RCM Technologies, Inc. (NASDAQ: RCMT) – Q3 2025 Earnings

RCM Technologies, Inc. (NASDAQ: RCMT) – Q3 2025 Earnings

Earnings Release Date: Nov. 05, 2025

Stock Price: $23.06

Market Cap: $175.9 million

Q3 sales of $70.3 million vs $60.4 million in the prior year

Q3 EPS of $0.30 vs $0.35 in the prior year

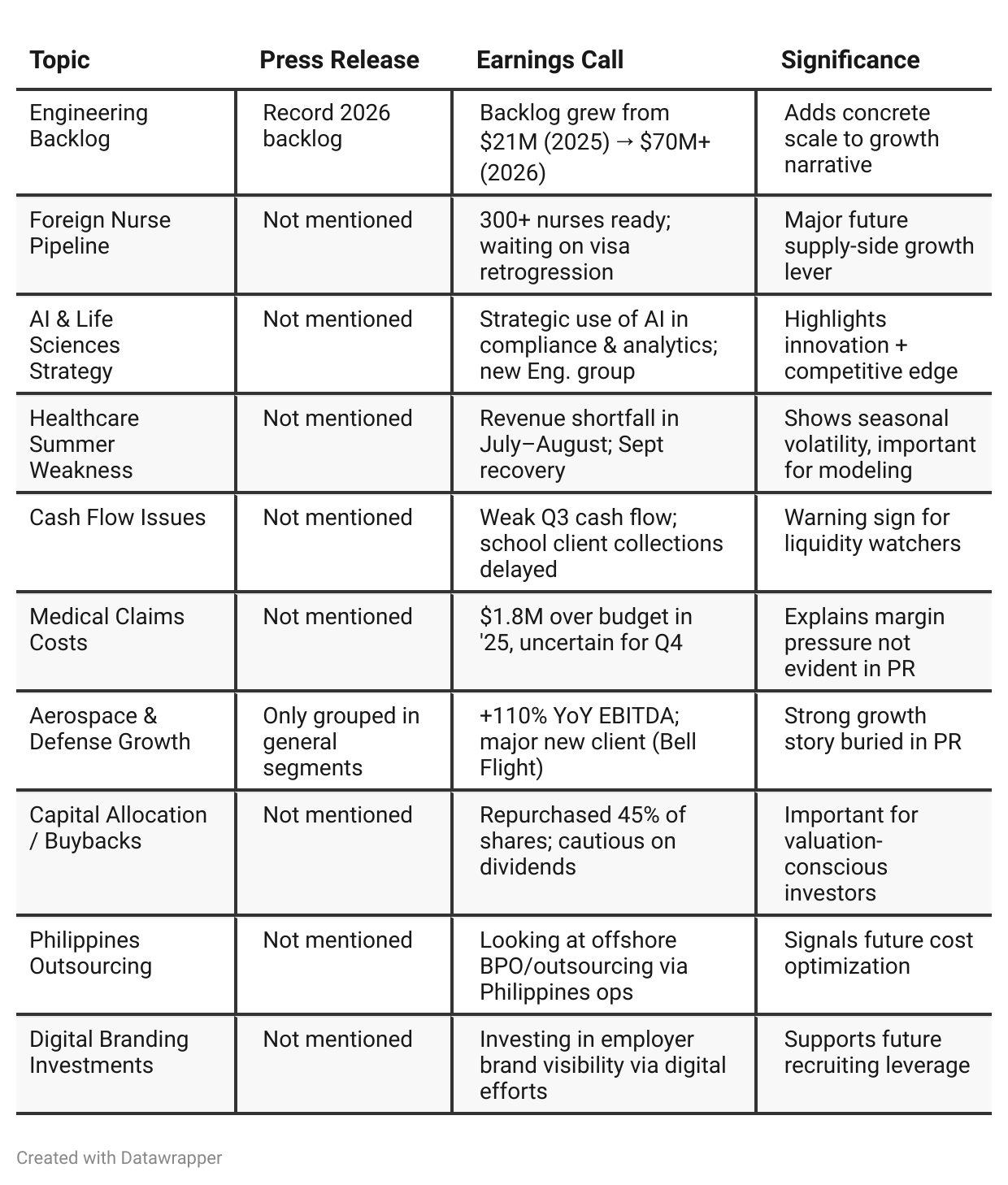

Press Release vs Call Transcript Comparison

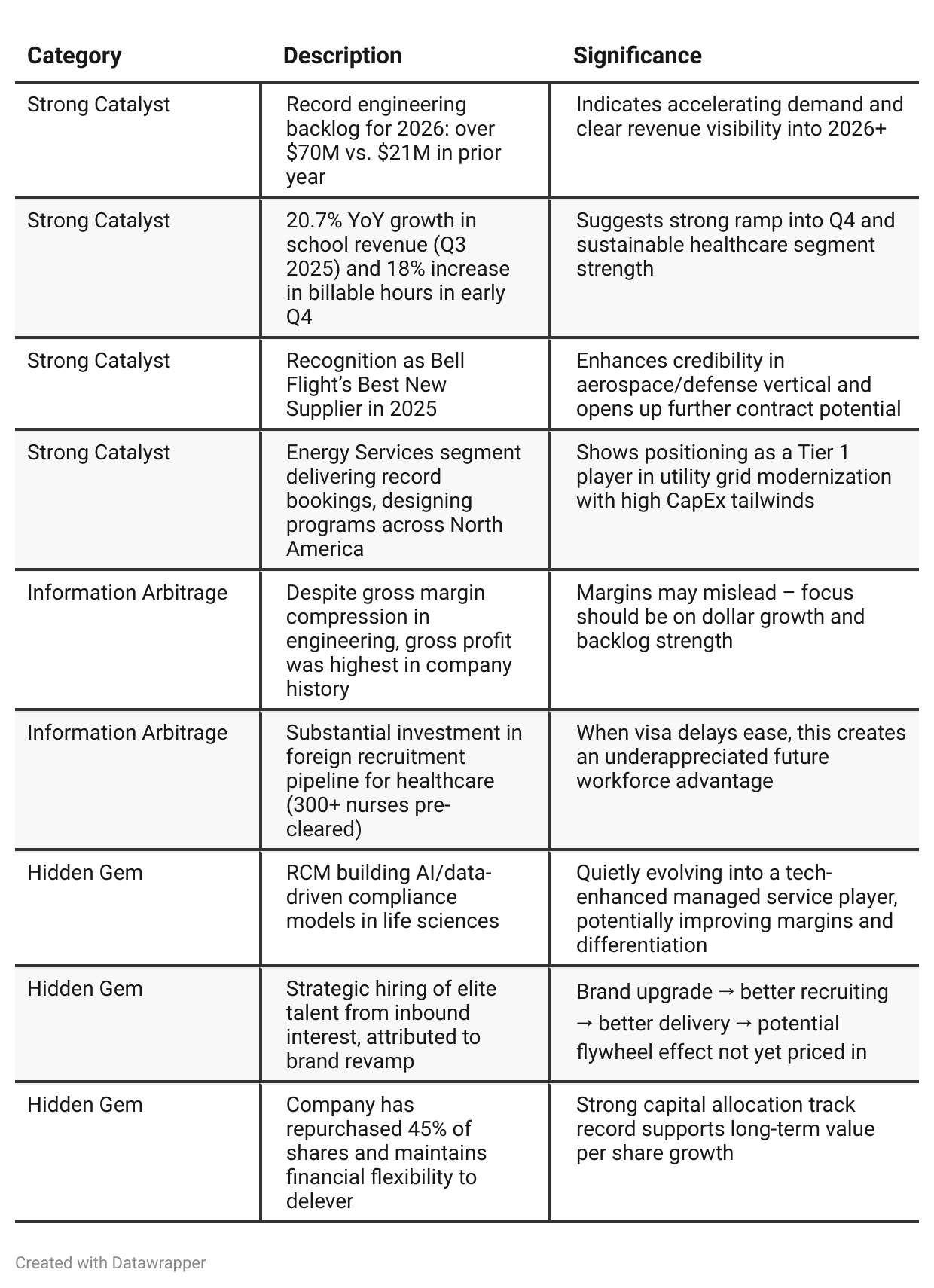

Valuation Insight: Management highlights they’ve repurchased 45% of shares outstanding at ~$8.50 average, arguing shares remain materially undervalued — a key investor signal.

Self-insurance Policy: Confirmed continuation despite volatility in medical costs. Long-term cost-efficiency favored over switching to full insurance — worth tracking for SG&A impact.

Positive Insights

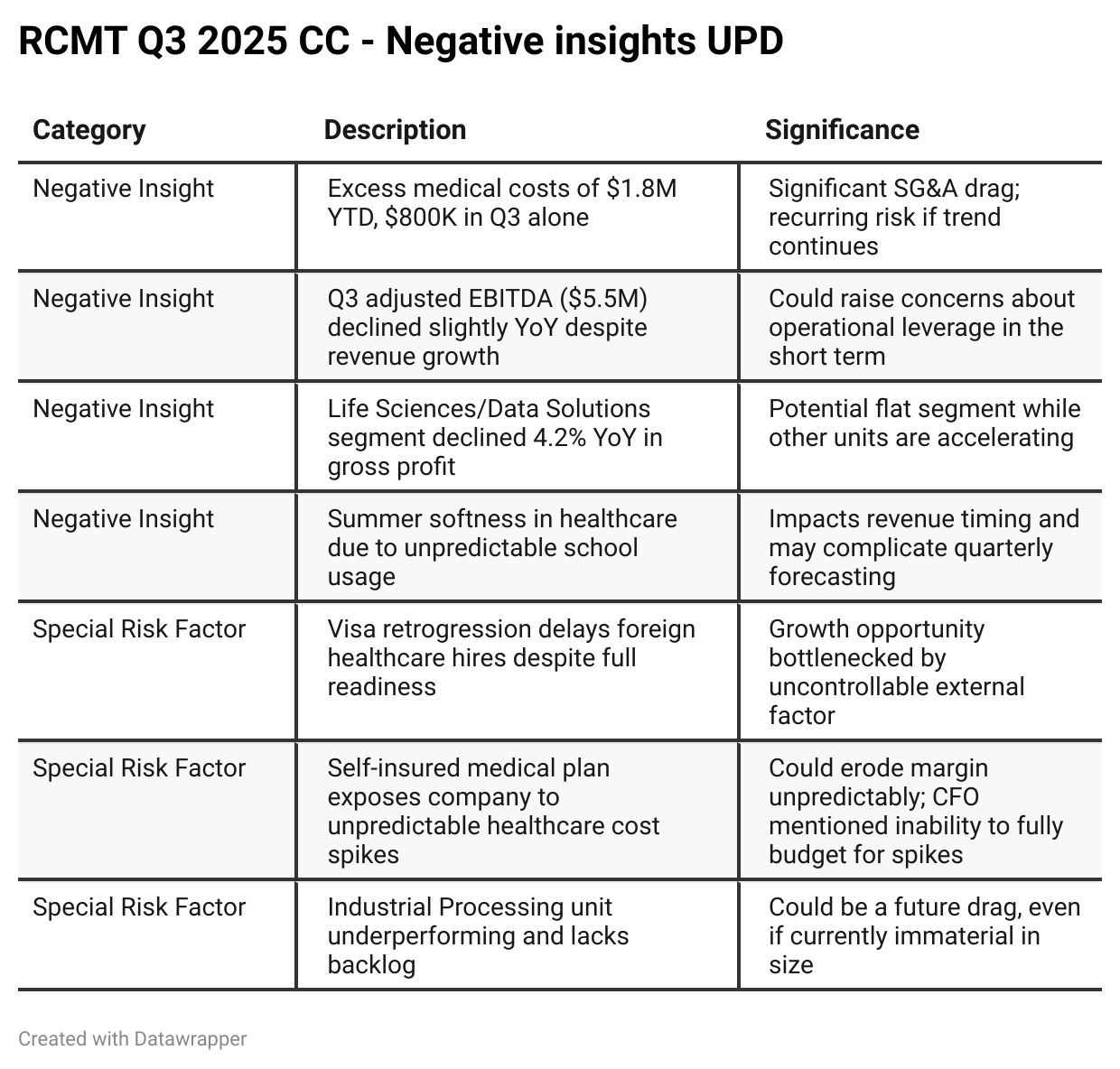

Negative Insights

Tariff Risk

Tariffs were mentioned in the context of life sciences industry disruption, along with favored nation drug pricing and process automation.

Impact: These trends have caused workforce reductions among RCM clients but also led to capital investment in manufacturing, which RCM is now supporting.

RCM’s Mitigation Strategy:

Partnered with an AI-driven validation company to streamline compliance and reduce manufacturing turnaround time.

Launched a dedicated life sciences engineering group to capitalize on the transition.

Outlook:

Management views these disruptions as an opportunity, not a net negative. No direct impact on RCMT’s own supply chain or material cost structure was disclosed.

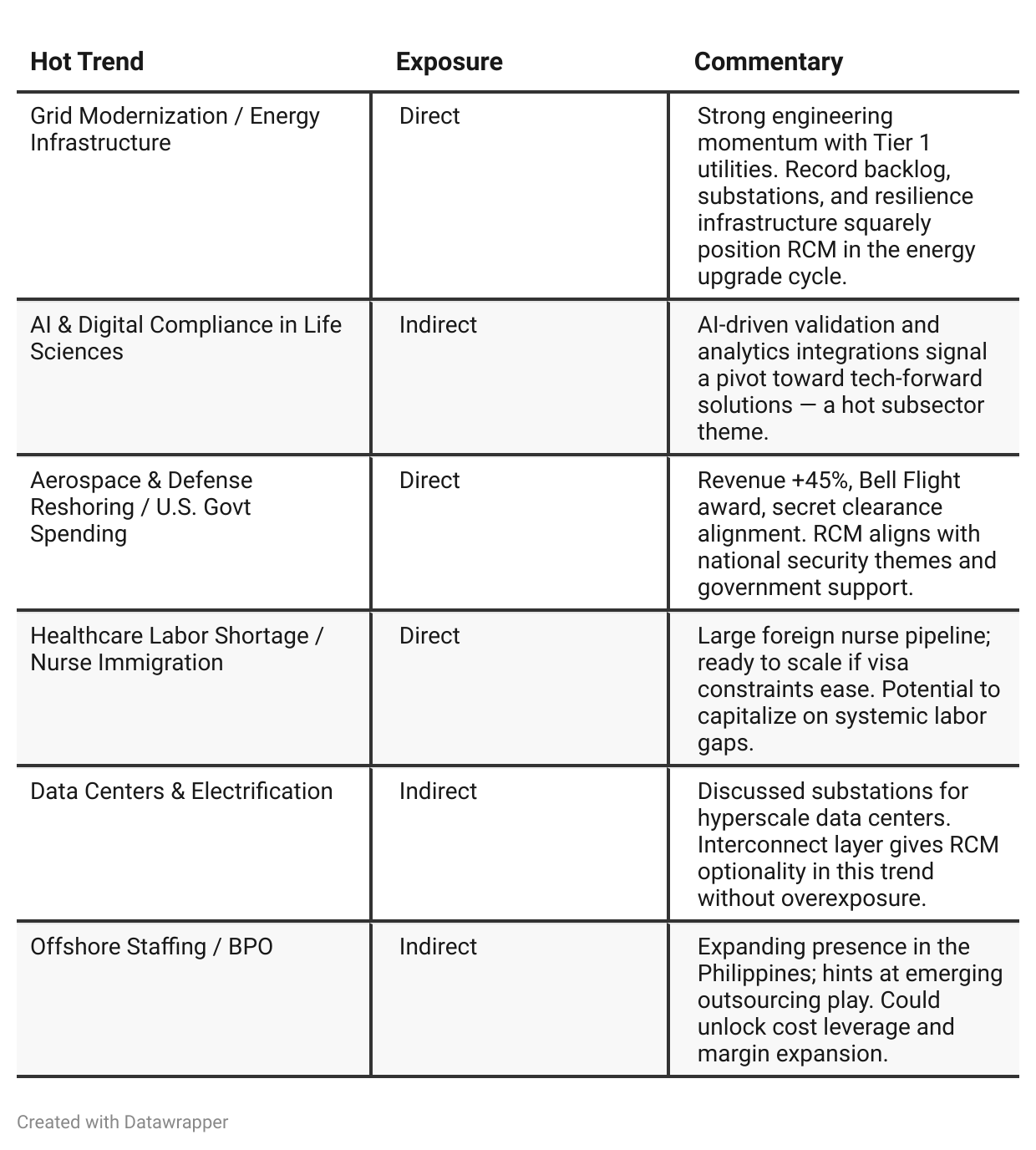

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison

RCM Technologies has evolved from a cautiously confident operator into a momentum-fueled leader across core verticals. In Q2, they focused on resilience, integration, and smart positioning. By Q3, the tone matured into one of measured dominance, with record backlogs, brand-fueled talent inflow, and tangible wins across engineering, healthcare, and life sciences. Despite medical cost inflation and Q3 seasonality, RCM is entering Q4 on strong footing with clear growth levers and strategic optionality intact.Year-over-year comparison

RCMT has evolved from a steady builder into a confident operator scaling across engineering, healthcare, and life sciences. In Q3 2024, it emphasized stability, client satisfaction, and platform growth. By Q3 2025, it emerged as a Tier 1 player with record backlogs, inflow of top-tier talent, AI-enhanced services, and aggressive expansion opportunities. While medical costs and school-year seasonality impacted short-term margins, the long-term outlook is bullish — driven by infrastructure demand, foreign nurse pipelines, and data-led healthcare innovation. The company enters Q4 with operational momentum and strategic options fully intact.

Final Takeaway

RCMT is in a growth phase, driven by strength in engineering and healthcare, with momentum building from strategic hires, digital innovation, and brand reputation. While foreign nurse visa delays and healthcare costs present headwinds, strong capital allocation, backlog visibility, and operational depth position the company well for 2026.

Verdict: BUY, with significant upside potential if backlog converts and healthcare recruitment bottlenecks ease.