Noodles & Company (NASDAQ: NDLS) – Q2 2025 Earnings

Noodles & Company (NASDAQ: NDLS) – Q2 2025 Earnings

Earnings Release Date: Aug. 13, 2025

Stock Price: $1.10

Market Cap: $50.7 million

Q2 2025 sales of $126.4 million vs $127.4 million in the prior year

Q2 2025 EPS of ($0.12) vs ($0.05) in the prior year

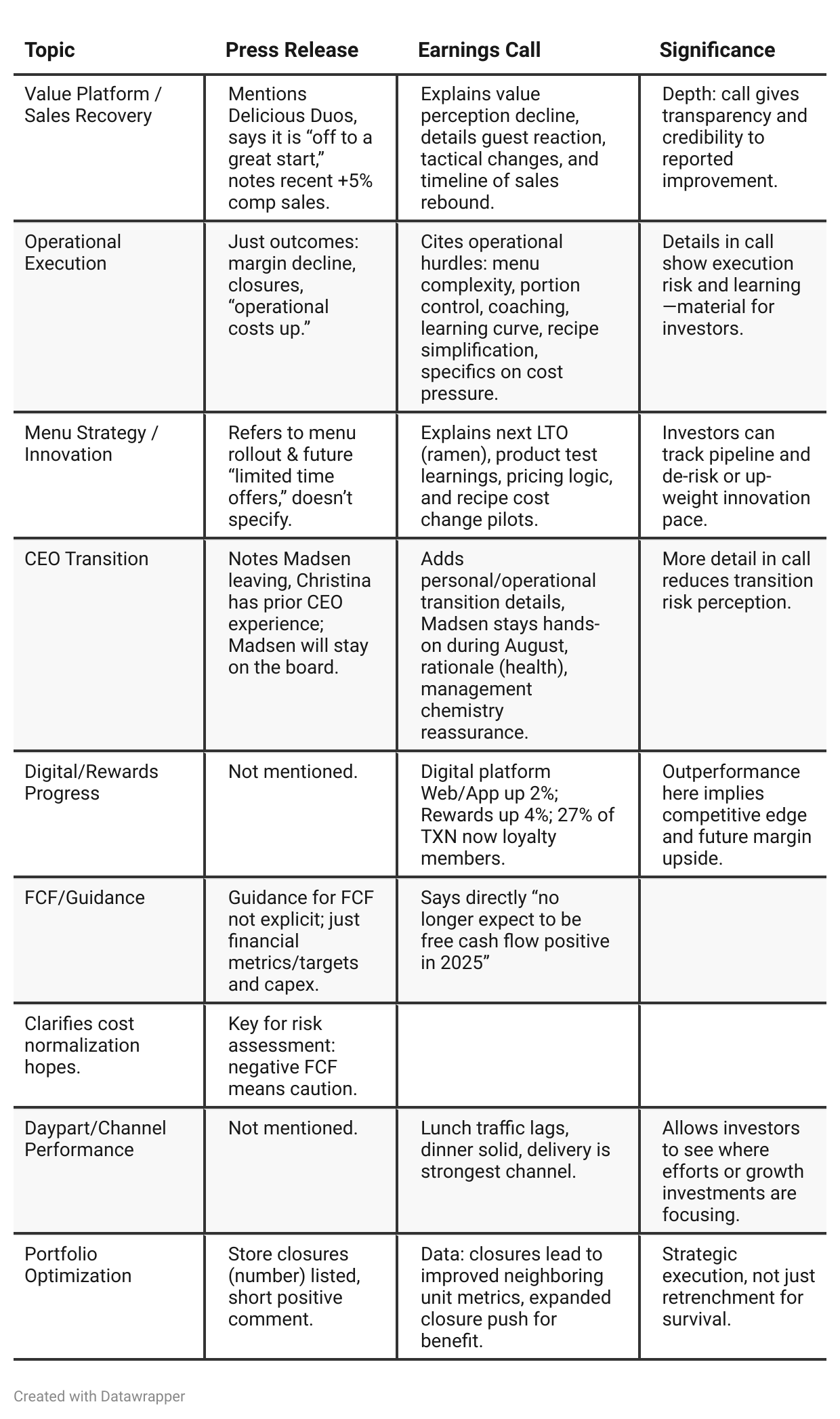

Press Release vs Call Transcript Comparison

Financial Health: Both documents confirm very tight liquidity/negative equity—call adds urgency about cost discipline, normalization, and shifting FCF timeline.

Management Accountability: Call gives transparency to why guidance changed, what was missed in modeling, and what is being changed—a positive for governance perception.

Investor Communication Tone: Call admits missteps on menu testing vs. real-world, reflects humility and realism; PR is more “polished” and less detailed.

Positive Catalysts Are Early & Fragile: All improvements (sales after Delicious Duos, loyalty growth, menu testing) are recent—implies any stumble can exacerbate negative trends.

Closures as a Double-Edged Sword: While portfolio optimization may boost nearby stores, it reduces scale, can increase per-unit G&A burden, and highlights former underlying performance drag.

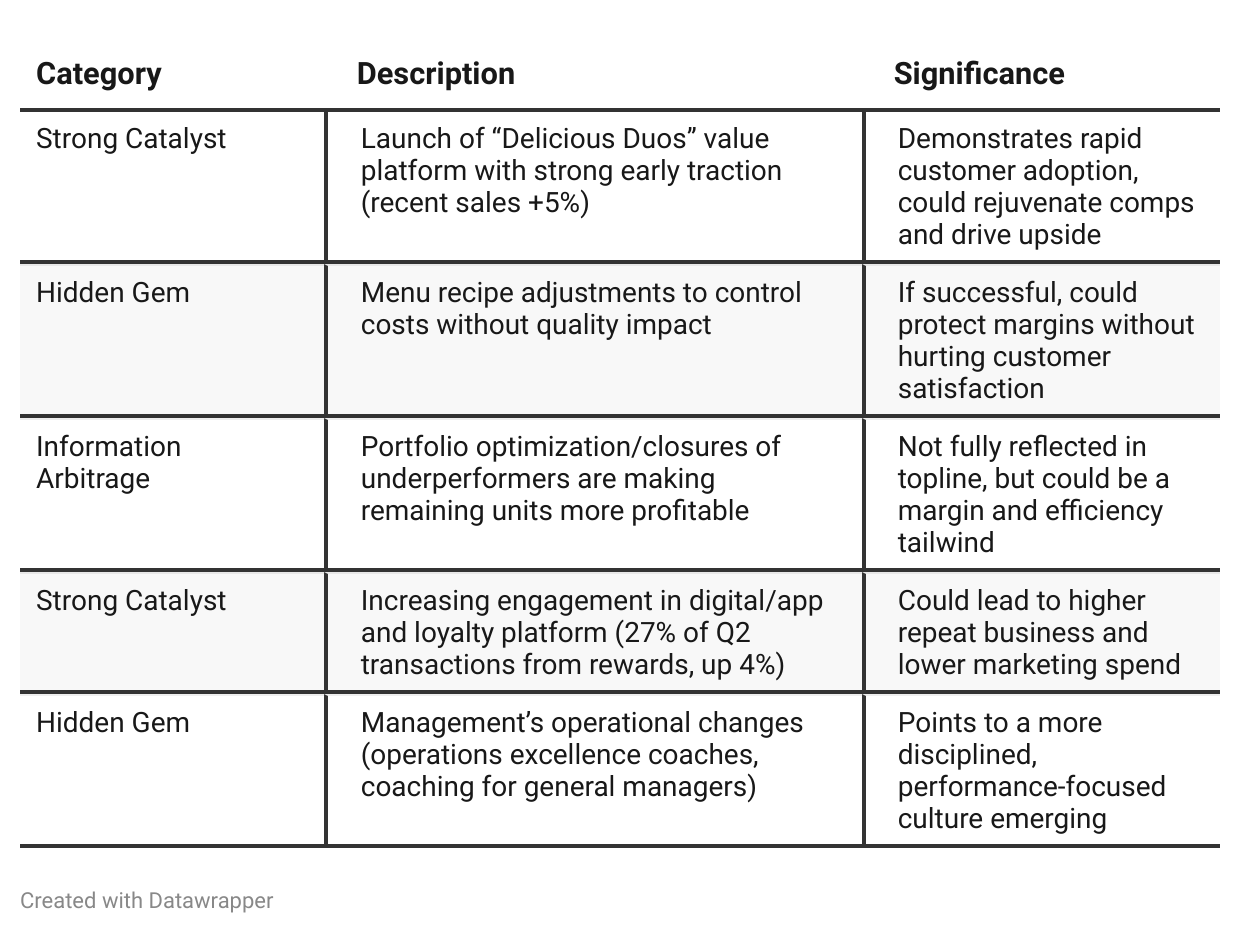

Positive Insights

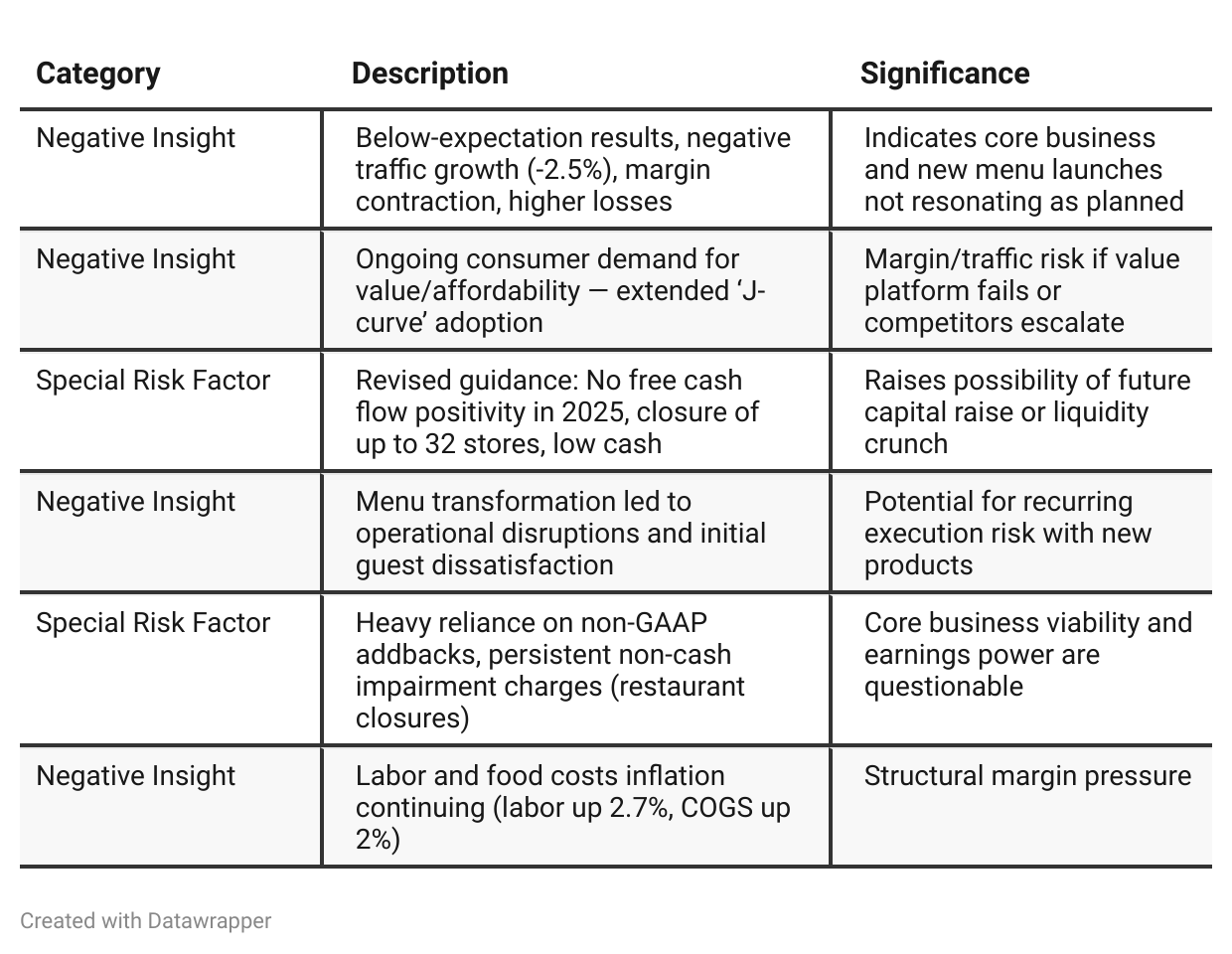

Negative Insights

Tariff Risk

Tariff/Trade Policy Mentions in Transcript:

The transcript includes only generic language in forward-looking statements about “economic conditions, including those resulting from inflation, increased interest rates, recessionary economic cycles, and changes in trade policies, including tariffs or other trade restrictions or the threat of such actions.”

There is no specific mention of U.S. tariffs, commodity sourcing actions, supply chain adjustments, or mitigation strategies regarding trade policy.

Analysis:

Since there are no direct remarks, tariff risk is not a currently disclosed or acute threat—at least according to management’s prepared discussion. However, as food inflation and sourcing/COGS are rising, it is possible tariff impact could become material, especially if management is silent due to ongoing negotiations or uncertainty.

Investors should monitor future calls, SEC risk disclosures, and cost-of-goods trends for any change in tone or new entrants regarding international supply chain risk, especially if U.S.-Asia or EU trade friction rises.

Previous Earnings Call

Quarter-over-quarter comparison

Noodles & Company entered 2025 on a wave of optimism: new menu launches, heavy marketing, and robust loyalty engagement had driven traffic and sales higher and fostered an upbeat “transformation” narrative. Management was confident that operational discipline and innovation positioned the company for both profitability and selective growth opportunities.However, by Q2 2025, the narrative shifts drastically. It becomes clear that the consumer environment is more challenging than anticipated; guest value perception drops after menu launches, margin improvement proves fleeting, and traffic turns negative. With this reality, the company pivots: substantial cost and portfolio rationalization, urgent menu/value fixes, and leadership change define the new direction. Optimistic language gives way to realism, and the focus shifts from “growth and innovation” to “stabilizing and adapting.”

Year-over-year comparison

Q2 2024: Noodles & Company was characterized by incremental gains, operational focus, and forward-looking optimism as it executed a measured and data-driven menu transformation and invested in digital/loyalty and cost control. There was a clear, steady path toward recovery and sustainable growth, with a strong belief in the company’s ability to out-execute the market amidst industry challenges.

Q2 2025: A year later, the optimism has given way to realism. The company is forced to reckon with harsher-than-expected macro realities: customers proved more sensitive to value and pricing than test markets suggested, leading to negative traffic and margin erosion. The tone shifts to defensive adaptation—rapid rollout of new value platforms, big menu and operational simplifications, and deeper closures. Leadership transitions and sharply downgraded financial outlooks reflect an urgent pivot from “growth and innovation” to “preservation and turnaround.” Execution and survival, not transformation and growth, define today’s narrative.

Final Takeaway

Noodles & Company is in a restructuring/turnaround phase, focused on fixing menu execution, recapturing value-seeking consumers, and optimizing its store portfolio. While recent menu and value-focused initiatives show green shoots, heavy operational risk, persistent margin contraction, and liquidity stress are glaring red flags. Consistent comp growth and cost discipline are essential for a true recovery. Verdict: HOLD, but watch for signs of cash burn or further strategic missteps—these could quickly change the risk/reward balance.