PulteGroup, Inc. (NYSE: PHM) – Q2 2025 Earnings

PulteGroup, Inc. (NYSE: PHM) – Q2 2025 Earnings

Earnings Release Date: Jul. 22, 2025

Stock Price: $120.23

Market Cap: $23954.9 million

Q2 2025 sales of $4.4 billion vs $4.6 billion in the prior year

Q2 2025 EPS of $3.03 vs $3.83 in the prior year

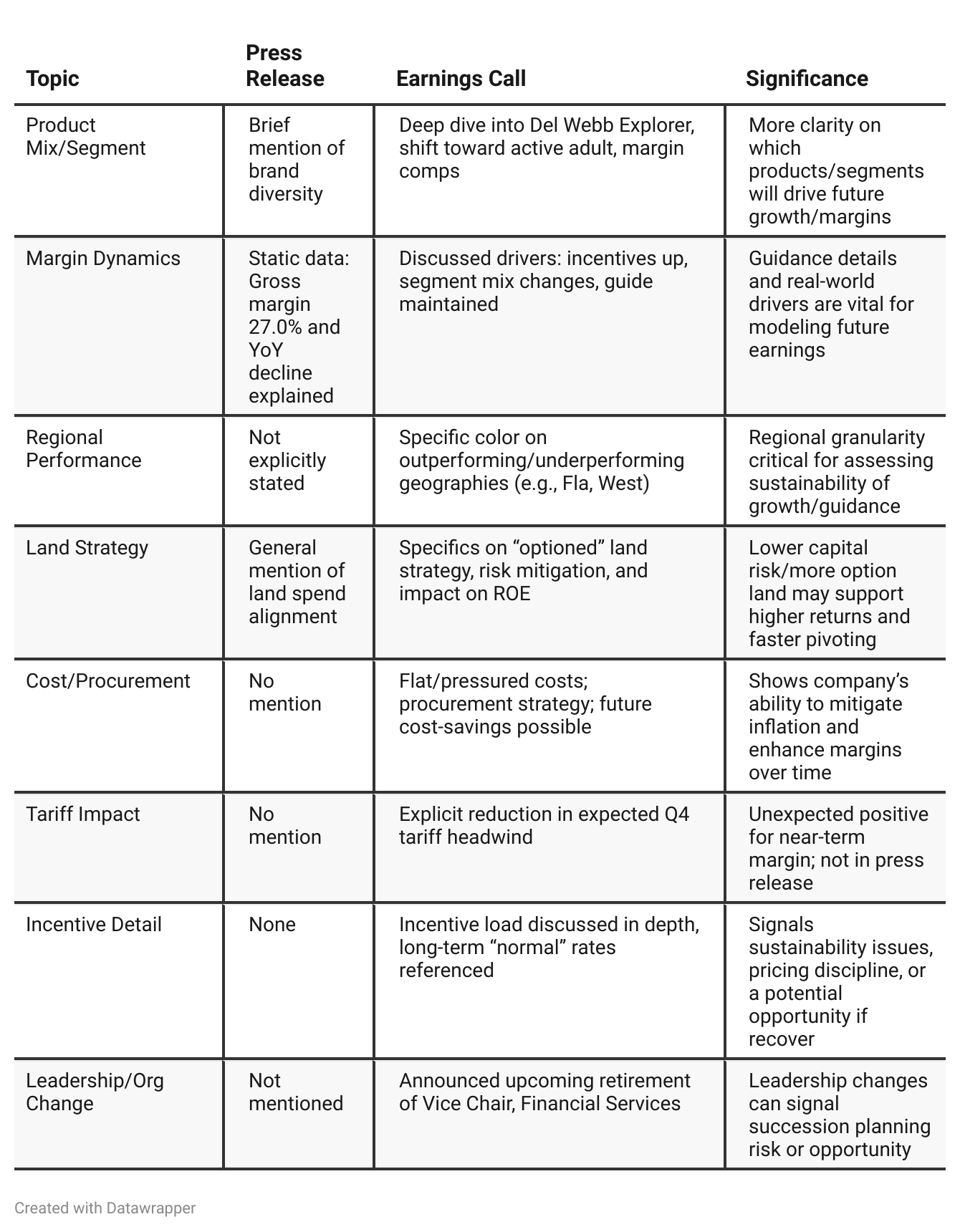

Press Release vs Call Transcript Comparison

Market Share Ambition: The transcript, not the press release, clarifies the company’s intent to use its strong land pipeline to grow 5–10% even in a choppy market, suggesting long-term bullishness.

Share Repurchases as Capital Allocation: Both mention, but the transcript frames buybacks as ongoing “consistent practice,” hinting at policy.

Segmental Margin Opportunities: The Q&A details that move-up homes generate 200bps better gross margin than entry-level, and active adult (Del Webb) deliver another 200bps on top of that. As mix shifts to higher-margin segments, overall company margin could improve (if volumes hold).

Affordability Elasticity: Management is upfront that further increases in incentives may not drive sales, which means the market’s price sensitivity is extremely high.

Transparency in Volatility: The call is much more transparent than the press release about the ongoing volatility in demand and the day-to-day uncertainty facing homebuilders.

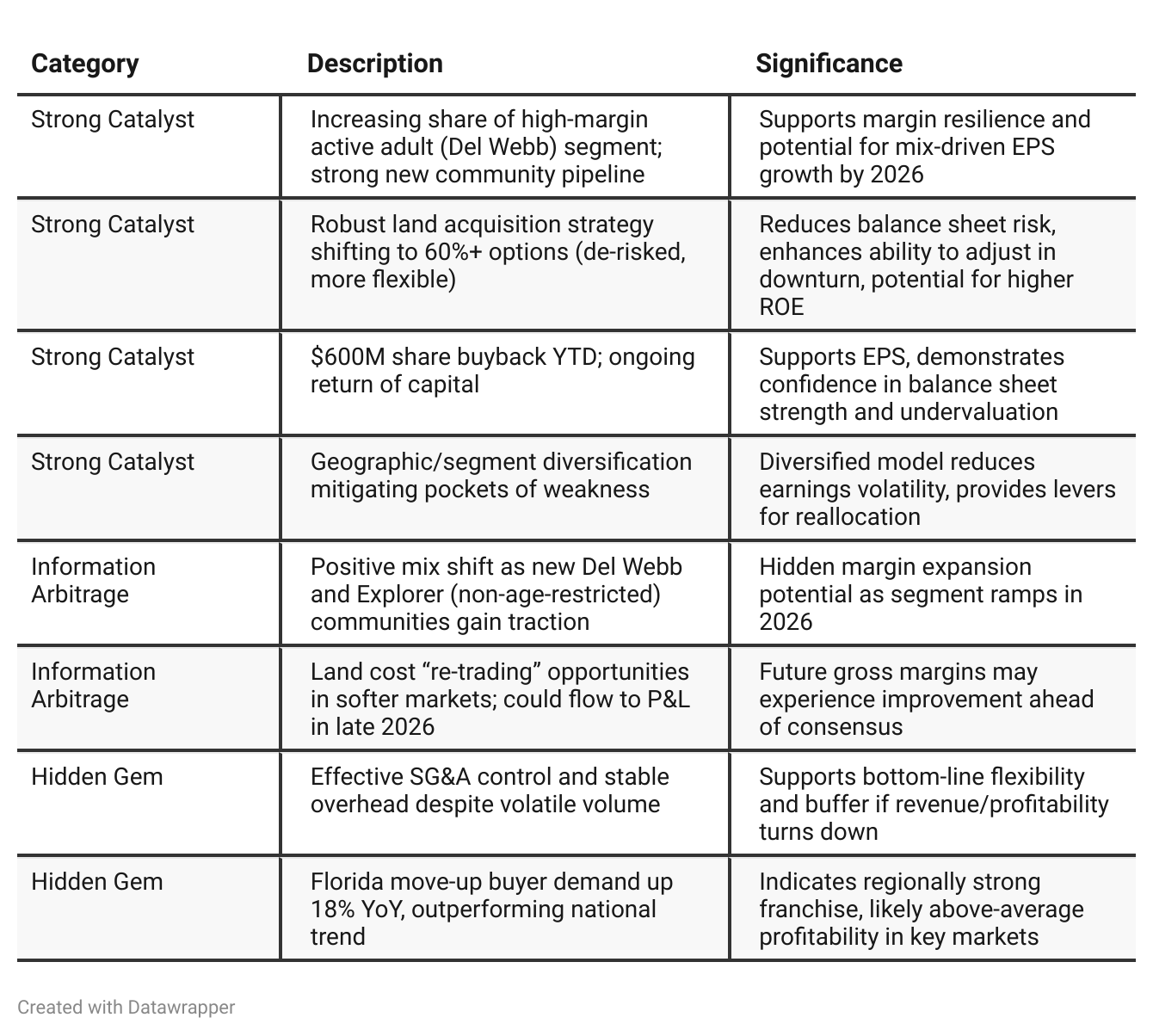

Positive Insights

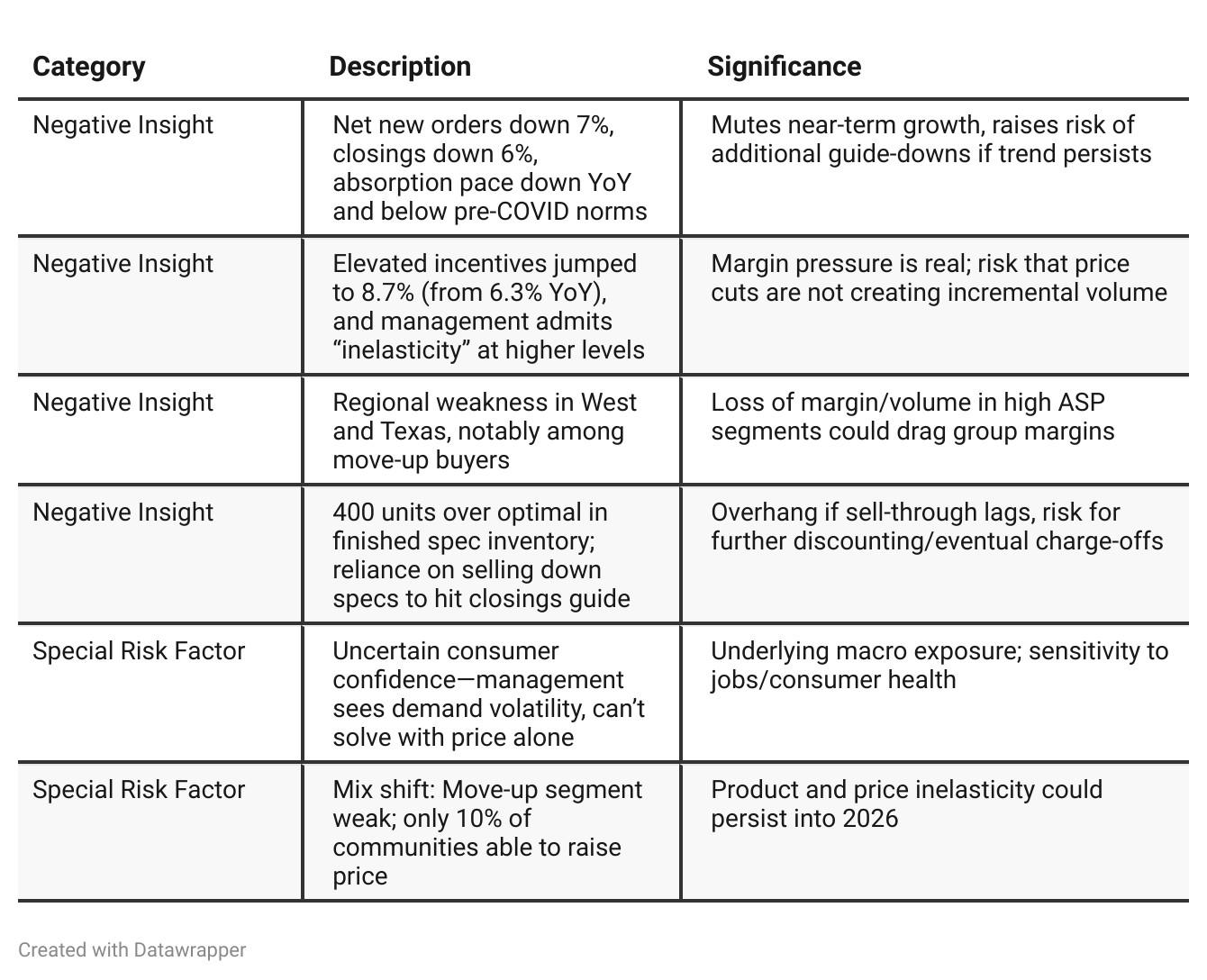

Negative Insights

Tariff Risk

Tariff Mentions/Actions:

Management acknowledged potential Canadian lumber tariff increases (“doubling”).

Only 20–25% of lumber is imported from Canada, limiting exposure.

Revised guidance: expected Q4 tariff impact lower than feared, mitigates some 2H incentive/margin drag.

No mention of major supply chain shifts, contract renegotiation, or price increases as a result; company seems able to absorb moderate cost increases given procurement strength.

Future tariff load anticipated to hit more meaningfully in “next year,” could be offset if domestic supply/costs remain stable.

Management dismisses catastrophic impact narrative, highlights partial insulation due to diverse lumber sourcing.

No discussion of market share, innovation, or strategic pivots driven by tariffs—risk judged as manageable unless tariffs broadly escalate.

Tariff Section Conclusion: Tariff risk is on management’s radar but viewed as a manageable, not existential, headwind. Near-term (Q4) impact is likely limited, though “next year” could see more pronounced effects if Canadian tariffs hold or rise. Cost discipline and diversified sourcing offer some insulation, but investors should monitor future updates and competitor responses.

Previous Earnings Call

Quarter-over-quarter comparison

In Q1, the company focused on pulling back starts, clearing spec inventory, and protecting price over chase—communicating confidence in their diversified platform and risk-mitigation efforts like land optioning and balance sheet strength. They responded to day-to-day volatility, recalibrated guidance down, and openly spoke of staying nimble as the macro picture clouded and tariffs loomed.

By Q2, that stance hardens: The management openly states the limits of what incentives can do amid soft consumer confidence and is candid that some product/market combinations cannot be “stimulated” by discounts. Opportunities are being seized in land (“re-trading”), and more granularity is provided on what is working—namely, the Del Webb segment—and where risk is showing (West and Texas). Execution discipline is now less about global margin posture and more about micro-market and micro-segment adaptation. Leadership’s commentary shows less patience for volume and more for defending or expanding market share where they see superior returns.

Year-over-year comparison

In Q2 2024, PulteGroup was riding high on robust demand, strong pricing, operational discipline, and an ambitious approach to community expansion and land pipeline efficiency. Management’s messaging was confident, focusing on growth and returns, with measured awareness of some choppier undercurrents (notably Florida/Texas inventory and buyer psychology). Risks were downplayed as manageable, and investment in land, people, and process was accelerating.

By Q2 2025, that narrative has shifted noticeably. Management is less focused on growth, more on adaptability and discipline. The operating environment is described as difficult, with buyer confidence and demand inelastic to incentives. Segment and region performance is more disparate, driving a highly tactical and localized approach. PulteGroup is using its platform strength and capital flexibility to play defense—selling through spec, re-trading land, and returning capital—while leveraging bright spots like Del Webb to mitigate broad-based softness. Margin preservation gives way to protecting returns and cash flow, as hope for a macro-driven demand uptick becomes central but by no means certain. The tone is cautious but not pessimistic: management is clear-eyed about challenges and focused on controlling what they can, setting up for reacceleration in a stronger environment but not betting on it in the interim.

Final Takeaway

PulteGroup is in a stabilization phase focused on disciplined risk reduction, capital return, and leveraging product/geographic diversity. While positive catalysts exist in land strategy, Del Webb segment growth, and cost resettlement opportunities, near-term headwinds from volume declines, margin pressure, and persistent demand uncertainty offset those positives. Investors should watch order rates, incentive discipline, and execution on reducing spec inventory, while tracking new land and margin developments for a future inflection point. Verdict: Hold, with direction determined by demand trends and cost realization in 2H’25.