Mama's Creations, Inc. (NASDAQ: MAMA) – Q2 2026 Earnings

Mama’s Creations, Inc. (NASDAQ: MAMA) – Q2 2026 Earnings

Earnings Release Date: Sep. 08, 2025

Stock Price: $9.44

Market Cap: $354.9 million

Q2 2026 sales of $35.2 million vs $28.4 million in the prior year

Q2 2026 EPS of $0.03 vs $0.03 in the prior year

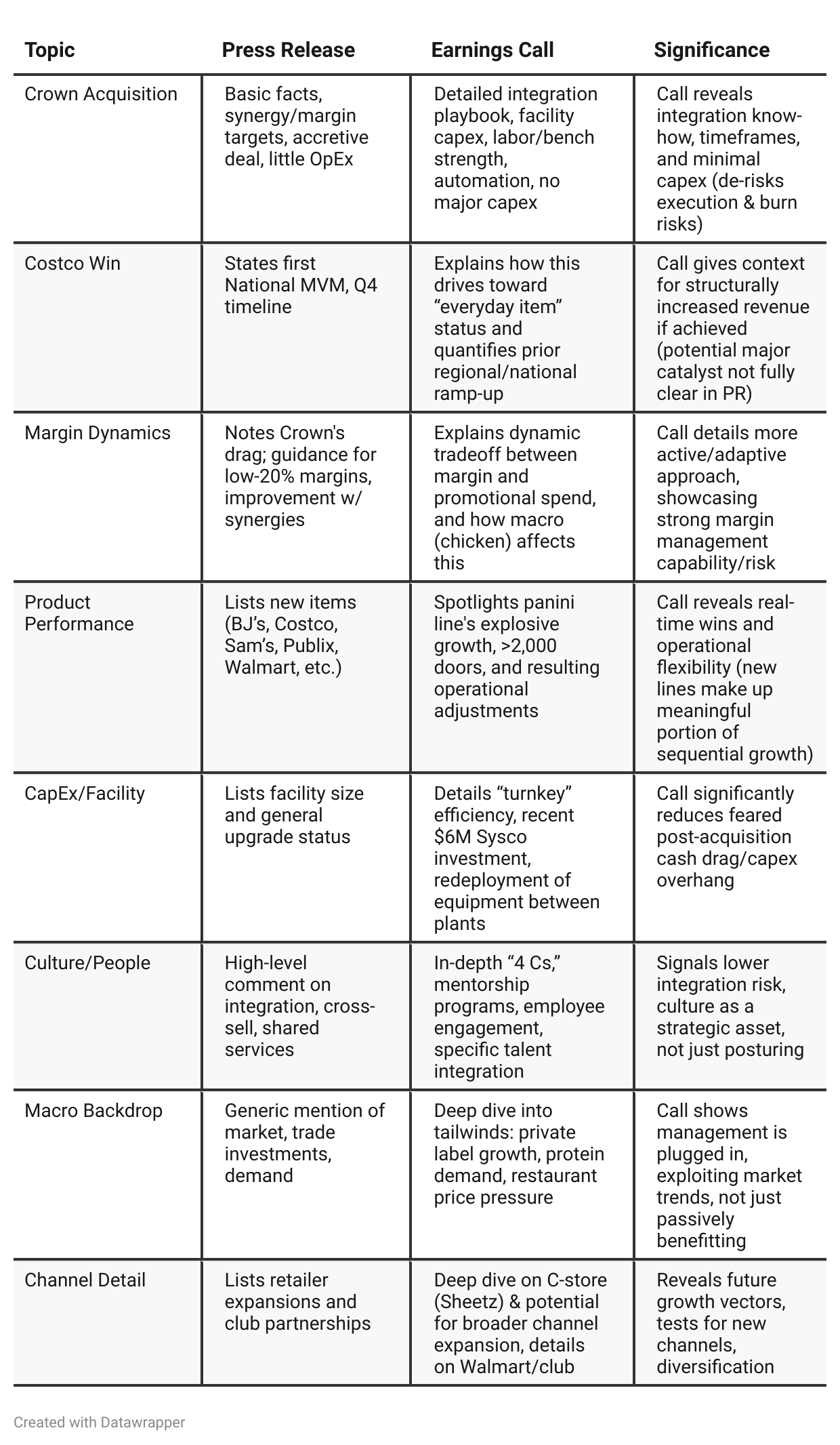

Press Release vs Call Transcript Comparison

Management Tone/Confidence: On the call, management is extremely transparent, candid, and focused on concrete operating and integration levers. Their willingness to share both wins and operational details increases credibility.

Capital Structure/Balance Sheet: Multiple mentions of very conservative leverage, proactive facility amendments, and a strong cash position post-acquisition. Call directly addresses how future opportunities will be funded, reducing dilution/funding risk.

Integration Experience: Management openly references doing this before with Creative Salads, creating a “pattern recognition” effect that makes the Crown acquisition measurably less risky than a typical bolt-on.

Capacity to Double Revenue: CEO’s conviction (supported by practical facility/equipment/labor info) that the current network could support doubling revenue provides a quantitative target for investors.

Macro Awareness: The team is acutely aware of tailwinds/risks in retail/food inflation trends, private label/fresh/refrigerated market shifts, and customer/consumer preferences—suggesting proactive vs. reactive strategy.

Potential for Near-Term Volatility: Management consistently emphasizes patience and proper sequencing of integration, which could translate to bumpy quarters before full synergy realization.

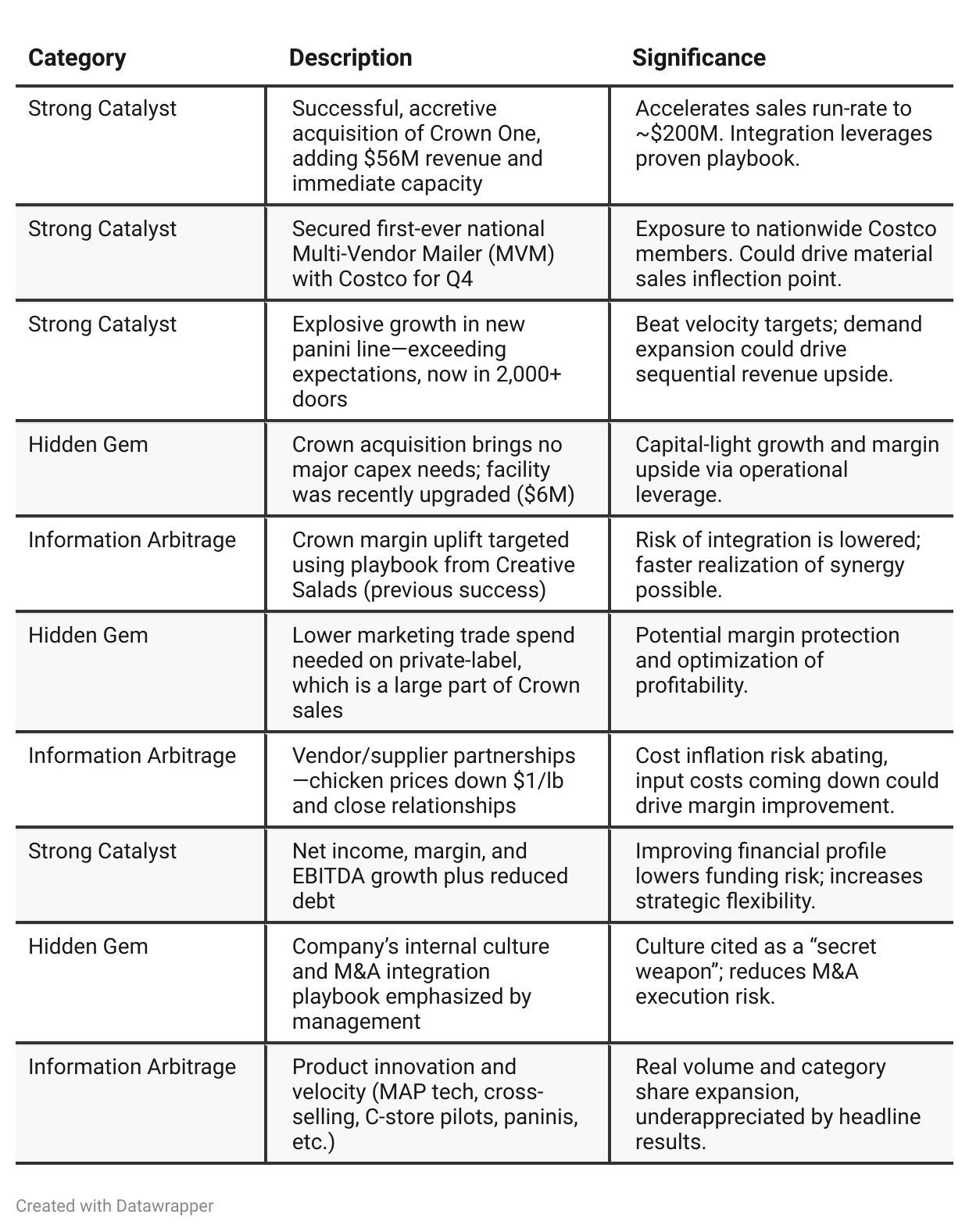

Positive Insights

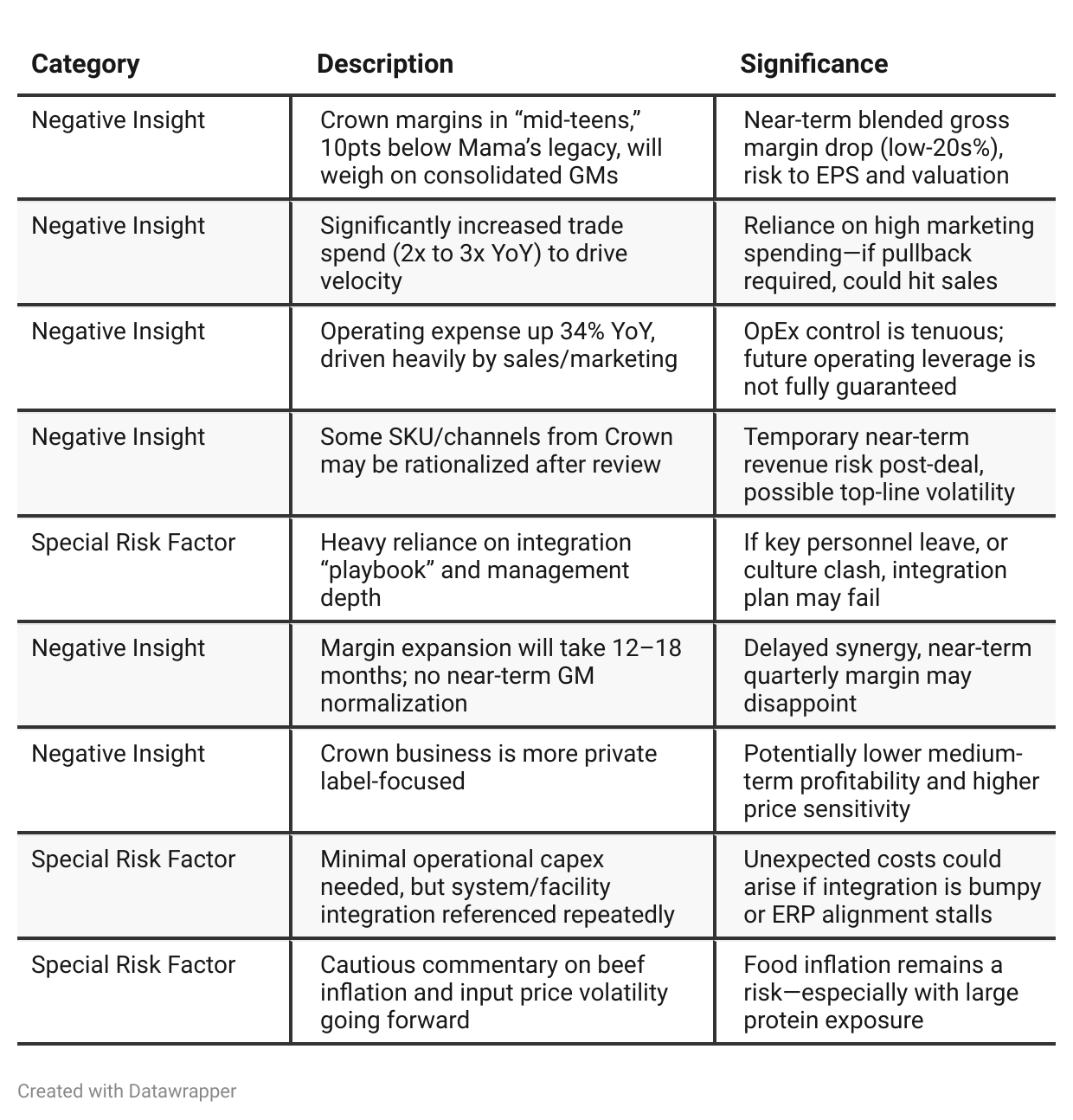

Negative Insights

Tariff Risk

Mention of Tariffs or U.S. Trade Policy:

No explicit mention of U.S. tariffs or trade policies in the transcript.

No discussion of exposure to international supply chain risk or trade actions impacting the business’s cost of goods, logistics, or market share.

No references to mitigating actions such as shifting suppliers, adjusting pricing due to tariffs, or discussing competitive disadvantages from tariffs.

Implication:

Based on the transcript alone, tariffs and trade policy do not currently present a disclosed risk to Mama’s Creations’ earnings, growth, or supply chain. No forward-looking statements or projections related to tariffs were included.

Investors should seek to verify this lack of risk by reviewing future 10-Q “Risk Factors” sections and monitoring for potential policy changes, especially given protein/food industry volatility.

Previous Earnings Call

Quarter-over-quarter comparison

Early FY26 (Q1): Mama’s Creations emerges from heavy operational/capex investments with robust core growth, margin expansion, and strong execution of the “four Cs” strategy. The company is disciplined about organic growth, selectively aggressive on high-ROI trade and new innovations, and maintains optionality for M&A, with a cautious, focused, internally strong footing (“ready for what’s next, but strictly disciplined”).Mid FY26 (Q2): MAMA pivots from purely organic momentum to a new phase as a scaled, consolidating platform, catalyzed by the acquisition of Crown One. Integration of this sizable, accretive asset becomes the new mission-critical task—margin compression and operational complexity acknowledged as necessary near-term costs for outsize future returns. Messaging turns more ambitious: from defending and building the base to capturing escape velocity, achieving synergistic integration, and leveraging the opportunity to double run-rate sales as a true national deli leader. The company retains confidence and humility, emphasizing the need to proceed at a measured pace and not rush integration, while leveraging culture and proven playbooks for long-term success.

Year-over-year comparison

Q2 2025: Mama’s Creations is in disciplined “build-and-fix” mode, emphasizing internal operational excellence, cost control, and margin restoration. The company is intentionally laying the foundation for future growth—with a continuous improvement mindset, testing innovation, opening new channels, and discussing M&A only as a longer-term goal.

Q2 2026: The narrative has evolved to “scale and integrate at pace,” driven by the leapfrog acquisition of Crown One. Mama’s has become a platform company. The story is now one of executing disciplined M&A, synergistic integration, rapid run-rate growth, channel cross-pollination, and ROI-leveraged marketing. Margin is sacrificed in the near-term for accelerated volume and future upside, but with an experienced team and track record mitigating integration risk.

Final Takeaway

Mama’s Creations (NASDAQ:MAMA) is in a growth and integration phase, leveraging the Crown One acquisition to drive scale and entry into new channels and customers. While strong product performance, run-rate revenue acceleration, and operational efficiencies provide solid upside potential, near-term margin dilution and integration execution risks remain. Successful realization of Crown synergies and sustainable gross margin expansion are the critical factors to watch. Verdict: HOLD with upside bias—the story is promising, but tangible post-integration progress (especially on margins and sales mix) is needed before a conviction Buy.