MIND Technology, Inc. (NASDAQ: MIND) – Q2 2026 Earnings

MIND Technology, Inc. (NASDAQ: MIND) – Q2 2026 Earnings

Earnings Release Date: Sep. 9, 2025

Stock Price: $9.48

Market Cap: $75.5 million

Q2 2026 sales of $13.6 million vs $10.0 million in the prior year

Q2 2026 EPS of $0.24 vs ($0.11) in the prior year

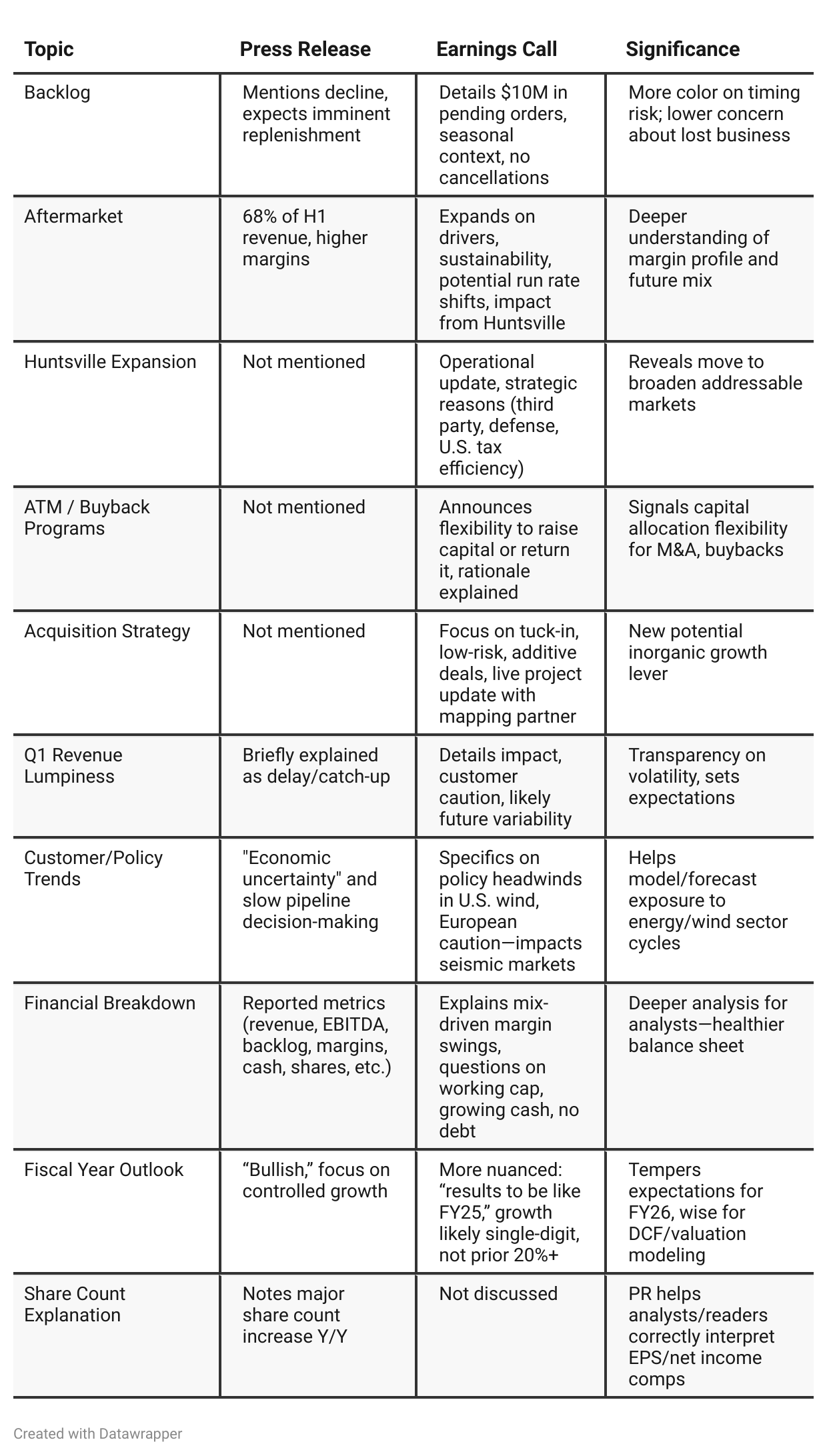

Press Release vs Call Transcript Comparison

Press Release is High-Level, Promotional: Focused on headline performance, broad optimism, and key GAAP/non-GAAP numbers. Relatively light on narrative around market risk, volatility, or execution specifics.

Earnings Call Offers Much More Depth: Includes live Q&A, nuanced takes on customer behavior, granular explanations for backlog swings, explicit discussion of timeline and uncertainty around order flow, and a rare dual capital tool strategy (ATM + buyback). Also, the call surfaces management’s views on sector disruption/opportunities (e.g., renewables, rare earths, defense applications) and operational choices for cost, scale, and margin protection.

Shareholder Value Focus: Both documents underscore commitment to driving shareholder value—call leans harder into specifics (flexibility, returns discipline, focus on low-risk tuck-in M&A).

Risk Transparency: Call more candid about customer caution, market softness, and potential for continued order delays, suggesting management wants to dampen expectations for uninterrupted growth.

Product and Market Diversification: Discussion of using manufacturing and service capacity for third parties and potentially moving into defense/maritime security illustrates a strategic attempt to broaden revenue streams as certain legacy markets (seismic) become choppier.

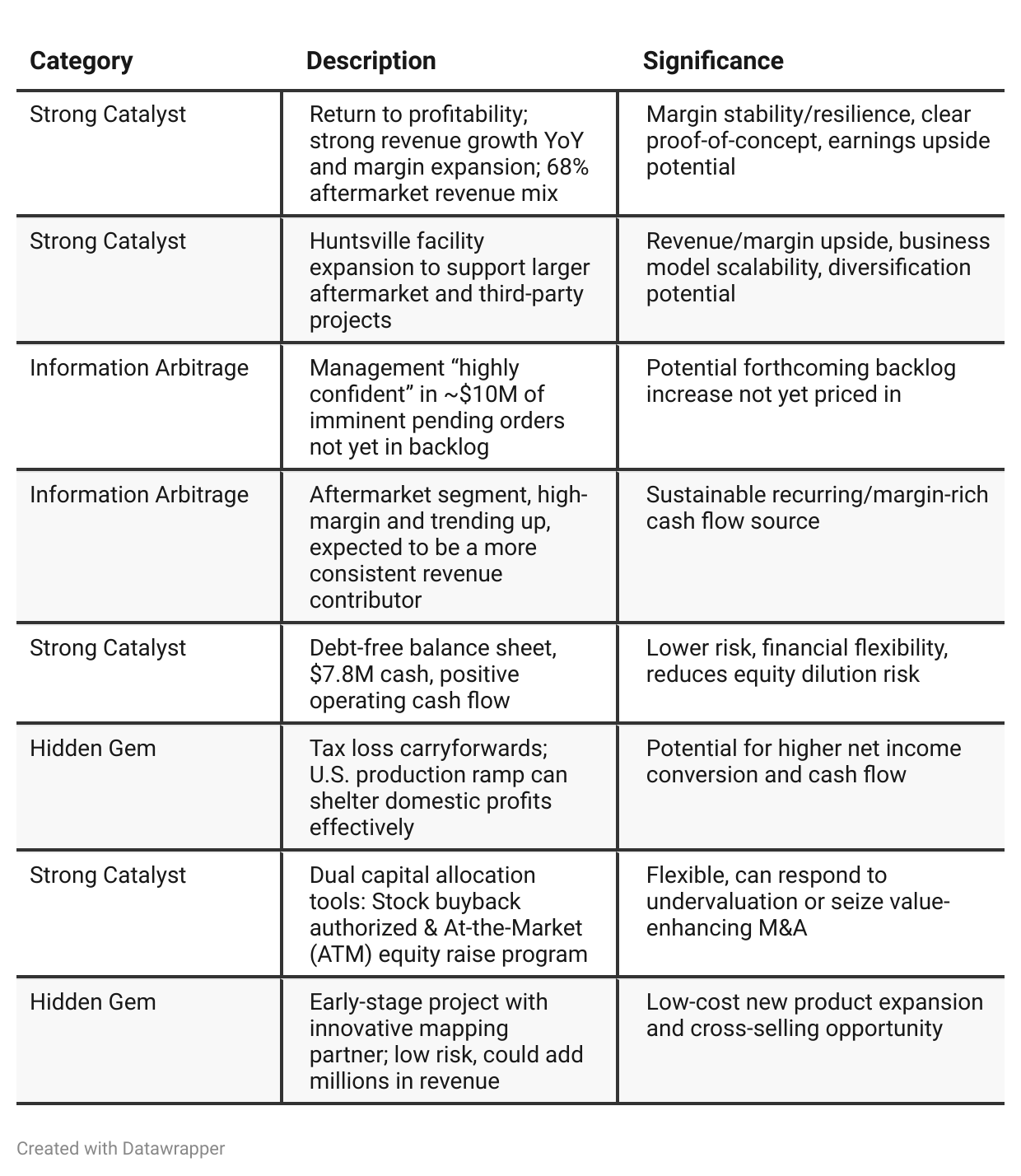

Positive Insights

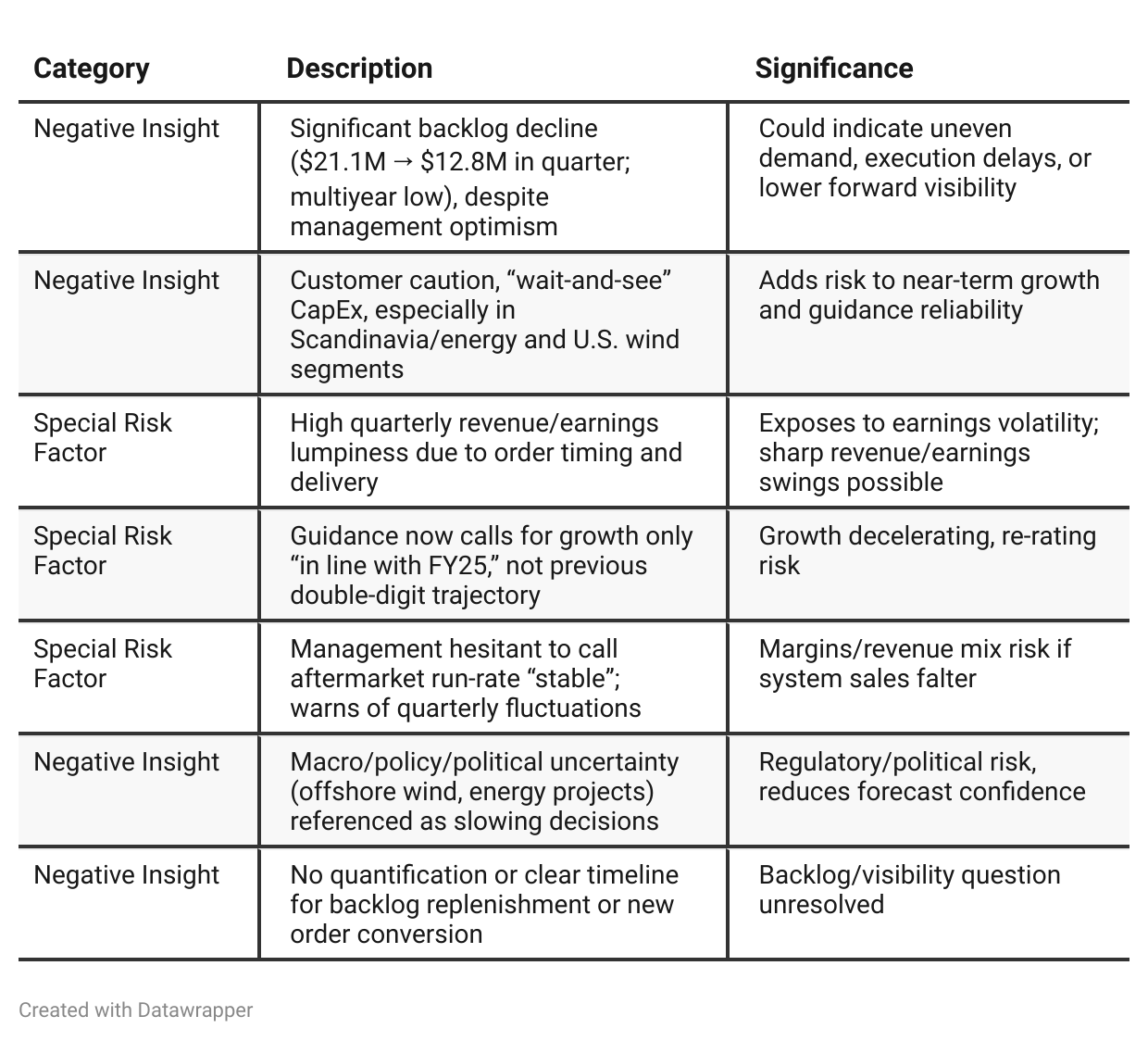

Negative Insights

Tariff Risk

Tariffs were not mentioned explicitly in the transcript.

No direct or indirect impact from tariffs identified in current business results or outlook.

U.S. facility expansion could provide some future insulation if trade tensions increase, but this is not management’s stated motivation.

Investor Action: No immediate need to monitor for tariff impact based on the current call, but investors should track any future commentary in filings or calls, as an escalation in tariff/trade risk could change the risk profile, especially for marine/high-tech manufacturing companies with global supply chains.

Sentiment Analysis

The overall sentiment is bullish. Most relevant commentary expresses optimism about $MIND’s growth prospects, technical setup, and the potential for significant upside moves (often citing expectations of 50-100% or more gains). Several posts emphasize strong fundamentals, margin expansion, a clean balance sheet, and positive catalysts such as ramping aftermarket revenue and operational improvements. While a minority of comments raise concerns about the mixed signals from simultaneous ATM/buyback activity or the recent backlog decline, these are generally outweighed by enthusiasm around technical analysis, tactical flexibility, and confidence in future orders. The bullishness is reinforced by repeated calls to hold or accumulate the stock in anticipation of further appreciation.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

In Q1, MIND Technology worked to reassure investors that poor results and a quarterly loss were driven by temporary delivery timing, not demand, and painted an optimistic picture of near-term recovery and active pipeline. Management talked up the transformation to a more resilient, growth-ready company with a robust balance sheet, technological leadership, and new growth initiatives. By Q2, after a successful financial rebound, that optimism was tempered by new transparency about execution risks, lumpiness in large order timing, and a shrinking backlog. The narrative shifted to one of cautious confidence, with more pragmatic growth guidance and a dual focus on maintaining flexibility for both capital raises and buybacks. Macro and customer caution—previously background risks—became more front-and-center, and management now emphasizes sustainable margin/cash flow (especially from aftermarket/services), ongoing innovation, and the need to manage through uncertain times. Investors are guided to expect “stable, not spectacular” growth, with potential for recovery hinging on backlog rebuild and sustained operating execution.Year-over-year comparison

Q2 2025: MIND Technology was riding a wave of strong sequential and year-over-year performance, heralding growth, expanded profitability, and a major capital structure transformation that removed market overhangs. Management emphasized a clean balance sheet, high backlog, thriving customer engagement, margin gains, and the flexibility to pursue new business or M&A with greater agility.

Q2 2026: While the company delivered financially, the narrative has matured into one of prudent optimism and risk management. Management openly discusses volatility, the sharp decline in backlog, customer spending hesitation, and the possibility of quarterly swings due to macro and end-market headwinds. New capital allocation programs—ATM and buyback—highlight a toolkit for both opportunities and self-defense. The narrative is now one of resilience and tactical discipline: focusing on recurring revenue, operational adaptability, and shoring up profitability in a less predictable demand environment.

Final Takeaway

MIND Technology is in a stabilization-to-growth phase, focusing on margin expansion, aftermarket/service growth, and operational flexibility. While a clean balance sheet and signs of an improving revenue mix are encouraging, the sharp backlog drop and management’s softer growth guidance highlight near-term demand/churn risk. Execution on backlog replenishment and proven aftermarket consistency will be critical for future performance. Verdict: Hold—with a positive bias if pending order catalysts deliver, but risk control is warranted given macro and lumpiness concerns.