Smith Micro Software, Inc. (NASDAQ: SMSI) – Q2 2025 Earnings

Smith Micro Software, Inc. (NASDAQ: SMSI) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $0.72

Market Cap: $14.0 million

Q2 2025 sales of $4.4 million vs $5.1 million in the prior year

Q2 2025 EPS of ($0.14) vs ($0.38) in the prior year

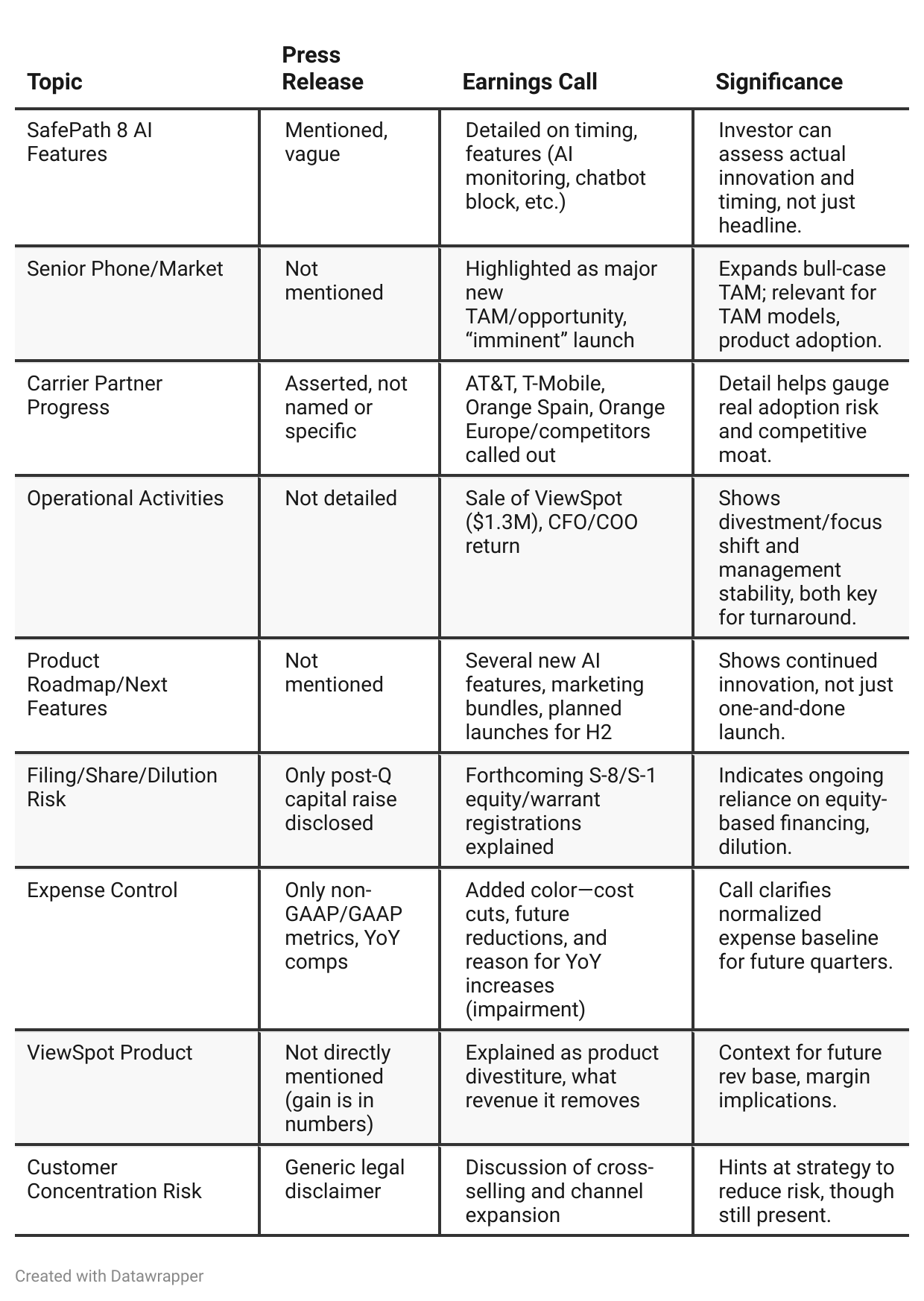

Press Release vs Call Transcript Comparison

The call provides much greater visibility into company strategy, go-to-market priorities, and near-term product launches than the press release.

The press release leans heavily on improvement in non-GAAP loss and gross margin; the call contextualizes this with explicit cost-management tactics and the impact of impairment charges.

The call’s mention of senior-market TAM, “set it and forget it” SafePath enhancements, and new AT&T/T-Mobile/Orange initiatives exposes upside that can’t be modeled using the press release alone.

Ongoing heavy GAAP losses, low cash, and impending dilution are clear negatives in both, but the call’s disclosure of further cost controls and asset sales makes the risk of operational “shrinking to survive” more visible.

Both documents contain bullish forward-looking statements, but the call has a more measured tone about “emerging from a difficult period,” versus the press release’s more unequivocal growth narrative.

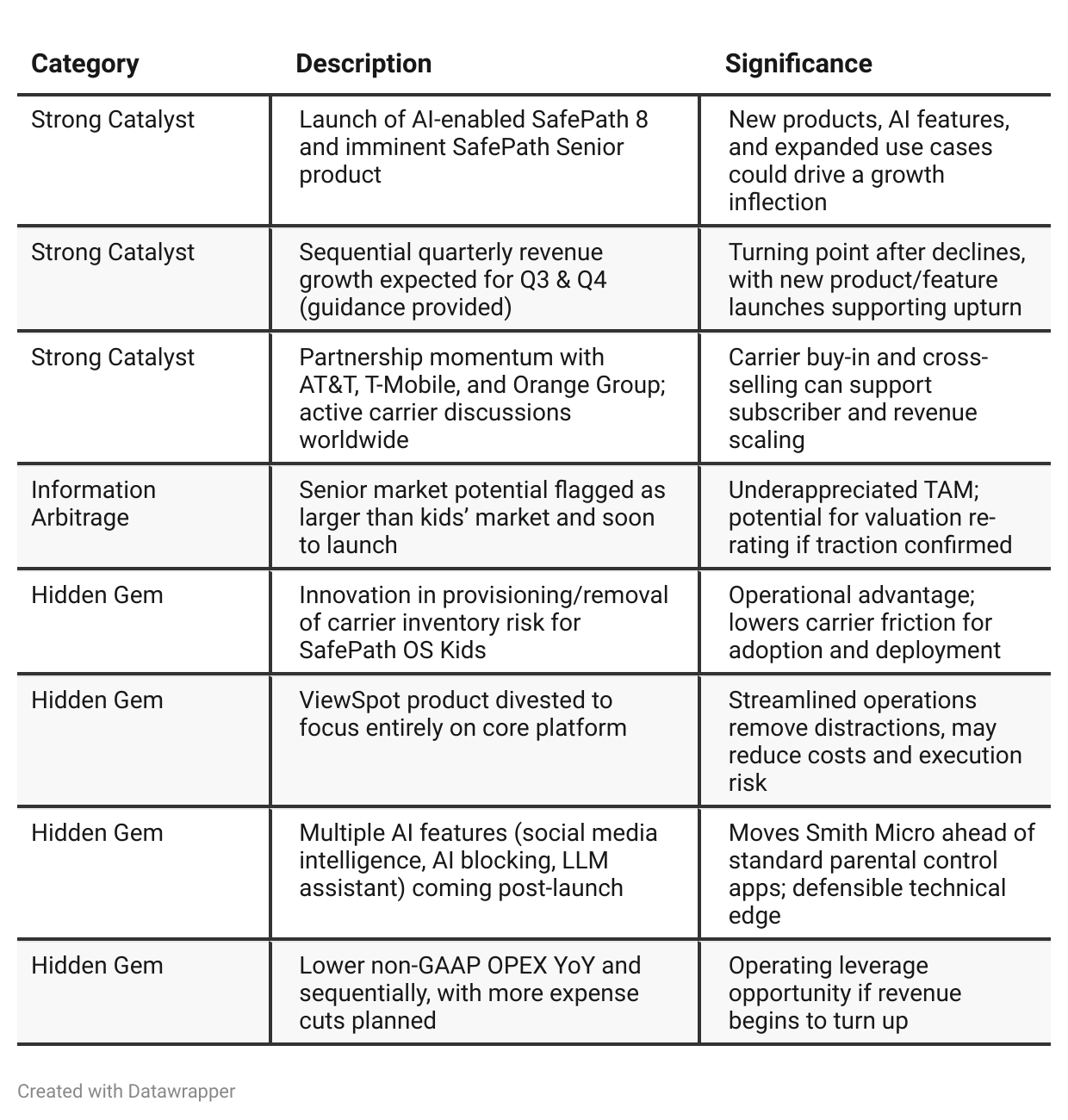

Positive Insights

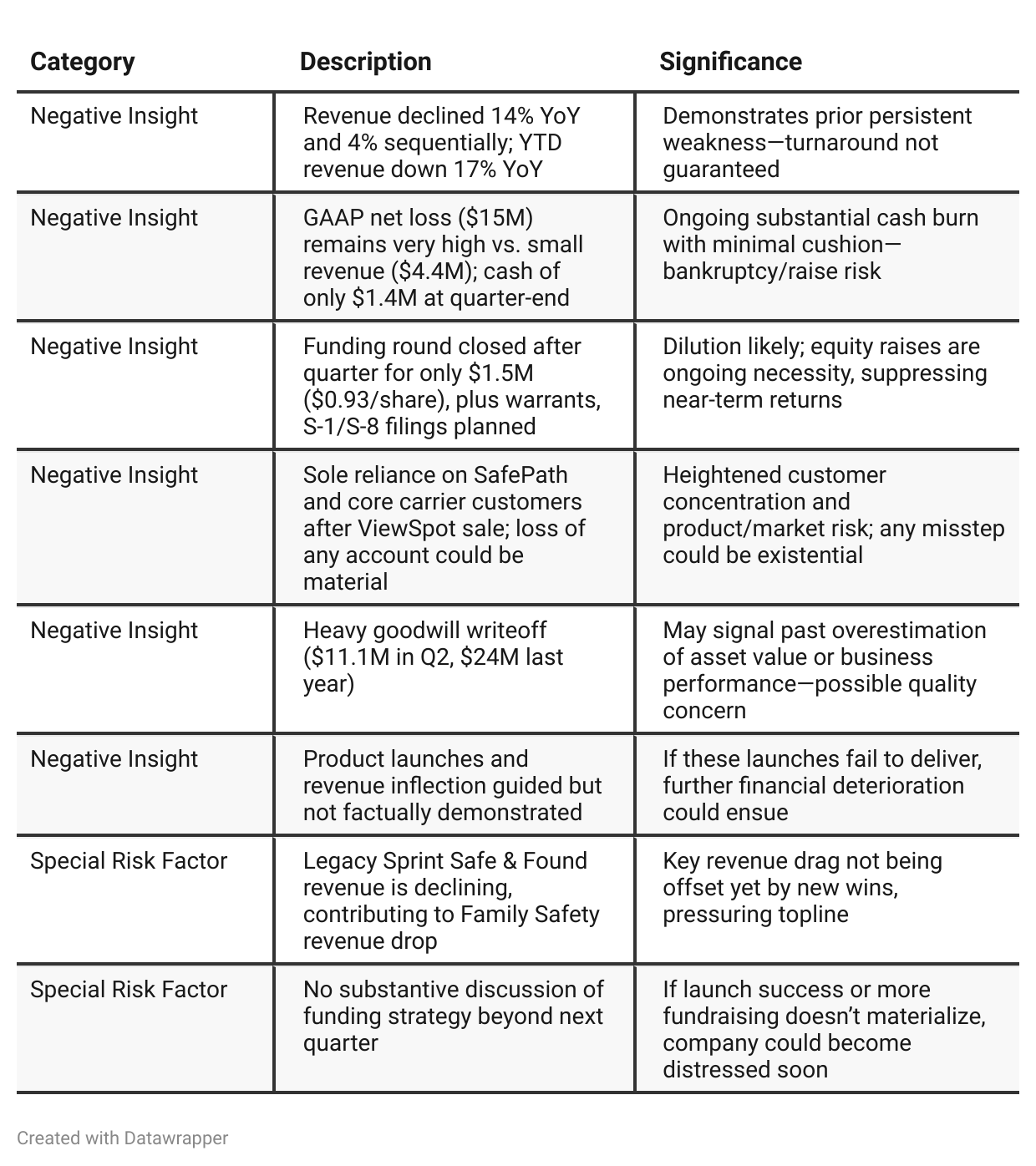

Negative Insights

Tariff Risk

Transcript Review for Tariff Mentions & Trade Policy Issues:

Result: No discussion of U.S. tariffs, trade policy, or international supply chain re-structuring.

No stated risk, mitigation plan, or commentary on impacts (positive or negative) of tariffs on revenue, costs, or competitive positioning.

No forward-looking statements or projections related to tariff impacts.

Investor Note: Absence may indicate low direct tariff exposure, but investors should verify in SEC filings—especially given European expansion.

Sentiment Analysis

The overall sentiment for Smith Micro Software ($SMSI) is bullish. Investors are expressing optimism about recent gross profit achievement, the potential for a delayed rally as the quarter’s profitability is realized, and a turnaround narrative supported by cost-cutting and leadership changes. Several comments reference historical runs, upcoming catalysts, and upside price targets, while risk is acknowledged but generally outweighed by expected rewards. The tone is overwhelmingly positive, with many anticipating upward price movement and improved fundamentals.

Previous Earnings Call

Quarter-over-quarter comparison

Smith Micro’s narrative has evolved from cautious optimism in Q1 2025, rooted in pipeline-building and experimental rollouts, to one of assertive (but conditional) turnaround in Q2 2025. Q1 emphasized innovation, hope for adoption by mobile operators, and groundwork-laying for new SafePath AI features and senior/child product lines, with most opportunities positioned as “just around the corner.” By Q2, the company’s messaging is less about preparation and more about action, with product launches, organizational realignment, divestiture of distractions, and new funding moves bringing sharper focus and urgency. There is now specific guidance for sequential revenue growth and a visible effort to manage the company’s cash and cost structure tightly. The tone has shifted from “we’re getting ready” to “we’re now executing”—yet, the financial risks and funding needs have also become more explicit, making execution and customer conversion crucial in the immediate quarters ahead.Year-over-year comparison

From Q2 2024 to Q2 2025, Smith Micro’s narrative transitions from a company reeling from lost legacy contracts and seeking stabilization through cost-cutting, pipeline growth, and partnership wins to a firm attempting a concrete turnaround based on new-product execution. The company in Q2 2024 was fixing its foundation, reporting marketing efforts, digital initiatives, and future launches as ways back to growth. By Q2 2025, the narrative is that of sharper action: new AI-enabled products are launched, competitive differentiation is clearer, and the company claims actual operational momentum. Management discusses both success in cutting costs and—candidly—the strains of large losses and low cash, but the tone is more forceful, expressing belief that Smith Micro is finally in a position to reverse declining trends. Going forward, the explicit challenge is clear: convert recent launches and partnerships into sustained, profitable revenue growth amidst continuing pressure on resources.

Final Takeaway

Smith Micro is in a critical restructuring phase, focused on a high-stakes pivot to AI-powered family and senior safety platforms. Current carrier engagement, coming product launches, and AI features offer powerful upside potential, but severe near-term financial and funding risks persist. Execution on launches, revenue turnaround, and cash management are make-or-break. Investors should closely monitor liquidity events, product traction, and carrier expansion for a possible thesis change.

Verdict: HOLD, with high risk/reward skew. Next 1-2 quarters are pivotal for determining sustainable upside or existential risk.