Mitek Systems, Inc. (NASDAQ: MITK) – Q3 2025 Earnings

Mitek Systems, Inc. (NASDAQ: MITK) – Q3 2025 Earnings

Earnings Release Date: Aug. 7, 2025

Stock Price: $9.12

Market Cap: $416.3 million

Q3 2025 sales of $45.7 million vs $45.0 million in the prior year

Q3 2025 EPS of $0.22 vs $0.25 in the prior year

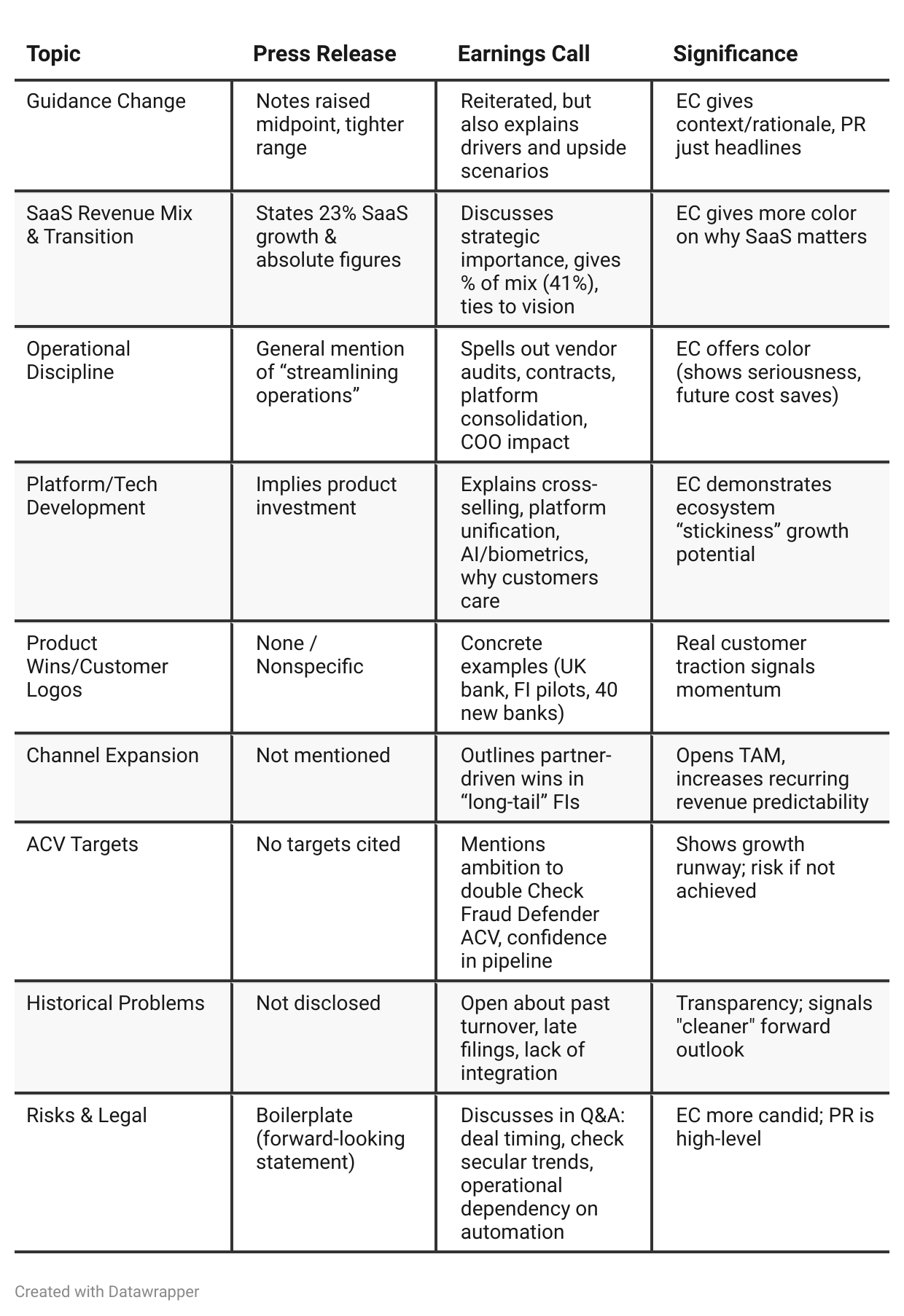

Press Release vs Call Transcript Comparison

Transparency: The earnings call is markedly more transparent about past missteps and operational weaknesses than the press release, which focuses on positivity. This candor builds trust if followed with execution.

Transition Risk: The migration to SaaS and fully unified platform has execution risks but is necessary for future valuation uplift. The EC’s discussion of internal milestones (e.g., Identity breakeven) are critical markers.

Management Turnover: Alluded to as being “in the past” on the call. Silence in the PR could mislead new investors who haven’t followed the saga.

Capital Allocation: Discussions of debt paydown, buybacks, and credit facility in the EC give richer context on how cash will be used (PR leaves this out).

Improved Cash Flow: Both documents highlight free cash flow, but the EC points out what drove the improvements and cautions that certain one-offs (interest arbitrage, working capital catch-up) will fade.

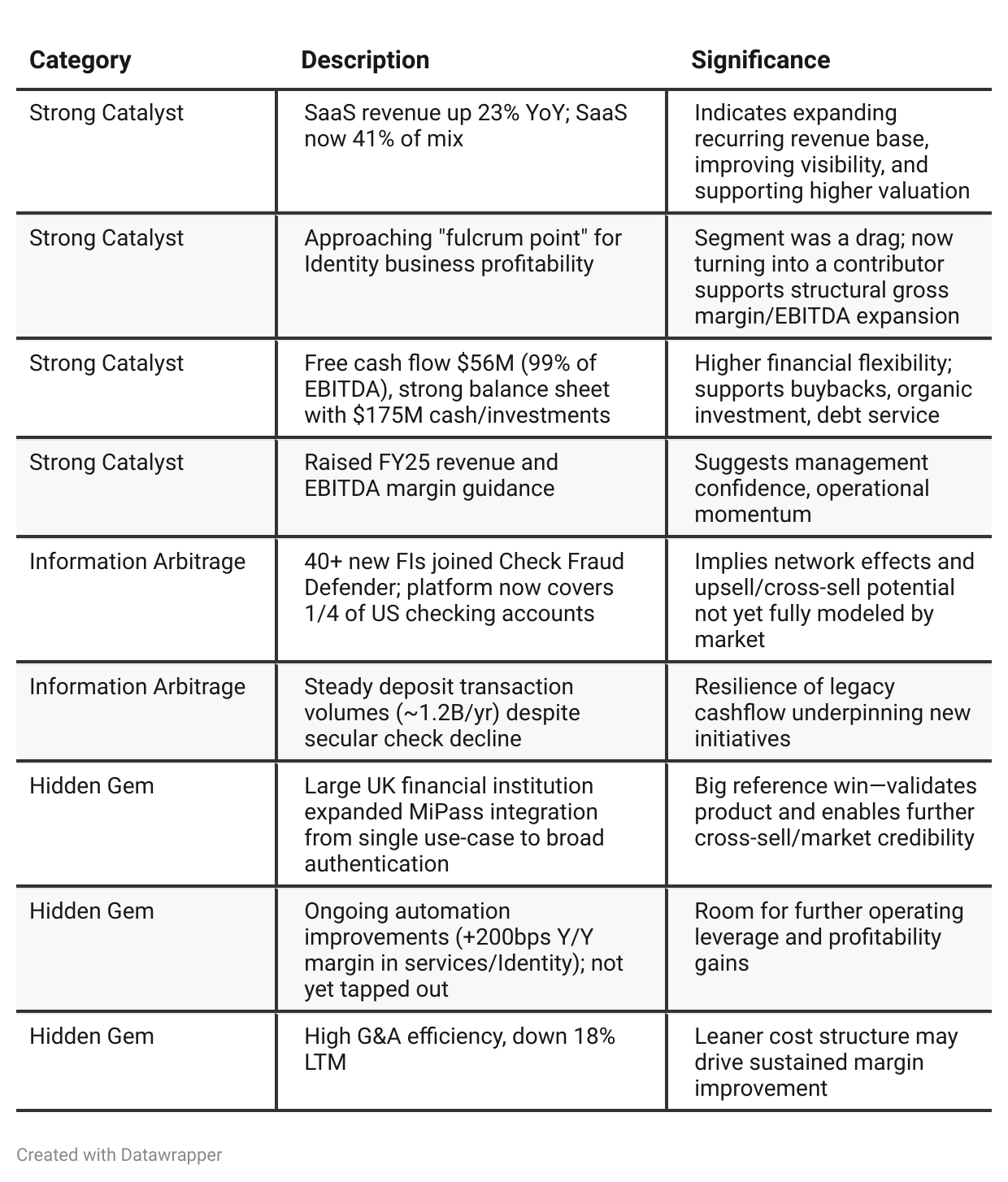

Positive Insights

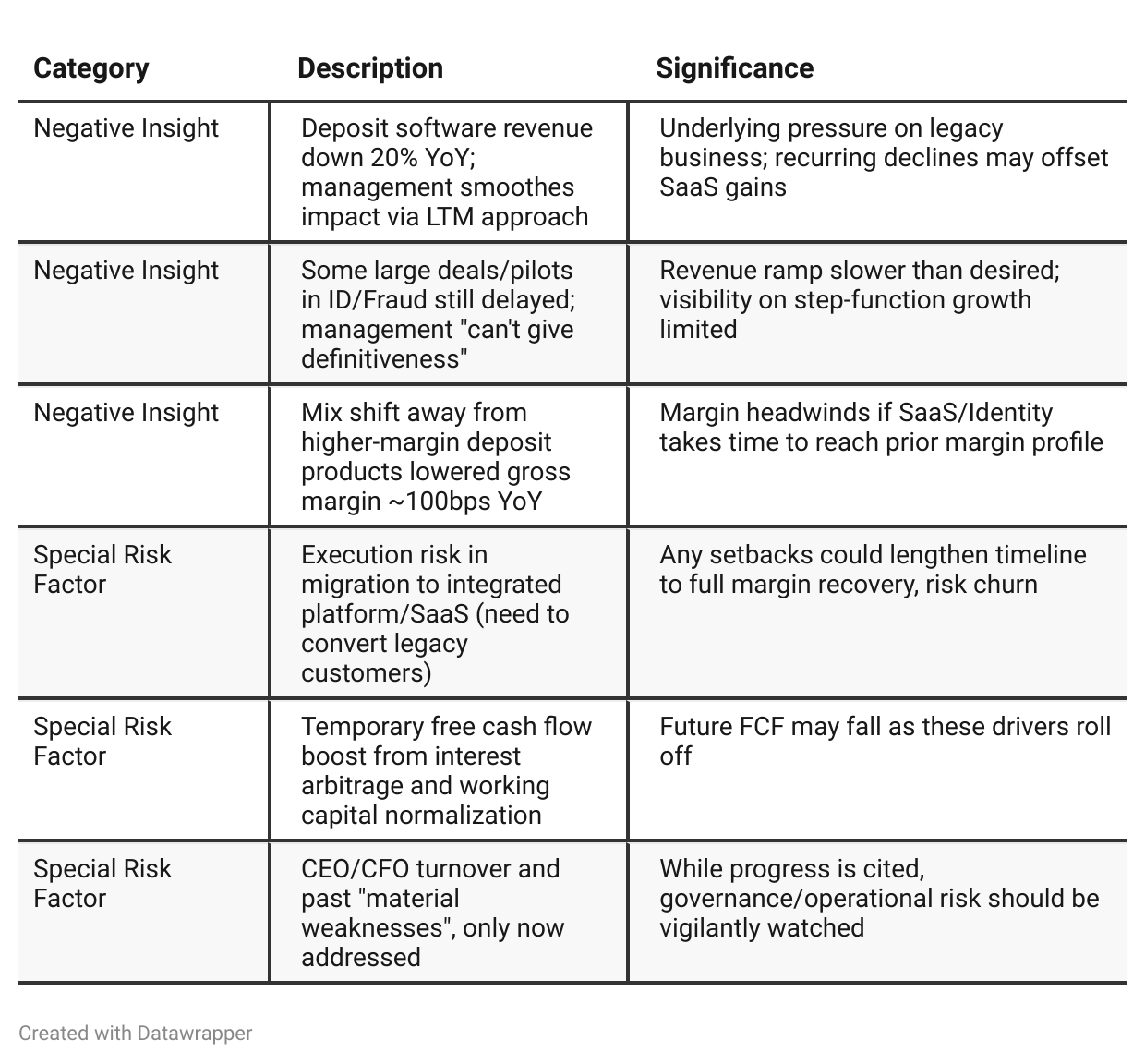

Negative Insights

Tariff Risk

There are no explicit mentions of U.S. tariffs, trade policies, or supply chain/geopolitical disruptions in the transcript. The business operates in digital/cloud software (digital identity and fraud prevention), which are generally less sensitive to direct tariff or trade policy shocks than hardware or physical goods industries. No supply chain shifting, contract renegotiation, or pricing actions related to tariffs are discussed. The company does serve customers globally and receives revenue in multiple currencies (dollar, euro, pound), but trade wars or tariffs do not currently appear as material risk factors per management commentary.

Sentiment Analysis

The overall sentiment toward MITK is bullish. Multiple mentions highlight strong price momentum, significant earnings growth, and bullish technical signals such as volume surges and resistance breakouts. MITK is described as undervalued and included in strong buy and top insider buy lists. Although a few tweets are informational, the majority reflect a clear positive investor sentiment, emphasizing both fundamental and technical strengths driving strong optimism around the stock.

Previous Earnings Call

Quarter-over-quarter comparison

From Q2 to Q3 2025, Mitek Systems’ narrative has evolved from “building a strong foundation” and early-stage transformation to tangible progress in execution, operational efficiency, and strategic milestones. In Q2, the company celebrated solid financial results and set ambitious SaaS and platform goals, focusing on re-tooling processes, growing mission-critical adoption, and investing in product innovation and automation. By Q3, the tone shifts to delivery: they are now reaching profitability milestones in the Identity business, ramping cash generation, hitting operational discipline targets, and citing high-value customer expansions as proof points. Management exhibits more confidence that legacy structural, cultural, and integration issues are resolved, and places increasing weight on durability, integrated solutions, and cross-product adoption as the new engines of value. Financial discipline, scale, and platform convergence now define the next phase, as the business moves from foundational optimization to scalable execution and solution leadership in digital Identity and Fraud.Year-over-year comparison

Q3 2024: Management is on the defensive. Revenue misses (especially in ID R&D biometrics) force a candid reset of expectations. The company initiates integration (of ID R&D), organizational tightening, and portfolio optimization. They are open about sales challenges, deal complexity, and cost headwinds, but remain confident about the long-term tech and market opportunity—yet short-term uncertainty dominates.

Q3 2025: The company’s story has matured into one of delivery and discipline. The new CEO presents a business that has digested legacy challenges, achieved meaningful integration, and reached profitability milestones in segments that had been dragging results. Messaging centers on operational excellence, platform unification, and measurable SaaS/recurring revenue progress. They acknowledge ongoing secular headwinds in legacy businesses, but the tone is of pragmatic, execution-focused optimism, emphasizing platform stickiness, scalable efficiency, and a credible pathway to durable margin and cash flow expansion. In short: Mitek’s journey is now about scaling and winning in a structurally sound, integrated platform model—having successfully navigated through its execution and integration turbulence of the prior year.

Final Takeaway

Mitek Systems is in a transformation phase, focusing on SaaS-driven Identity and Fraud solutions while stabilizing its legacy deposits platform. With strong revenue mix shift to SaaS, improving profitability, and a fortress balance sheet, execution on identity platform scaling and customer wins will determine its trajectory. While secular declines in legacy revenue present a risk, the company’s operational discipline, early evidence of platform stickiness, and institutional wins position it well for future multiple and earnings expansion. Verdict: Buy, with upside potential tied to successful SaaS ramp and execution on large enterprise deals.