Rocky Mountain Chocolate Factory, Inc. (NASDAQ: RMCF) – Q1 2026 Earnings

Rocky Mountain Chocolate Factory, Inc. (NASDAQ: RMCF) – Q1 2026 Earnings

Earnings Release Date: Jul. 15, 2025

Stock Price: $1.80

Market Cap: $13.9 million

Q1 2026 sales of $6.4 million vs $6.4 million in the prior year

Q1 2026 EPS of ($0.04) vs ($0.26) in the prior year

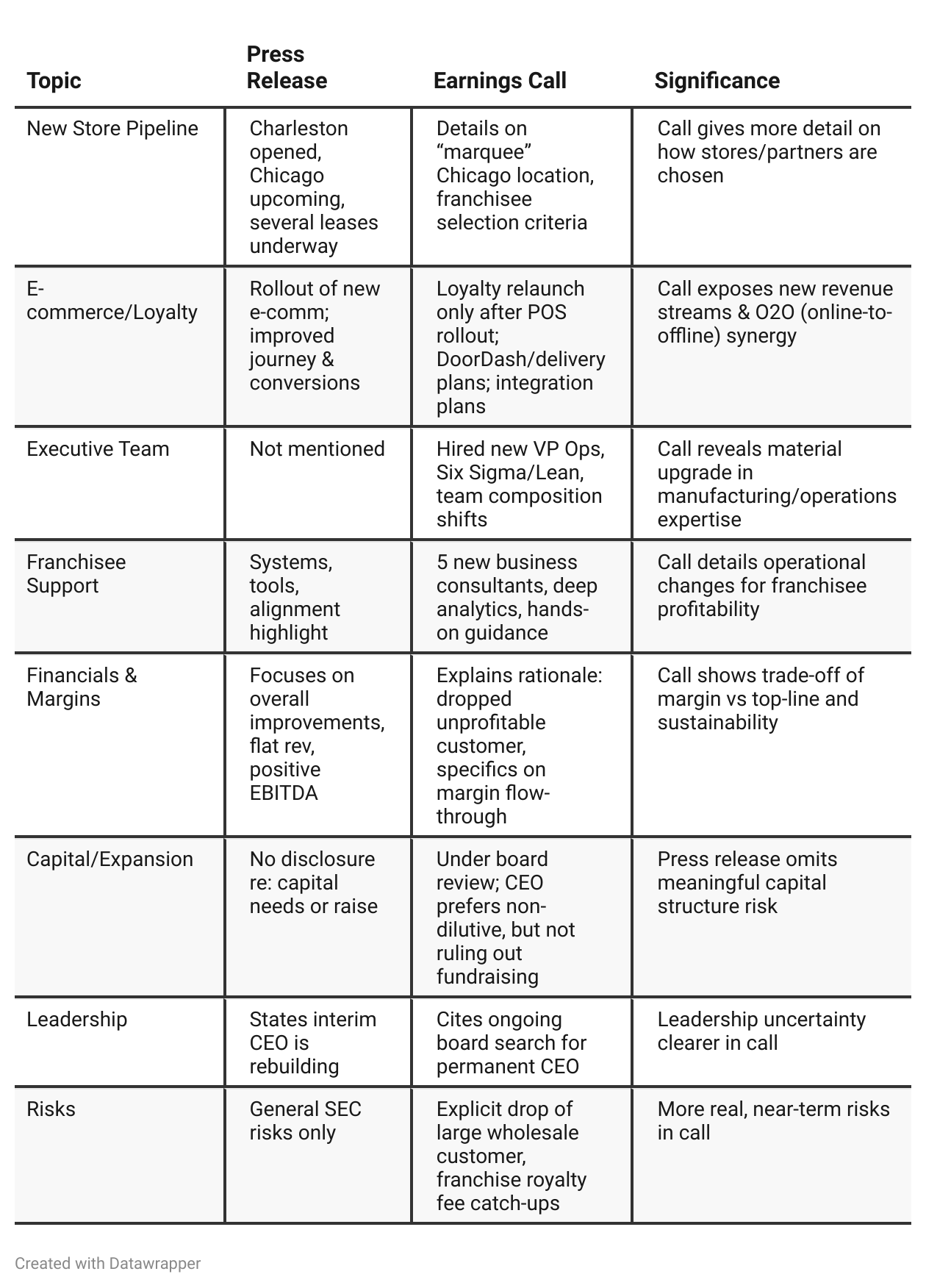

Press Release vs Call Transcript Comparison

Execution over promises: The call emphasizes management’s disciplined, data-driven decision making, willingness to walk away from unprofitable business, and attention to unit-level economics—often a step-change in quality for small/mid-cap franchises.

Transformation still nascent: Both documents stress early days: momentum is improving, but “work still to be done.” Investors should not expect near-term big jumps in EPS or revenue, but gradual improvements.

Franchisee mix may slow growth: Focus on more sophisticated/multi-unit operators plus increased data demands and support may slow net new store growth, but likely to improve unit economics and reduce support costs, key for margin expansion.

Technology rollouts: POS/ERP upgrades are common “inflection” points in chains—if adoption lags, planned e-commerce and loyalty gains may be delayed. However, 100+ store adoption in Q1 is a positive sign.

Investor Communication: The Q&A in the call clarifies several items not disclosed in the release (capital needs, pricing discipline, details on new markets, loyalty, board search), highlighting the value of direct commentary.

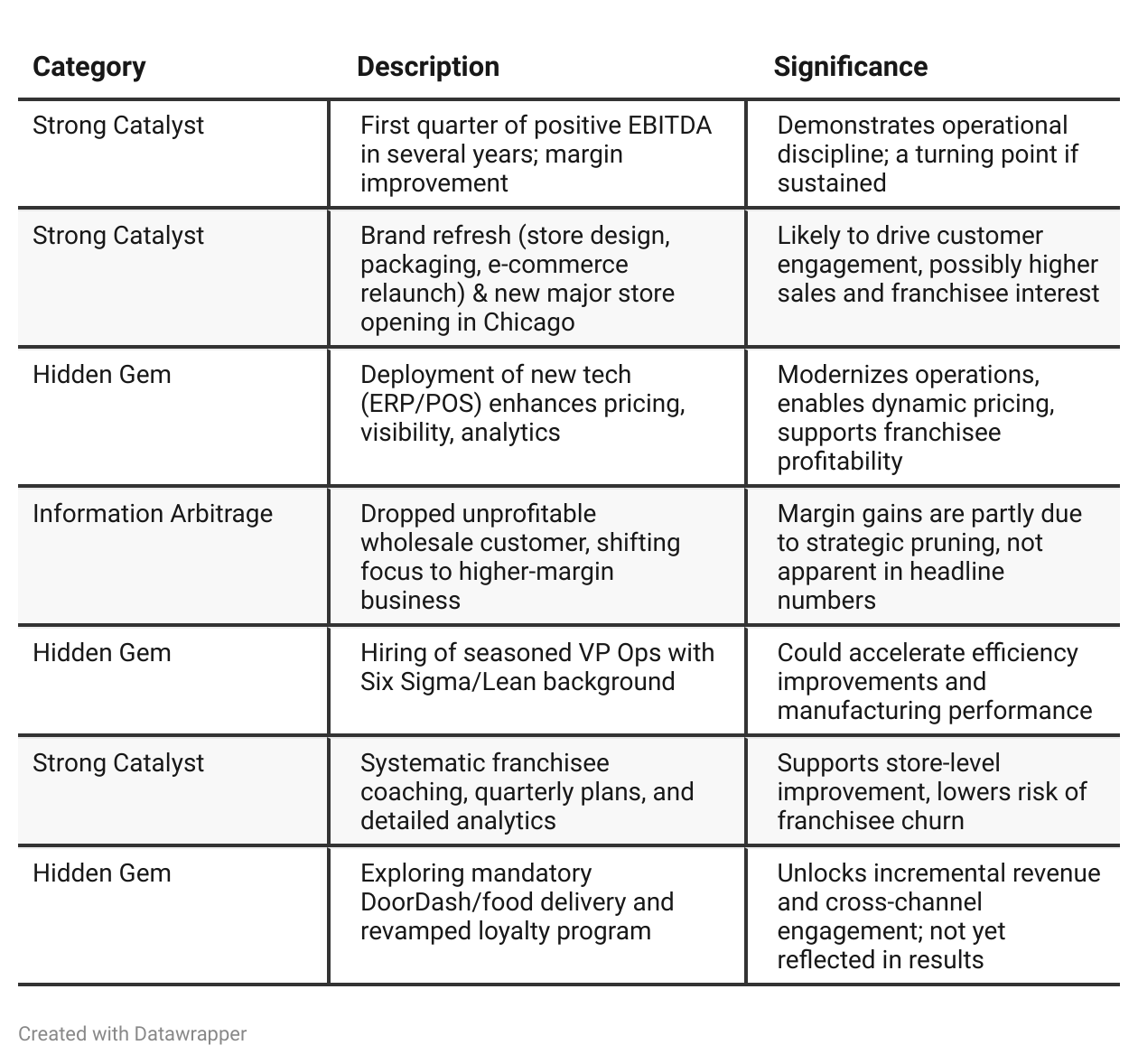

Positive Insights

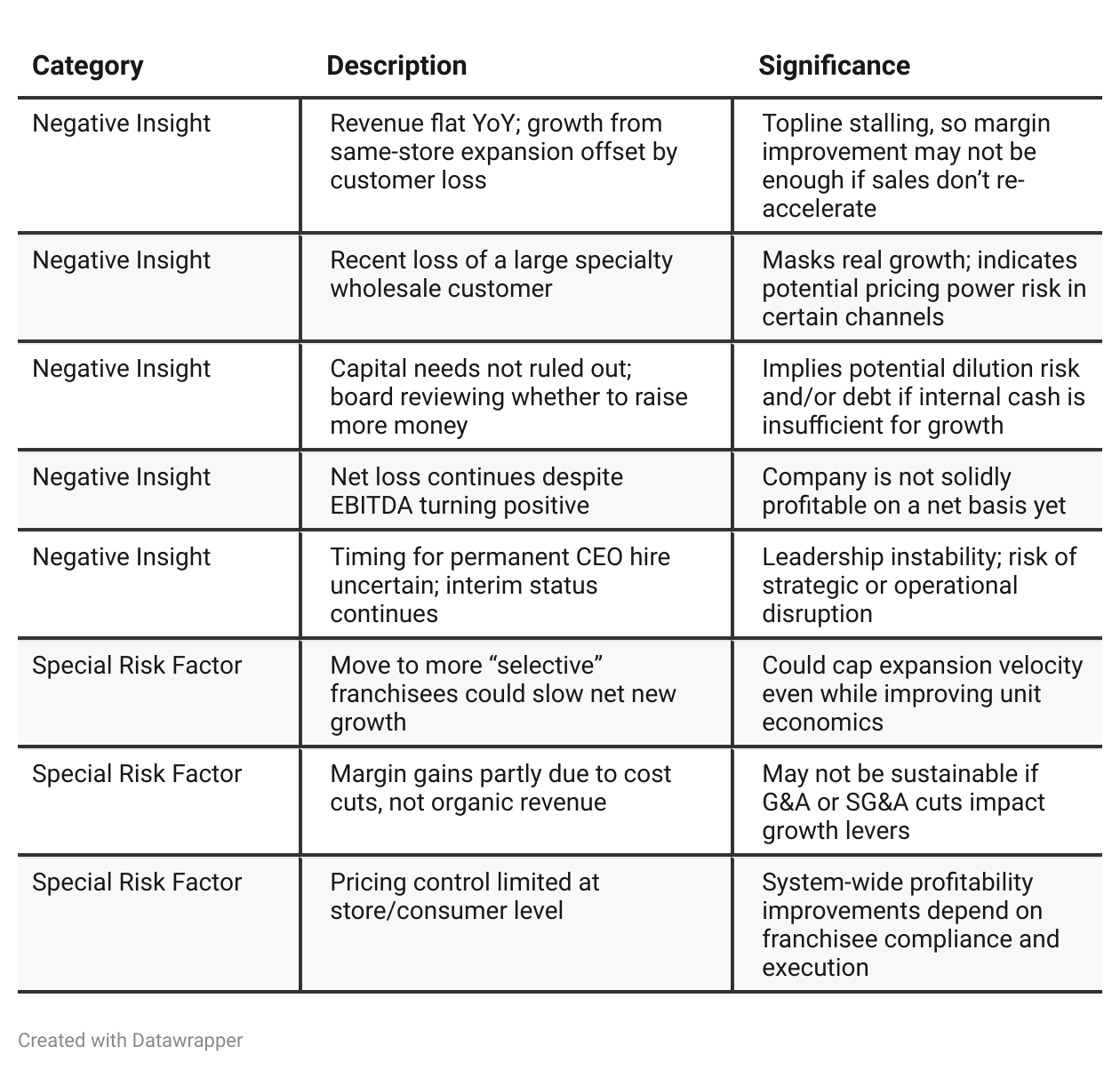

Negative Insights

Tariff Risk

No mention of U.S. tariffs, trade wars, or direct trade policy impact in the entire transcript.

No discussion of supply chain shifts, contract renegotiations, or price adjustments directly attributed to tariffs.

No explicit commentary on input price volatility due to trade (cocoa, imported packaging, etc.)

No evidence of tariffs directly affecting competitive advantage or innovation.

Sentiment Analysis

The overall sentiment toward RMCF is bullish. Investors express optimism about the company's turnaround potential, referencing the possibility of significant stock appreciation and the positive impact of management actions such as dynamic pricing and insider buying. Multiple comments indicate personal investment decisions based on the belief in future growth, with several viewing the stock as a potential multibagger. While there are isolated concerns, the prevailing tone is constructive and reflects confidence in the company's strategy and prospects.

Previous Earnings Call

Quarter-over-quarter comparison

Rocky Mountain Chocolate Factory has shifted from a phase of introspective, foundational rebuilding (Q4 2025) to one of outward-looking execution and scalable improvement (Q1 2026). In the earlier call, leadership was candid about legacy problems—supply chain weaknesses, unprofitable partnerships, and the need for a cultural reset—and detailed rigorous steps to address these while laying the groundwork for tech-driven operational improvements. By Q1 2026, the company is assertively moving from fixing to building: reporting tangible margin gains, achieving positive EBITDA, and rolling out a refreshed store model and brand identity. The narrative is more confident, with management now focused on franchisee expansion, technology-driven profit optimization, and new revenue streams (e-commerce, delivery, loyalty programs). However, unresolved leadership stability and looming capital needs signal that the transformation, while progressing, carries ongoing risk. The company’s story has moved from hopeful repair to early signs of stabilization and potentially sustainable growth—contingent on continued disciplined execution and resolution of funding and leadership uncertainties.Year-over-year comparison

From Q1 2025 to Q1 2026, Rocky Mountain Chocolate Factory’s narrative has evolved from crisis response and foundation rebuilding to tangible performance improvement and operational discipline. One year ago, management’s tone was one of transparent reckoning, focused on diagnosing past failures, restoring leadership, and rebuilding the business framework with new systems, capital, and franchise strategies. The company was still battling lingering store contractions, liquidity issues, and cultural reset.

By Q1 2026, the narrative is one of "turning a corner": the operational foundation (POS/ERP, talent, strategic partners) is in place, and the company has moved to “execution mode.” Positive EBITDA, rising margins (despite flat sales), and real-time store-level analytics mark measurable results. Franchisee enthusiasm and system upgrades lead the story, accompanied by a new and bolder approach to digital and delivery channels. Management now speaks with more confidence, though it candidly notes unresolved leadership transition and the possibility of future capital needs.

Final Takeaway

Rocky Mountain Chocolate Factory is in an operational turnaround phase, with an intensified focus on margin optimization, technology upgrades, and franchisee support. Positive EBITDA and cost discipline are early signs of improvement, but flat sales, capital structure uncertainty, and leadership transition remain material risks. The pathway to upside lies in proving the new store model, capturing digital revenue, and clarifying capital needs. Execution—particularly on growth and permanent leadership—will be critical. Verdict: HOLD, with upside if topline accelerates and risk if more capital must be raised or leadership instability persists.