Centrus Energy Corp. (NYSE: LEU) – Q2 2025 Earnings

Centrus Energy Corp. (NYSE: LEU) – Q2 2025 Earnings

Earnings Release Date: Aug. 05, 2025

Stock Price: $210.05

Market Cap: $3718.5 million

Q2 2025 sales of $154.5 million vs $189.0 million in the prior year

Q2 2025 EPS of $1.59 vs $1.89 in the prior year

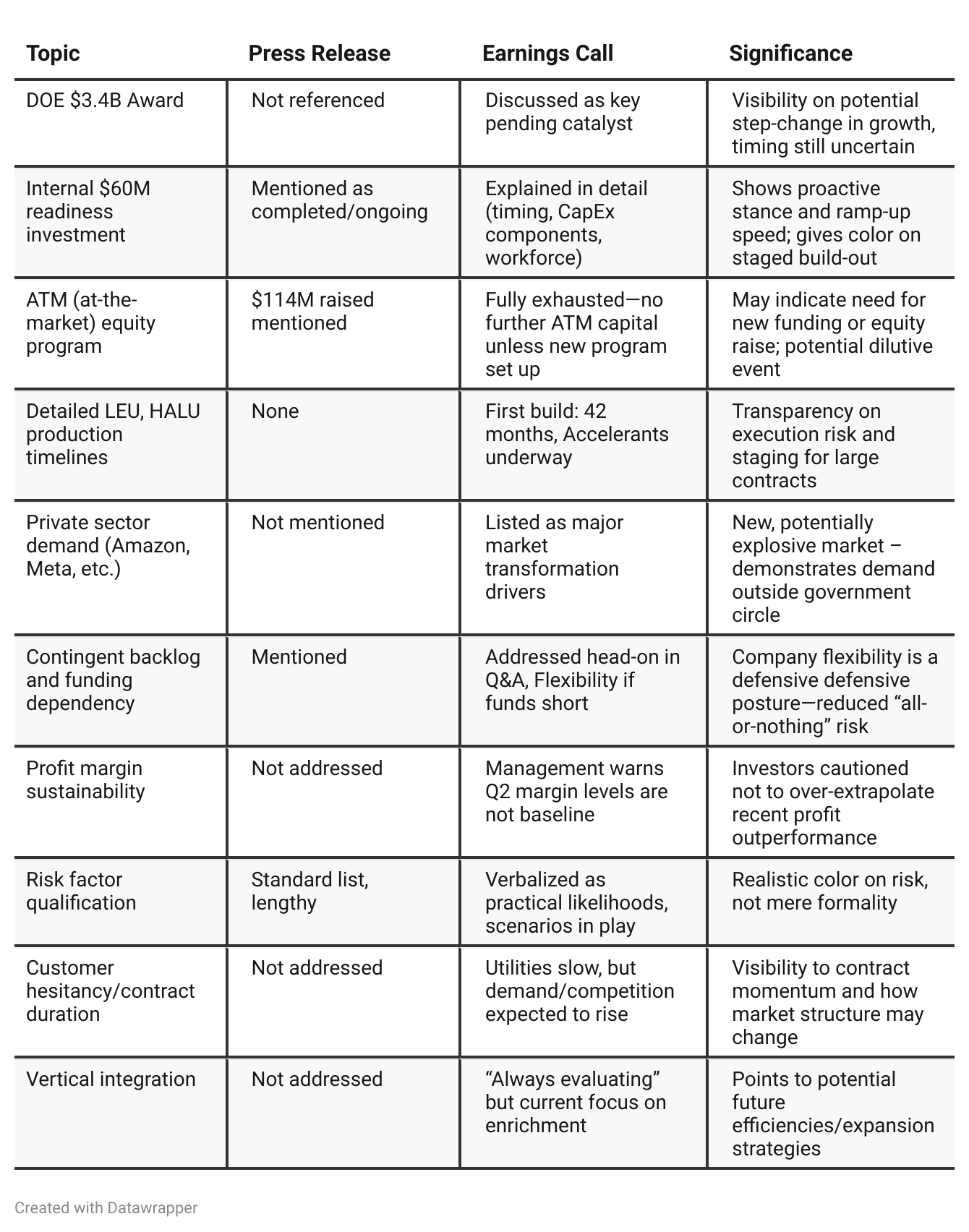

Press Release vs Call Transcript Comparison

Strategy: Management is open about not being able to fully compensate for the possible loss of Russian enrichment capacity, but is working to position Centrus as a key part of the future solution via public-private partnerships and rapid build-out readiness.

Flexible Operations: Company is actively considering whether to stage facility expansion, starting with available funds before (or instead of) winning full government awards—this flexibility is not clear in the press release.

Communication Tone: The call is much more candid—addressing volatility, contract timing, and the likelihood that Q2 margin/profitability is an “outlier,” not a new normal.

Private Market: Substantial new demand is expected from non-traditional buyers (e.g., AI, crypto, tech firms)—a potential upside that’s barely acknowledged in the press release.

Supply Chain Management: Details on manufacturing constraints, readiness initiatives, and staged capacity expansion planning are only voiced during the call, which is critical to assessing execution risk and time-to-revenue.

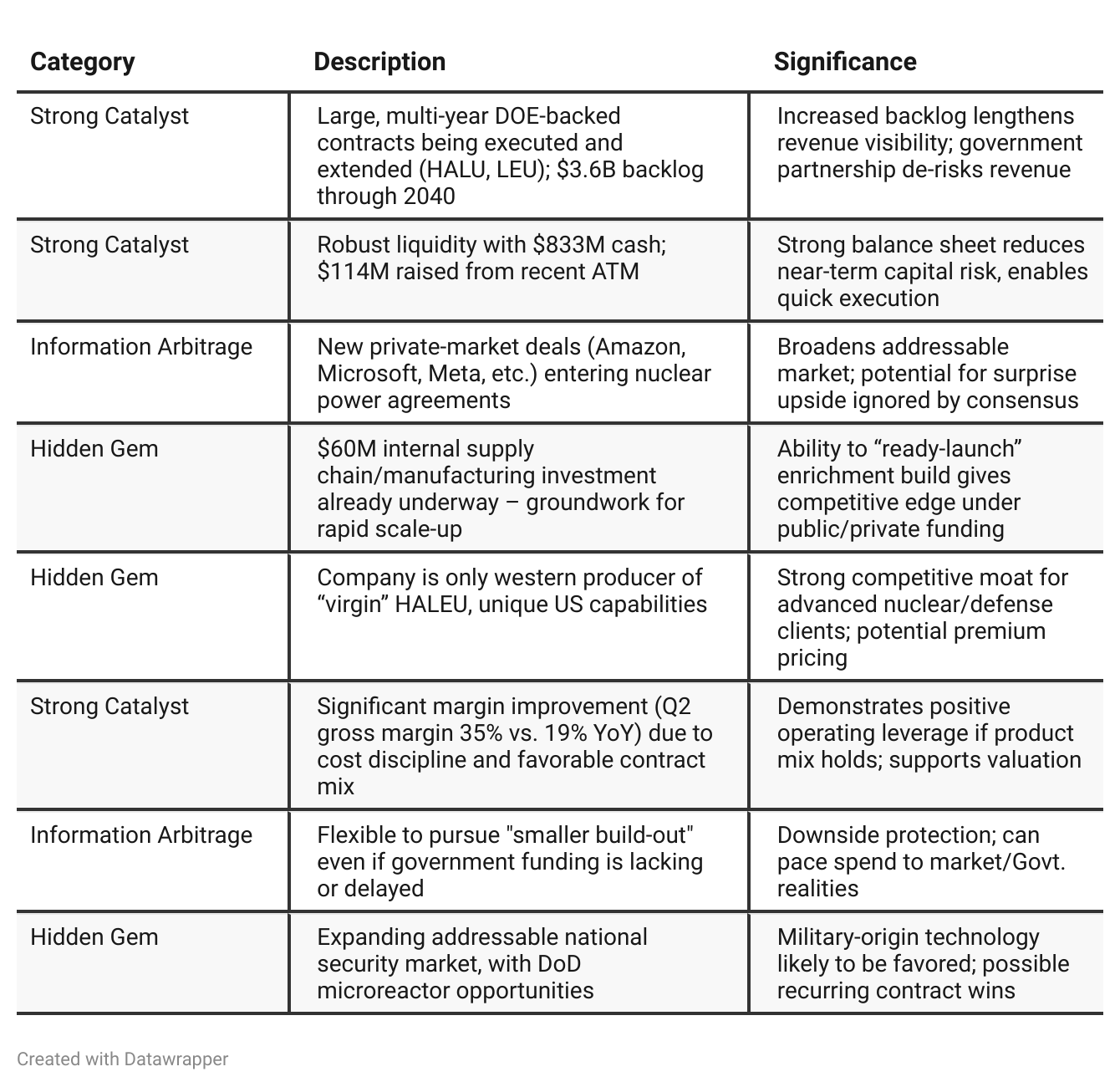

Positive Insights

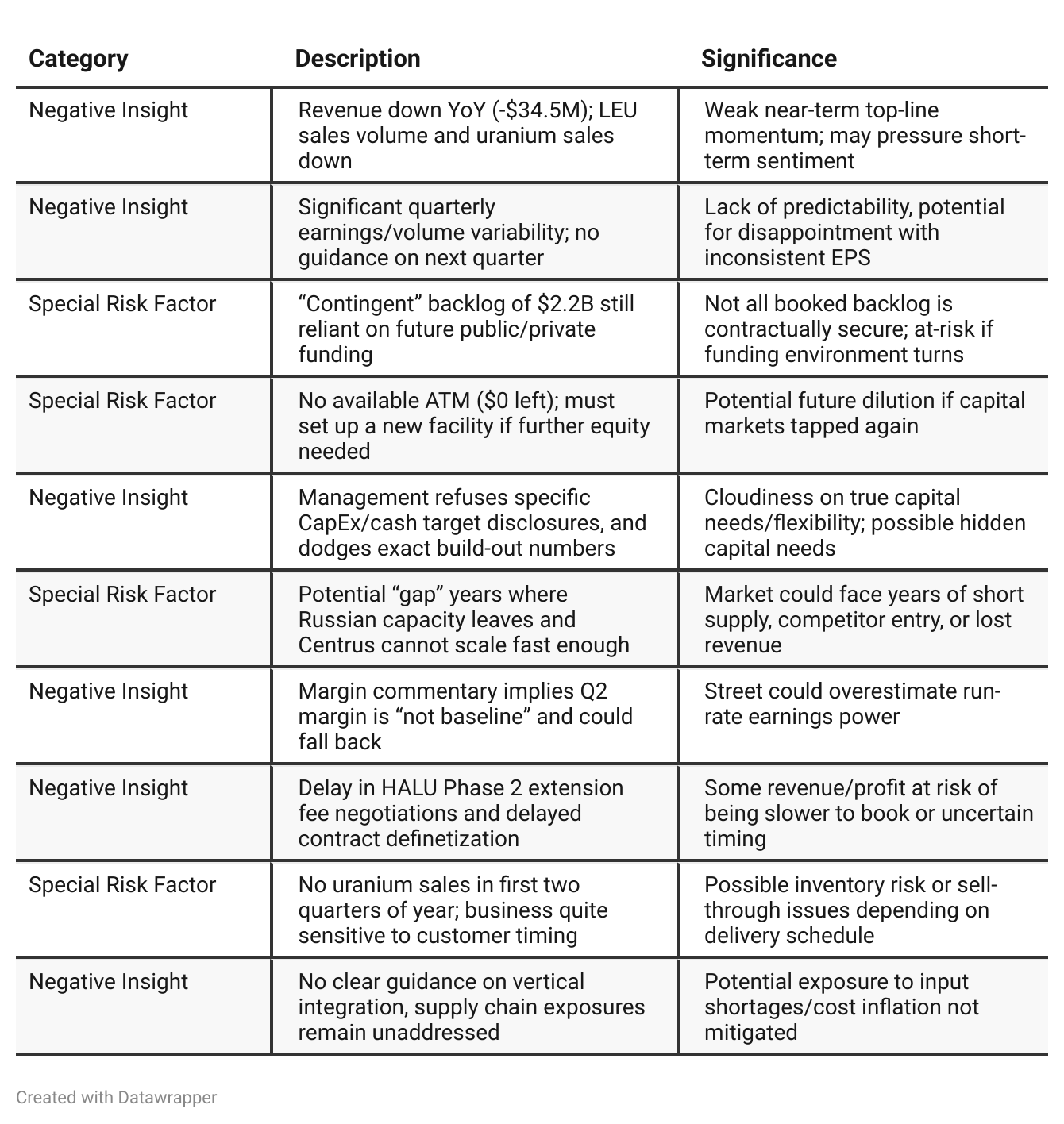

Negative Insights

Tariff Risk

Exposure: The company is indirectly exposed to U.S. trade policy changes, including tariffs, sanctions, and bans—especially relating to Russian uranium supply.

Mitigation: Centrus is proactively localizing its supply chain and manufacturing in the U.S., positioning itself as a secure, domestic provider—this reduces trade/tariff risk.

Competitive Impact: Tariffs or bans on foreign (esp. Russian) enrichment are likely to increase demand for Centrus’ services, potentially expanding market share.

Actions: No specific mention of contract renegotiations or price increases due to tariffs; the company is investing in U.S. infrastructure to ensure resilience against such risks.

Outlook: Management sees trade restrictions as a potential tailwind rather than a threat, but growth depends on ongoing government policy support and timely funding.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 Story: Centrus Energy entered 2025 with momentum—highlighting its unique, American, licensed nuclear enrichment tech, resolved short-term logistics/supply hiccups, robust political support, and a clear focus on securing federal funding and readiness for growth. Most optimism was tied to DOE award timing and execution on supply chain and production reliability.Q2 Update: By Q2, Centrus shifted from a strictly governmental/national security pitch to a broader “nuclear renaissance” theme, emphasizing pent-up private sector demand, tangible new commercial commitments, and big-picture US industrial policy tailwinds. Messaging suggests Centrus is not only waiting for government contracts but now in a broader, accelerating growth market, with the flexibility to pursue either full-scale or phased expansion—even as margin and funding volatility persist.

Year-over-year comparison

Q2 2024: Centrus Energy’s story was about building the foundation—securing government contracts, emphasizing its all-American credentials, de-risking the balance sheet, and obtaining DOE waivers to bridge the U.S.-Russia enrichment gap. The core message was process discipline and readiness, with future growth seen as tied to government allocation and public-private partnership.

Q2 2025: The company’s narrative has evolved from defensive and preparatory to bold and opportunistic. Now, Centris is not just “ready,” but at the heart of a U.S. and global nuclear resurgence, attracting non-traditional commercial demand and multiple layers of public/private investment. Messaging is more vibrant, celebrating operating wins, sector tailwinds, and a broadly expanding market. Financial discussions show improved margins and a willingness to pursue growth flexibly—as scale, demand, and capital (from any source) align.

Final Takeaway

Centrus Energy (LEU) is in an accelerating growth phase, leveraging unique domestic enrichment capabilities and a solid government and private sector backlog, with emerging opportunities from new, non-traditional buyers. While the company is positioned to benefit from U.S. and global nuclear policy tailwinds, investor returns hinge on execution speed, successful conversion of contingent backlog, and clarity on CapEx requirements. Risks remain around funding dependency, margin inconsistency, and the need for further capital if funding lags. Execution on government contracts, cost control, and swift capacity scale-up will be critical for upside realization. Verdict: Hold (with upward bias). Material awards, asset-light expansion, or clear capex visibility would justify a more bullish stance.