Richardson Electronics, Ltd. (NASDAQ: RELL) – Q1 2026 Earnings

Richardson Electronics, Ltd. (NASDAQ: RELL) – Q1 2026 Earnings

Earnings Release Date: Oct. 08, 2025

Stock Price: $9.84

Market Cap: $121.9 million

Q1 2026 sales of $54.6 million vs $53.7 million in the prior year

Q1 2026 EPS of $0.13 vs $0.04 in the prior year

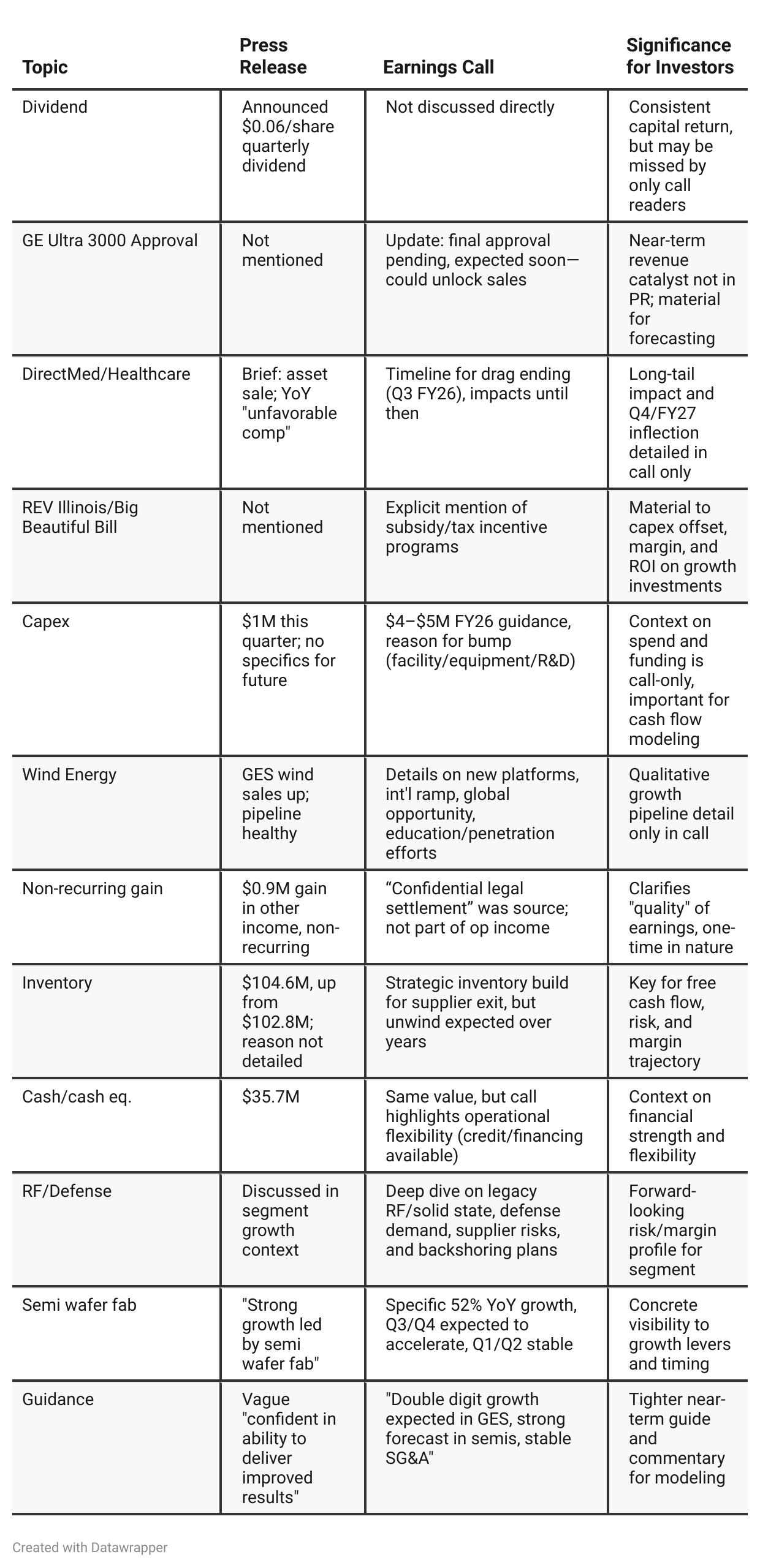

Press Release vs Call Transcript Comparison

Visibility/Transparency: The press release fulfills regulatory disclosure needs but omits crucial timelines, pipeline health, and color on catalysts and risk mitigation that are highly relevant to investors evaluating future results.

Quality of Earnings: Press release headline of tripled operating income is accurate, but much of the absolute increase is non-recurring (settlement gain) as disclosed only in the call—future quarters may not repeat this benefit.

Segment Strategy: The call provides granularity on how RELL is shifting capex/hiring toward green energy and semi/wafer fab, with less clarity in PR; wind, semi, and defense are positioned as growth pillars.

Capital Allocation: Only in the call do we see the strategic use and expected easy attainment of state incentives, which reduce risk/boost ROI for major new investments (LaFox demo site, expansion).

International Opportunity: Call clarifies international wind growth is slower but promising, important for sizing upside relative to current revenue mix.

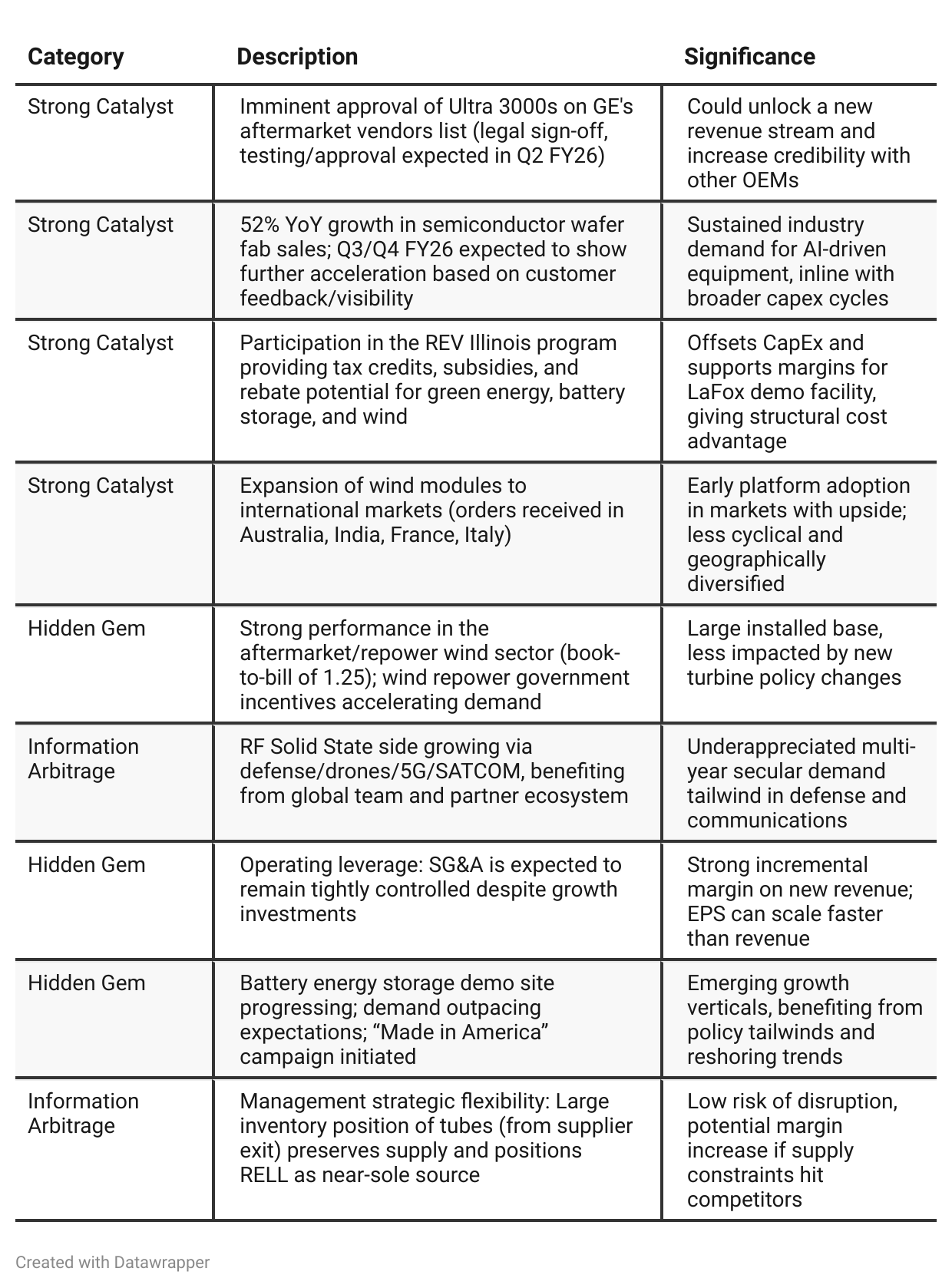

Positive Insights

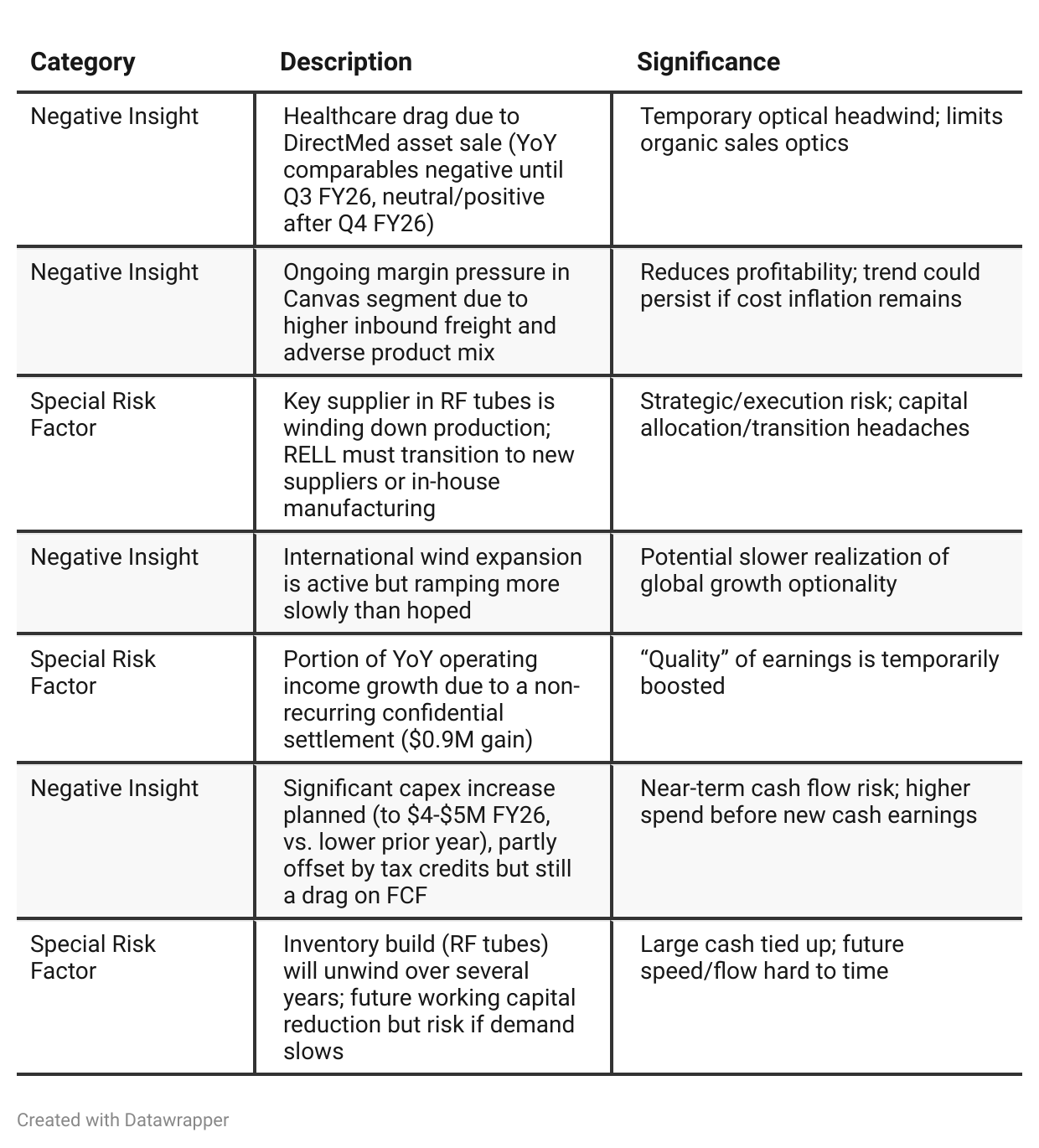

Negative Insights

Tariff Risk

Mentions of U.S. Tariffs/Trade Policy: No explicit reference to U.S. tariffs or trade policy risk/impact in this transcript.

Implied Risk Surface:

Rising inbound freight costs (Canvas segment) possibly related to broader supply chain costs, but no direct link to tariffs specified.

Management’s “Made in America” campaign and U.S. expansion (LaFox, Texas) could signal strategic positioning to reduce tariff exposure if trade tensions escalate, but this is not explicit.

Actions/Outlook: No clear actions or comments specific to tariffs, so investors should monitor future disclosures or filings.

Tariffs or Trade Policy Mentions:

Direct Mentions: None in the Q1 FY26 call transcript.

Indirect Impacts: Elevated inbound freight costs in the Canvys segment could, in some part, be a result of trade policy or logistics disruptions, but management does not specify tariffs or related measures.

Strategic Mitigation: The company highlights “Made in America” positioning, expanded U.S. manufacturing, and utilization of state/local subsidies (REV Illinois), all of which may reduce exposure to future tariff headwinds, but no explicit commentary is given.

Competitive Impact: No discussion of any relative advantage or disadvantage stemming from potential tariffs on major competitors.

Investor Guidance on Tariffs/Trade:

Investors should remain alert to future earnings calls and filings for any change in tone around supply chain costs, global logistics, or tariff policy, especially given rising global trade tensions.

Monitor whether management cites further increases in freight or production costs, as these may eventually be linked to external tariff or trade disruptions.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q4 FY25 was a quarter of transition, with Richardson Electronics highlighting their navigation through major strategic changes: the divestiture of healthcare assets, double-digit growth in wind and semi, and a strong cash position. Management’s tone was celebratory yet realistic—acknowledging that external pressures (tariffs, global instability) remained, but operational discipline and new technology partnerships set a strong foundation for FY26 and beyond.In Q1 FY26, the narrative advances from foundation-building to execution readiness. The tone is practical, with new growth drivers—such as the imminent GE approval, global pipeline expansion, and state subsidy wins—firmly in focus. Management openly addresses temporary headwinds (earnings quality, healthcare drag, margin mix, supplier risks) while expressing a disciplined commitment to capital allocation, cost control, and converting the built pipeline into realized growth. Guidance is more nuanced, with specific timelines and acknowledged variabilities.

Year-over-year comparison

In Q1 FY2025, Richardson Electronics was in a rebuilding and recovery mode, having just returned to year-over-year growth after a difficult period marked by gross margin compression, inventory build-up, and economic/macro uncertainty. Leadership’s messaging was focused on emerging positives: green energy and semi-fab growth, pipeline replenishment, and cautious expansion into international markets. The overriding theme was patience and pipeline development, with a careful approach to expenses and cash.

By Q1 FY2026, the narrative shifted to actionable execution and operational confidence. Leadership is now handling live transitions (healthcare business sold, tube supplier withdrawal), leveraging government and local policy incentives, and focusing on generating sustainable profitability and high-quality growth. Management is more explicit about both opportunities and risks, including one-time financial items and temporary headwinds. There’s a move from selling a story of “recovery and potential” to demonstrating a platform for “scalable, diversified growth”—with a far greater focus on how execution and operational discipline will drive results over the next year and beyond.

Final Takeaway

Richardson Electronics (RELL) is in a transition and growth phase, focusing on engineered green energy solutions, semiconductor fab, wind repower, and aftermarket defense markets. Positive catalysts are on the near-term horizon, particularly with expected new product/channel approvals and policy-driven demand. However, optical and execution risks (healthcare drag, supplier transition, temporary margins) temper the near-term outlook. Execution on key pipeline conversions and RF business strategy will be critical for re-rating. Verdict: Hold with positive bias—a move to Buy contingent on clear, visible operational follow-through and normalization of earnings quality.