LifeVantage Corporation (NASDAQ: LFVN) – Q4 2025 Earnings

LifeVantage Corporation (NASDAQ: LFVN) – Q4 2025 Earnings

Earnings Release Date: Sep. 04, 2025

Stock Price: $13.46

Market Cap: $165.9 million

Q4 2025 sales of $55.1 million vs $48.9 million in the prior year

Q4 2025 adjusted EPS of $0.17 vs $0.14 in the prior year

Full year sales of $228.5 million vs $200.2 million in the prior year

Full year adjusted EPS of $0.82 vs $0.59 in the prior year

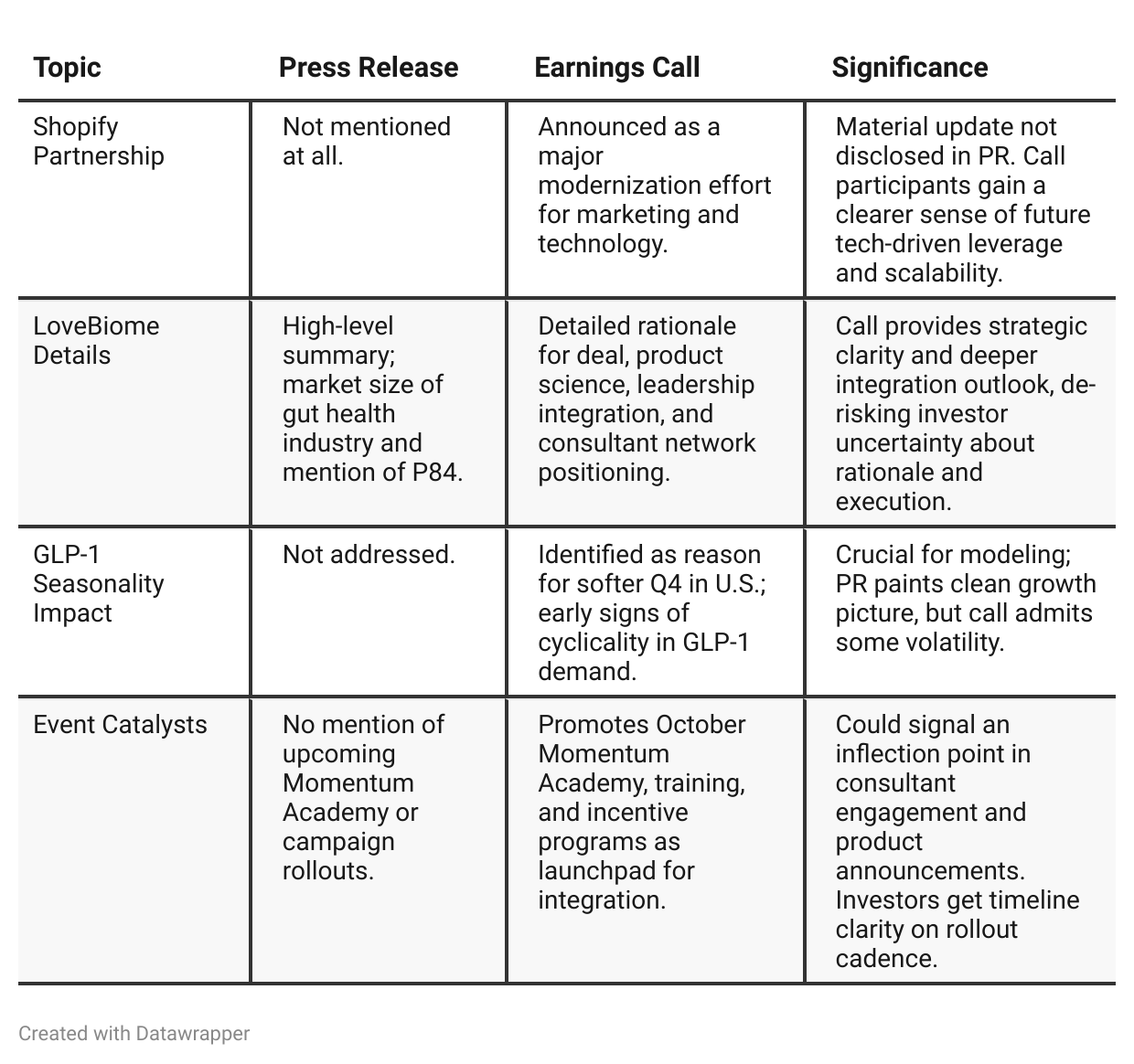

Press Release vs Call Transcript Comparison

While the press release focuses on headline financials and strong product themes, the earnings call introduces key strategic developments and caveats not captured in the PR—namely, seasonality-driven softness in GLP-1 sales, the unquantified but strategically important LoveBiome acquisition, and the Shopify tech modernization plan.

These differences matter because they clarify the drivers of FY26 guidance, uncover early indicators of product cyclicality, and highlight how LFVN plans to scale beyond its existing playbook. Investors who only read the press release would miss several operational shifts and forward-looking risks that are essential to making a well-informed decision.

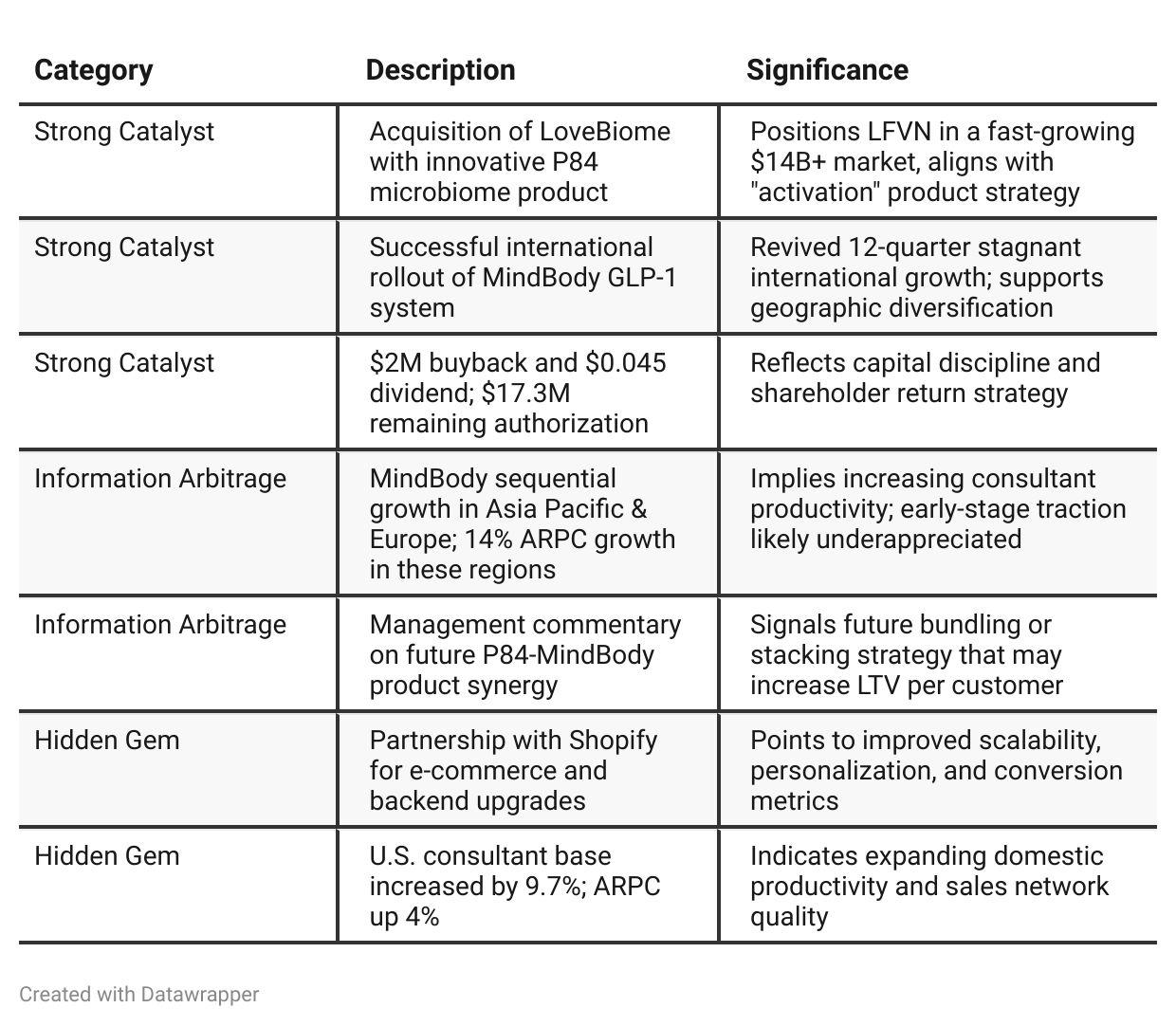

Positive Insights

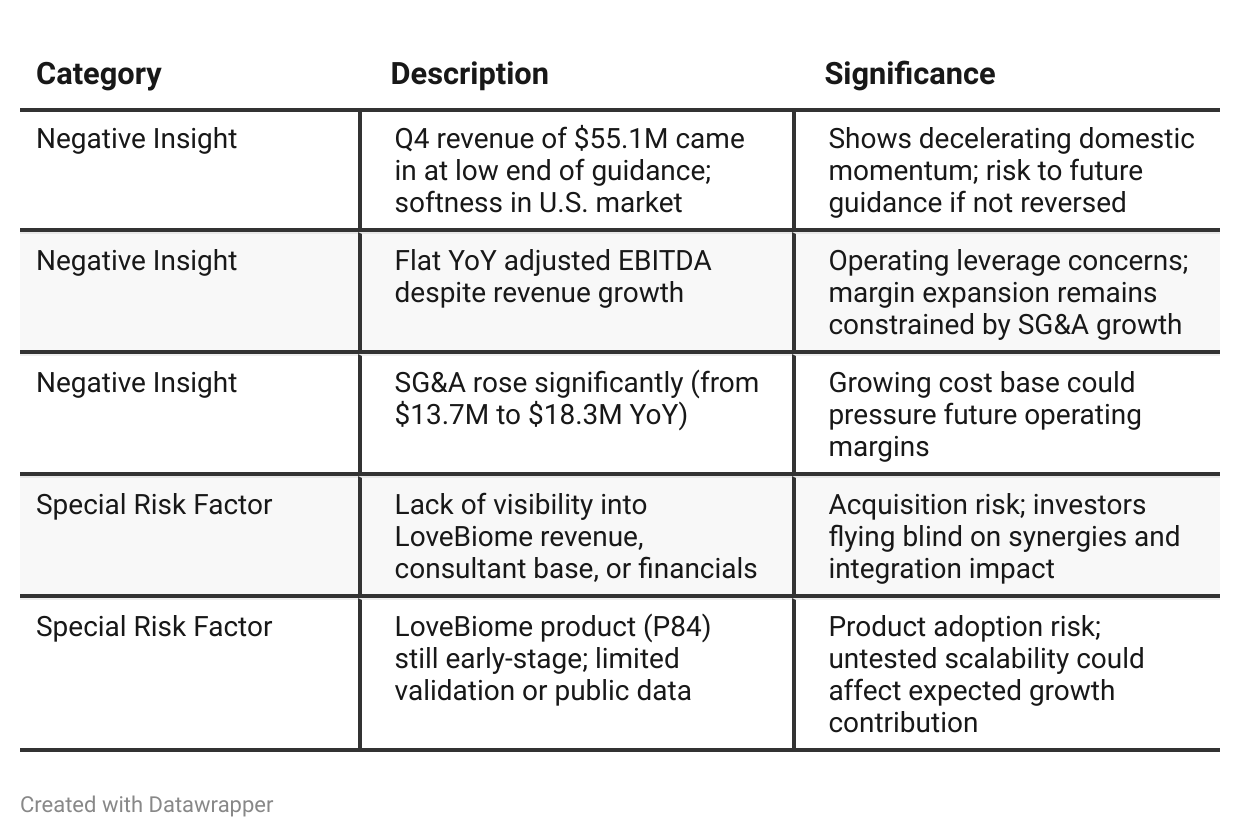

Negative Insights

Tariff Risk

No mention of U.S. tariffs or trade policy in the Q4 2025 call. There were no discussions of supply chain disruption, input costs, or international regulatory barriers tied to tariff regimes. Company’s international strategy (Japan, Europe, Australia, Thailand) seems to proceed without friction related to trade policy.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q3 and Q4 2025, LifeVantage shifted from post-launch stabilization of its MindBody product to forward-looking strategic execution.

The Q4 call marked a turning point with the acquisition of LoveBiome, signaling a broader wellness platform approach and a more aggressive push toward operational scale and market capture in both gut health and e-commerce infrastructure.

The transition underscores LFVN’s intent to become a more complete and tech-savvy wellness company rooted in activation science.Year-over-year comparison

In Q4 2024, LifeVantage was focused on navigating revenue headwinds and building a foundation for future growth through compensation redesigns, customer retention initiatives, and product development.

Fast forward to Q4 2025, that foundation has started to pay off. The company is now leaning into momentum driven by the successful launch of its MindBody GLP-1 system, an international turnaround, and a transformational acquisition (LoveBiome) that broadens its wellness footprint into microbiome health.

The narrative has shifted from cautious optimism to confident execution—with emphasis on innovation, consultant engagement, strategic M&A, and scalable infrastructure (Shopify)—positioning LifeVantage for its next phase of expansion.

Final Takeaway

LifeVantage is in a growth phase, pursuing both geographic expansion and strategic M&A to solidify its position in wellness-focused direct sales.

The MindBody system continues to drive momentum internationally, while the LoveBiome acquisition offers exposure to a fast-growing gut health market. However, domestic demand softness and acquisition opacity warrant near-term caution. Execution on integration, U.S. growth recovery, and Shopify modernization will be critical for delivering on the bullish long-term narrative.

Verdict: Hold, with moderate upside potential if integration and product synergy materialize.