Medifast, Inc. (NYSE: MED) – Q2 2025 Earnings

Medifast, Inc. (NYSE: MED) – Q2 2025 Earnings

Earnings Release Date: Aug. 4, 2025

Stock Price: $13.75

Market Cap: $151.1 million

Q2 2025 sales of $105.6 million vs $168.6 million in the prior year

Q2 2025 EPS of $0.22 vs $(0.75) in the prior year

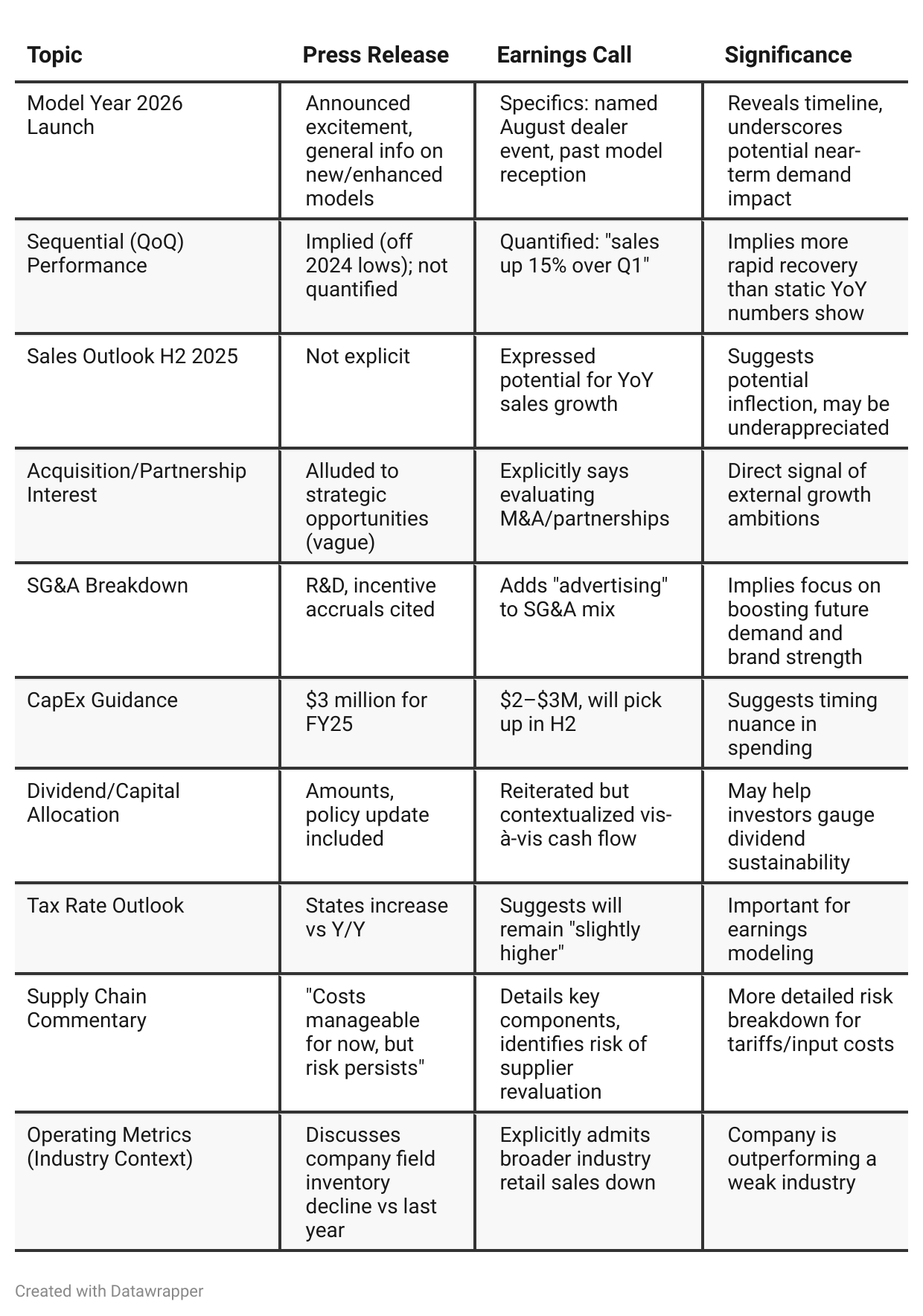

Press Release vs Call Transcript Comparison

Communication Tone: The call was more candid, providing more specifics on timing (e.g., August dealer event), raw materials, and relative performance. The press release was more curated for broad consumption, with less detail.

Dealer/Channel Health: Multiple references on the call to dealer caution and retail environment—useful for investors monitoring industry cycle turns.

Cash Flow and Dividends: Sufficient cushion remains, but dividend sustainability could be stressed if net income remains under pressure.

Signaling to Investors: Acquisition ambition, portfolio innovation, and focus on inventory all suggest management is navigating proactively, not just defensively.

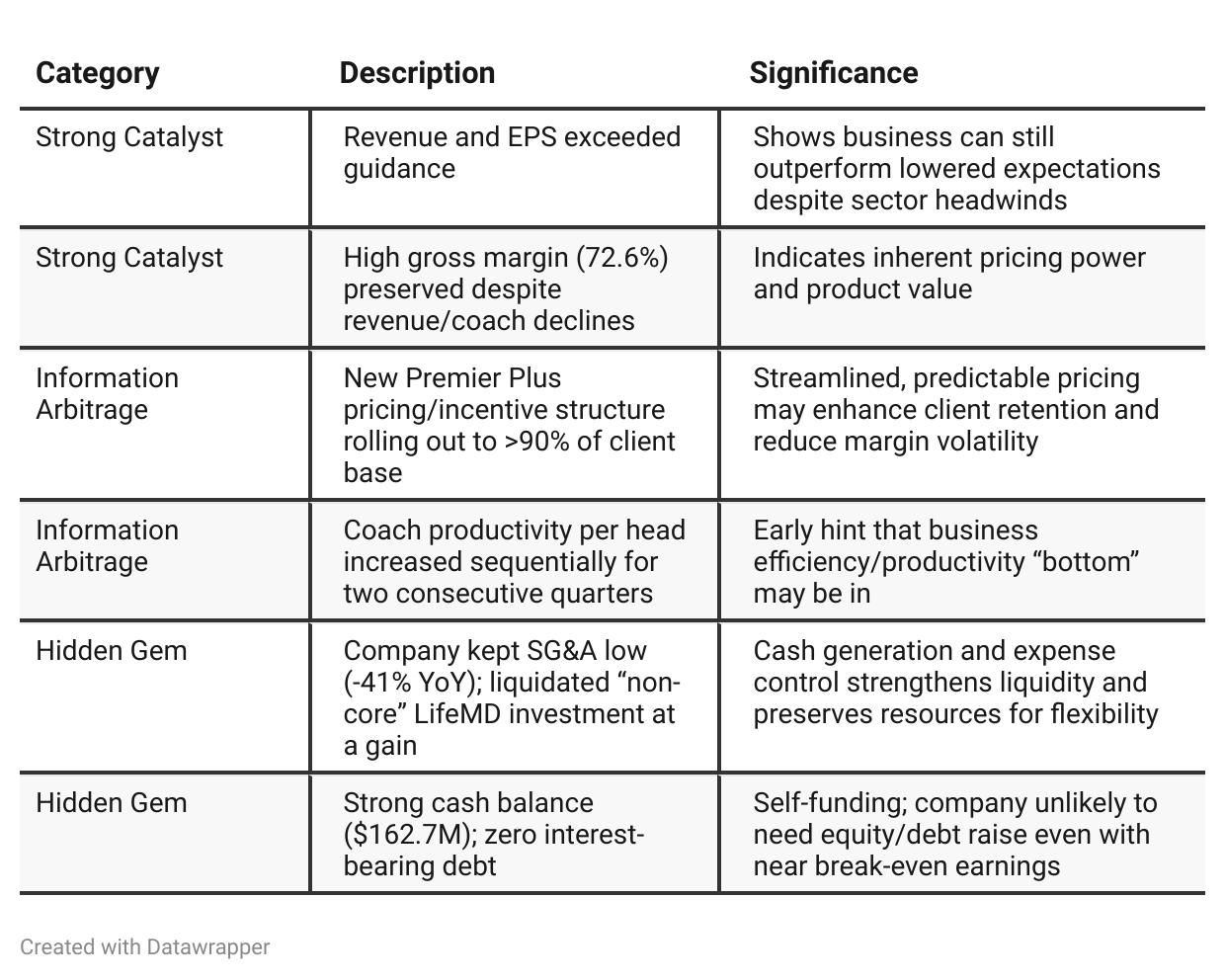

Positive Insights

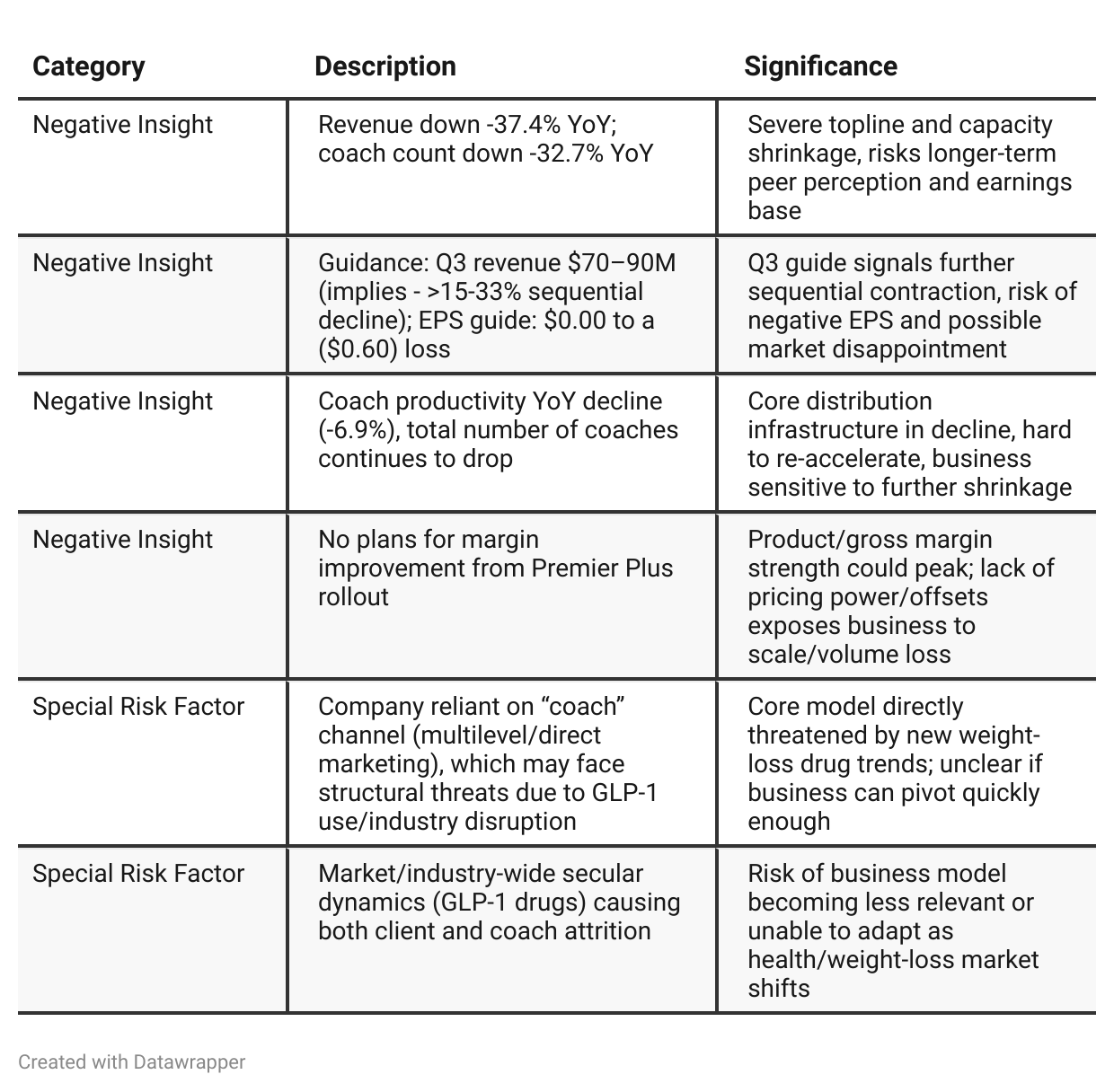

Negative Insights

Tariff Risk

No mentions of tariffs, trade policy, or related supply chain/geopolitical risks were found in this transcript. There is no discussion of international trade disruptions, tariff cost impacts, or contingency plans regarding tariffs. Investors with exposure to import/export risk should check future filings, but current transcript shows no focus in this area.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: MetaFast presented itself as a company in the early stage of a challenging turnaround, responding to disruption from GLP-1 drugs by betting on the power of its coach network and the flexibility of its product suite. Management acknowledged daunting YoY declines, but optimism was staked on new coach cohorts, product launches (Active, Ascend), and early signs of stabilization in productivity and recruitment. The core message was: “Our model, if empowered and modernized, can survive and grow despite industry upheaval.”Q2 2025: The narrative has become more pragmatic and tactical. Management’s optimism is tempered with realism—the scale and persistence of revenue/post-coach declines are unmistakable. Attention is centered on operational execution: new pricing (Premier Plus), tighter compensation logic (EDGE), better digital tools, and a broader narrative of addressing “metabolic health,” not just weight loss. Guidance is downbeat, but there’s careful communication about liquidity, cost control, and sequential improvements in per-coach productivity. The company frames itself less as “disrupted, but soon to grow” and more as “operationally resilient, evolving to endure and eventually recover.”

Year-over-year comparison

Q2 2024: MetaFast approaches the year with aggressive transformation plans, targeting the explosive growth in GLP-1 support markets and betting on new products, integrated solutions, and customer acquisition via marketing spend. Management is enthusiastic and vision-driven, positioning the company as nimble, bold, and well-funded to invest through the storm.

Q2 2025: A year later, reality has set in. The company’s network and top line have contracted drastically as the GLP-1 revolution matures, and customer acquisition challenges intensify. Leadership pivots to operational discipline: cost management, retention-focused innovation, coach and customer lifetime value. Tactical changes (pricing, incentives, digital tools) aim to stabilize core metrics and prepare the business for durable, if more modest, future growth. The narrative is of resilience and adaptation—less bold, more focused on sustainable execution in a harsher landscape.

Final Takeaway

MetaFast (MED) is in a late-stage transformation phase—facing severe topline/headcount pressure, but exhibiting strong discipline in cost control and margin defense. Its future depends on stabilizing its coach network, demonstrating true traction in its new pricing/product programs, and finding a viable place alongside the industry’s GLP-1 disruptors. Liquidity buys time, but secular challenges necessitate clear, quantifiable stabilization within the next few quarters. Verdict: HOLD, with risk/reward balanced pending evidence of revenue/coach “bottoming” or successful new product adoption.