Omni-Lite Industries Canada Inc. (OTCQX: OLNCF/OML.V) – Q2 2025 Earnings

Omni-Lite Industries Canada Inc. (OTCQX: OLNCF/OML.V) – Q2 2025 Earnings

Earnings Release Date: Aug. 13, 2025

Stock Price: $1.12

Market Cap: $17.3 million

Q2 2025 sales of $3.5 million vs $4.3 million in the prior year

Q2 2025 EPS of $(0.01) vs $0.02 in the prior year

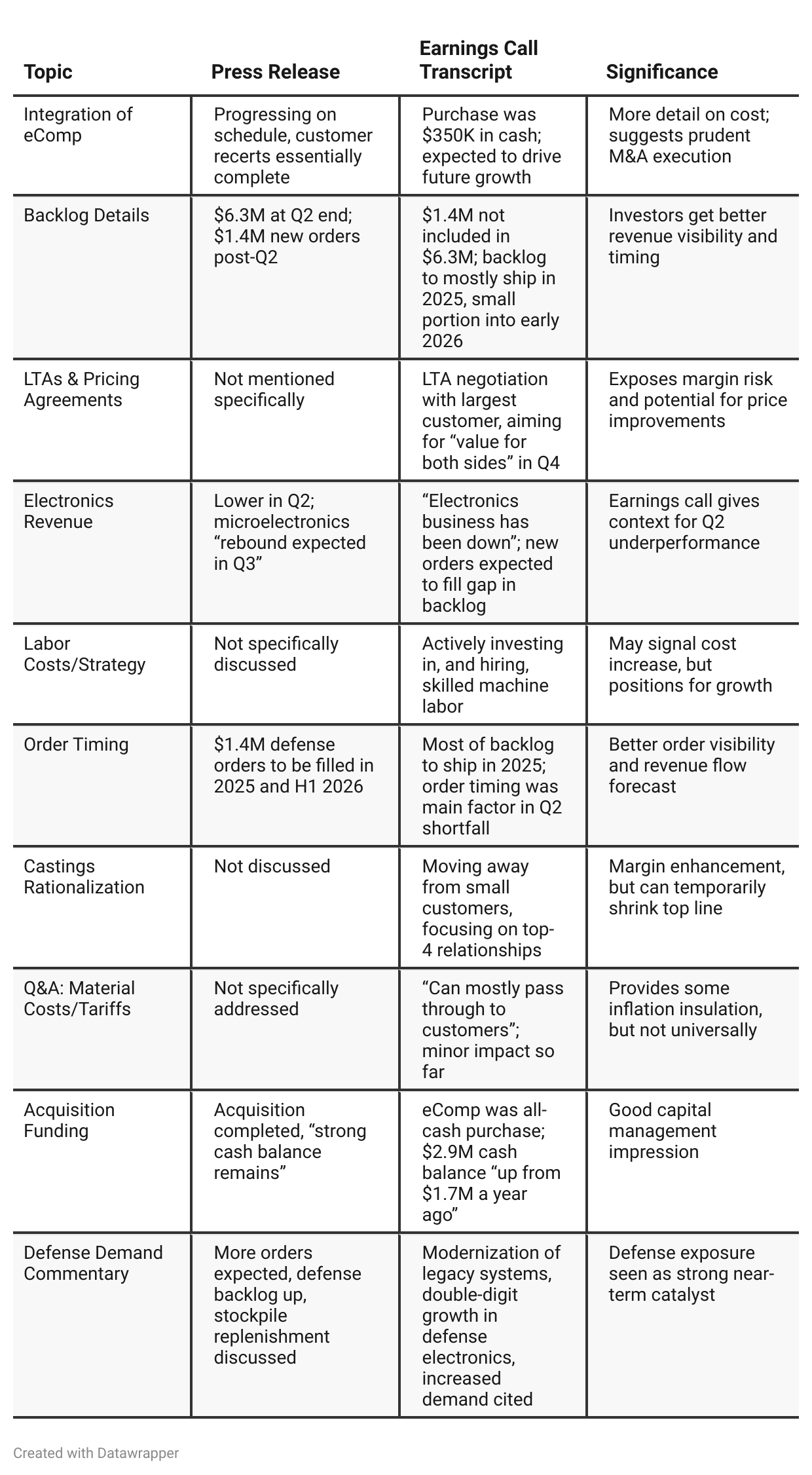

Press Release vs Call Transcript Comparison

Press Release focuses more on headline performance metrics; call transcript gives color on strategy, cost management, and execution details.

The earnings call’s Q&A surfaces investor concerns (backlog timing, cost pass-through) that are not at all addressed directly in the press release.

The emphasis on recurring, long-cycle defense contracts (electronics) is more prominent in call, supporting investment case for more stable cash flows.

No direct mention of stock buybacks or dividend policy in either document—a possible oversight if one is seeking shareholder return priorities.

No mention of competition in the press release; earning call notes market share gains and “taking business” due to speed of delivery.

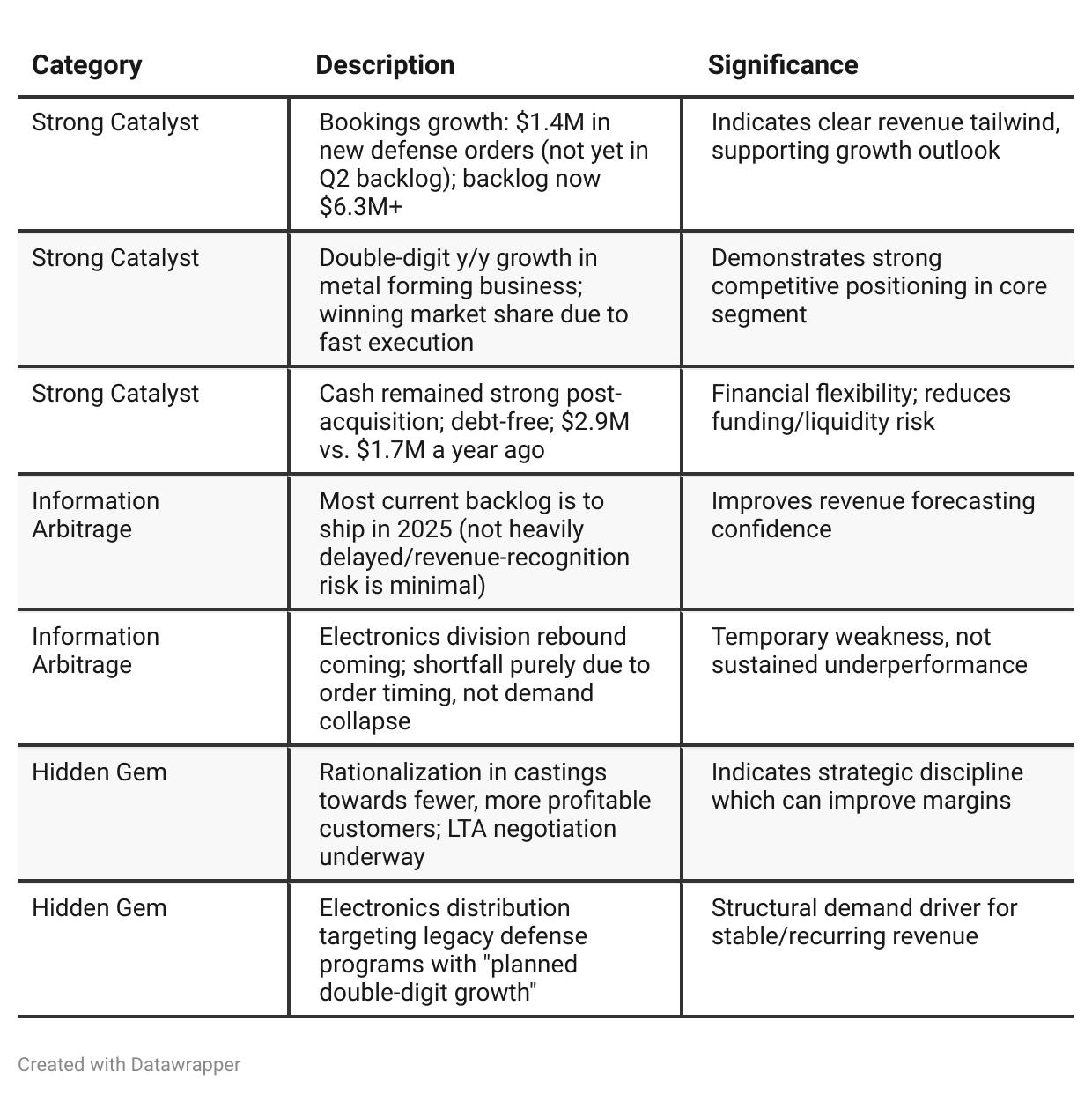

Positive Insights

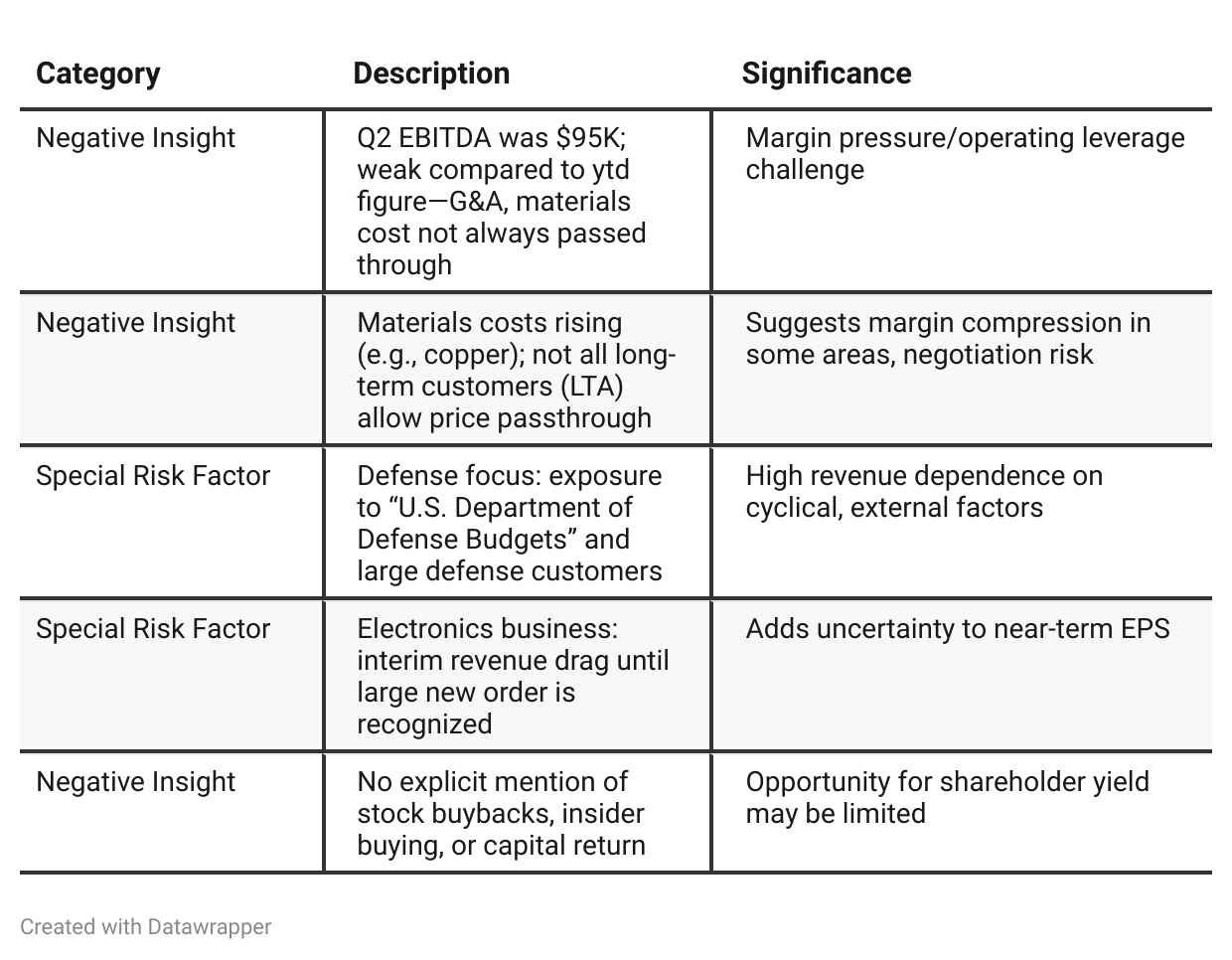

Negative Insights

Tariff Risk

The company addressed tariff risk during the Q&A as follows:

Most production is for defense/critical infrastructure; these products have received minimal tariff impact so far.

Where material costs (like copper) have increased, the company typically passes these increases on to customers.

In cases where prices are locked in long-term agreements, there can be lag before those prices are adjusted, but management expects to negotiate for more favorable terms soon.

Mitigation Strategies:

Pricing power: In most areas, costs are handled via spot pricing or adjustable purchase orders.

Customer contracts: Typically allow for cost pass-through except in certain LTAs, which are under negotiation.

No evidence of significant market share or innovation impact due to tariffs currently.

Forward-looking:

Management expects “minimal impact” from tariffs to continue, but is proactively renegotiating to address any longer-term structural challenges in LTAs.

Conclusion: Tariff risk is currently well-managed and considered a minimal threat, but margin vulnerability remains until LTA negotiations conclude.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: Omni-Lite enters the year in a consolidating and cautiously opportunistic posture. Management highlights execution on newly qualified aerospace fasteners and a strategic acquisition (eComp) to add channel/customer relationships and fill a product gap in legacy electronics. The tone is steady and targeted: margin accretive focus, customer diversification, and maintaining a strong balance sheet.Q2 2025: Management’s narrative shifts into assertive growth mode. The company updates on successful backlog conversion, large new defense orders, proactive investment in labor to capture demand, progress on key long-term pricing negotiations, and clear market share gains through operational agility. There’s higher confidence (even amid near-term electronics lulls) with a more direct message that Omni-Lite is positioned for acceleration as macro trends (defense spending, supply chain tightness) play in their favor. Margin and execution remain under scrutiny, especially given cost inflation and the timing of order recognition, but confidence in multi-year tailwinds is stronger and more tangible.

Year-over-year comparison

Q2 2024: Omni-Lite was in a phase of broad-based growth, benefiting from macro tailwinds in commercial aerospace and defense, with robust top-line and margin gains and strong bookings pipelines. The message centered on riding momentum and delivering record results while managing risk.

Q2 2025: The company’s narrative matures: management is now focused on translating backlog into revenue, navigating segment-specific volatility (especially in electronics), controlling costs in a higher-inflation world, and affirmatively investing in capacity and long-term customer relationships. The message is more nuanced, acknowledging risk and variability, but also competitive strengths (speed, flexibility), and the need for operating discipline as growth is pursued.

Final Takeaway

Omni-Lite Industries Inc. is in a growth and cost-optimization phase, capitalizing on rising aerospace/defense demand and executing on recent acquisitions. Order momentum and financial stability are positives, but the company faces margin pressure from rising input costs and must finalize price negotiations and restore electronics growth. Success in closing profitable long-term agreements and converting backlog into revenue/margin will be pivotal. Verdict: Hold, with upside potential if margin execution improves and defense tailwinds persist.