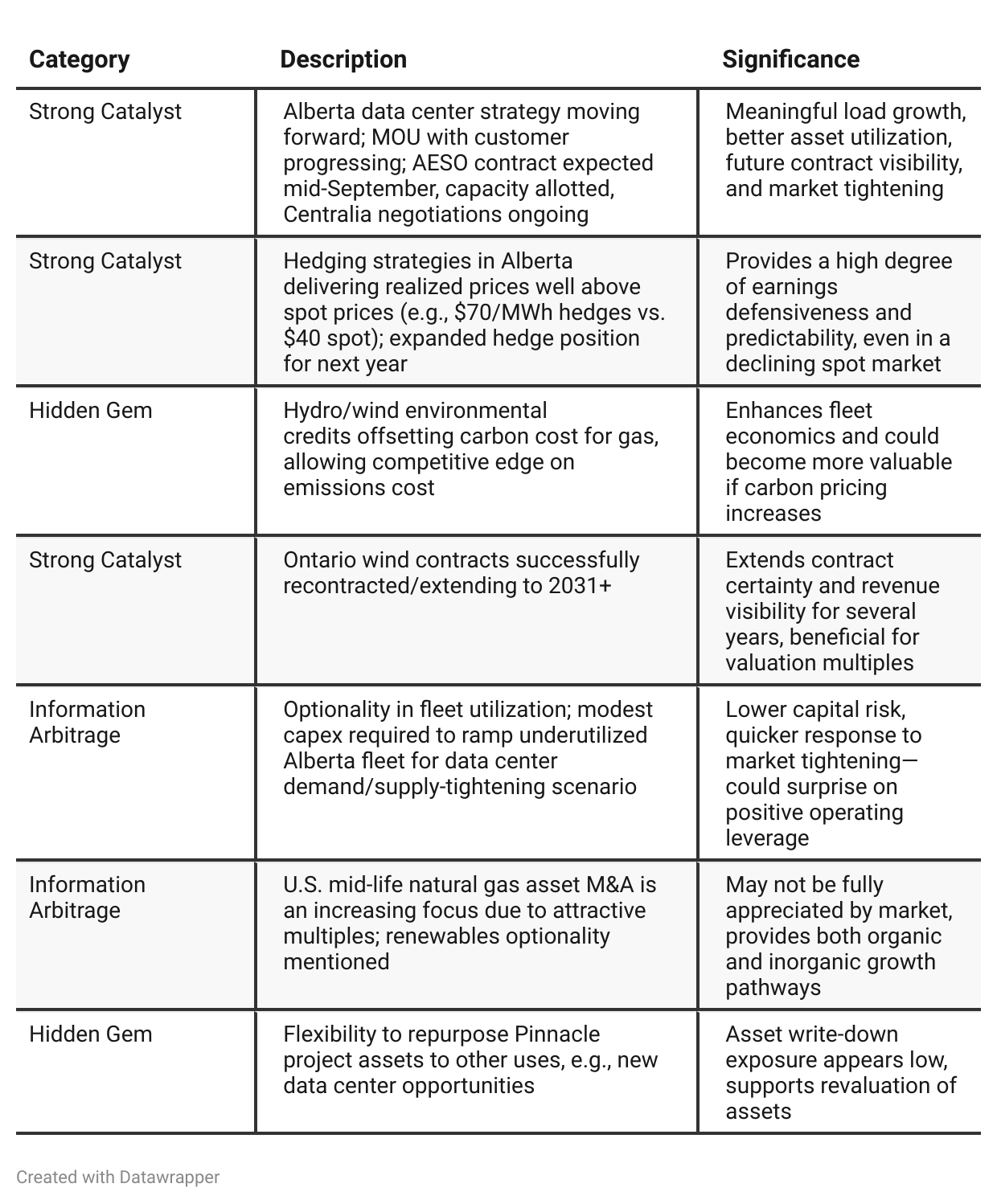

Positive Insights

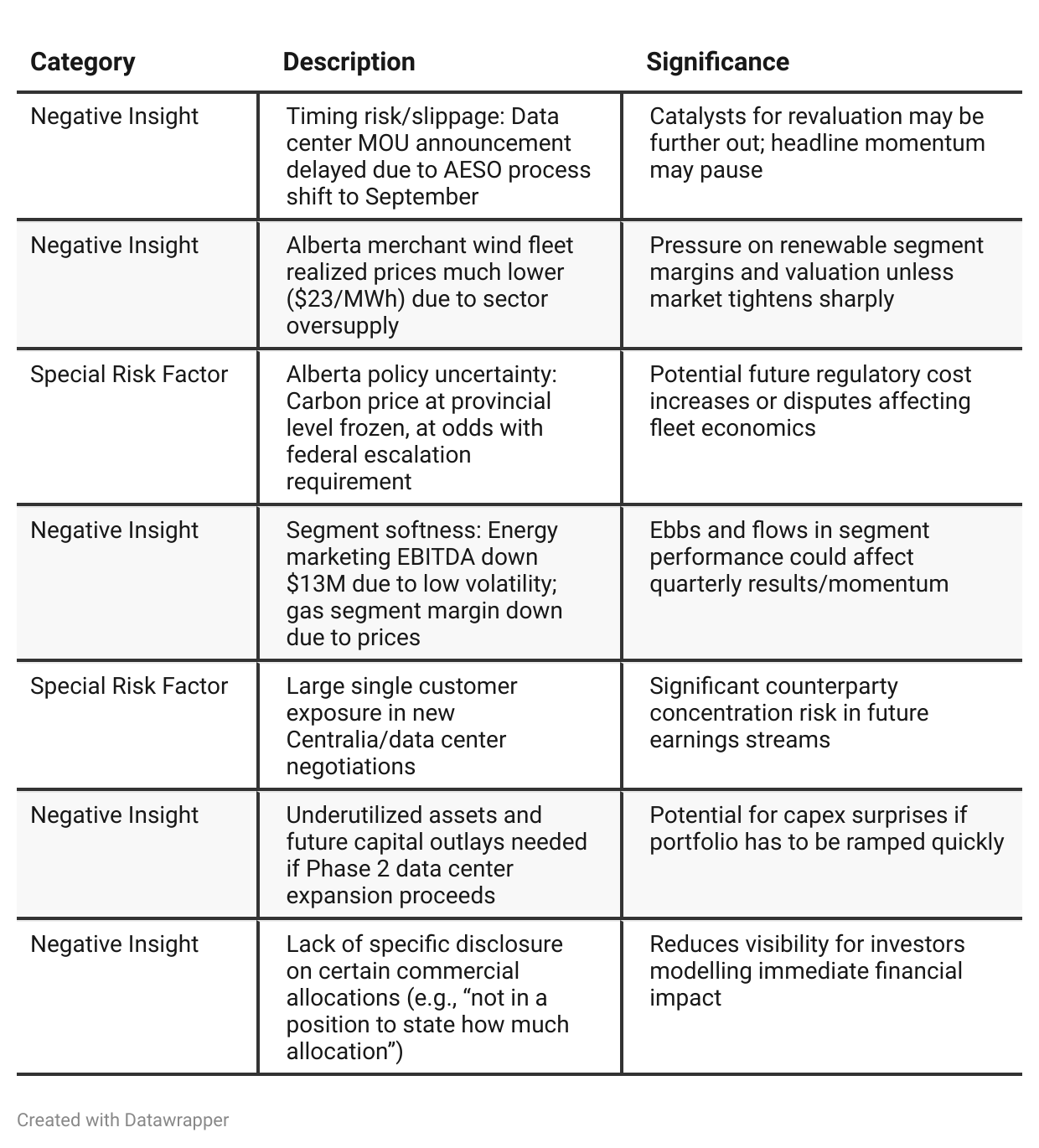

Negative Insights

Tariff Risk

No direct references to U.S. tariffs or trade policy affecting supply chain, revenue, profitability, or project execution in this transcript.

Mitigation/Adaptation Actions: Not discussed.

Market Effects: Not addressed.

Forward-Looking Tariff Commentary: None present.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: TransAlta articulated a vision of disciplined, defensive growth in a complex macro environment, prioritizing diversification away from Alberta, increasing contracted cash flows, and maximizing value from legacy assets. The narrative was cautious but opportunistic, focusing on hedging, M&A, portfolio optimization, and sustained shareholder returns, all while acknowledging regulatory and cost risks.Q2 2025: The company’s story shifts to one of delivery and execution—moving key projects and contracts (data centers, Centralia, wind recontracting) from negotiation towards completion, locking in operational and financial resilience (hedging, cost management, liquidity), and openly addressing execution and timing risks. The tone is more assertive, with management “pleased” with both current results and progress on priorities laid out in Q1. Strategic direction remains constant, but the focus is now on tangible near-term catalysts, with active efforts to close deals and secure growth while skillfully managing risks.

Year-over-year comparison

In Q2 2024, TransAlta was a company in prudent wait-and-see mode—emphasizing capital discipline, hedge protection, regulatory navigation, and laying out multiple optional paths forward (legacy asset redevelopment, new growth, Heartland/M&A). Opportunity and value in legacy assets are recognized, but described as future potential.

By Q2 2025, TransAlta’s narrative shifts forward: The company is executing on those options, moving key catalysts (data center contracts, Centralia conversion, wind contract renewals) toward completion and integrating them into its operational and financial performance. The messaging is more confident, operational improvements and customer deals are more specific, and risk (while still real) is positioned as manageable and largely internal (timing/execution, not market existential). The tone is now of a company successfully transitioning from prudent preparation to proactive delivery; disciplined, but with the operational and strategic momentum finally shifting in management’s favor.

Final Takeaway

TransAlta is in a late-stage restructuring/growth phase, focused on repurposing legacy assets into new growth engines (data centers, gas conversions) while managing risk with robust hedging and strong liquidity. Key growth drivers are the Alberta data center strategy, Centralia redevelopment, and ongoing asset optimization/M&A. Major catalysts are subject to timing risks and require successful contract execution. While the company’s business model shows resilience, execution on data center deals and regulatory clarity will determine its ultimate upside.

Verdict: Hold (positive bias)—potential upside materializes if data center/capacity contracts convert into revenue and earnings as envisioned.