OppFi Inc. (NYSE: OPFI) – Q2 2025 Earnings

OppFi Inc. (NYSE: OPFI) – Q2 2025 Earnings

Earnings Release Date: Aug. 6, 2025

Stock Price: $9.99

Market Cap: $265.8 million

Q2 2025 sales of $142.4 million vs $126.3 million in the prior year

Q2 2025 EPS of $0.45 vs $0.29 in the prior year

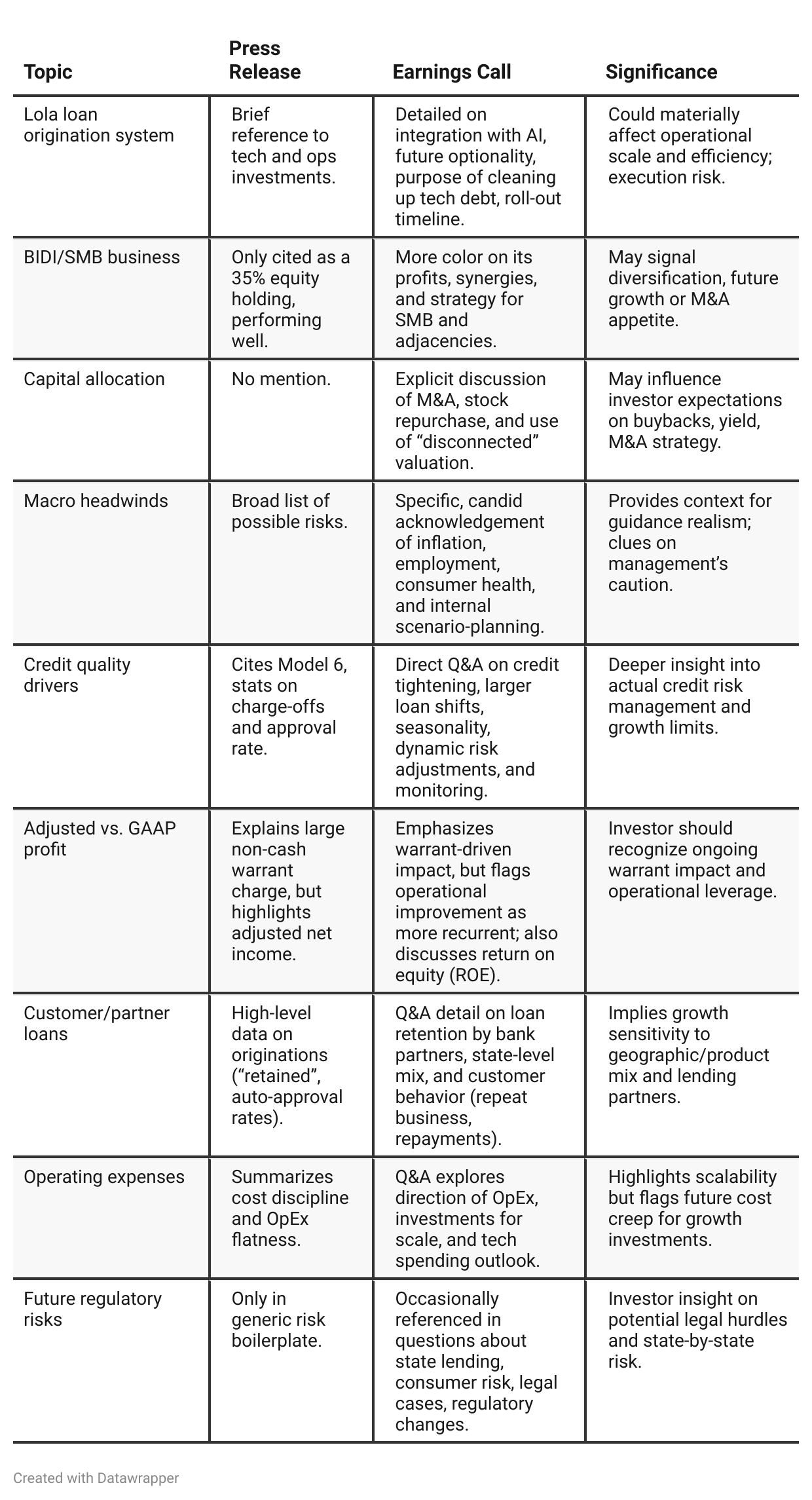

Press Release vs Call Transcript Comparison

Share Count / Dilution: The call makes clearer that the impact of dilution, particularly from warrants and stock comp, is material and ongoing, producing a big difference between “headline” adjusted EPS and actual EPS available to common holders.

Customer Repeat Dynamics: On the call, management highlighted the “large population of customers that have paid in full and come back,” which wasn’t covered in the press release. This implies brand/customer loyalty is aiding growth, which could defend future margins.

Marketing Spend/CPAs: The call references efficiency of marketing spend and channel testing, which underscores the importance of cost per acquisition (CPA) management as growth accelerates.

Tech Platform/“Tech Debt”: Analysts should appreciate that Lola’s anticipated impact is longer-term modernization and modularity, not immediate margin expansion.

Risk Appetite: The call’s tone is strikingly cautious considering record results. Management intends not to “swing for the fences” but defend margins and watch macro risks, which suggests prudent, not aggressive, balance sheet management.

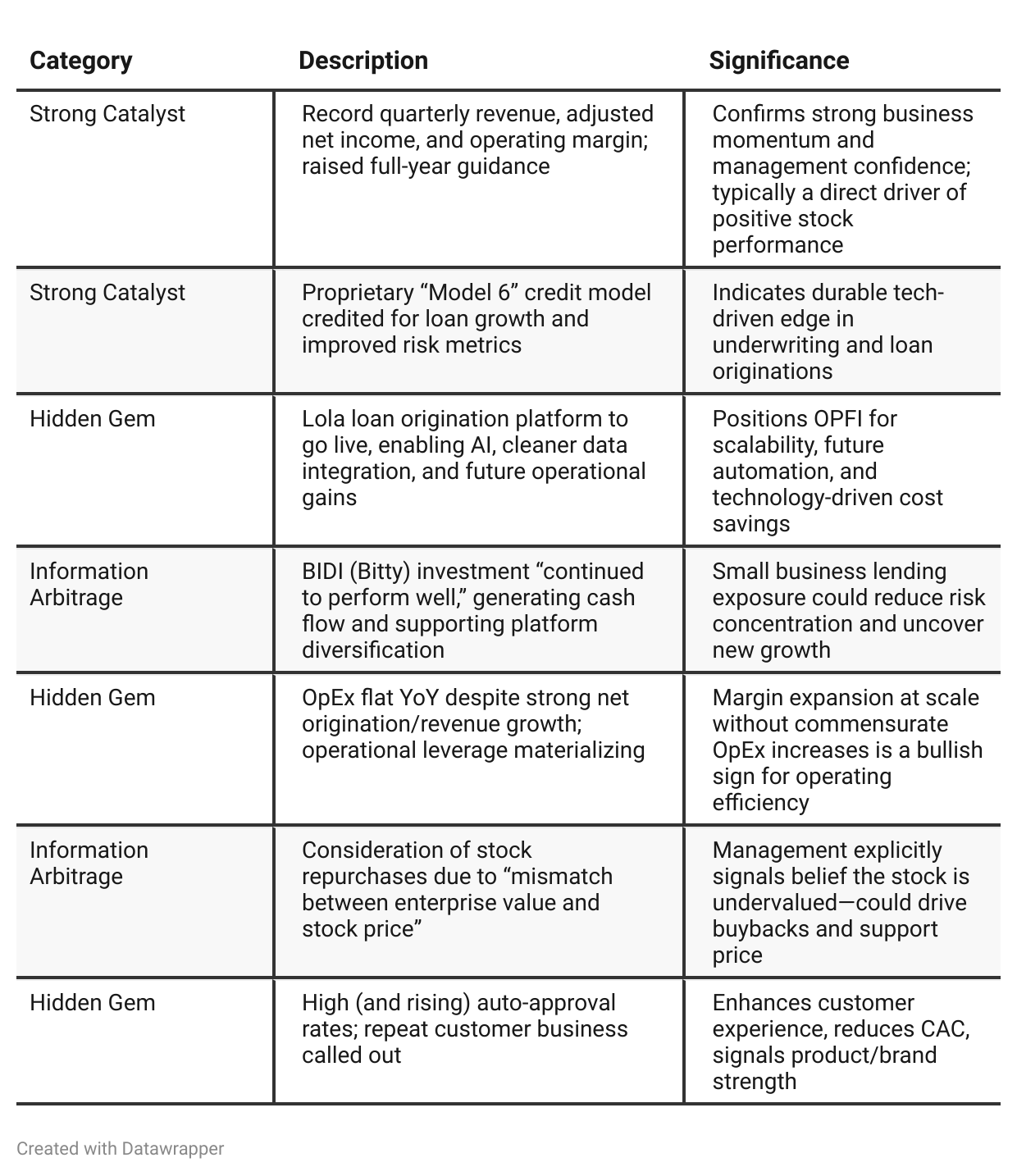

Positive Insights

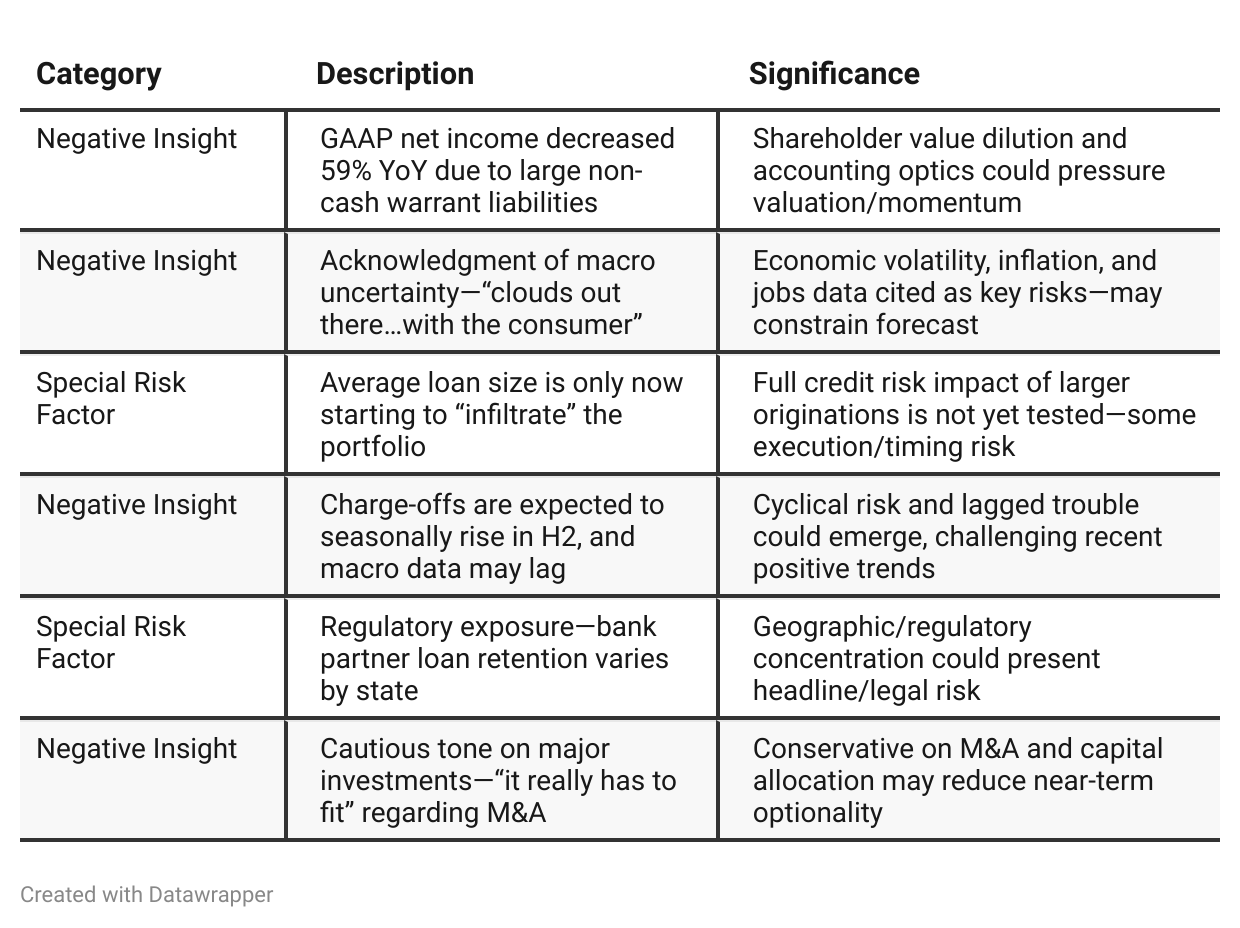

Negative Insights

Tariff Risk

Transcript Mentions:

No specific mentions of tariffs, US trade policy, or relevant supply chain/market share impacts were found.

No explicit questions from analysts regarding tariffs or sourcing.

Analysis: There is no direct evidence from this call that tariffs or trade policy are material risk factors for OppFi’s business model at present. Management did cite “tariffs” in cautionary language about risk factors (as part of a standard forward-looking statement disclaimer), but it does not appear to be affecting revenue, operations, or competitive position for this quarter. No mitigation actions (supply chain shifts, pricing changes) were detailed. Investors should continue to monitor regulatory disclosures and risk factors for any emerging exposure but, based solely on this transcript, tariffs are not a focus or material risk at this time.

Previous Earnings Call

Quarter-over-quarter comparison

Early 2025 (Q1): OPFI’s tone is bullish, highlighting a record start to the year with substantial improvements in revenue, net income, and operational metrics. The management team is focused on leveraging the improvements from Model 6, driving cost discipline, rewarding shareholders (special dividend, debt paydown), and continuing strong credit quality. They exude confidence in their long-term vision of building a digital finance platform and show eagerness for future growth via both organic and selective inorganic opportunities.Mid-2025 (Q2): The optimism endures, underpinned by continued record results and raised guidance. However, the narrative matures: management places new emphasis on technological modernization (Lola rollout), incremental growth via larger loans, and operational resilience. They actively discuss the importance of monitoring macro headwinds, highlighting “clouds” such as inflation and employment, and readiness to adapt should the environment deteriorate. They also become more open about capital allocation intentions (buybacks), and operationalize prior strategic comments into visible action items (collections, loan sizing, AI integrations).

Year-over-year comparison

Q2 2024: OPFI is riding high on a wave of operational improvements, cost discipline, and credit wins. With record financials, the company signals its ability to generate free cash flow and pursue both shareholder returns (dividends, buybacks) and new growth avenues (SMB lending through BIDI). The company’s narrative centers on the successful execution of its strategic foundation and the ability to selectively pursue new opportunities.

Q2 2025: In a year, OPFI has matured its tone. The company still posts record results and climbs to new levels of efficiency and profitability—now, however, management’s story leans heavily into future-proofing: launching the Lola platform to integrate AI and scalability, re-examining credit policies in view of macro headwinds, and sharpening its messaging around risk, seasonality, and adaptability. The narrative shifts from “turnaround and opportunity” to “steady innovation and prudent, tech-driven expansion,” with leadership openly flagging the importance of dynamic risk management as economic uncertainty mounts.

Final Takeaway

OppFi (NYSE: OPFI) is in a growth and scaling phase, leveraging its proprietary Model 6 credit platform and entering the next stage of tech-driven innovation with the Lola origination system. While the company is posting record revenue and strong operating leverage, key risks include macroeconomic volatility, GAAP/adjusted net income gaps due to non-cash items, and the full seasonality impact on charge-offs yet to play out. Capital runway is strong, and management signals confidence through potential buybacks and prudent growth strategy. Execution on tech modernization and continued credit discipline will be pivotal to sustaining momentum. Verdict: Buy, with upside tied to successful rollout of Lola, resilience against macro softness, and prudent risk management.