Rocky Mountain Chocolate Factory, Inc. (NASDAQ: RMCF) – Q2 2026 Earnings

Rocky Mountain Chocolate Factory, Inc. (NASDAQ: RMCF) – Q2 2026 Earnings

Earnings Release Date: Oct. 13, 2025

Stock Price: $1.62

Market Cap: $12.5 million

Q2 2026 sales of $6.8 million vs $6.4 million in the prior year

Q2 2026 EPS of ($0.09) vs ($0.11) in the prior year

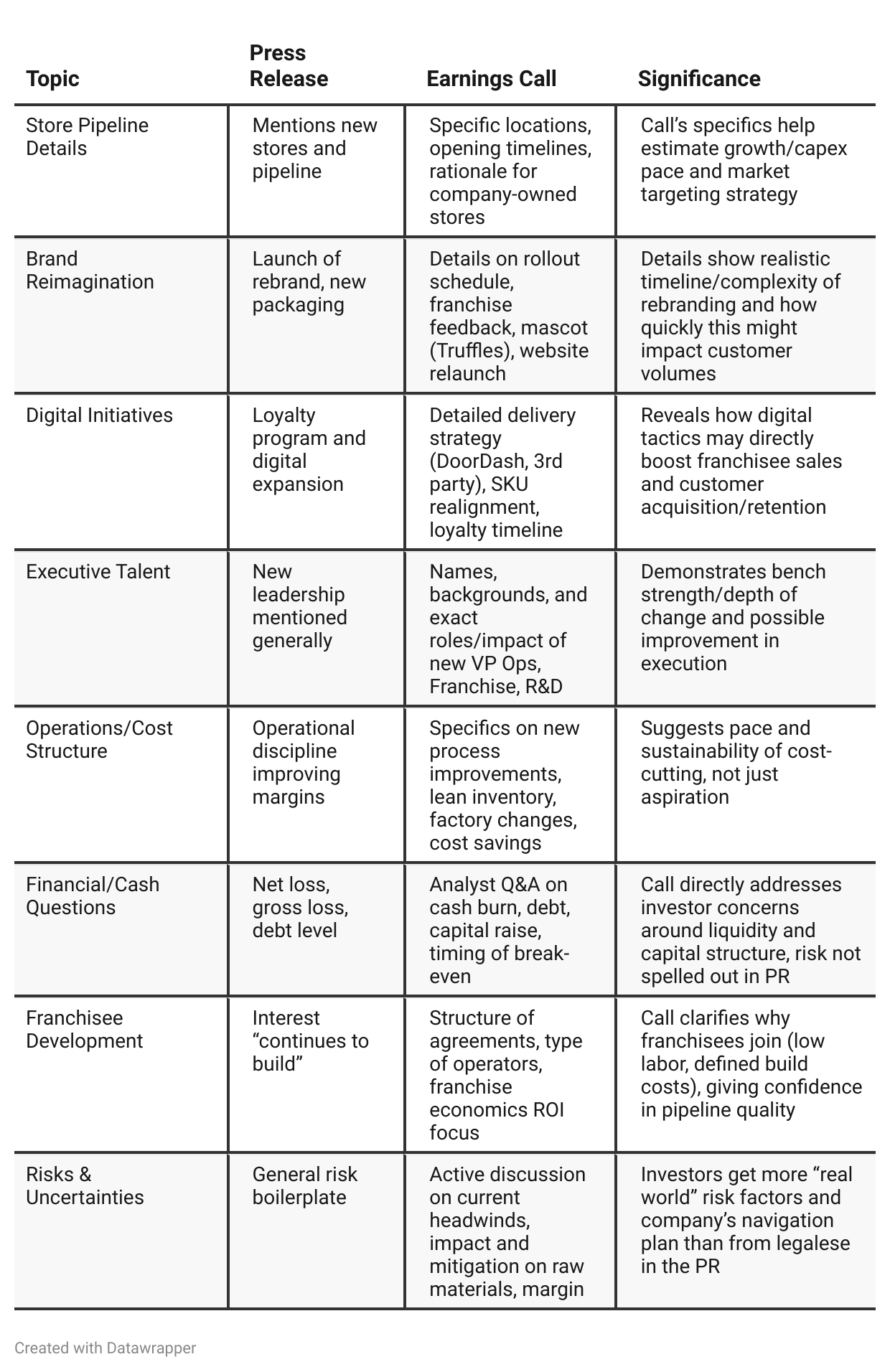

Press Release vs Call Transcript Comparison

Culture Shift: The call reveals a more ambitious and candid internal narrative than the measured PR language, signaling a true turning point in culture/change management. Tone and specificity increase trust in management’s game plan.

Margin Insight: Call color on cocoa pricing, hedging, input cost normalization, and how/when these flow to the P&L gives a much more nuanced view of gross margin outlook than the high-level numbers in the PR.

Balance Sheet Management: The call clarifies rationale for debt (seasonal need, not ongoing operations) and sets investor expectations regarding dilution/financing risks, something absent from the press release.

Execution Risk: The admission that store remodel results and new Ops processes are still being tested (call) sets realistic short-term expectations, whereas the PR offers a more forward-looking, polished message.

Growth Quality: Management is explicit about intentional franchisee growth (call) rather than “growth for growth’s sake,” hinting at higher long-term unit-level profitability—an important qualitative distinction.

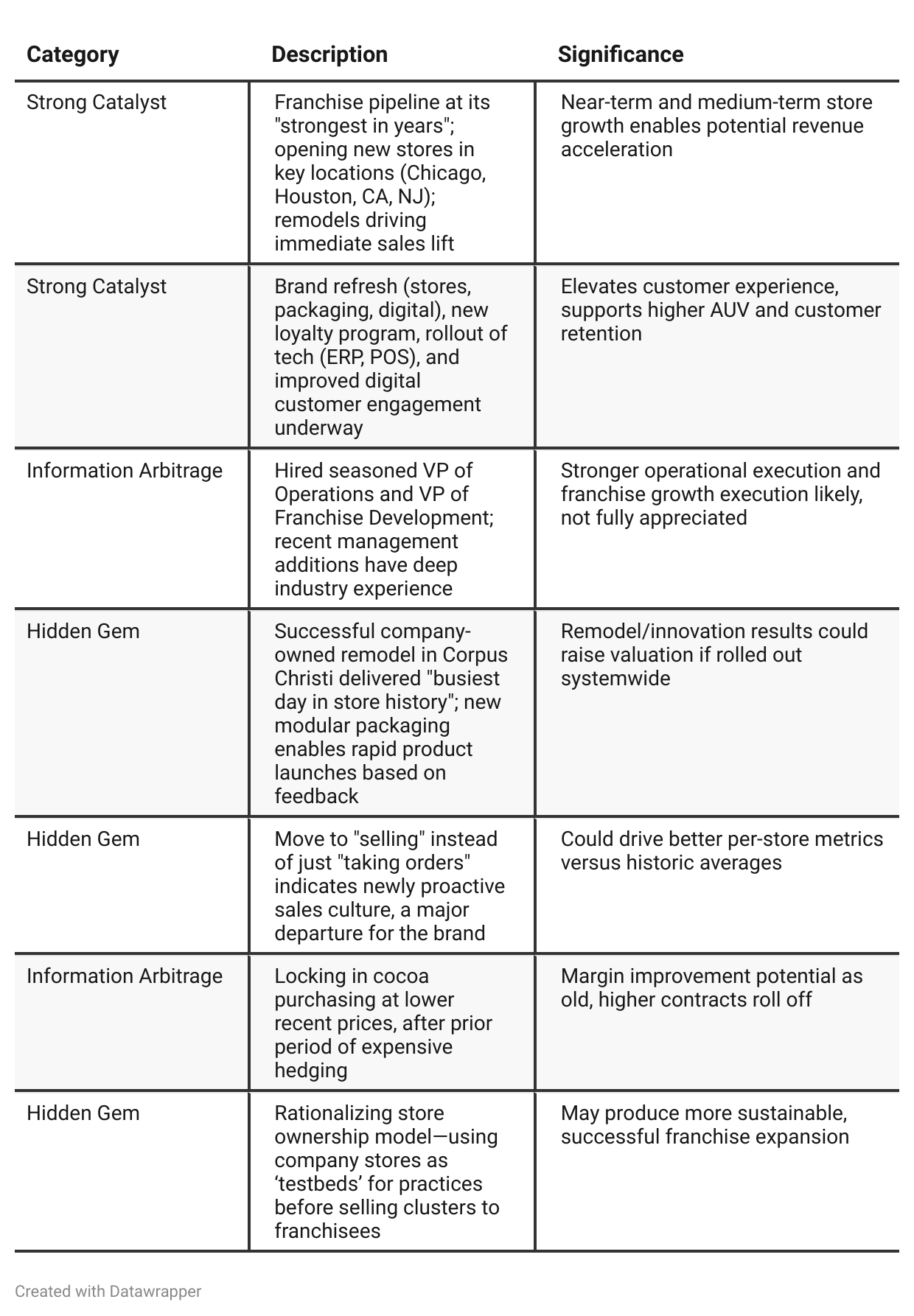

Positive Insights

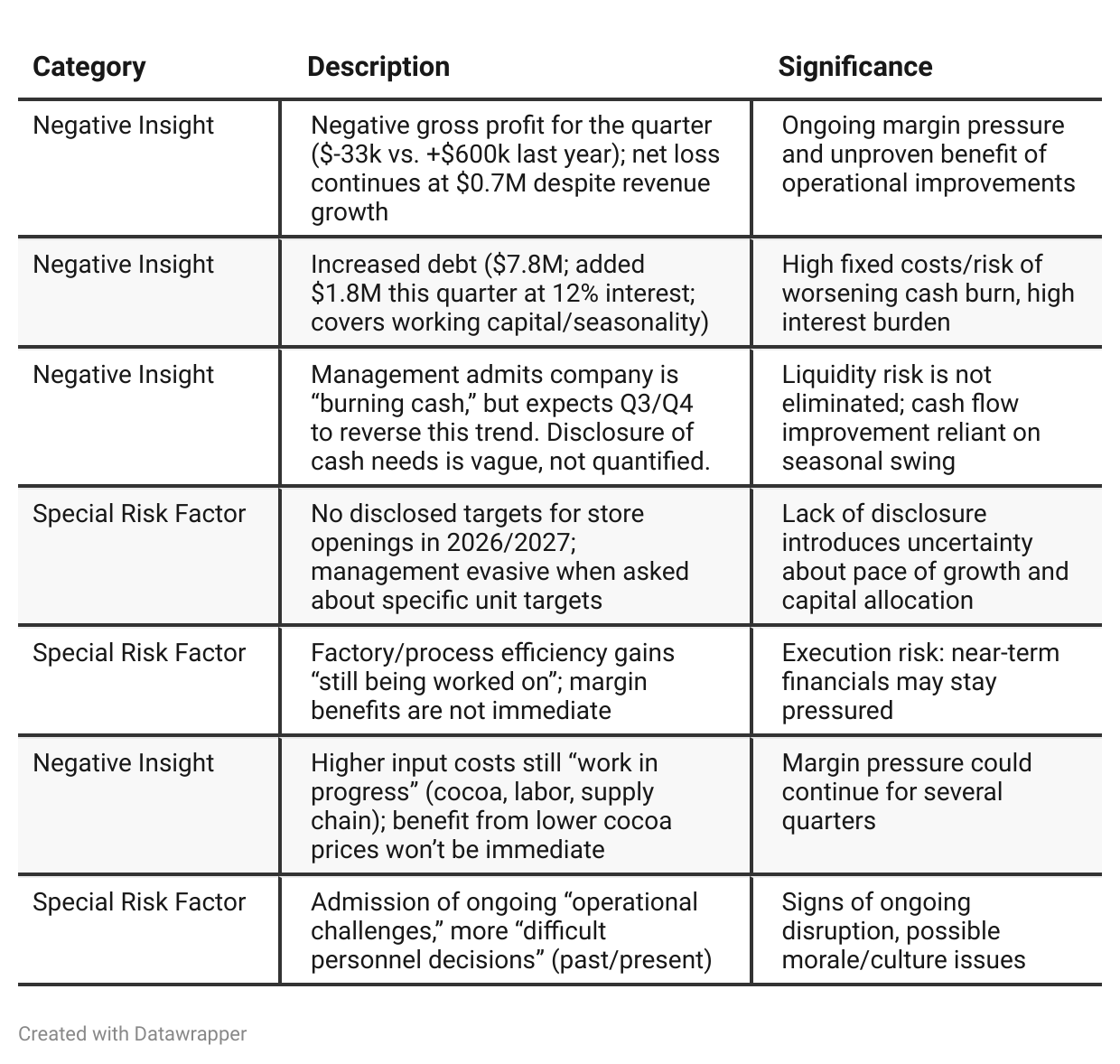

Negative Insights

Tariff Risk

Transcript mentions NO direct discussion of U.S. tariffs, trade policies, or related mitigation strategies.

No impacts, plans, or risks from tariffs, customs, or shifting global supply chains are discussed.

Implication: Investors should monitor future calls/filings for any updates in this area, particularly if supply chain or international expansion accelerates.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2026: RMCF transitions from “rebuilding” to “executing,” with the foundation laid in tech, people, process—finally turning the corner with EBITDA moving positive and franchisee/disciplined growth strategies showing early fruit. The company’s main message is “we are putting the past behind us and the work is now visible.”Q2 2026: The company doubles down on operational discipline, hands-on execution, and deliberate expansion. Strategic hires bolster execution, and the move to energetic, measured expansion leverages new tools and hard-won internal changes. The narrative is less about “potential” and more about “transformation delivering real results—but not without challenges.” Messaging is more mature: “We’re in the hard part now—proving the model works, scaling it, and managing risks around cash, margins, and execution.”

Year-over-year comparison

Q2 2025: Rocky Mountain Chocolate Factory is a brand-in-transformation with management investing in infrastructure, leadership, and foundational reforms. Most initiatives—from branding to technology to franchise systems—are in pilot or early phases. The messaging is focused on preparation, setting the stage, and gathering momentum. Risks are managed by careful liquidity, cost controls, and operational discipline.

Q2 2026: One year later, the company message is about execution, discipline, and measurable performance. More operator-centric language is used, with confidence in both the people (“best team we’ve ever had”) and the playbook (“from planning to performance”). Franchise and company store growth has more substance, tied directly to empirical evidence of remodel impact and new unit ramp. Challenges (cash burn, debt, negative margins) are not hidden, but addressed with action plans—showing the stakes are higher, but also that management is “in the arena.” The narrative is one of a company moving from “getting ready and fixing” to “doing and scaling,” with ongoing risks but a stronger base for value creation.

Final Takeaway

Rocky Mountain Chocolate Factory is in a restructuring/early growth phase, focusing on revitalizing its brand, digital presence, and operational foundation with experienced leadership and a more disciplined approach to unit growth. While there are strong potential catalysts from new store openings, remodels, and digital engagement, the business is not yet through the financial “danger zone”: margins are negative, cash burn and leverage are elevated, and the speed of turnaround is not fully transparent. Execution—especially over the next two quarters—will be critical. Verdict: Hold, with possible upside if operational gains drive margin improvement in the near-term, but with real downside if cash burn persists.