Senstar Technologies Corporation (NASDAQ: SNT) – Q2 2025 Earnings

Senstar Technologies Corporation (NASDAQ: SNT) – Q2 2025 Earnings

Earnings Release Date: Aug. 25, 2025

Stock Price: $4.36

Market Cap: $101.7 million

Q2 2025 sales of $9.7 million vs $8.3 million in the prior year

Q2 2025 EPS of $0.05 vs $0.02 in the prior year

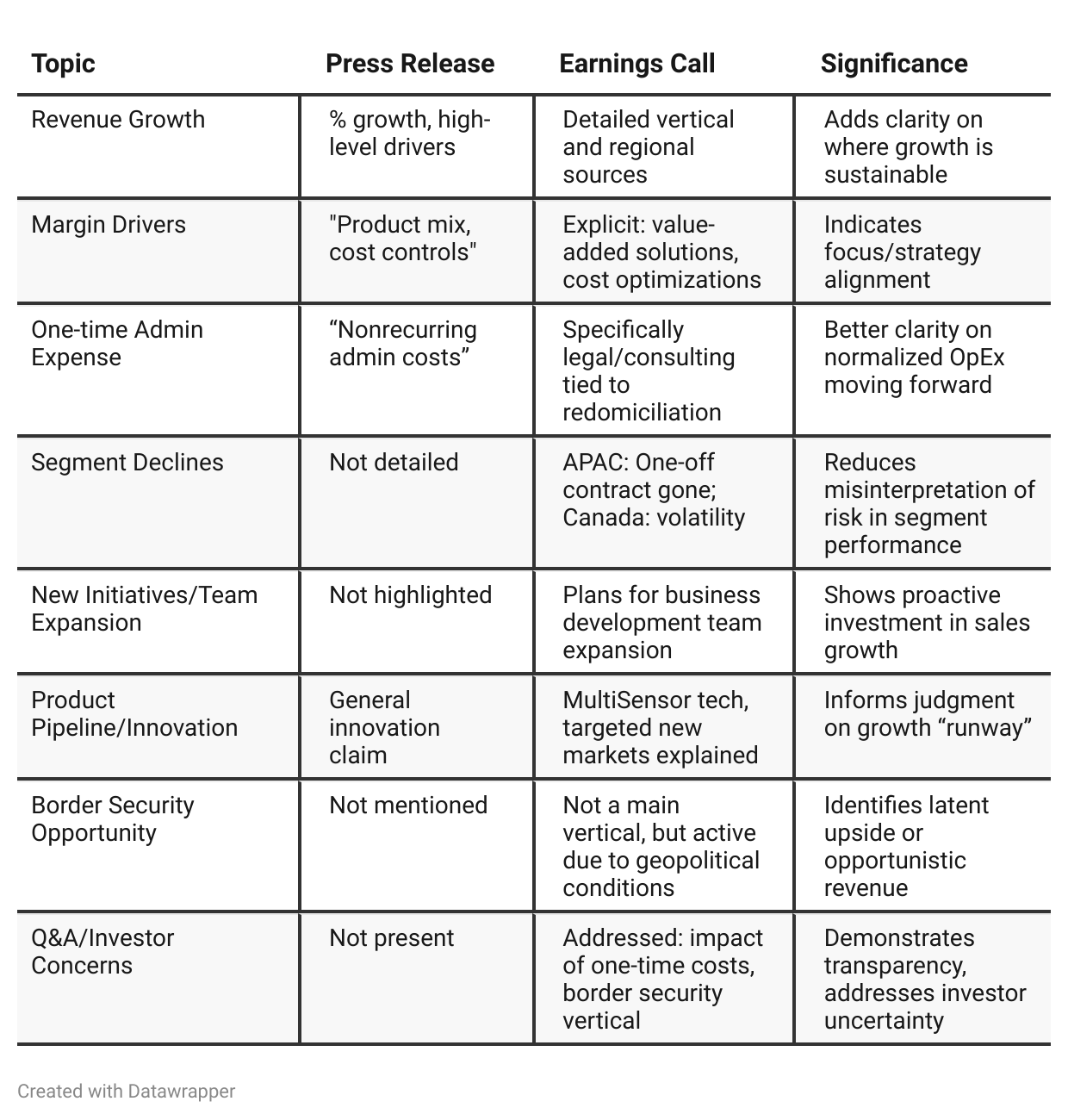

Press Release vs Call Transcript Comparison

Cash Position Slightly Up, No Debt: Both highlight this; positive for financial flexibility.

Operating Leverage: Repeated, but call details how revenue growth scales expenses.

FX Sensitivity: Only discussed on call—an important risk factor if dollar shifts continue.

Sustained International Effort: Call reveals more about diversified growth, compared to press release’s U.S./Europe focus.

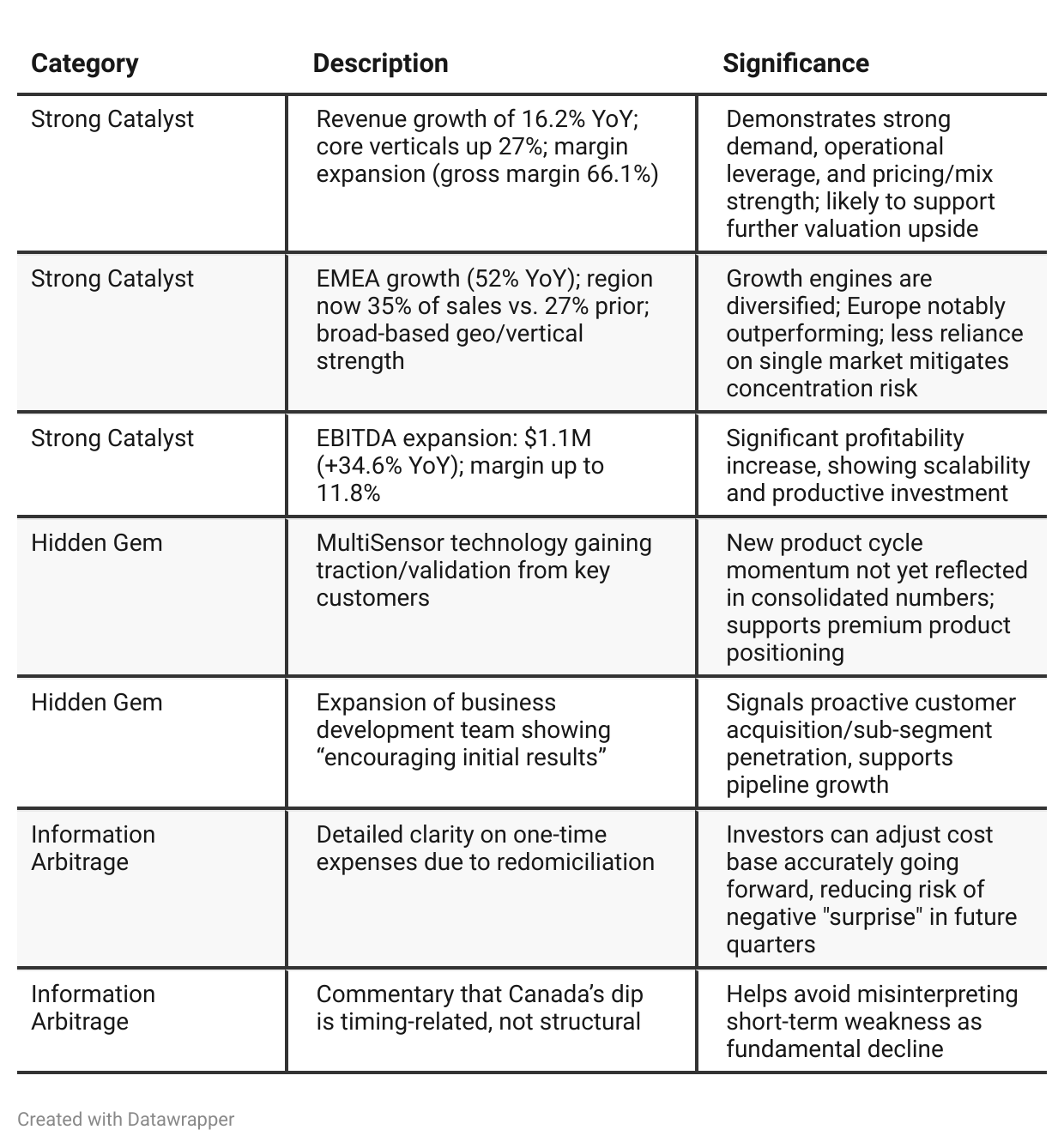

Positive Insights

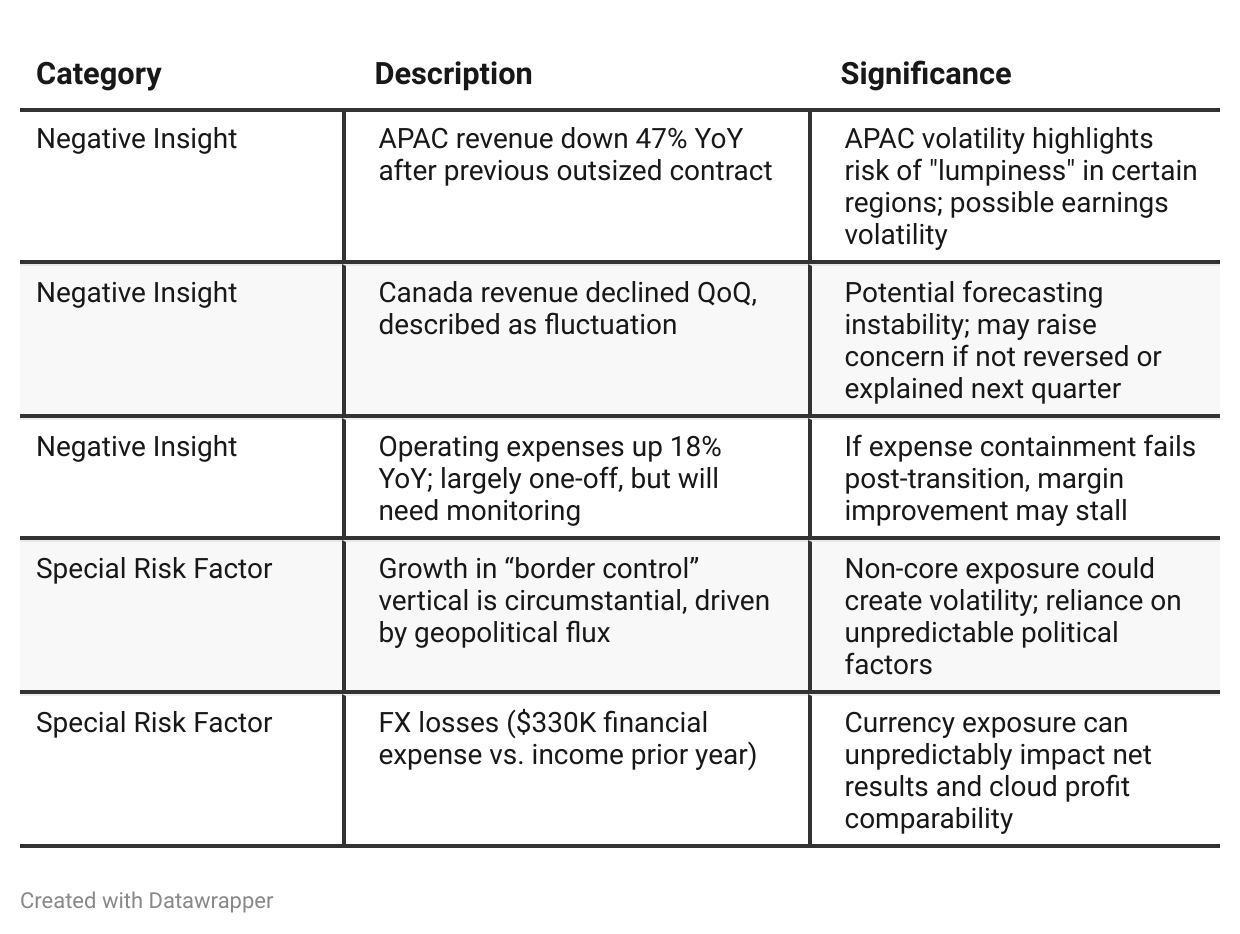

Negative Insights

Tariff Risk

Transcript mentions tariffs only in standard forward-looking/cautionary language.

No specific discussion of adverse impact from tariffs or related policies on revenue, costs, or supply chain.

No mitigation actions disclosed (e.g., alternate supply chains, pricing changes).

No statements on market share shifts or competitive positioning due to tariffs.

No forward-looking projections on tariff effects.

Investor Action: Given no active or contemplated tariff headwinds in the call, but general caution found in the legal disclaimer, investors should monitor SEC filings and news releases for changes in global trade/tariff landscape that might impact future quarters, especially with security technology exports or geographic expansion.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: Senstar’s management is disciplined and focused, telling a story of emerging margin strength, deep cost control, and the beginnings of a product-driven growth cycle (particularly with MultiSensor/Cascade Plus). There’s a careful tone—celebrating improvement, but not overreaching, with an eye on prudent operations and risk management, especially in a volatile macro environment (e.g., tariffs).

Q2 2025: The company’s narrative is brighter, more outward looking, and increasingly confident. Strong results in EMEA and North America demonstrate that earlier investments are paying off. There is clear evidence of a shift from simply controlling costs to deliberately scaling—via sales personnel expansion, cross-selling, larger international “key account” pursuits, and technology that’s gaining real customer traction. Risks are acknowledged honestly (APAC volatility, one-time admin spends, timing in Canada), but are positioned as manageable within a resilient, self-funded business model.

Year-over-year comparison

In Q2 2024, Senstar was squarely focused on operational recovery—navigating flat revenue with strengthened margins, improved cost control, and the highly anticipated rollout of its MultiSensor product. There was a tone of cautious discipline, emphasizing the need to overcome project timing delays in key regions and waiting on the impact of new innovation.

By Q2 2025, the narrative transforms into one of assertive international growth, competitive differentiation, and confident scaling. EMEA emerges as a new powerhouse; MultiSensor is moving from the promise to commercial traction; the organization is expanding its sales force and pouncing on broader adjacent markets. The company is now much more forward looking—openly discussing opportunities and risks, dissecting one-time expenses, and doubling down on international and product-led strategy to build momentum. The tone is more ambitious, less focused on recovery/defense, and more on attacking growth in diverse ways.

Final Takeaway

Senstar Technologies Corporation is in a growth phase, with a clear strategic shift toward international expansion (notably EMEA), new product innovation (MultiSensor), and targeted verticals (energy, corrections, utilities). The company is delivering both revenue and margin expansion, demonstrating operating leverage and prudent cost control. While there are isolated risks in APAC volatility and FX, the business is self-funding and not reliant on capital markets. Investor focus should remain on cash discipline, margin trends post-redomiciliation, and the conversion of pipeline/innovation into top-line acceleration.

Verdict: BUY, with potential upside driven by international momentum and product innovation, while monitoring for FX and regional volatility.