Sensus Healthcare, Inc. (NASDAQ: SRTS) – Q1 2025 Earnings

Sensus Healthcare, Inc. (NASDAQ: SRTS) – Q1 2025 Earnings

Earnings Release Date: May 15, 2025

Stock Price: $4.82

Market Cap: $78.6 million

Q1 2025 sales of $8.3 million vs $10.7 million in the prior year

Q1 2025 EPS of ($0.16) vs $0.14 in the prior year

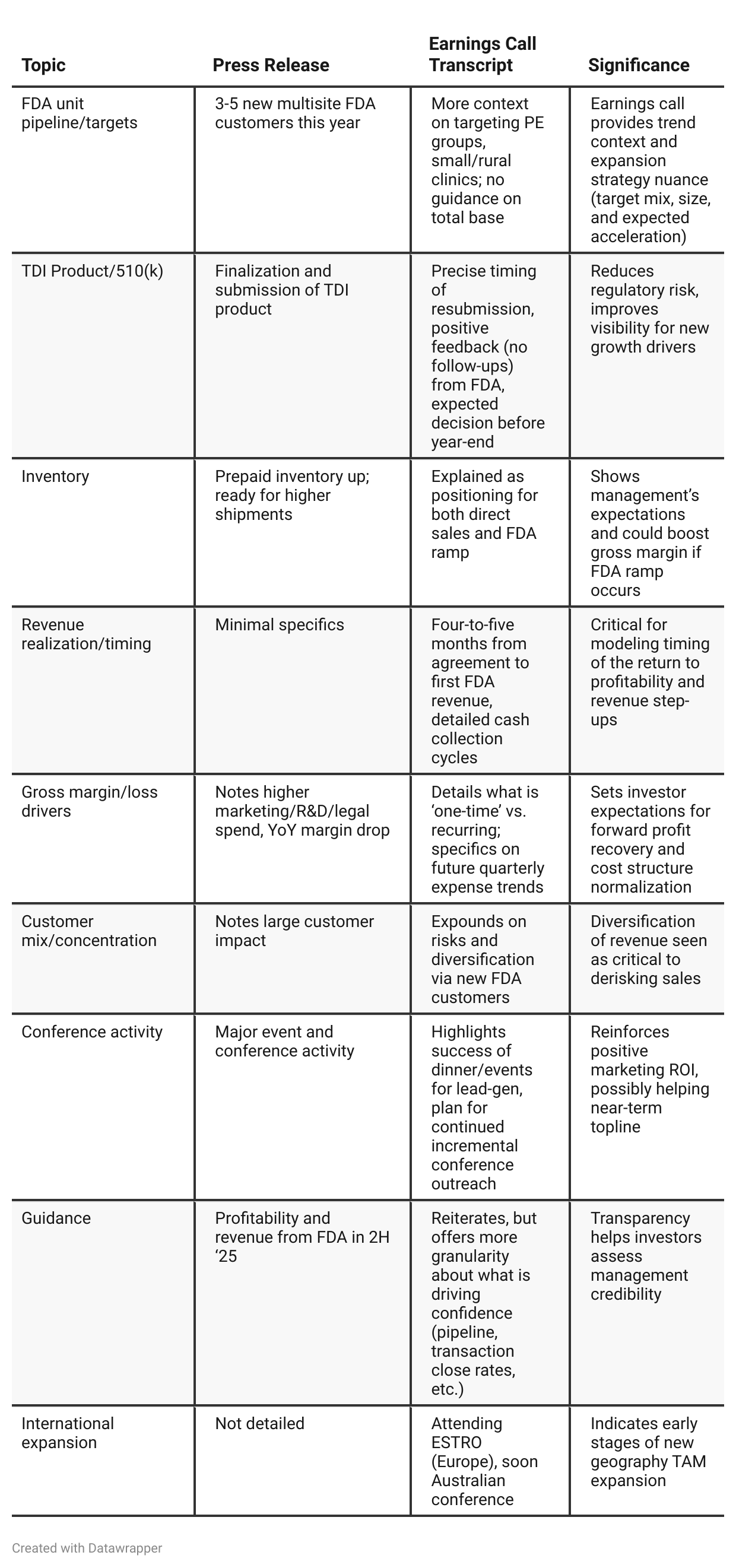

Press Release vs Call Transcript Comparison

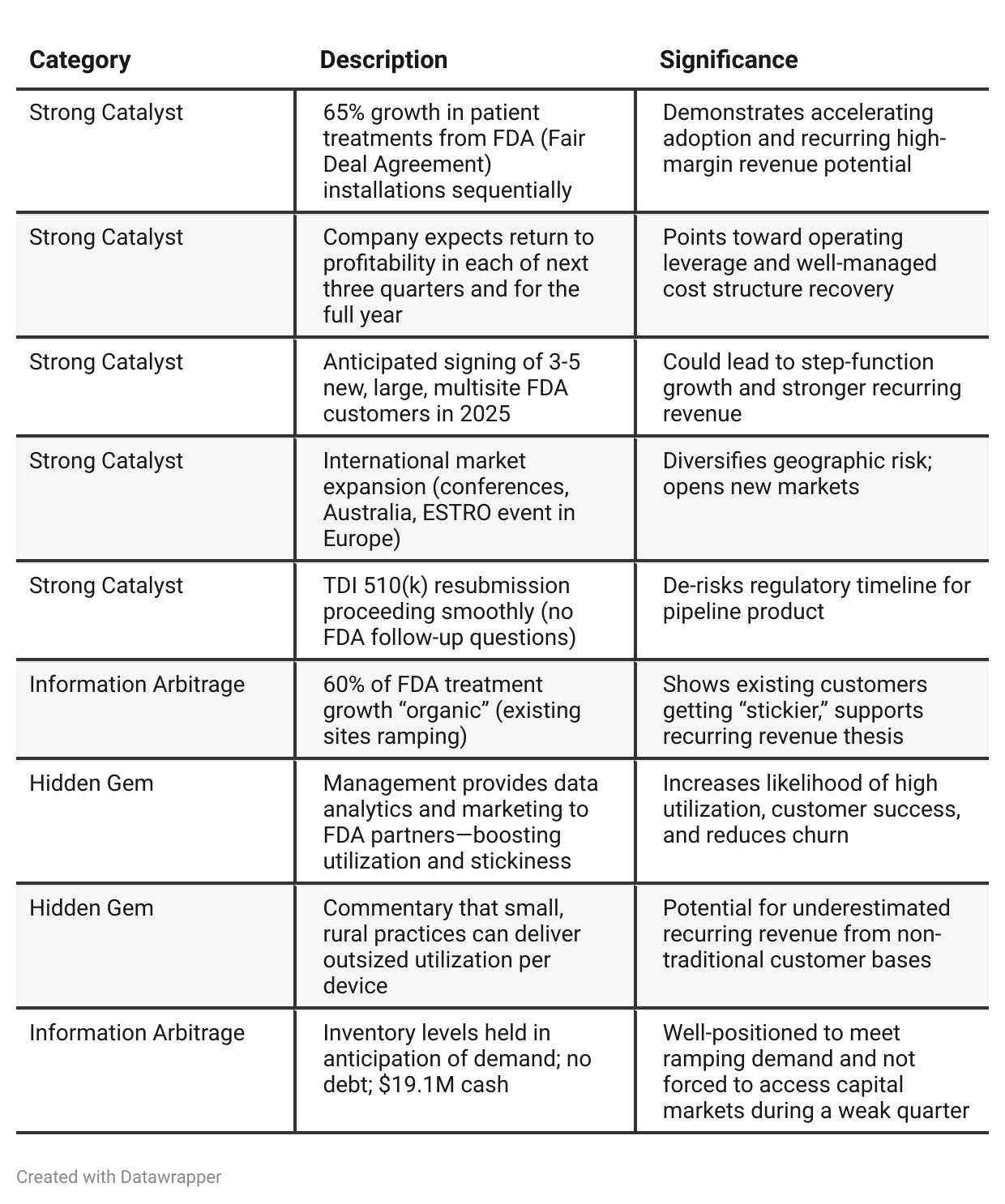

Recurrence Model Transition: Sensus is purposefully moving away from reliance on large up-front capital sales toward recurring revenue via FDA agreements. This is significant: recurring models, once proven, often merit higher multiples. However, there is a time and working capital lag before this shows up in reported results.

Data/Analytics & Customer Partnership: The company’s willingness to provide data insight and marketing support for FDA customers is a meaningful strategy to accelerate install utilization, reduce churn, and maximize per-site revenue—key for the recurring revenue thesis.

Event-driven Demand: Marketing efforts (esp. major dinner/channel events) are bearing fruit in pipeline growth and brand awareness. This could mean marketing ROI is justifying increased spend, setting foundation for significant forward sales.

R&D and Reimbursement Lobbying: While it pressures near-term margin, the investment in advocacy and TDI innovation could have positive long-tail returns (e.g., better reimbursement rates, expanded product lines).

Execution/Timing Risk: Due to install-to-revenue lag, Q2 may still be weak before the inflection in 2H. Investors focused on short-term results or quarter-to-quarter growth may need to be patient.

No Immediate Macro/Geopolitical Risks: As of now (per both), no major adverse effects from global conflicts or tariffs; positive vs. some healthtech names.

Positive Insights

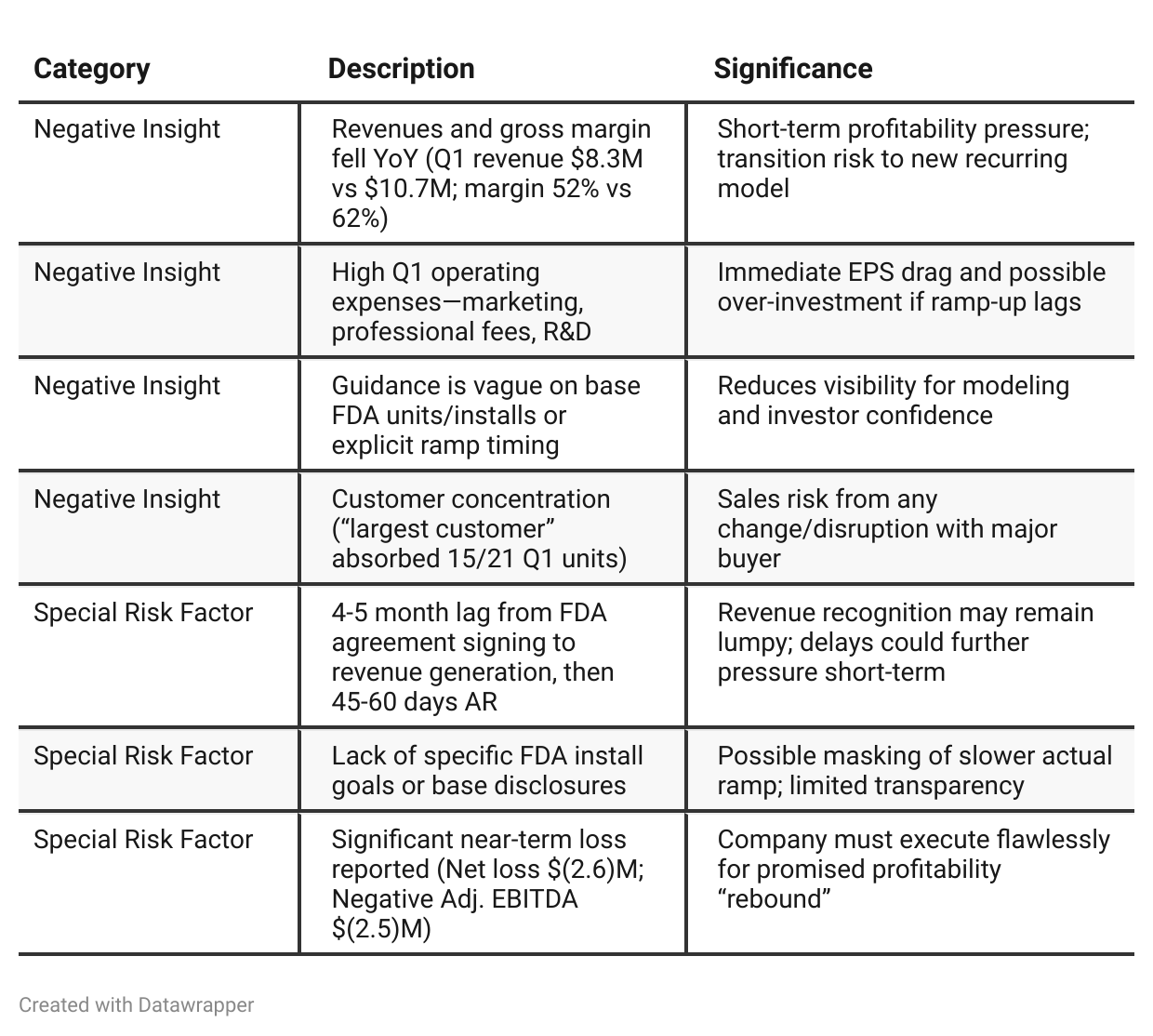

Negative Insights

Tariff Risk

Management was asked directly about U.S. tariffs. CEO stated clearly: “So far we have not witnessed any tariff repercussions on any of our businesses.”

No mention of changing supply chains, pricing strategies, or margin impacts due to tariffs.

No forward-looking warnings tied to trade policy or potential market share disruptions.

Competitive stance and ability to innovate remain unimpacted by tariffs at this stage.

Conclusion: For now, tariffs are not a material risk to Sensus Healthcare based on management testimony. Investors should nonetheless monitor industry trends for changes.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q4 2024: Sensus Healthcare was riding high on a year of record growth, profitability, and execution. The tone was proud and forward-looking, emphasizing new customer wins, success of established and new programs (FDA, international, even veterinary), and excitement about upcoming product launches and regulatory milestones. The narrative focused on owning market leadership, sustaining profitability, and strategic bets on big enterprise customers.Q1 2025: Despite strategic optimism, Sensus hit a near-term “pause” in its momentum: revenue dropped, expenses spiked, and profitability turned negative, all described as planned, temporary, and strategic (heavy investment). The narrative pivots to reassure investors: recurring revenue is now materializing—65% q/q patient growth in FDA units, most of which is from deeper “same-store” activity, not just new additions. Management gets candid about timing/tiering of ramp, revenue lags, and new expense levels, promising a return to profitability and signaling a foundation for future operational leverage. The company is more open about measuring the success of recurring revenue programs, shifting its focus from “points on the board” to “quality of revenue”—not just installs, but active, high-utilization, sticky installs. Progress in the pipeline (TDI, regulatory) and grassroots marketing are stressed as offsetting any short-term pain.

Year-over-year comparison

Q1 2024: Sensus Healthcare was coming off a period of rapid acceleration, with explosive growth in both revenue and profitability, successful product launches, a sharply expanding installed base, and the debut of its new—but not yet fully proven—recurring revenue model (Fair Deal Agreement). Message: “Momentum is on our side.”

Q1 2025: The company experienced a short-term reversal: revenue and profits dropped, due to both lower large-customer unit sales and sharply increased strategic investments in marketing, legal, and R&D. While the immediate numbers disappointed, management is more transparent about timing for a rebound, measurable progress in recurring revenue (65% q/q FDA patient growth), and organic growth in usage per machine. The focus has shifted from “topline at all costs” to building high-utilization, recurring revenue streams, improved customer stickiness, and establishing a higher-quality, higher-value business mix.

Final Takeaway

Sensus Healthcare is in a transitional growth phase, focused on shifting from volatile one-off capital sales to a recurring-revenue model via Fair Deal Agreements and innovation (such as the TDI system). The near-term outlook is pressured by higher spending, declining revenue, and margin compression, but if execution matches management’s optimistic guidance, significant re-rating potential exists. Investors should closely watch revenue and margin trends in Q2/Q3, FDA unit ramp speed, and expense normalization. Verdict: Hold—for now, execution is critical for upside.