Richardson Electronics, Ltd. (NASDAQ: RELL) – Q4 2025 Earnings

Richardson Electronics, Ltd. (NASDAQ: RELL) – Q4 2025 Earnings

Earnings Release Date: Jul. 23, 2025

Stock Price: $9.78

Market Cap: $120.7 million

Q4 2025 sales of $51.9 million vs $47.4 million in the prior year

Q4 2025 adjusted EPS of $0.12 vs $0.02 in the prior year

Full year sales of $208.9 million vs $196.5 million in the prior year

Full year adjusted EPS of $0.22 vs $0.03 in the prior year

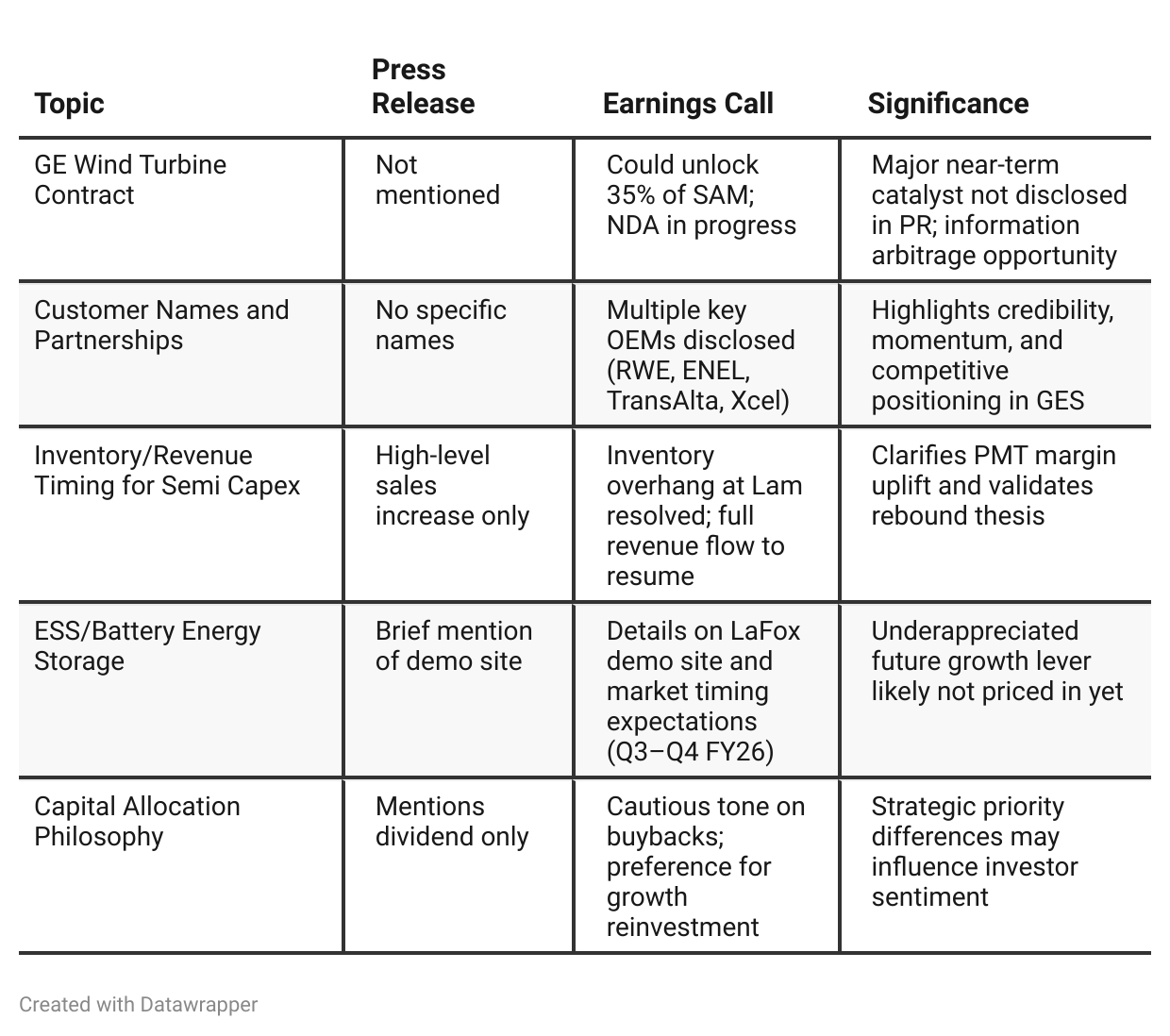

Press Release vs Call Transcript Comparison

The press release presented a solid, steady-growth narrative with a focus on financial metrics, segment sales growth, and operational execution. However, the earnings call revealed deeper strategic dynamics—especially around customer wins (e.g., RWE, GE), market expansion (Europe, Asia), the Lam rebound, and infrastructure investments (ESS demo site, Sweetwater design hub)—that were not mentioned in the release.

These incremental insights give investors a much clearer picture of where Richardson Electronics is headed and suggest that the press release may understate both the near-term and long-term growth potential. Investors relying solely on the press release may miss key inflection points and underappreciated catalysts.

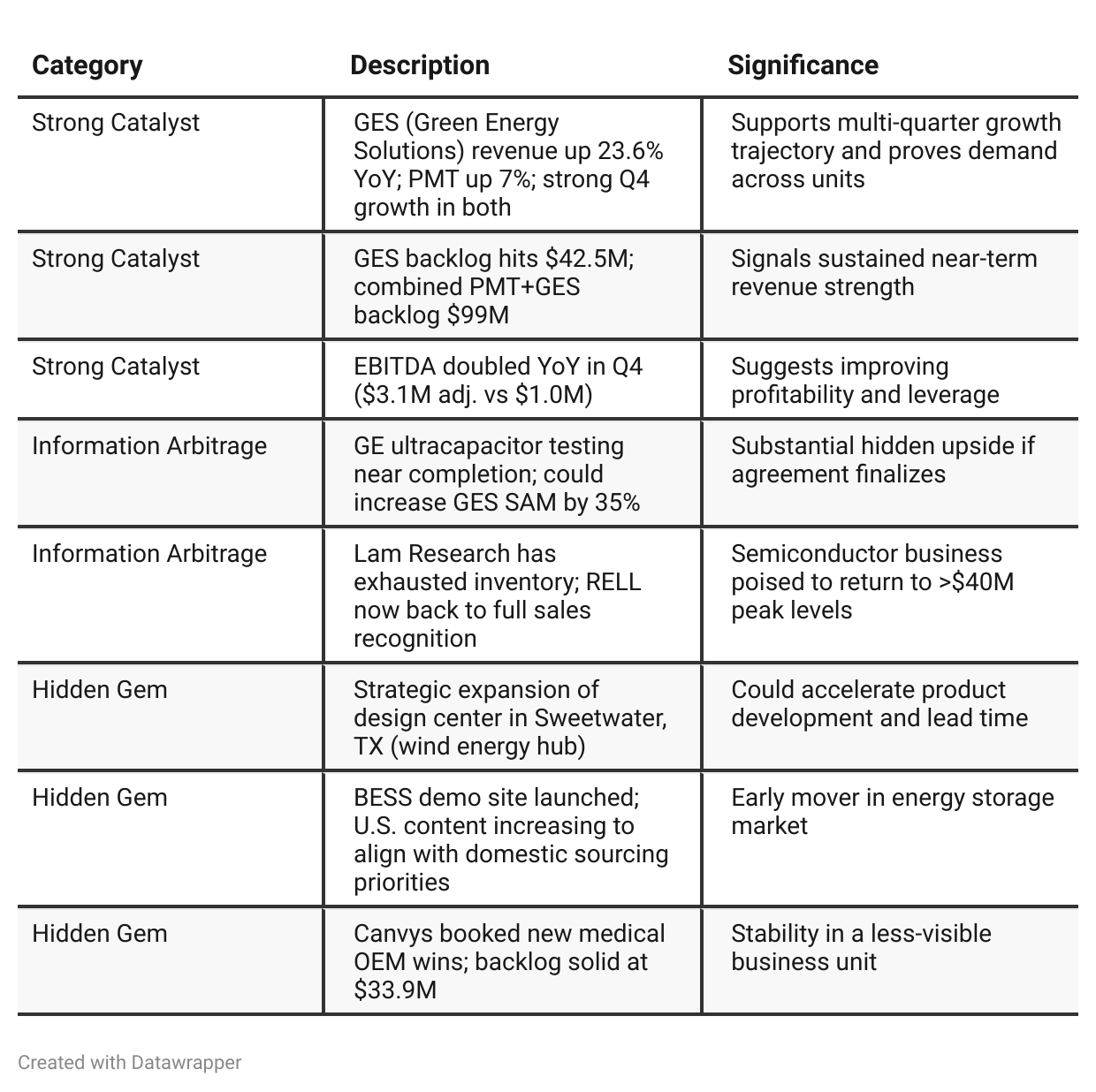

Positive Insights

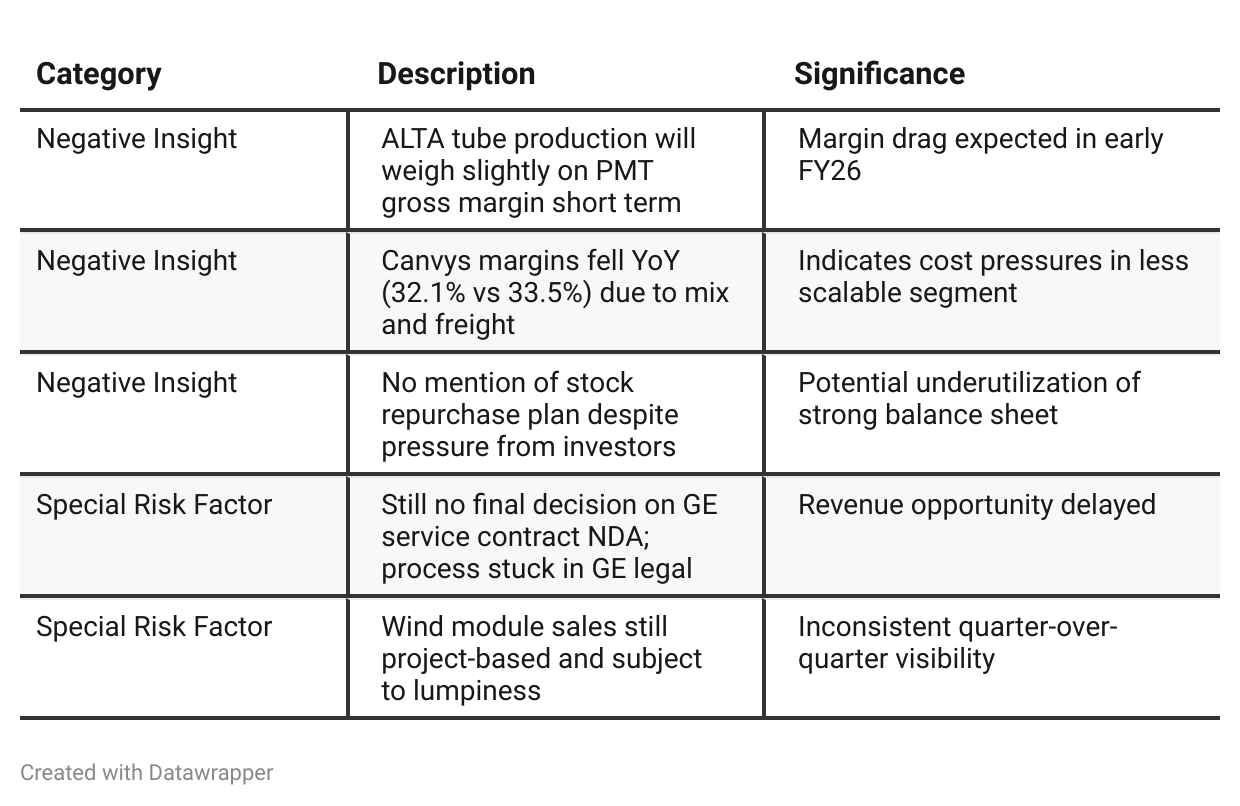

Negative Insights

Tariff Risk

Mentions of Tariffs:

Tariff risks were explicitly cited as a concern, particularly in power management and energy solutions.

Company is adjusting global supply chain to reduce China exposure—<5% of GES wind content now from China.

Expanding U.S.-based manufacturing to mitigate exposure.

Focus shifting to markets with favorable subsidies (Illinois, CA, MA); federal subsidies seen as less reliable.

Mitigation Actions:

Supply chain adjustment (non-China sourcing); localization of content; new domestic manufacturing partnerships; new design center in Sweetwater, TX.

Forward-Looking Statements on Tariffs:

Management views disruptions as potential growth opportunities. They're positioning to benefit from companies needing to nearshore production and align with U.S. sourcing rules.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q3 and Q4 FY2025, Richardson Electronics transitioned from a cleanup and repositioning narrative to a confident execution phase.

The Q3 call centered around explaining the Healthcare divestiture, managing one-time charges, and reiterating its refocused commitment to GES and PMT. By Q4, the company was clearly operating in forward gear—highlighting specific new wins, expanding into global markets, formalizing infrastructure to accelerate product timelines, and positioning for further growth in FY’26.The tone became more assertive, operational plans were more detailed, and the potential for scale became more evident—especially in wind energy and semiconductor wafer fab. The company now appears structurally cleaner, financially stronger, and more focused on margin-accretive opportunities with expanding total addressable markets.

Year-over-year comparison

From Q3 to Q4 FY25, Richardson Electronics’ story evolved from strategic repositioning to execution-driven growth.

In Q3, the tone was largely transitional—emphasizing the divestiture of Healthcare and setting the stage for a GES/PMT-centric future. By Q4, the tone sharpened toward operational momentum, with evidence of execution: backlog expansion, new customer wins, margin improvement, and internal capability building.The company’s strategic messaging is coalescing around a clearly defined dual-engine growth model (GES + PMT) with tailwinds from energy transformation, reshoring, and advanced component demand. Although not all uncertainties are resolved (e.g., M&A, tariffs), management now appears more comfortable leaning into a proactive posture with targeted investments, select global expansion, and product pipeline acceleration.

Final Takeaway

Richardson Electronics is in a growth phase, with strong momentum in Green Energy and early signs of recovery in its high-margin semiconductor business.

While tariff pressures and GE delays introduce some uncertainty, the backlog, cash flow, and customer traction signal underlying strength. Execution on the GE integration, BESS ramp, and global expansion will determine how much of that potential materializes in FY26.

Verdict: HOLD with upside bias, especially if near-term catalysts unlock trapped value.