Lesaka Technologies, Inc. (NASDAQ: LSAK) – Q4 2025 Earnings

Lesaka Technologies, Inc. (NASDAQ: LSAK) – Q4 2025 Earnings

Earnings Release Date: Sep. 10, 2025

Stock Price: $4.58

Market Cap: $376.48 M million

Q4 2025 sales of $168.5 million vs $146.0 million in the prior year

Q4 2025 EPS of $($0.35) vs $($0.08) in the prior year

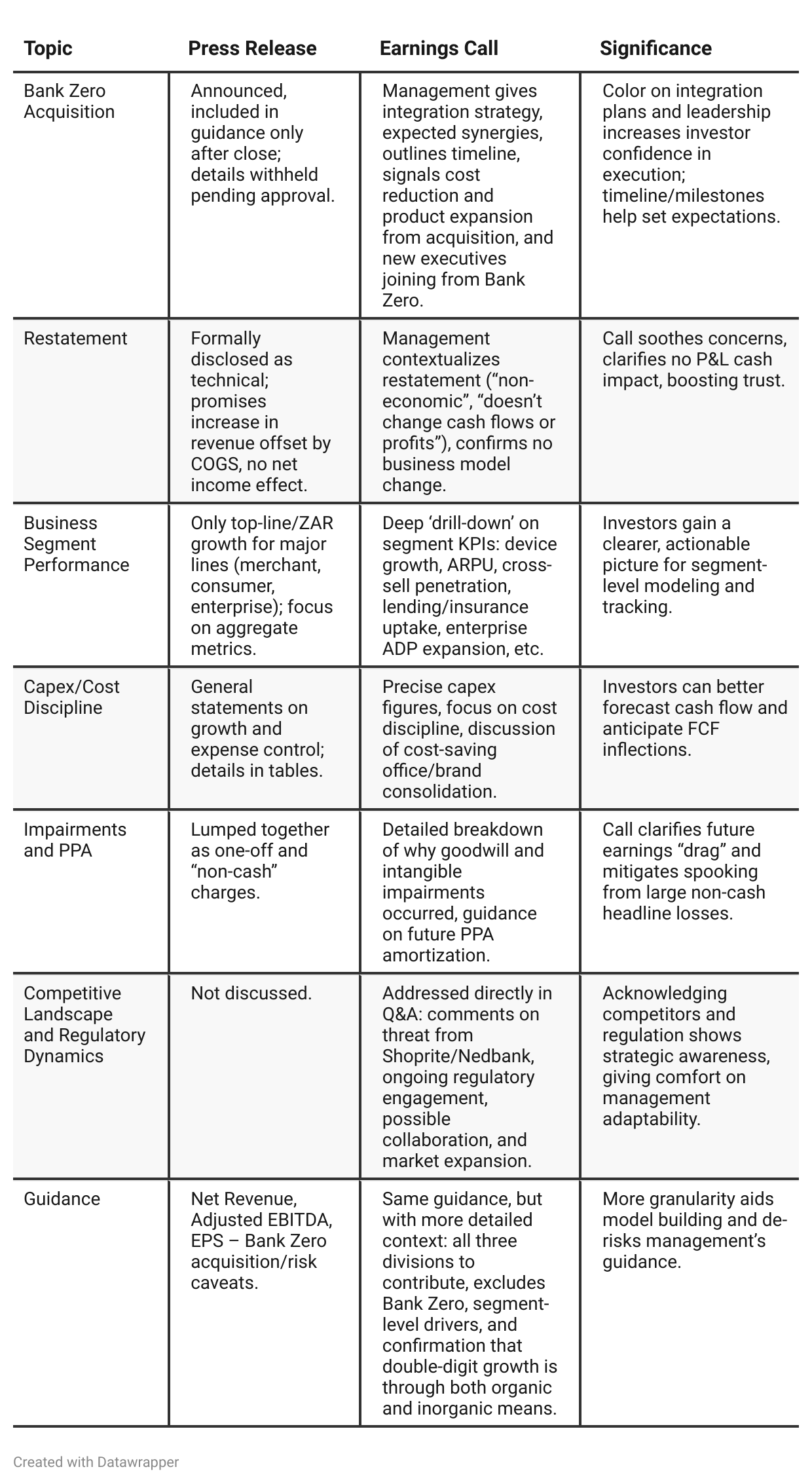

Press Release vs Call Transcript Comparison

Investor Communication: The call is used to “reset” investor focus on adjusted earnings over net loss, likely because of the high non-cash cost and outlier items.

Transparency and Confidence: Reiteration of hitting guidance “12 consecutive quarters” builds a track record of credibility.

Segment Strategy: Consumer business focus on cross-sell, digital engagement, grant beneficiary migration from failing SOE/post-bank.

Merchant Platform Integration: The platform consolidation is still in progress; significant further benefits yet to flow (costs up front, delayed rewards).

Enterprise as “Build Year”: Management positions Enterprise as a “build/consolidate” rather than “earnings” contributor for FY25, but fixates on future margin growth.

Macro/Exogenous Shocks: Management notes that while business is offset from direct macro stress, “unknown unknowns” (exogenous events, regulatory, etc.) are always a risk.

Balance Sheet Watch: While leverage is high, it is projected to drop post-Bank Zero, so there is a “window” in which the company is more vulnerable to shocks, but with an identified catalyst to fix.

Non-GAAP Dependence: Both documents stress Net Revenue and Adjusted EBITDA due to noise in GAAP as a result of mix changes, restatements, and non-recurring items.

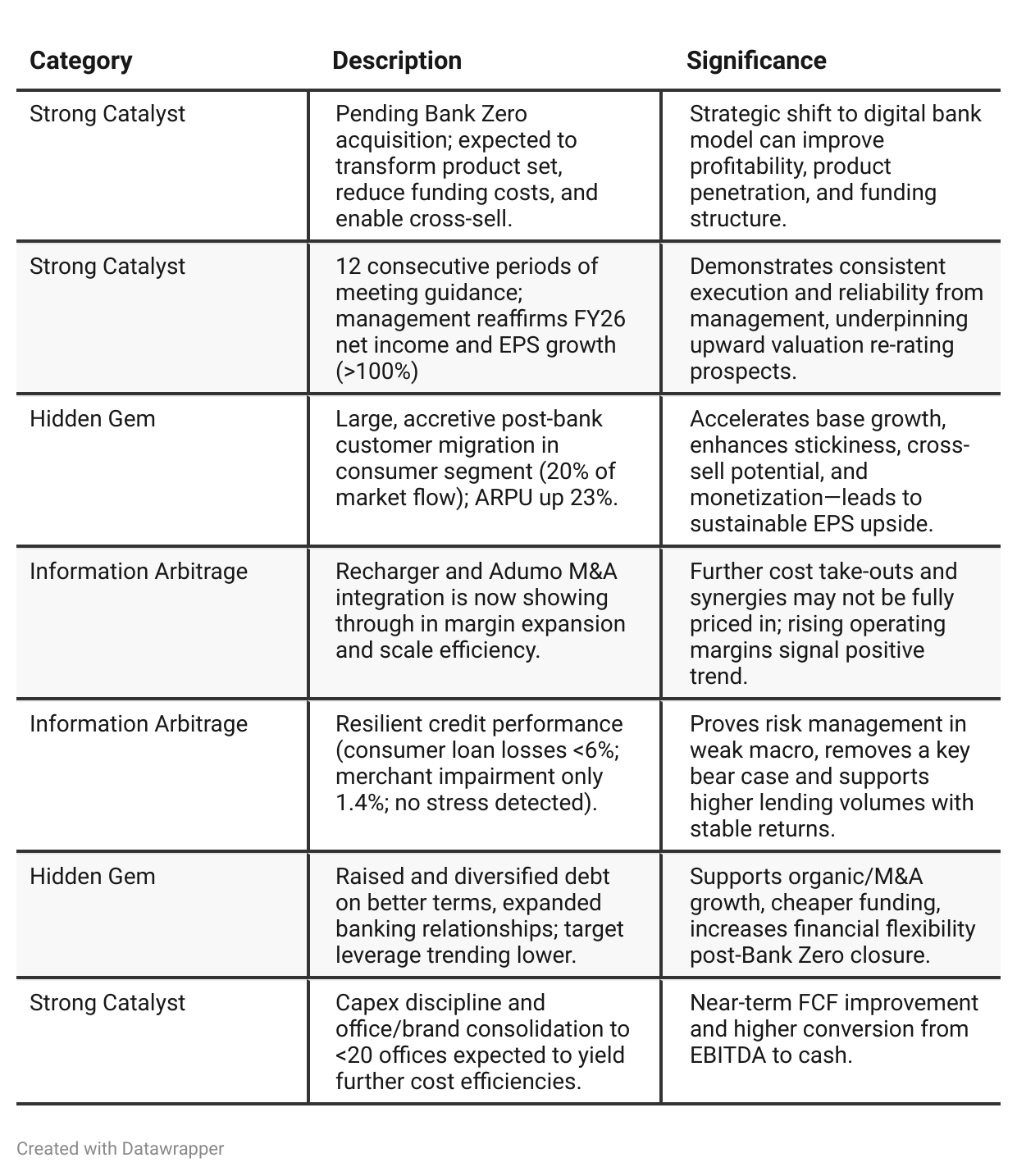

Positive Insights

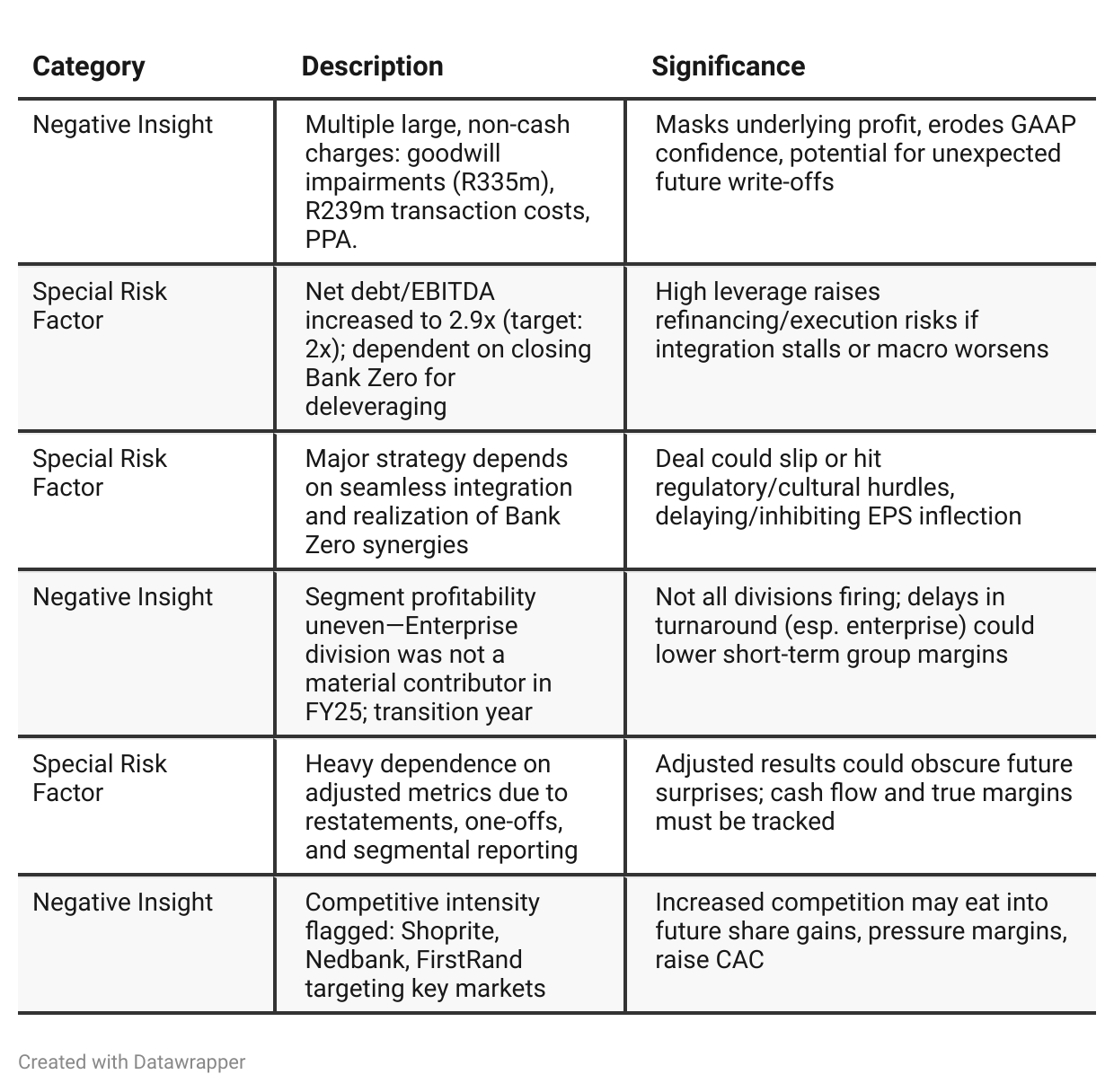

Negative Insights

Tariff Risk

Transcript Analysis for Tariff/Trade Policy Discussion:

No mention of U.S. tariffs, global trade policies, tariff mitigation, or related supply chain/market access risks.

Conclusion: Tariffs or trade policy are not currently material to Lesaka Technologies’ business model or financial risk set (based on this call).

Previous Earnings Call

Quarter-over-quarter comparison

Q3 2025: Lesaka Tech is in the thick of a transformation, completing major integrations (Adumo, Recharger), cleaning up legacy Enterprise activities, and shoring up its capital structure. Confidence is steadily building as KPIs improve, especially in the Consumer segment, while the narrative centers on building a coherent platform and proving its new model. Q3 demonstrates delivery on guidance, disciplined capital allocation, and early signs of scale benefits, but some segments still lag and require explaining.Q4 2025: The company’s story shifts markedly toward one of momentum and transformation realized. Management now speaks confidently about the platform’s scalability, accelerating cross-sell, and integration gains—with P&L discipline showing through higher EBITDA and margins. The Bank Zero acquisition is positioned as a game-changing catalyst, promising cost and funding advantages, broader product capability, and a step-change in addressable markets. The company meets guidance for the twelfth consecutive quarter, rebases KPIs to emphasize activity and value, and appears operationally and competitively ready for the next phase—characterized by leadership in digital financial services for underbanked segments. The tone is notably more optimistic, forward-looking, and grounded in evidence of execution as opposed to mere expectation.

Year-over-year comparison

In Q4 2024, Lasaka Technologies stood at the end of its multi-year turnaround—proudly reporting its first full-year profit in five years, executing on M&A, and preparing for a platform leap with the Adumo acquisition. The tone was careful but upbeat, management underscoring the hard work ahead and the learning curve of transformation from fragmented, loss-making operations to a cohesive fintech platform.

By Q4 2025, that platform has come together. The narrative has matured to one of integration, scale efficiency, and execution with confidence. Management is now focused on extracting value from a unified offering, launching digital banking (Bank Zero), and driving multi-segment growth. Risks are acknowledged—particularly integration and competition—but are framed as challenges to be managed rather than existential threats. The company now presents itself not only as a local disruptor, but as a category-defining fintech with the scale, product range, and leadership talent to capitalize on new market opportunities—poised for margin expansion and sustained profitable growth.

Final Takeaway

Lesaka Technologies is in a late-stage transformation phase, integrating acquisitions and building out a vertically integrated fintech platform targeting underserved markets in Southern Africa. The company is capitalizing on structural tailwinds in financial digitization, with strong momentum in consumer and merchant segments and significant future catalysts from Bank Zero, operational leverage, and market expansion. While positive execution is evident, headline GAAP volatility, high leverage, and reliance on ongoing integration are risks. Execution on the Bank Zero deal and further organic growth will be critical for future multiple rerating. Verdict: Buy, with high upside pending successful integration and regulatory sign-off.