Nortech Systems Incorporated (NASDAQ: NSYS) – Q2 2025 Earnings

Nortech Systems Incorporated (NASDAQ: NSYS) – Q2 2025 Earnings

Earnings Release Date: Aug. 7, 2025

Stock Price: $7.87

Market Cap: $21.8 million

Q2 2025 sales of $30.7 million vs $33.9 million in the prior year

Q2 2025 EPS of $0.12 vs $0.05 in the prior year

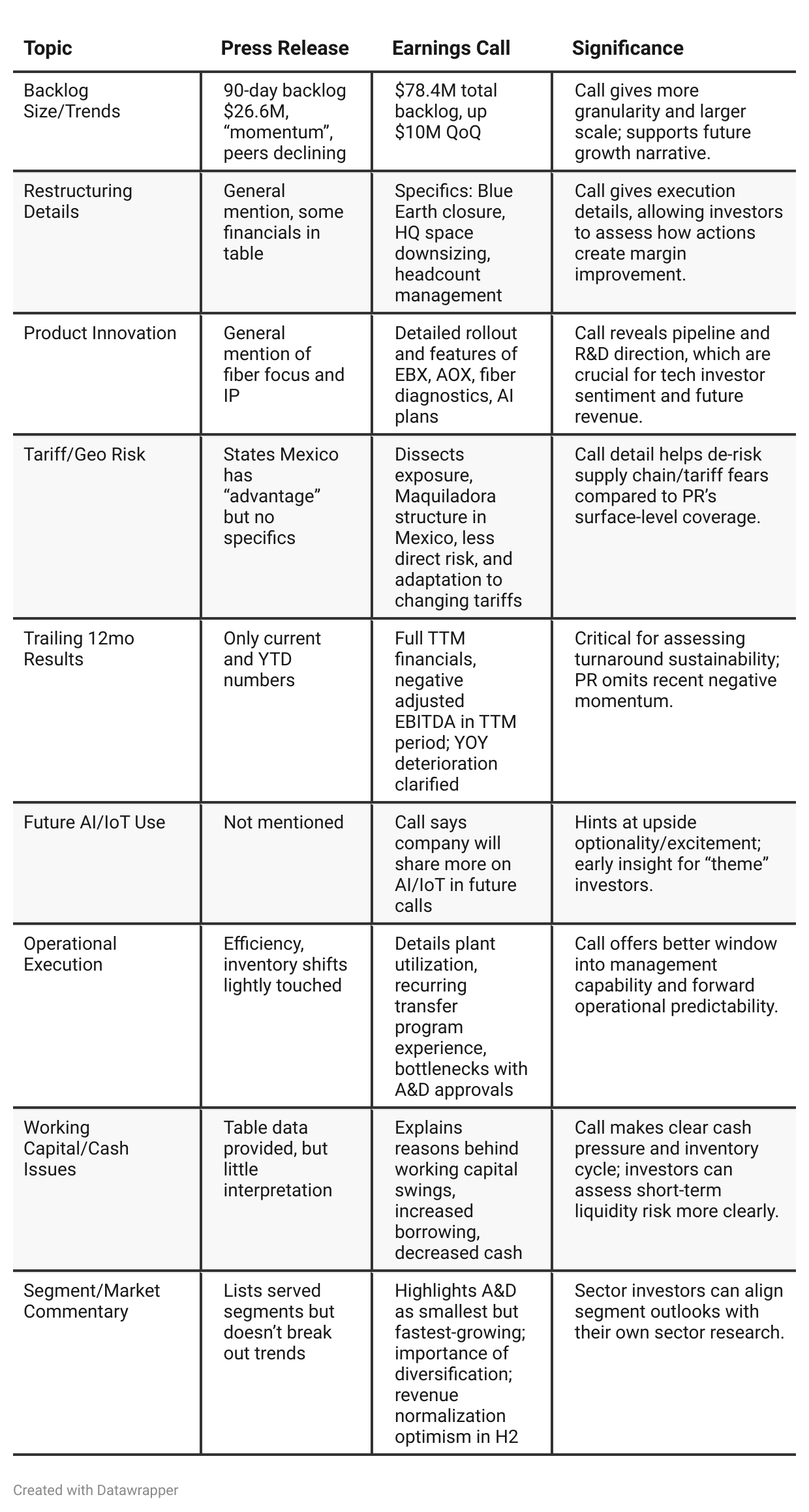

Press Release vs Call Transcript Comparison

Press Release is a curation of positive, investor-friendly “headlines,” while the Earnings Call provides much-needed context, transparency, and detail. The release omits weak trailing numbers and critical details on operational headwinds but is effective for a quick optimistic take.

The Earnings Call is necessary reading for investors who want to understand whether recent margin improvements are sustainable or a temporary aberration. It includes more “color” on both asset allocation (inventory, plant utilization) and liabilities (credit line, restructuring costs).

Risk Management: The call’s candid discussion of supply chain, geopolitical risk, and tariff exposure gives investors greater peace of mind—or at least, the ability to assess for themselves how exposed Nortech is to future shocks.

Turnaround Thesis: The press release makes restructuring sound done and success assured; the call makes clear that some of these actions are recent, and that their impact has not yet run the full course—raising both risk and opportunity.

AI and Tech Innovation: The call brings up AI and IoT plans and the R&D push toward fiber optics, which is a forward-looking differentiator not present in the release.

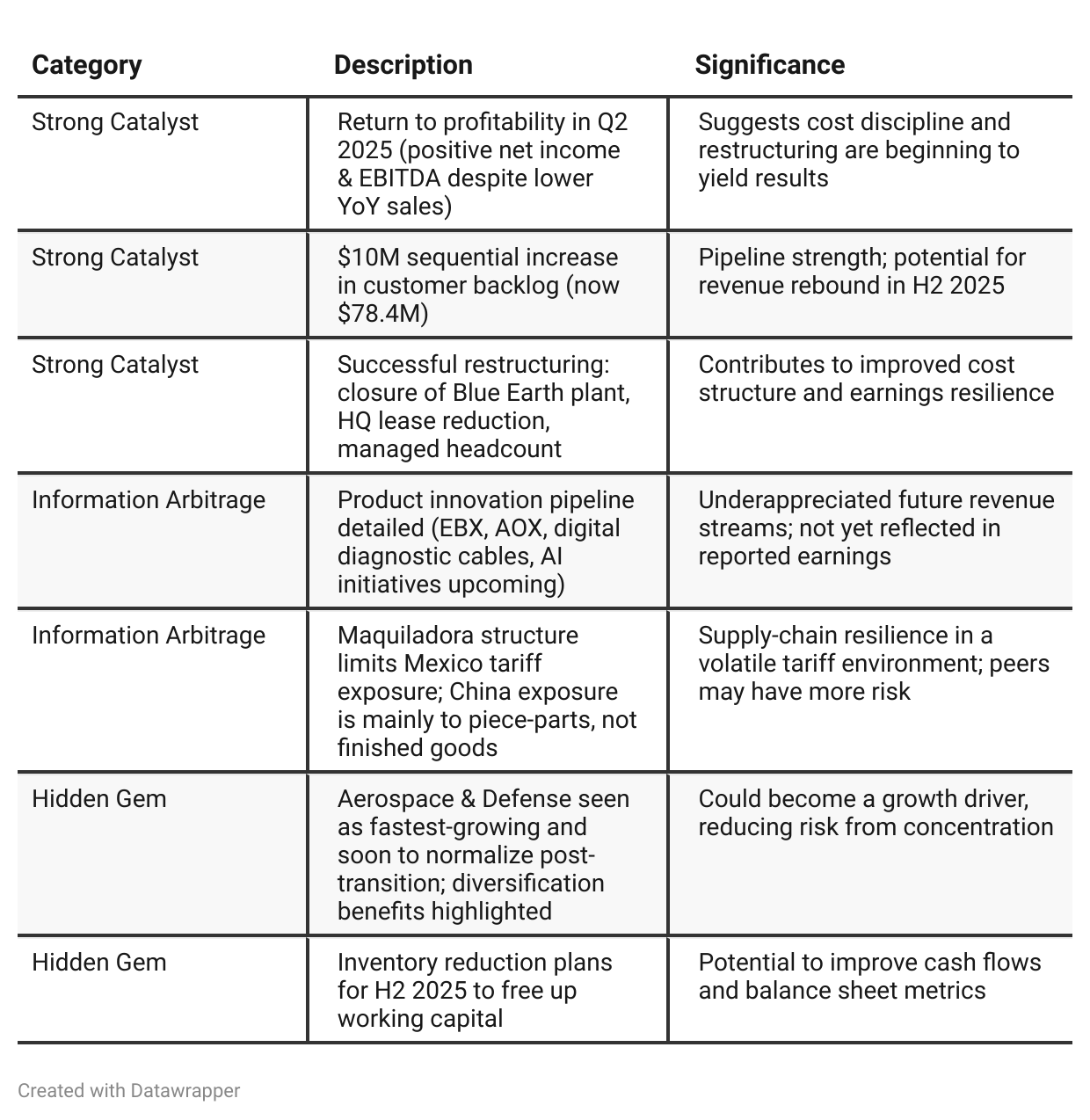

Positive Insights

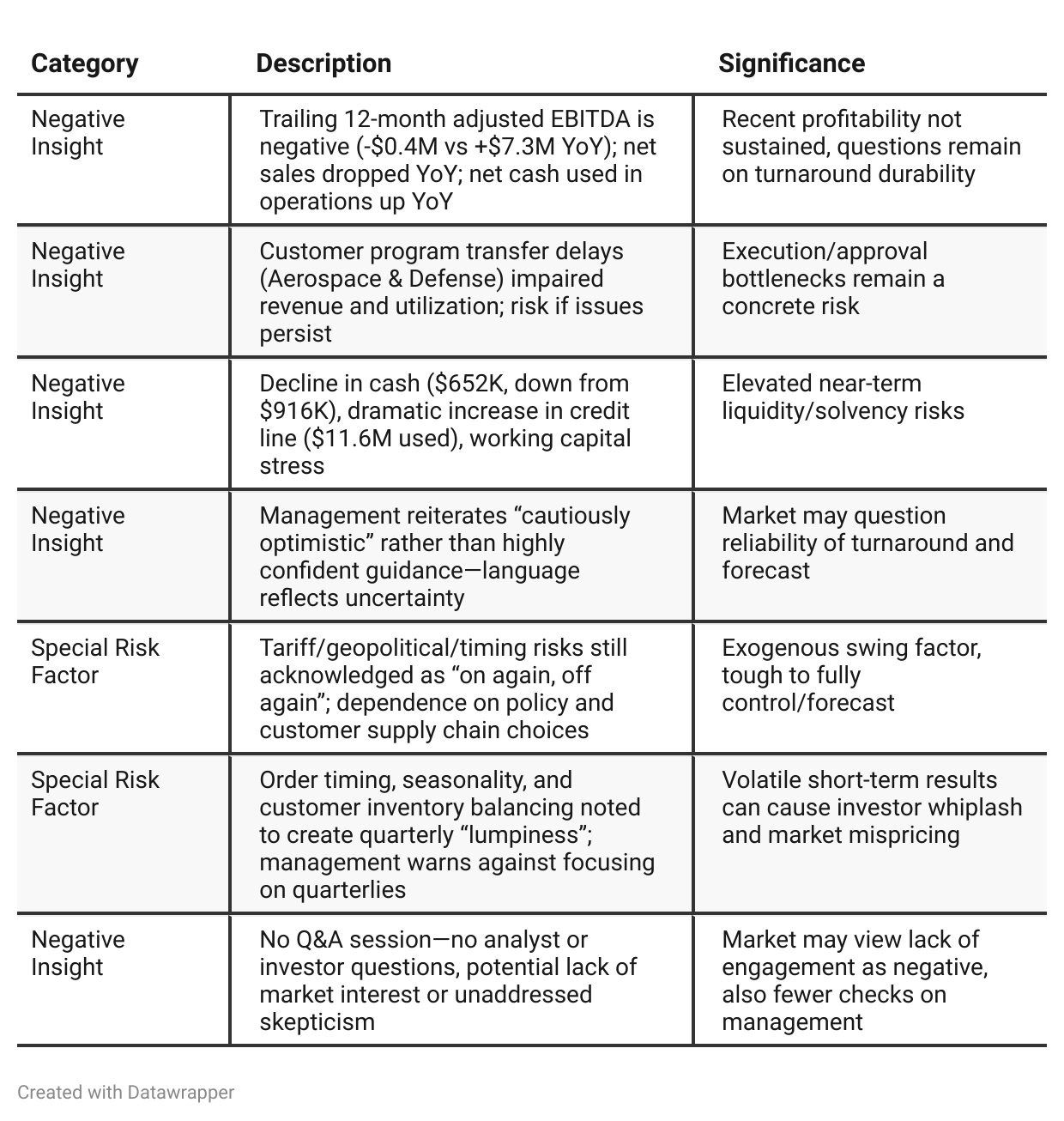

Negative Insights

Tariff Risk

Tariffs can impact manufacturers with China/Mexico facilities.

Nortech not importer of record from Mexico (Maquiladora structure), so direct U.S. tariff exposure on those goods is low.

Production in China generally built 'in country for country' (localized), so risk from Chinese/U.S. tariffs is mainly on parts, not whole goods.

Tariff situation described as "on again, off again"—company actively monitors and shifts sourcing/pricing as needed.

Sentiment Analysis

The overall sentiment toward NSYS is bullish. The relevant posts highlight positive developments such as debt restructuring providing increased financial flexibility, a surprising return to profitability, backlog stability, and a strong recovery in the aerospace and defense sectors. Additionally, price targets provided are above the current price, suggesting upward expectations. While one reference mentions a "bumpy ride," the emphasis is generally on improved fundamentals and growth, supporting an optimistic outlook.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2025 finds Nortech at a low point: earnings are under pressure, revenue falls sharply, and the company is undertaking aggressive restructuring to survive and reposition for growth. Management repeatedly references the pain and necessity of these changes, but expresses optimism about their eventual payoff and the company’s positioning for macro/fundamental trends such as nearshoring and fiber optic adoption.By Q2 2025, the narrative is more balanced and constructive. The management tone remains cautious, but now grounds optimism in concrete progress: improved profitability even in the face of lower revenue, enhanced operational efficiency, material backlog growth, and visible progress on transferring customer programs and securing approvals. There is a clear sense that the most disruptive period of transition is ending, and the company is beginning to see early benefits from its strategic moves. However, risks remain—especially around liquidity and the need to deliver on backlog in a still-volatile environment.

Year-over-year comparison

Q2 2024 summarized Nortech as a company deep in transition: proactively facing short-term sales headwinds, absorbing costs from restructuring and facility moves, and making foundational investments for future gains, even as order visibility remained low and gross margins compressed.

By Q2 2025, the narrative has matured. Management is able to point to tangible results from those prior sacrifices—profitability is returning despite lower revenue, operational improvements are being realized, and customer backlog is expanding (a leading indicator for future sales). The transition phase is giving way to a period of cautious rebound, with the company now focused on demonstrating that backlog translates to sustained financial recovery, while continuing to navigate liquidity constraints and external uncertainties (e.g., tariffs).

Final Takeaway

Nortech Systems is in a late-stage restructuring/early stabilization phase, focusing on operational efficiency, cost structure improvement, and new product introduction (fiber optics, digital technologies). While positive developments in backlog and margin improvement are encouraging, significant risks remain around liquidity, execution of customer transitions, and full-year profitability. Clear evidence of sustained cash flow and backlog conversion is needed before the turnaround can be considered durable. Verdict: HOLD. Investors should watch for continued improvement in margins, cash flow, and customer win conversion—especially in A&D and fiber optic products.