Mistras Group, Inc. (NYSE: MG) – Q1 2025 Earnings

Mistras Group, Inc. (NYSE: MG) – Q1 2025 Earnings

Earnings Release Date: May 7, 2025

Stock Price: $9.59

Market Cap: $297.3 million

Q1 2025 sales of $161.6 million vs $184.4 million in the prior year

Q1 2025 EPS of -$0.10 vs $0.03 in the prior year

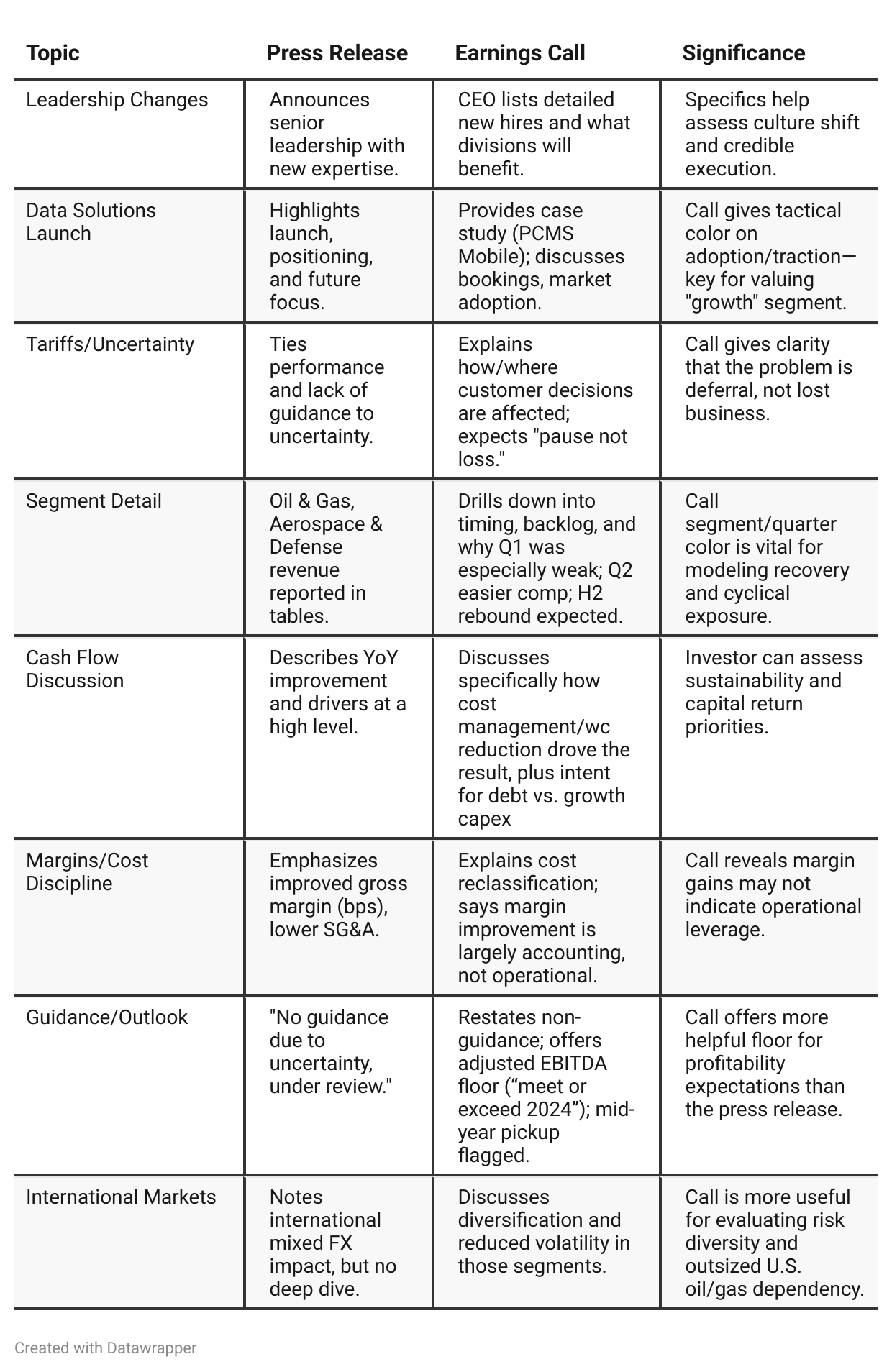

Press Release vs Call Transcript Comparison

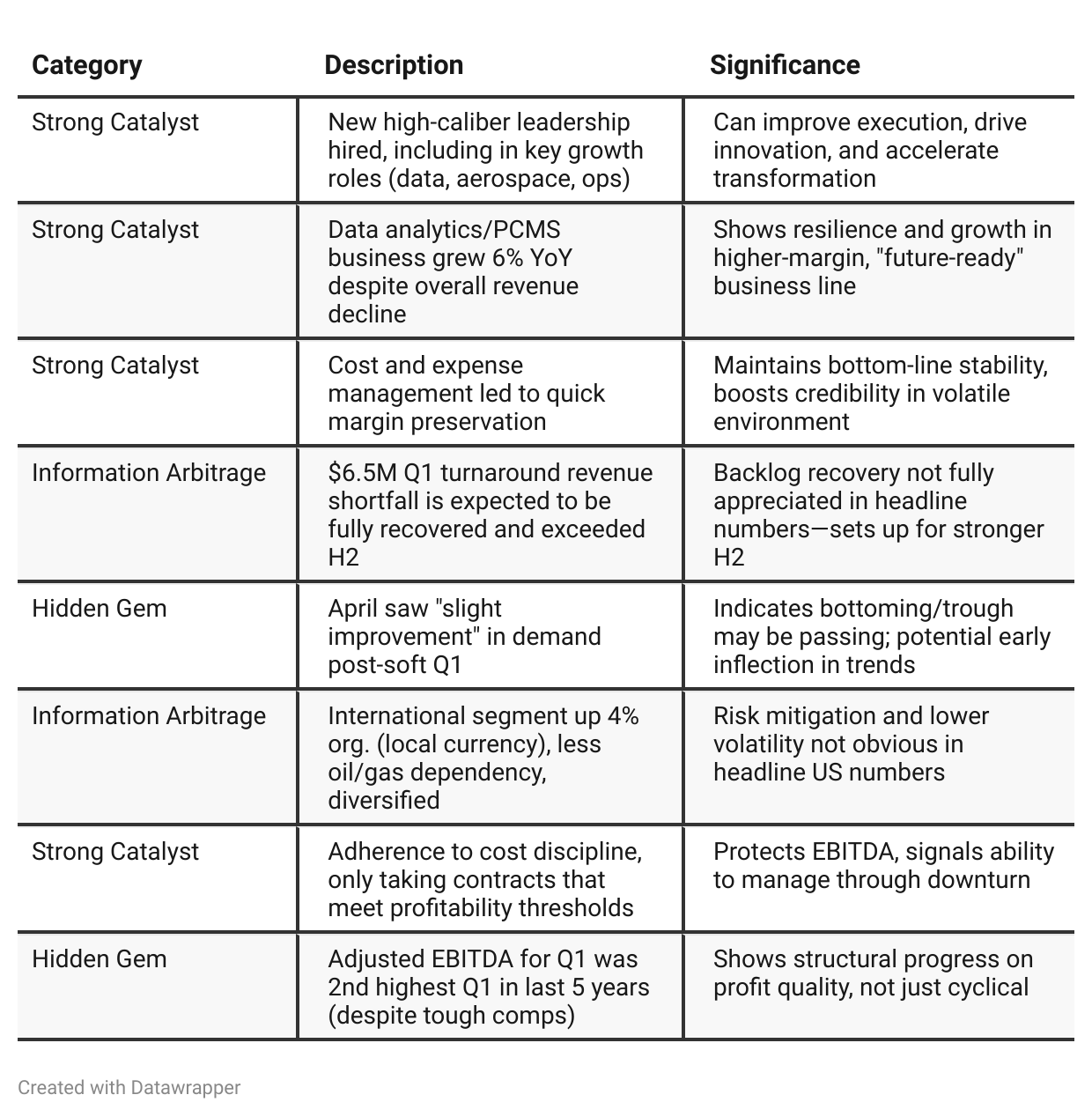

Growth Focus: Despite current challenges, company is investing in talent and proprietary digital platforms—signals focus on transforming revenue mix, not just cost-cutting.

Recovery Path Dependency: Explicit linkage between macro clarity (trade, tariffs) and project cadence means investors should monitor policy headlines closely.

Transparency Improving: Restatement and cost reclassification, plus more granular segment reporting, are positive signs for governance.

Leverage Risk Moderate: Leverage ratio is up but under control; management prioritizes debt reduction unless attractive growth capex is found.

No Customer Attrition: CEO stressed that market share remains stable, clients deferring rather than defecting.

Positive Insights

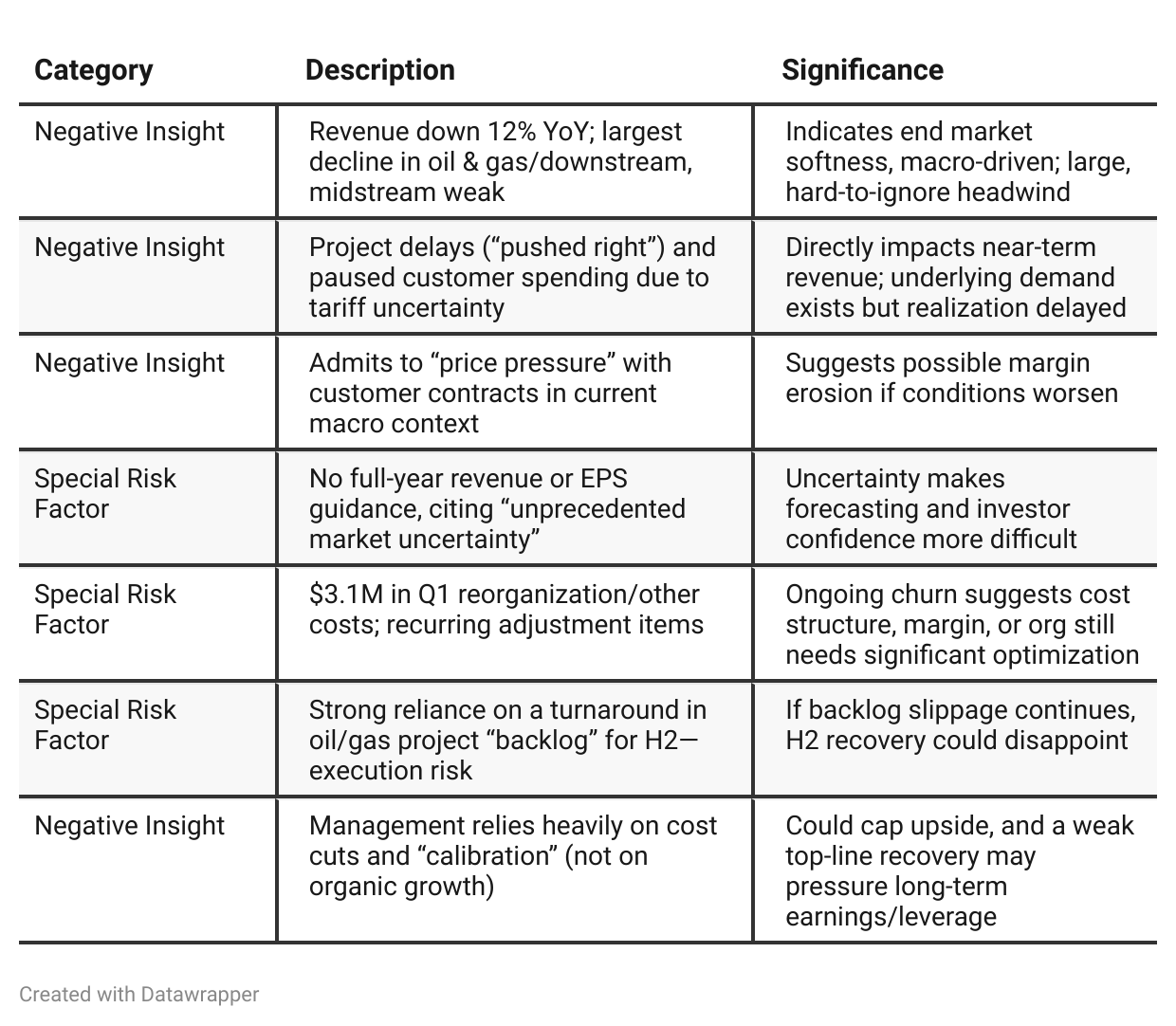

Negative Insights

Tariff Risks

Impact Not Direct, But Significant Indirect Effect: The company says tariffs have limited direct effect (assets in North America), but customers (especially in O&G, manufacturing, and aerospace) are experiencing supply chain disruptions, budget reviews, and delaying project starts. This is directly cited as a driver of the Q1 revenue shortfall.

Mitigation/Response: Mistras is taking a “proactive” and consultative approach with its customers, reviewing contracts for ROI, and working to provide increased value and analytics—no mention of relocating supply chain or adjusting internal production.

Competitive/Market Share: No explicit comment that tariffs are eroding market share. Management believes the “pause” in activity is cyclical and demand remains robust, just not yet realized.

Future Effects: Management states that in the long run tariffs might be positive for Mistras if advanced manufacturing (i.e., reshoring) increases in the U.S., thereby expanding demand for its services. However, in the near term, tariff-induced uncertainty and supply chain disruptions are causing customers to delay spending and projects, which directly impacts Mistras’ top-line results.

Previous Analysis

Quarter-over-quarter comparison (Previous Analysis)

Mistras exited 2024 with strong financial momentum, successful cost discipline, and renewed optimism from a high-profile CEO transition. The mood was positive, touting record EBITDA margins, broad-based growth, new leadership energy, and successful customer engagement. They signaled confidence in extending these achievements, albeit with some caution about macro factors and a pending review of business lines under new leadership.

By Q1 2025, the narrative shifts noticeably to a more sober, operationally-focused tone. Revenue headwinds materialized faster and sharper than expected, mainly due to customer delays from tariffs, budget uncertainty, and supply chain disruptions. Management dials up its emphasis on cost controls and prudent commercial discipline to defend margins as revenue falters. However, they also signal potential upside from deferred O&G turnarounds and the launch of new digital offerings. Talent investment accelerates, showing a pivot toward innovation and future growth. The company retains long-term optimism but is candid about near-term uncertainty and remains cautious on providing guidance until visibility improves and strategic review is completed.

Year-over-year comparison

Q1 2024: Mistras is energized, executing strongly, and emboldened by transformative operational, pricing, and organizational initiatives (Project Phoenix). The company is posting record numbers, raising guidance, and is confident about sustaining top- and bottom-line momentum into 2025 and beyond. Strategic investments (especially in digital/data and Aerospace & Defense) are presented as levers for future growth and margin expansion.

Q1 2025: The narrative pivots to resilience over growth: Mistras faces unexpected macro and tariff-driven revenue pressure in major markets. Leadership responds with rapid cost controls, strict contract/profitability discipline, and a focus on delivering customer ROI and developing digital solutions (now in execution, e.g., PCMS Mobile). Optimism is more measured and conditional; the company’s long-term value proposition is unchanged but the immediate focus is on weathering external volatility. No formal annual guidance is offered—the company is instead aiming to defend margins and position for recovery when macro conditions improve.

Final Takeaway

Mistras Group is in a transition/stabilization phase, focused on strategic cost controls, digital transformation, and organizational renewal. While deferred turnaround revenues and the successful launch of PCMS Mobile provide potential positive surprises, near-term risks remain from macro-driven customer spending delays and pricing pressure. Execution on digital growth, margin preservation, and project pipeline conversion will be critical. Verdict: HOLD, with moderate upside if revenue stabilizes and digital growth accelerates, but downside risk if macro/tariff headwinds persist or cost controls are insufficient.