LifeMD, Inc. (NASDAQ: LFMD) – Q2 2025 Earnings

LifeMD, Inc. (NASDAQ: LFMD) – Q2 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $12.35

Market Cap: $548.3 million

Q2 2025 sales of $62.2 million vs $50.7 million in the prior year

Q2 2025 EPS of ($0.06) vs ($0.19) in the prior year

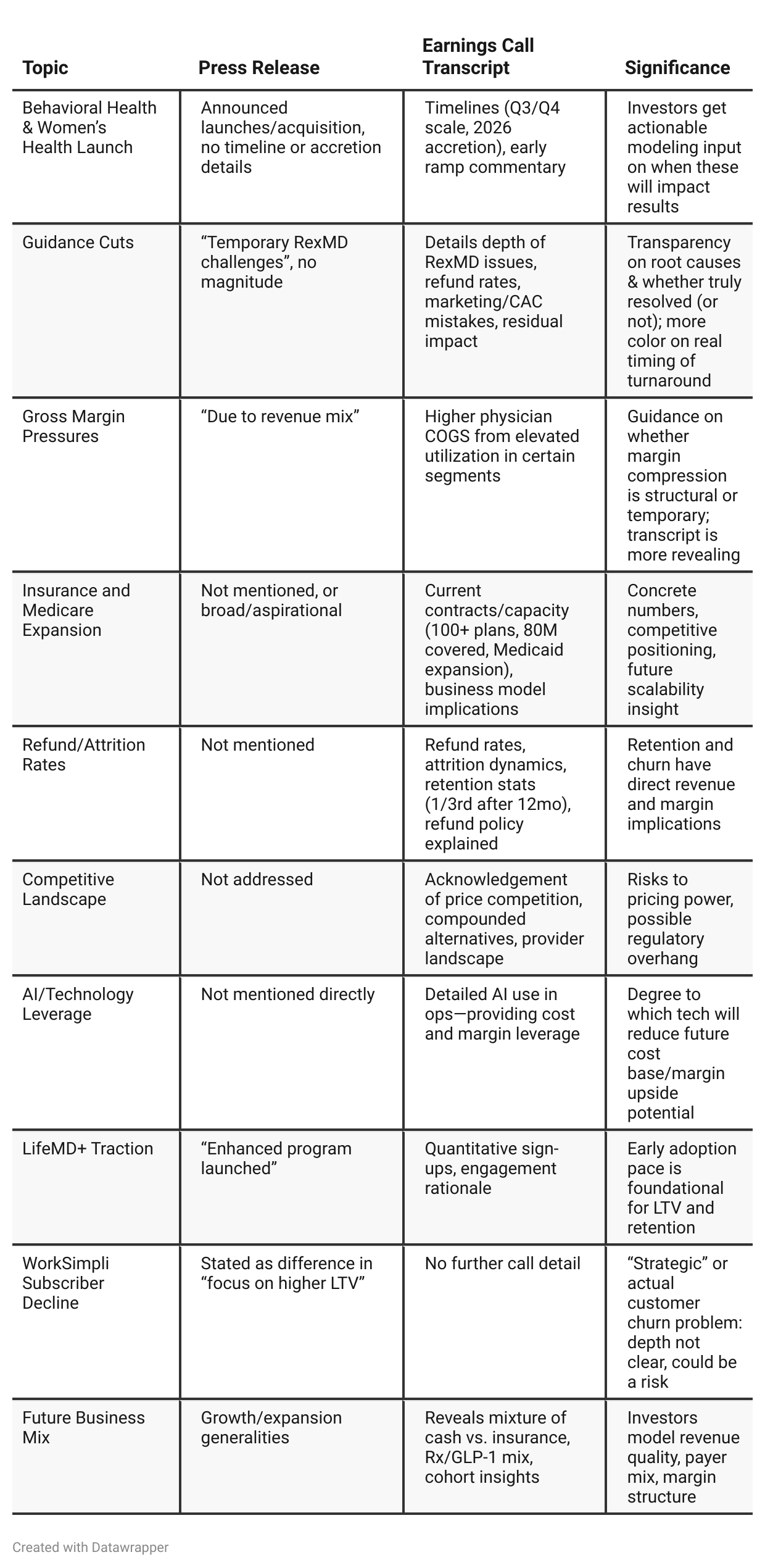

Press Release vs Call Transcript Comparison

Management Candor: The call reflects a much more candid admission of missteps (prioritization, marketing, refund issues) than the press release, which paints only positives.

Short vs. Long Term: The call transcript makes explicit that many growth levers (insurance, Medicare, behavioral/women’s health) are 2026+ events, not 2025, useful for valuation reference.

Execution Risk & Competition: The earnings call is frank about competitive intensity, retention/refund sensitivity, and management execution bandwidth as risk variables.

Balance Sheet: Both documents note debt-free status and strong cash, but only in the call is it clear this reflects both operational improvement and risk-aversion (e.g., repaying to avoid $1.1M future interest), a potentially defensive move.

Adjusted vs. GAAP Results: Both docs use non-GAAP figures, but the call is better for reconciling segment profitability and clarifying where margin expansion is achievable (e.g., AI, insurance scaling, business mix).

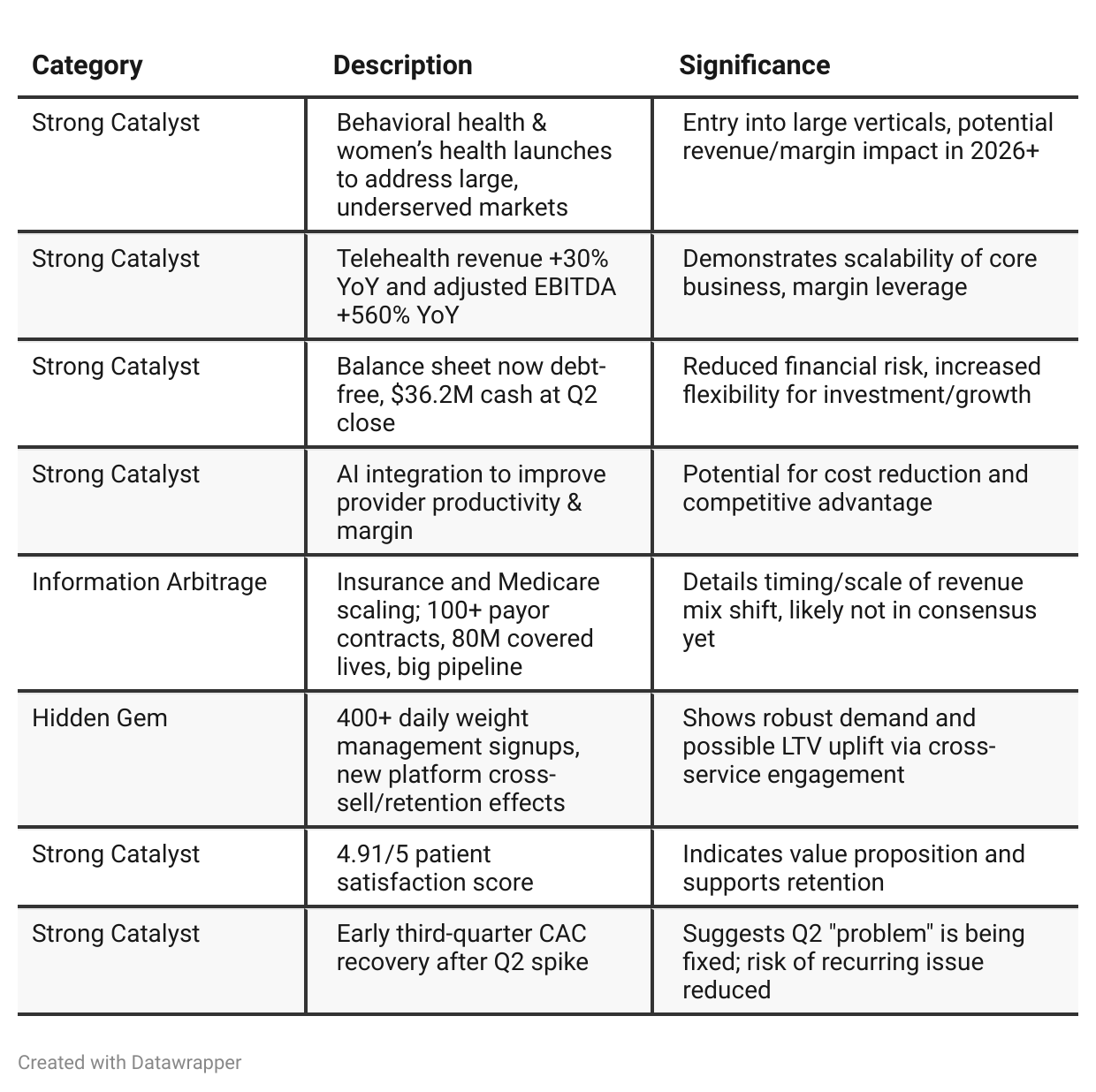

Positive Insights

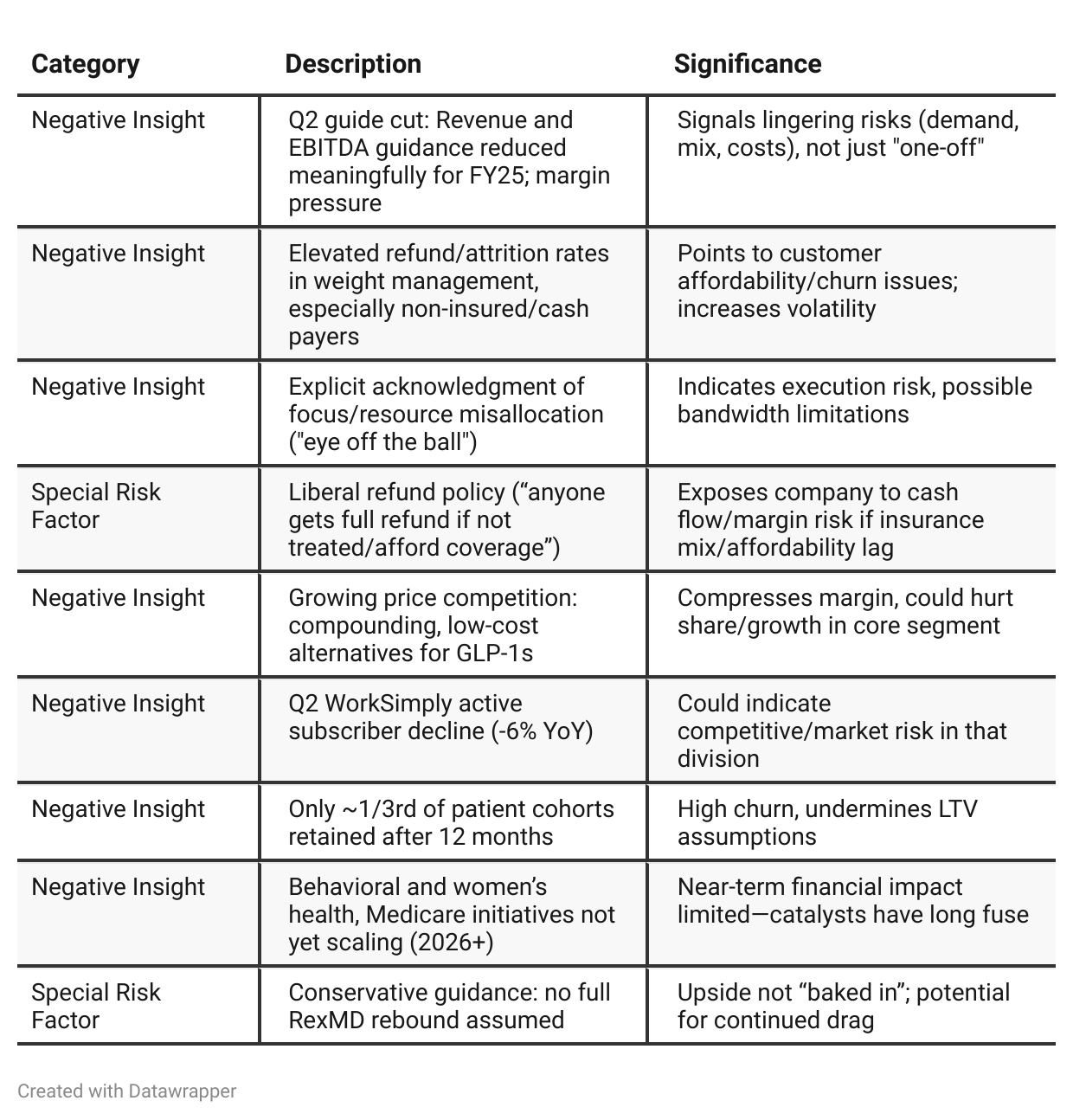

Negative Insights

Tariff Risk

There are no mentions of U.S. tariffs, international trade policy impacts, or related supply chain/pricing adjustments in the transcript. LifeMD’s business model (virtual care, pharmacy, digital services) is fundamentally domestic U.S.-focused and not directly exposed to tariff or trade policy risk. There is no indication in the call that management is facing, or taking action to mitigate, tariff impacts. No change in market share, innovation capability, or pricing is attributed to tariffs.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: LifeMD’s story was of an agile disruptor surging forward—hard numbers beat, every initiative firing, new segments (Medicare, women’s/behavioral health, HRT) coming online, and partnerships that would further the company’s edge. Management confidently raised guidance and focused investors on upside plays.Q2 2025: LifeMD’s narrative matured, showing the reality of rapid scaling in a competitive digital health market. Management confronted execution missteps, rising competition and margin pressures, and near-term churn/refund dynamics. The company shifted tone to pragmatic optimism—balancing long-term opportunity (insurance/Medicare, new verticals, AI-driven improvement) against growing pains. Guidance was cut to reflect discipline and realism. The “next act” is steadying the base and demonstrating that setbacks are fixable on the way to long-term, platform-driven growth.

Year-over-year comparison

Q2 2024: LifeMD’s story was one of accelerating growth and upside surprise: runaway success in telehealth, record weight management ramp, and early profits. The team was focused on scaling insurance and pharmacy, developing AI capability, growing retention, and shaping the most comprehensive care experience in the market. Challenges (like WorkSimply’s slump) were “transitory” and peripheral.

Q2 2025: The narrative shifts into a phase of maturity and pragmatism. While growth persists, it’s slower. Management is candid about executional setbacks, refund-driven margin pressures, and competitive realities. The focus now tilts toward operational rigor, margin restoration, and measured investments in insurance, Medicare, and diversified therapy options. Long-term opportunity in behavioral health and women’s health is intact, but payoff is delayed. The tone is less about conquering the telehealth world overnight—more about proving out resilient, profitable growth in a tough environment, with focus on execution and margin discipline until new product lines scale meaningfully in 2026.

Final Takeaway

LifeMD is in a transition and scaling phase, expanding its telehealth platform into high-value verticals (behavioral health, women’s health, Medicare) while maintaining robust core telehealth growth. However, Q2 revealed execution bandwidth risks, elevated churn and refunds in weight management, and persistent competitive pressure, forcing lower full-year revenue and profit guidance. While long-term growth levers (insurance, Medicare, AI-driven margin) are promising, most upside will not materialize until 2026. Execution on CAC controls, refund management, and scaling new programs will be critical.

Verdict: HOLD, with moderate potential upside if operational fixes gain traction and new segments ramp as promised.