Supremex Inc. (OTCPK: SUMXF/SXP:CA) – Q3 2025 Earnings

Supremex Inc. (OTCPK: SUMXF/SXP:CA) – Q3 2025 Earnings

Earnings Release Date: Nov. 06, 2025 (all figures in Canadian dollars)

Stock Price: $2.57

Market Cap: $63.1 million

Q3 2025 sales of $65.7 million vs $69.4 million in the prior year

Q3 2025 EPS of $0.37 vs ($0.92) in the prior year

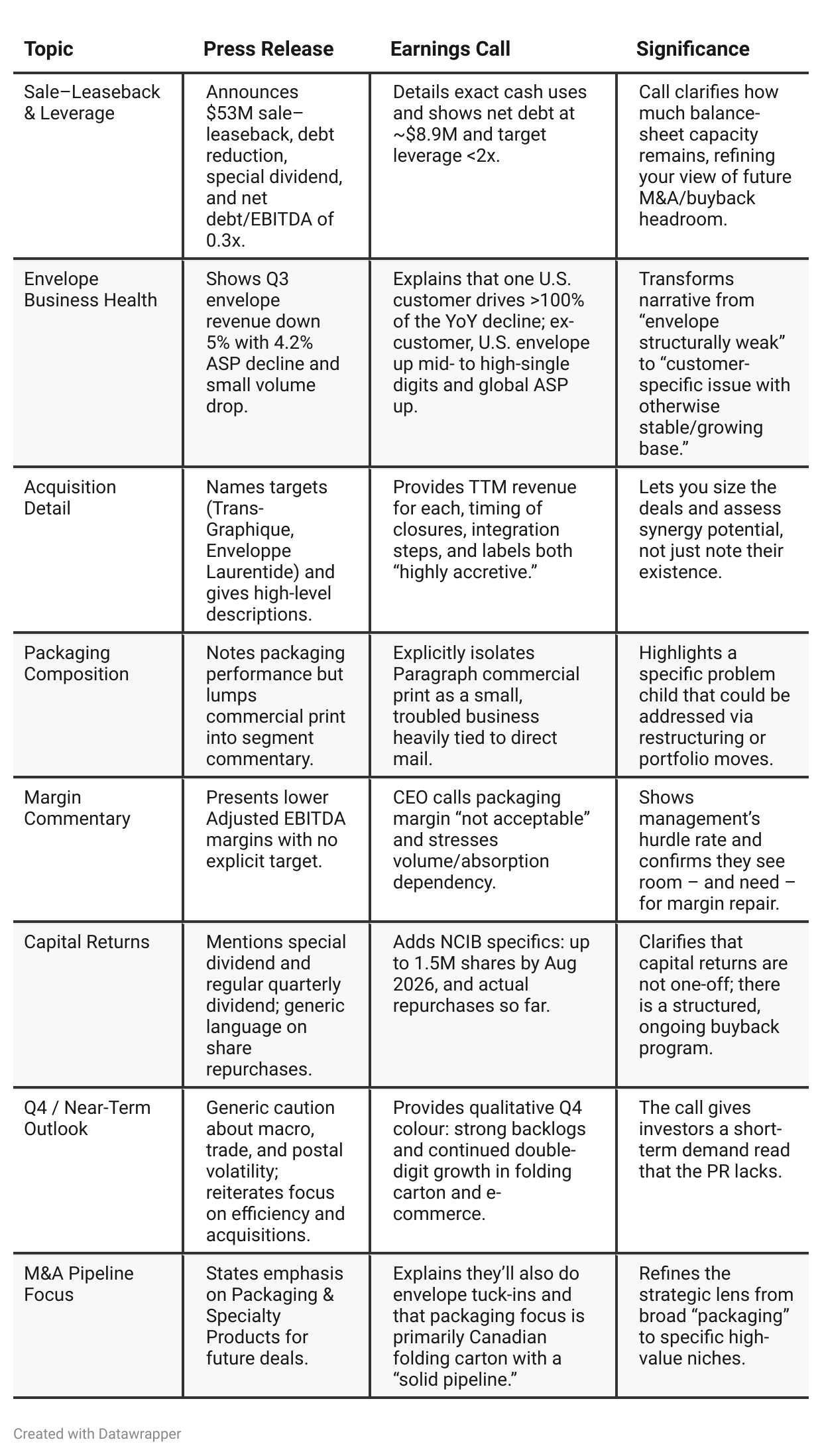

Press Release vs Call Transcript Comparison

Tone difference: The press release is upbeat and polished; the call is more candid, openly calling out “choppy waters,” “not acceptable” margins, and a problematic Paragraph business – but also highlighting underlying growth where it exists. This helps gauge management honesty and self-awareness.

Execution capability: Rapid integration of two acquisitions (closing, shutting down plants, moving volume, exiting facilities by October) suggests real operational discipline, important for a roll-up-plus-optimization strategy.

Capital allocation philosophy: Across both documents, you see a pattern – recycle capital from non-core assets (real estate) into debt reduction, tuck-in M&A, and shareholder returns, while keeping leverage low. That’s consistent with a value-and-cash-yield story rather than a high-growth one.

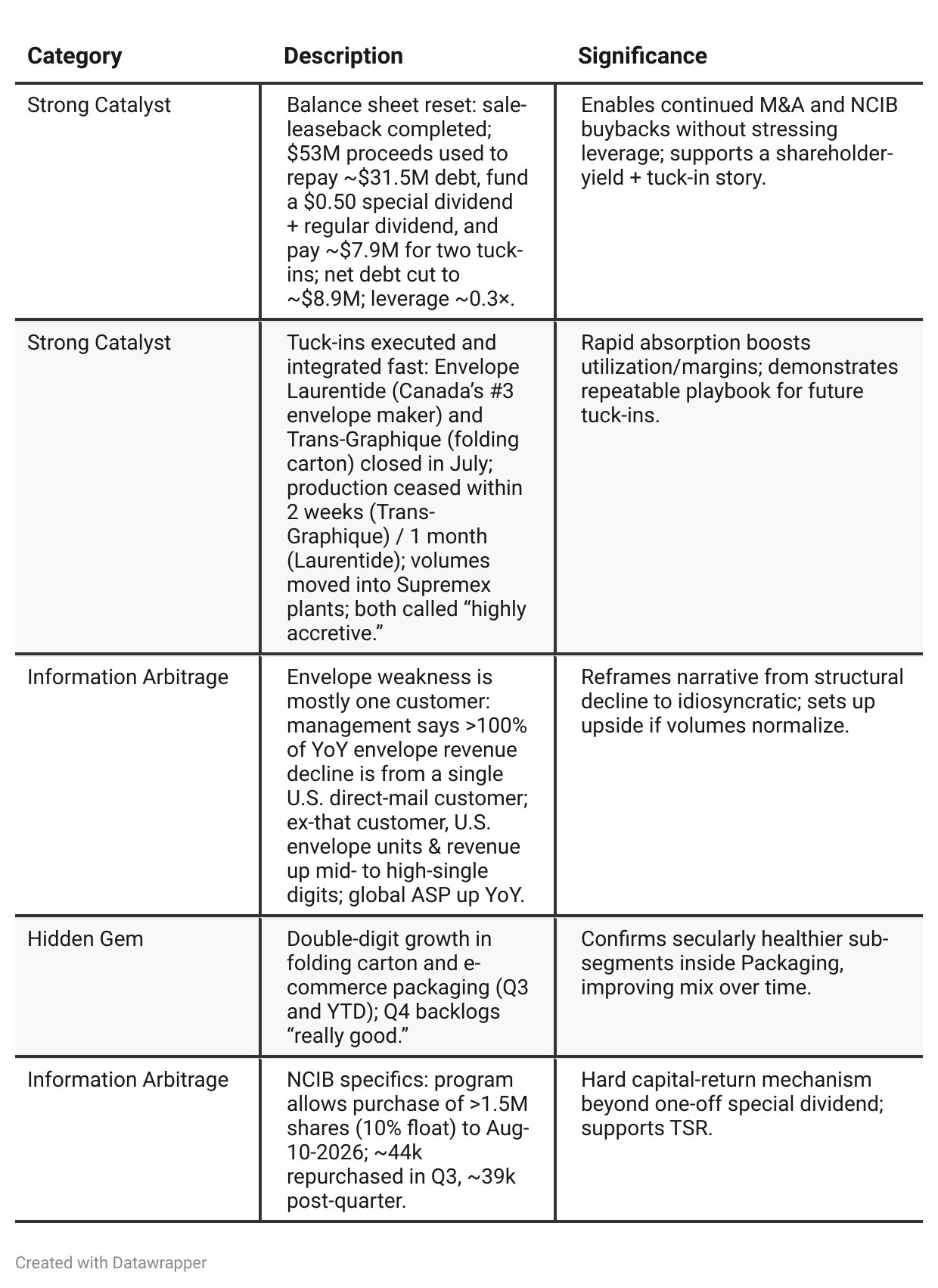

Positive Insights

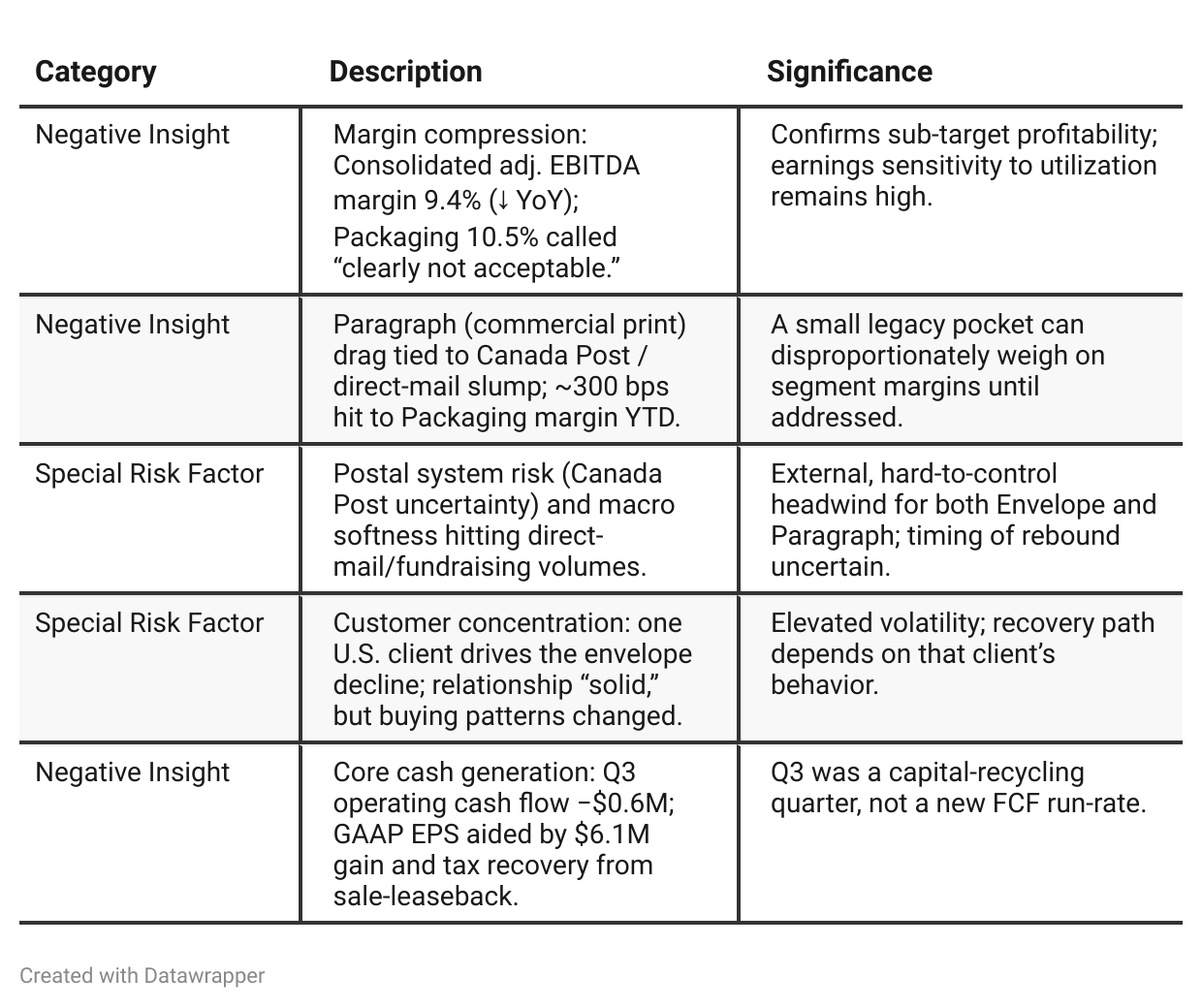

Negative Insights

Tariff Risk

Mentions in the call: None specific. Management references the broader “trade environment” in outlook language but gives no tariff-specific commentary.

Implications: Based on this transcript alone, tariffs are not presented as a current driver of revenue, supply chain, or margin outcomes; no mitigation actions (supplier shifts, pricing changes) were discussed. Investors should monitor future calls/filings for any change if trade policy evolves.

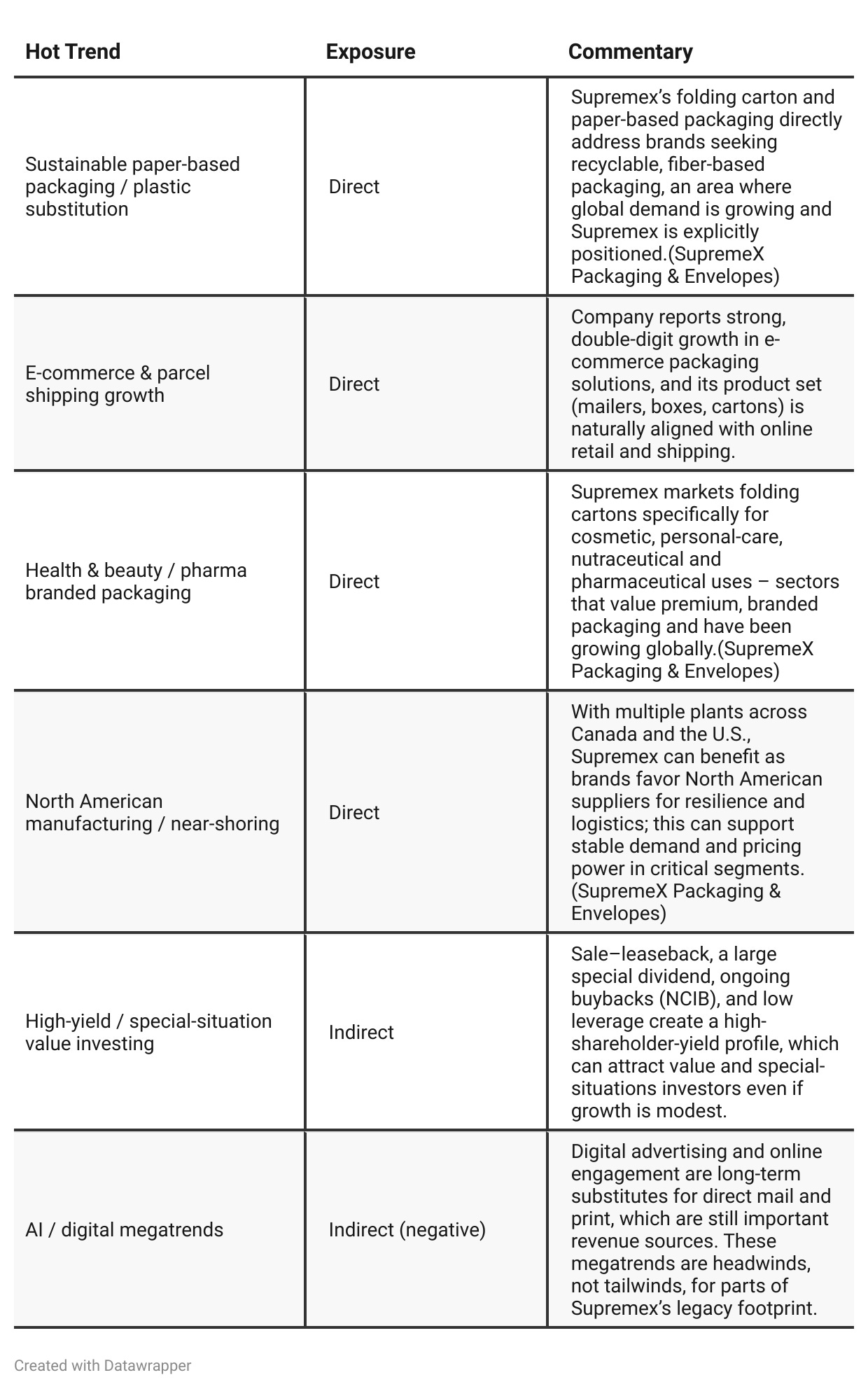

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison

Q2 2025:

Supremex entered midyear on the defensive. Management emphasized temporary hits (FX loss, one-customer issue) while highlighting the sale–leaseback and small acquisitions as shareholder-friendly wins. Tone leaned reactive, with an undercurrent of “trust us, fundamentals are fine.” Interim CFO signaled continuity but not permanence.Q3 2025:

By the next quarter, the company’s narrative matured significantly. A permanent CFO joins, the balance sheet transformation is complete, and management speaks from a position of control, not defense. They acknowledge continued weakness (Paragraph, postal headwinds) but articulate specific numbers, actions, and accountability. The mood is pragmatic yet constructive: a company emerging from balance-sheet repair into operational optimization mode, emphasizing margin recovery, selective M&A, and sustainable shareholder returns.Year-over-year comparison

Q3-2024 → Q3-2025:

The story advances from “we’re optimizing and planning to unlock value” to “we’ve unlocked value, reset the balance sheet, and are holding ourselves accountable for margin repair while doubling down on tuck-ins.” 2025 adds sharper disclosure (customer concentration; Paragraph drag), firmer capital-return mechanics (NCIB live; special dividend done), and a steadier leadership voice with a new CFO. The near-term growth lens tightens around folding carton & e-commerce, while management candidly flags Canada Post/Paragraph as the key margin headwinds to fix next.

Final Takeaway

Supremex appears in a stabilization + portfolio-mix phase: de-risked balance sheet, disciplined tuck-ins, and growth in folding carton/e-commerce are offset by postal-exposed pockets and a single-customer envelope headwind. While catalysts exist (customer recovery, Paragraph fix, sustained NCIB), margin repair and execution on absorption will be decisive. Verdict: HOLD, with upside if envelope volumes normalize and Packaging margins rebound while leverage stays low.