Optical Cable Corporation (NASDAQ: OCC) – Q2 2025 Earnings

Optical Cable Corporation (NASDAQ: OCC) – Q2 2025 Earnings

Earnings Release Date: Jun. 5, 2025.

Stock Price: $3.16

Market Cap: $24.4 million

Q2 2025 sales of $17.5 million vs $16.1 million in the prior year

Q2 2025 EPS of ($0.09) vs ($0.21) in the prior year

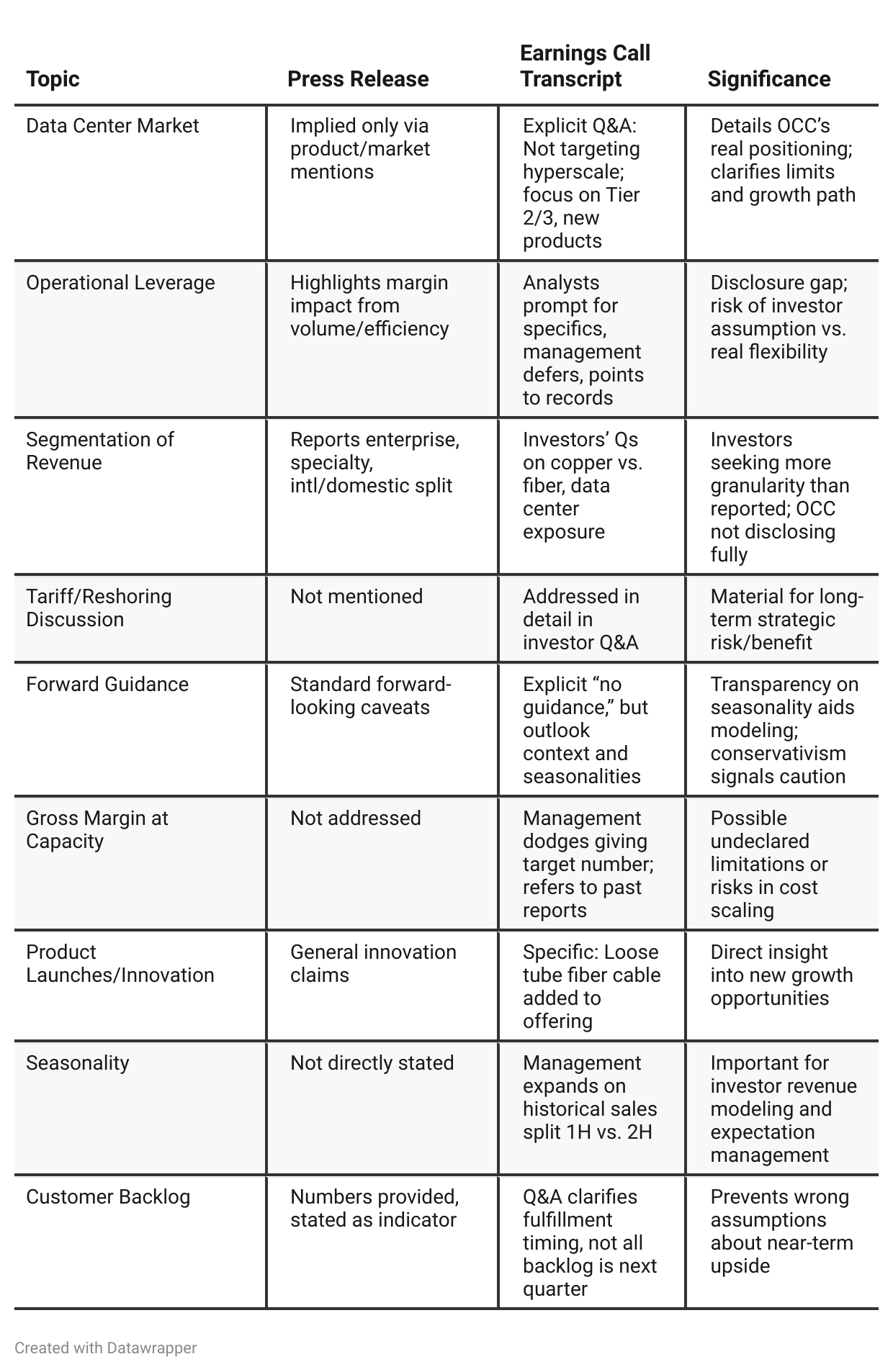

Press Release vs Call Transcript Comparison

Management Transparency: Call provides more nuanced data on backlog, seasonality, tariffs, and product mix, vital for sophisticated investors.

Growth Path: Press release sounds very bullish on growth/operating leverage; call tempers this with discussion of constraints and product mix volatility.

Potential Missed Opportunity: OCC’s current avoidance of the hyperscale data center market, despite local capacity (Dallas), may be a future opportunity or investor point of concern. Their admitted slow traction in smaller data centers suggests challenges moving up the value chain.

Financial Flexibility: Modest cash improvement but continued operating losses flag potential future liquidity needs if sales growth slows or expenses rise.

Competitive Edge: U.S.-based manufacturing is a competitive response to tariffs/reshoring trends, but benefits depend on future policy and supply chain stability.

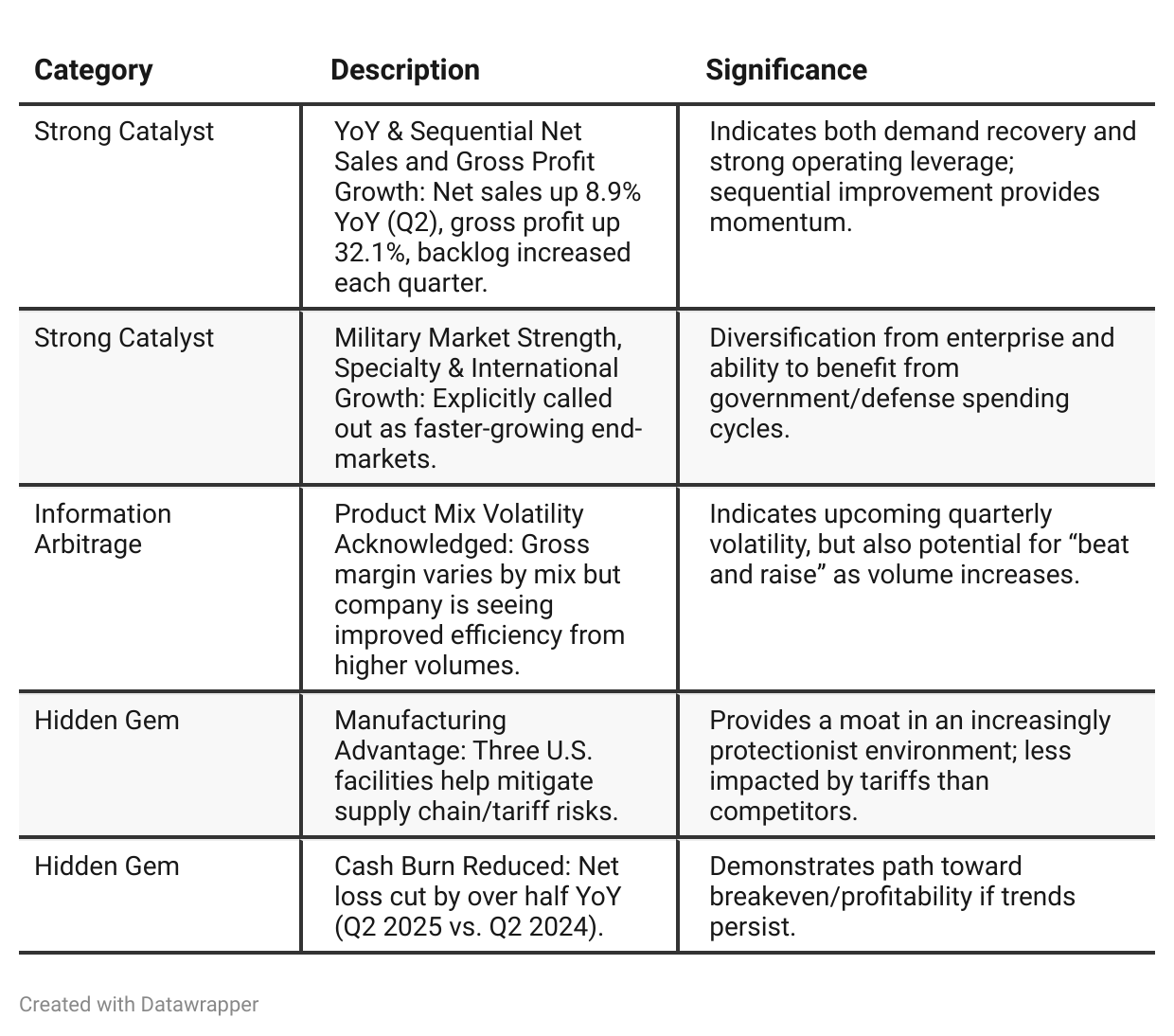

Positive Insights

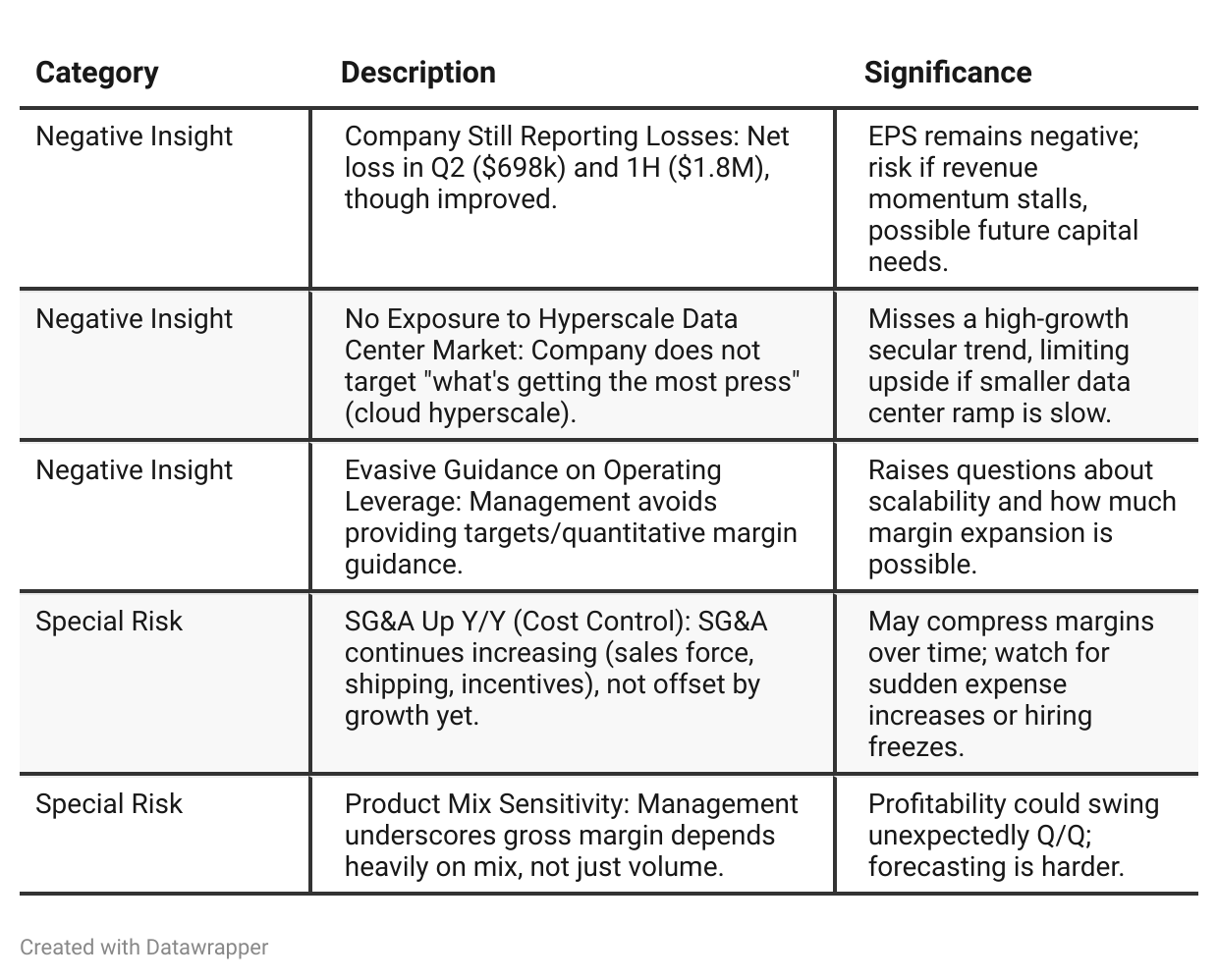

Negative Insights

Tariff Risk

Transcript Mentions: Management states OCC has been affected by tariffs, but less so than peers—all three manufacturing facilities are U.S.-based (tariff mitigation). However, some impact is still felt on certain products and export activity, with additional risk from “second-tier” supply chain exposure (i.e., supplier’s supplier).

Mitigation Actions: Company is monitoring the evolving tariff landscape and adjusting as needed but gives no specifics (e.g., no mention of relocating suppliers, changing pricing, or contract renegotiations).

Opportunity: OCC believes U.S. operations are a competitive advantage under “Building America” trends.

Outlook: Tariffs remain a risk for cost and export competitiveness; management sees less impact than competition, but full effects are evolving.

Investor Note: Track escalating U.S.-China/EU tariffs and OCC’s relative resilience—if tariffs rise further, OCC could claim share, but if global markets shift sourcing, exports may get hit.

Sentiment Analysis

The overall sentiment is bullish. Multiple investors express optimism about significant price appreciation, highlight OCC’s small float and recent backing for data center expansion, and associate the company with strong industry tailwinds in data center and fiber demand. Positive chart commentary and favorable sector comparisons further underscore a positive outlook, while there are virtually no negative or hesitant opinions.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2025: OCC is emerging from a sector-wide slump, reporting encouraging signs—a return to growth, backlog expansion, and improved margins from higher volumes. Management remains vigilant about external risks (seasonality, tariffs, macro politics) and underscores that recovery is early but real.Q2 2025: Recovery transforms to acceleration and confidence. OCC demonstrates not just year-over-year but sequential growth and margin gains. The backlog and forward load continue climbing, validating demand. The company elaborates on its strategic product adjustments (loose tube fiber) to participate in select data center opportunities while candidly acknowledging limits in the hyperscale segment. Discussion of tariffs shifts from potential threat to manageable complexity, thanks to OCC’s US-based manufacturing.

Year-over-year comparison

Q2 2024: OCC was battling through a tough industry-wide downturn, marked by year-over-year contraction, margin erosion, and negative profit swing. Leadership took a defensive stance, crediting resilience to its diversified end markets and operational discipline, while emphasizing sequential (not annual) gains as green shoots. Optimism was focused on an eventual recovery, but the company was mostly on the defensive, preserving capacity and watching for a turn.

Q2 2025: OCC re-emerges as a growth story. The results show real, measurable improvement: revenue, margin, backlog, and profitability all up significantly, with operating leverage again turning into an advantage rather than a source of pain. Messaging pivots to proactive execution—expanding product lines for new opportunities, especially select data center segments, and investing in sales to accelerate growth. Management’s tone shifts from explaining tough results to confidently touting execution and readiness for further expansion. OCC is positioned as a company that weathered the storm and is now building on a solid foundation for sustained, profitable growth.

Final Takeaway

Optical Cable Corporation is in a turnaround/growth phase, leveraging improving market trends and specialty/military demand but remains structurally unprofitable and is missing the highest-growth part of the data communications market. Success hinges on their ability to convert backlog into profitable sales while keeping costs in check and capturing new markets (especially smaller data centers). Verdict: Hold; upside if execution improves, risk if expenses outpace growth or if the company fails to penetrate new segments.