OneSpan Inc. (NASDAQ: OSPN) – Q2 2025 Earnings

OneSpan Inc. (NASDAQ: OSPN) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $14.60

Market Cap: $557.7 million

Q2 2025 sales of $59.8 million vs $60.9 million in the prior year

Q2 2025 EPS of $0.34 vs $0.31 in the prior year

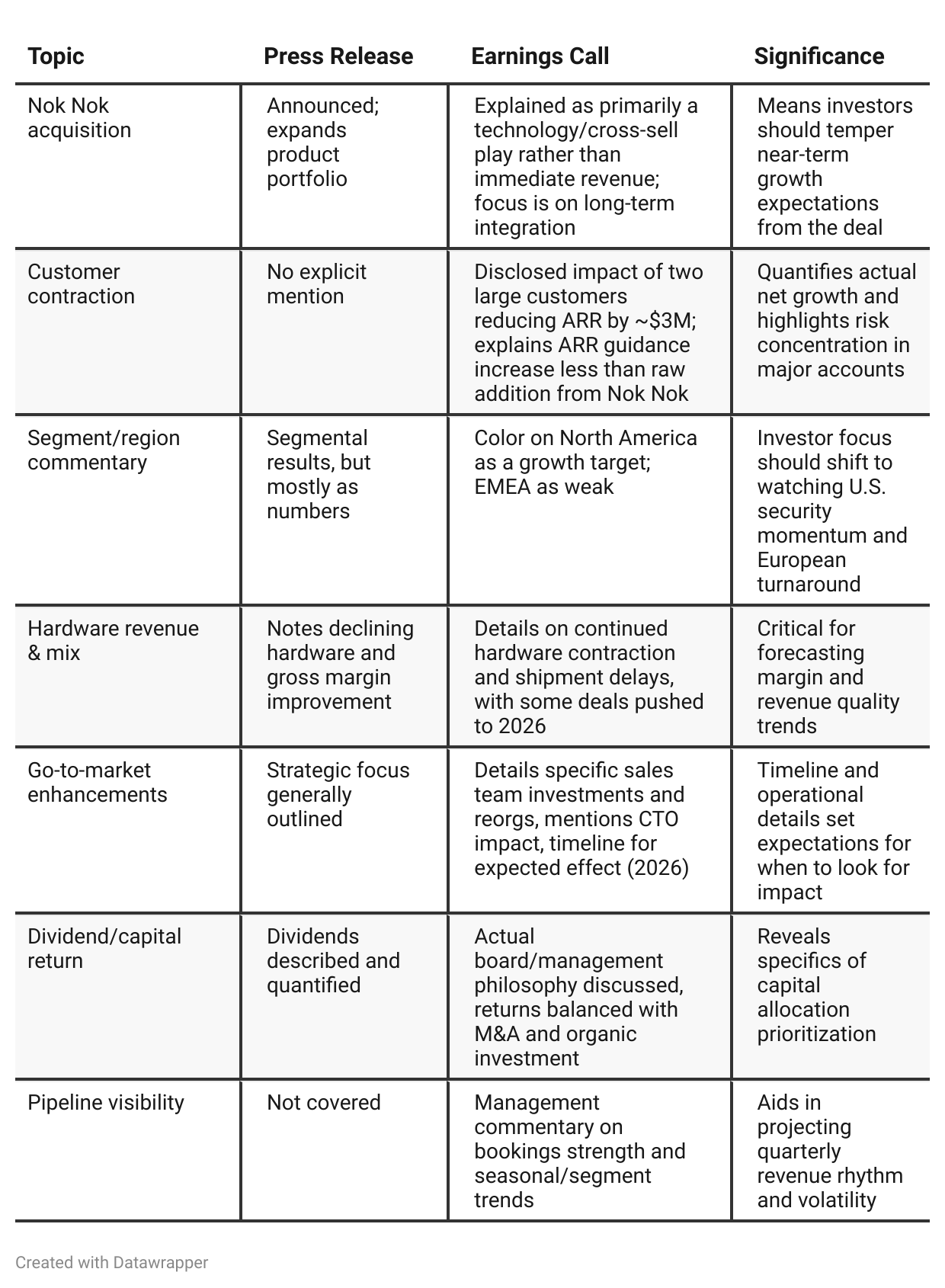

Press Release vs Call Transcript Comparison

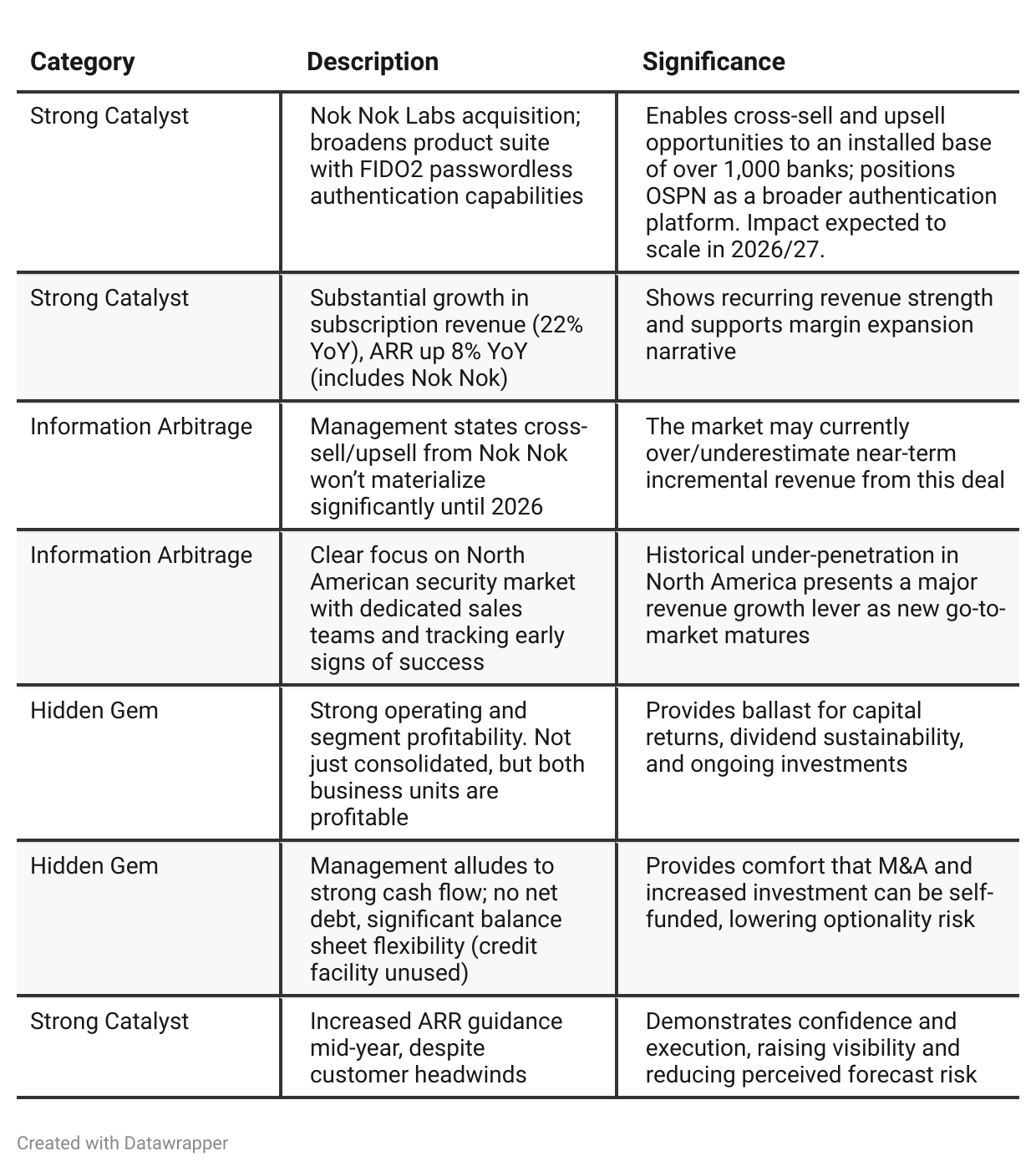

Financial Quality: The increase in gross margins is driven by product mix and a move away from low-margin hardware, which should be positive for profitability if recurring revenue growth continues.

Balance Sheet: With $92.9M in cash and a new $100M revolving credit facility (unused), the company is well-capitalized for more M&A if strategic opportunities arise.

Guidance Disciplined: Despite the acquisition, hardware contraction offsets some incremental ARR; guidance is conservative and responsive to operational realities.

Operational Transformation: Management is explicit about their ongoing transformation push and willingness to restructure, invest, and shift go-to-market. The call is much more transparent about timelines and magnitude than the press release.

Acquisition Philosophy: Management’s stated preference for “technology, not revenue” in recent acquisitions mitigates the risk of overpaying for near-term sales but means growth will be lumpy and integration risk higher.

Accounting Changes: The press release details changes to non-GAAP metrics reporting, which is routine but could affect perception of historical comparability.

Positive Insights

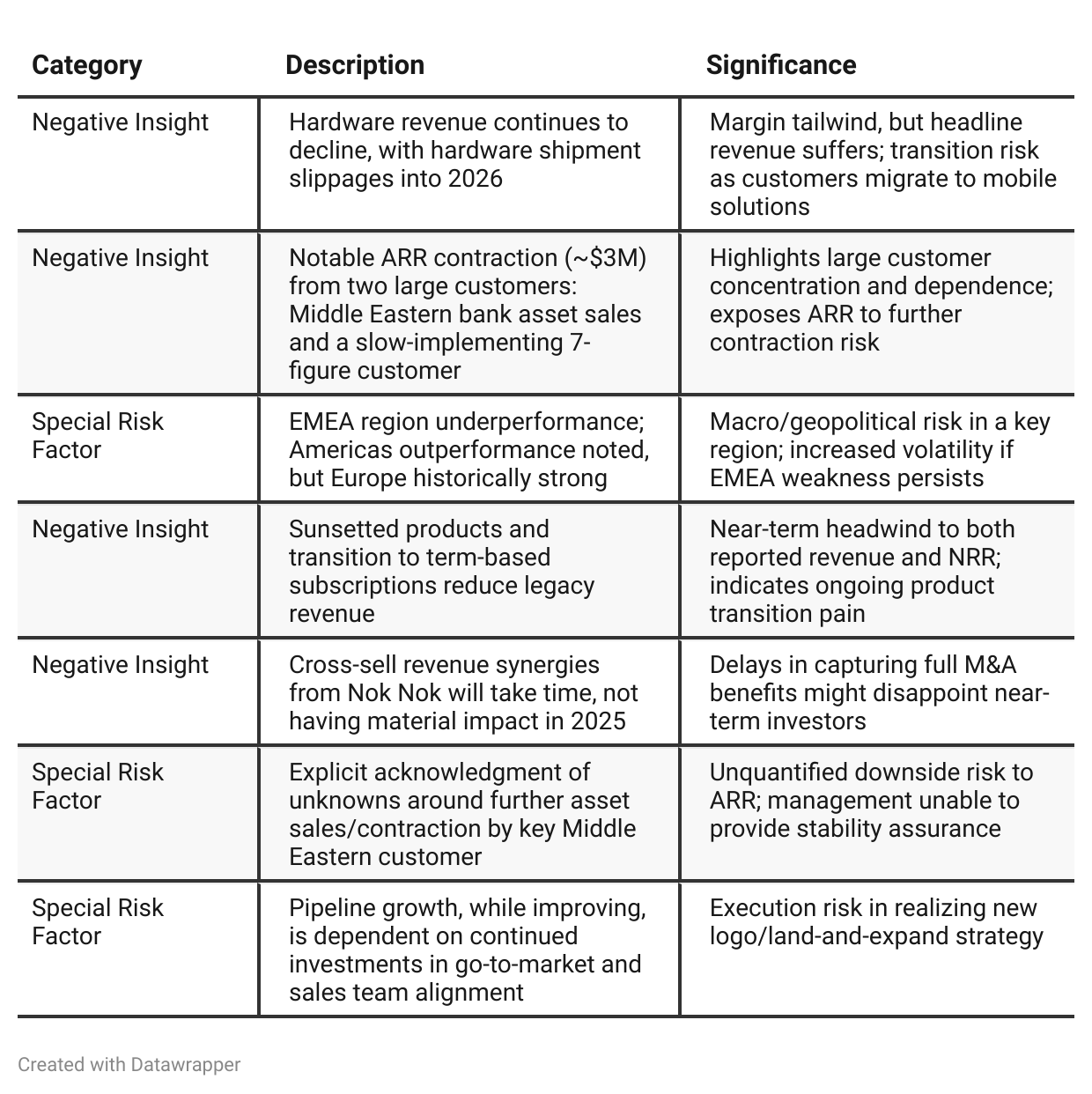

Negative Insights

Tariff Risk

Transcript Commentary: The company was directly asked about the impact of U.S. tariffs. Management said tariffs had “very minimal” effect in the quarter, quantifying the impact as “a few hundred thousand dollar[s]”—not material. No evidence of major supply chain, pricing, or competitive disruptions. Management also downplayed the impact of U.S. federal cuts, with only ~2% of revenue from federal contracts.

Mitigation/Actions: No specific supply chain or contract renegotiation actions mentioned; impact is small enough to absorb easily.

Sentiment Analysis

The overall sentiment toward $OSPN is bullish. Investors are highlighting strong subscription and ARR growth, expanding margins, robust cash flow and balance sheet, and attractive valuation metrics (such as a low P/E ratio and positive rating under value-focused models). The addition of Nok Nok Labs and insider share purchases reinforce confidence in future prospects. While some acknowledge slow overall growth due to legacy hardware, sentiment remains positive due to recurring revenue, dividend yield, and upside analyst targets.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

From Q1 to Q2 2025, OneSpan’s narrative has moved from a foundation of meticulous cost management, margin focus, and defensive positioning through industry transition, to one of cautious but visible offense. In Q1, management’s story was about holding the line on profitability while mitigating hardware drag and keeping growth aligned with expectations. By Q2, the company is actively transforming: launching new leadership in R&D, executing targeted (and underappreciated) M&A to future-proof its offering, building a more U.S.-centric sales engine, and outlining a credible plan for cross-selling advanced authentication. The openness about risks—customer contractions, EMEA softness, delayed M&A revenue—is now paired with greater strategic clarity and confidence in the path to accelerated growth in 2026. The result is a narrative shift from “profitable transition” to “platform-building for scalable, high-margin growth.”Year-over-year comparison

Between Q2 2024 and Q2 2025, OneSpan’s story has shifted from celebrating a successful turnaround and operational stabilization—anchored in cost-cutting, record SaaS/ARR growth, and margin rescue—to constructing a platform set up for strategic offense. The company has graduated from reprioritizing profitability and SaaS migration, to investing in new technology (via acquisition), overhauling go-to-market strategy, and articulating a path to accelerated future growth driven by expanded capabilities and deeper customer penetration. While the company is more forthcoming about risks and admits some challenges (notably large customer loss and hardware decline), there’s now a stronger sense of long-term prioritization: product innovation, cross-sell, and U.S. expansion. The new priority is scaling a sustainably profitable, platform-ready business poised for a new industry authentication wave by 2026, rather than just defending margins and stabilizing topline.

Final Takeaway

OneSpan is in a late-stage restructuring/early growth phase, focusing on transforming its revenue mix toward recurring, high-margin software and leveraging strategic M&A for cross-sell. While the shift is delivering operational and margin improvements, significant customer concentration and product transition risks persist. Execution on cross-selling, regional expansion (especially North America), and customer retention will be critical for achieving real acceleration in 2026. Verdict: Hold, with long-term upside potential if execution aligns with stated strategy.