RCM Technologies, Inc. (NASDAQ: RCMT) – Q2 2025 Earnings

RCM Technologies, Inc. (NASDAQ: RCMT) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $23.56

Market Cap: $179.4 million

Q2 2025 sales of $78.2 million vs $69.2 million in the prior year

Q2 2025 EPS of $0.50 vs $0.47 in the prior year

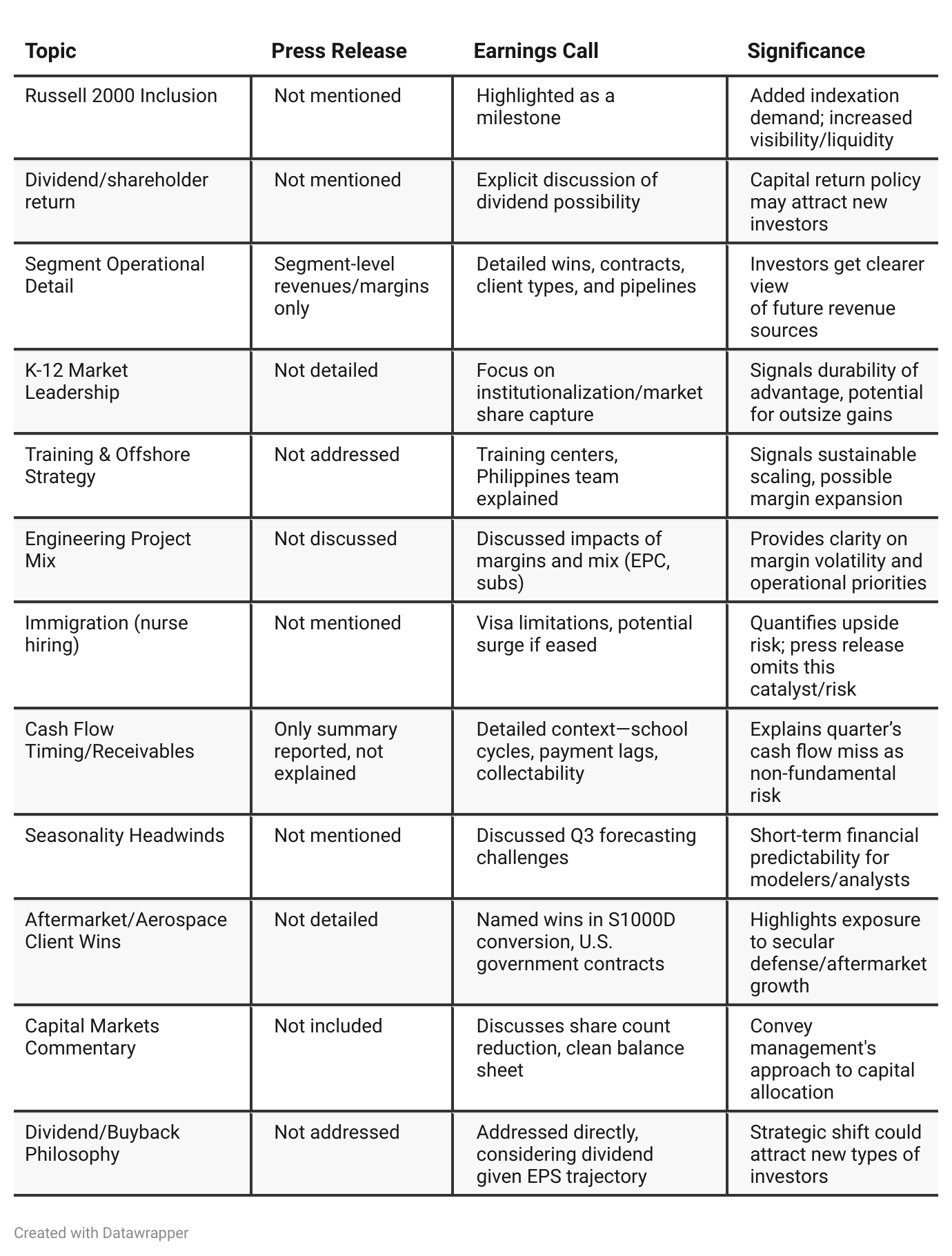

Press Release vs Call Transcript Comparison

Press release is numbers-focused, conservative, and backward-looking (standard for compliance and IR). By contrast, the call is forward-looking, qualitative, and full of color about execution, pipeline, market share, and competitive posture.

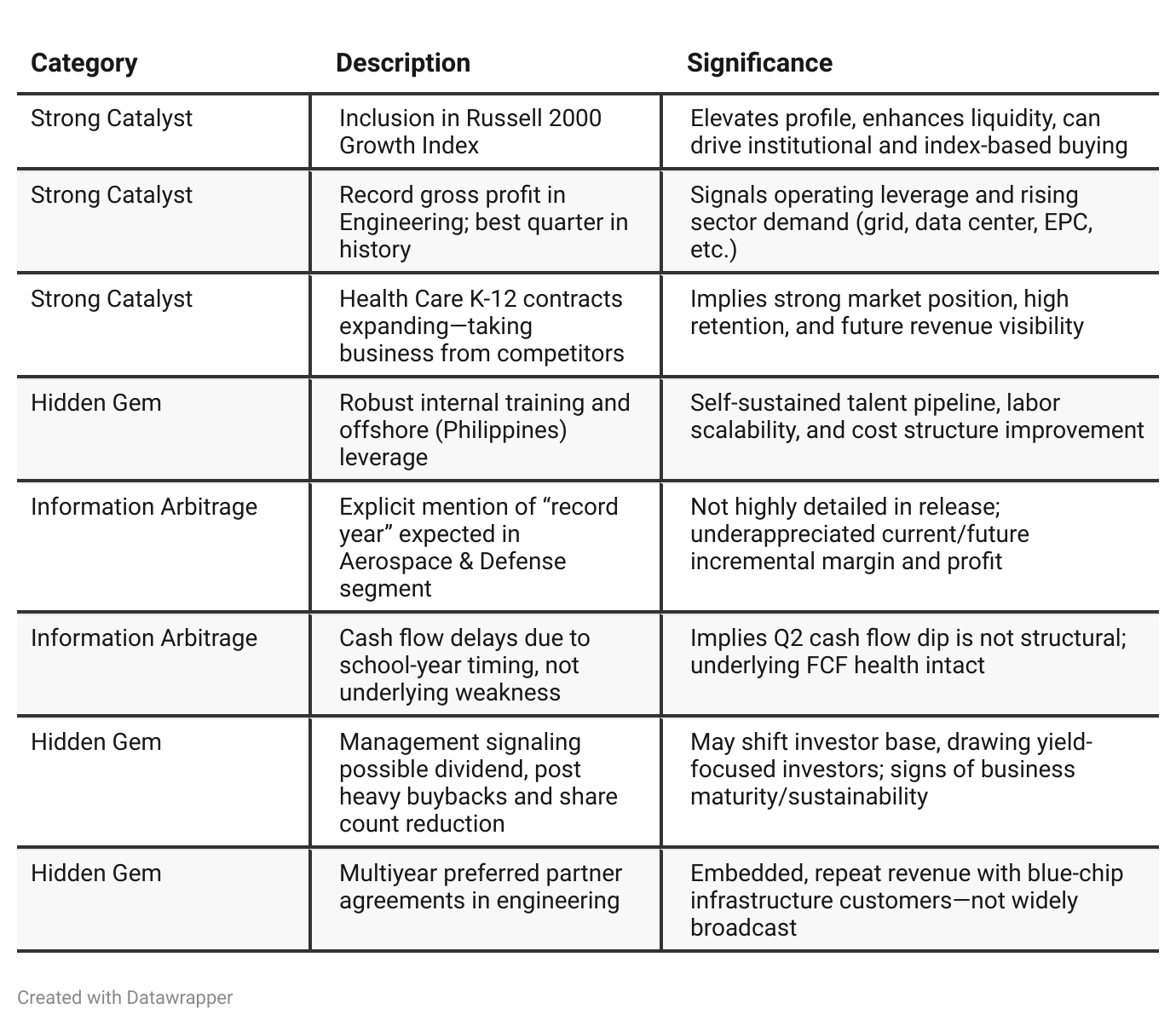

Key investing angle: The earnings call reveals management thinks they are just getting started, pointing to structural industry tailwinds (data center power, K-12 health staffing, aerospace/defense), self-help margin opportunities (offshoring, training, business integration), and external levers (immigration, visibility post-Russell inclusion) that aren’t in the press release.

The call signals comfort with potentially raising capital returns via dividend, due to share shrink and a “balance sheet as a strategic asset”—both strong signals to value/style investors.

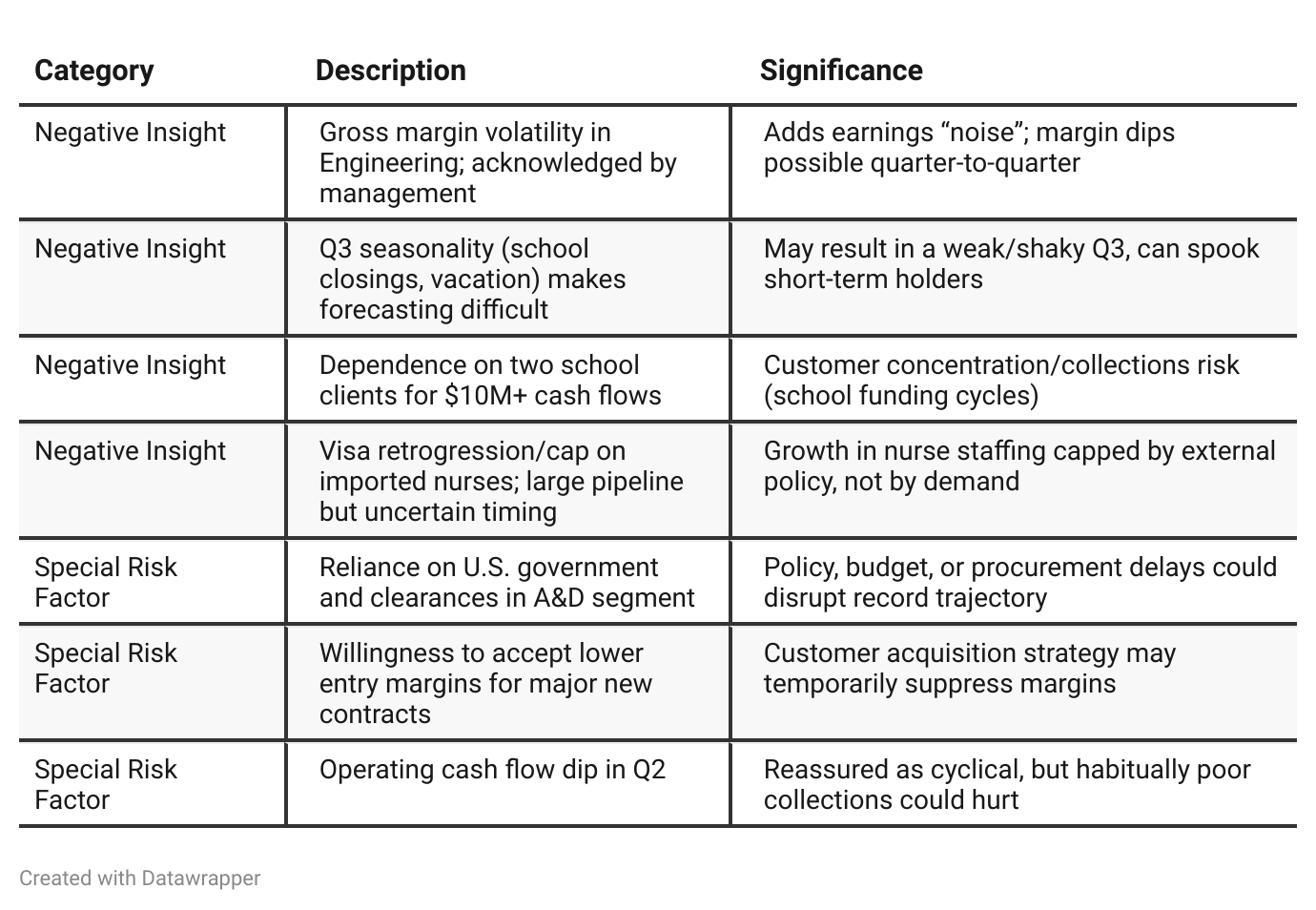

Risks are mostly around timing and near-term variability (margin swings, Q3 seasonality, payment delays), rather than end-market demand destruction.

Positive Insights

Negative Insights

Tariff Risk

There are no explicit mentions of tariffs or U.S. trade policy in the transcript. There are references to supply chain bottlenecks in data center infrastructure and a strategic focus on U.S. governmental/Aerospace contracts (which could have indirect trade/policy sensitivity). However:

No discussion of import duties, tariff-driven cost inflation, or mitigation strategies.

No announced actions like reshoring, renegotiating supplier deals, or shifting customer price burden due to tariff escalations.

No comments on losing or gaining competitive advantage through tariff regimes. Conclusion: Tariff risk does not appear to be a material concern or strategic focus for RCM Technologies at this time, based on the transcript.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: The company’s narrative is deeply rooted in foundational strength—investing in talent, building processes, extending core adjacencies, and maintaining financial discipline. The tone is slightly skeptical about why the market hasn’t rewarded this yet, but patient, focused on long-term compounding and resilience. The message to investors: “Trust that our groundwork and stewardship will soon compound into strong, sustainable outperformance.”Q2 2025: The narrative matures to external validation and execution mode—the foundation has translated into record results, industry recognition (Russell 2000), and aggressive market share wins. Management speaks more openly about their strategic options for rewarding shareholders (dividend, buyback), and addresses both opportunities and “lumpy” risks (collections, margins) with confidence and transparency. The message to investors: “Our strategy is working as intended, we’re ready to accelerate, and are now considering broader value unlocks for our shareholders.”

Year-over-year comparison

Q2 2024: RCM Technologies was deeply focused on platform building—laying operational bricks, making prudent investments, carefully expanding staff, and methodically shifting from pandemic recovery to sustainable, diversified growth. Management was confident but conservative, focused on managing costs, keeping pace with sector trends, and expressing optimism about a strong pipeline, particularly in education and energy. While bullish on growth, they remained guarded about near-term forecasts.

Q2 2025: Twelve months later, the company is operating at a different altitude. The narrative is not just about readiness or potential, but about realized and measurable progress. RCM is winning market share, scaling rapidly, showing record profits, and attaining industry recognition (e.g., the Russell 2000 inclusion). The capital allocation story evolves with a potential dividend and ongoing buybacks. Management communicates a “we’ve arrived” message—unapologetically more ambitious, taking business from the competition, and ready to capitalize on tailwinds with the infrastructure it so carefully built the previous year.

Final Takeaway

RCM Technologies is in a growth and scale phase, capitalizing on secular tailwinds in K-12 health staffing, power infrastructure, and aerospace/defense. Management is executing a disciplined playbook—buybacks, debt reduction, and now evaluating dividends—which may unlock additional investor demand. The company exhibits strong positioning and healthy pipeline momentum, but near-term results may remain seasonal and cash flow lumpy. Investors should monitor contract margin trends, collections, and federal/external policies. Verdict: Buy, with attractive risk/reward as execution and possible capital returns drive upside.