Leatt Corporation (OTCQB: LEAT) – Q2 2025 Earnings

Leatt Corporation (OTCQB: LEAT) – Q2 2025 Earnings

Earnings Release Date: Aug. 7, 2025

Stock Price: $9.93

Market Cap: $61.7 million

Q2 2025 sales of $16.18 million vs $10.08 million in the prior year

Q2 2025 EPS of $0.18 vs ($0.16) in the prior year

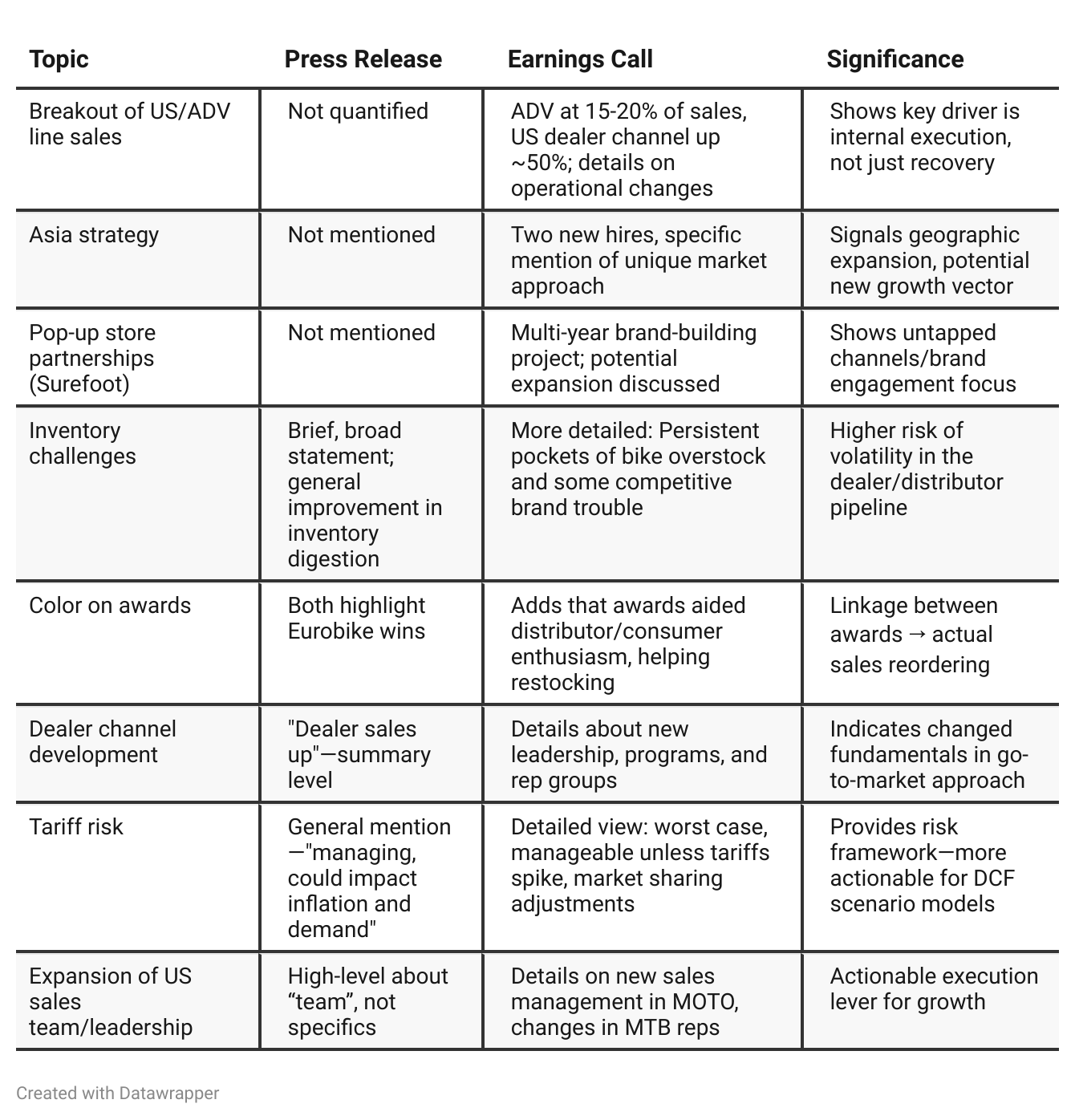

Press Release vs Call Transcript Comparison

Management Tone: The call provides much greater transparency and detail about management’s focus, new leadership hires, and strategic direction—very important for investor confidence and for identifying future execution risk (good and bad).

Macro Risks: Both documents mention tariffs and industry recovery, but the call transcript makes clear that management is actively monitoring and mitigating these, giving confidence that issues are in view but not yet acute.

Recognition Impact: Awards are more than just PR—they are cited as having tangible impact on distributor and consumer sentiment, supporting product restocking.

Sustainability of Growth: Call goes further to suggest recent growth is not driven by one-off events (tariffs/pre-buys); improvements in team, programs, and channels are the key—strengthening long-term investment case.

Operational Leverage: Gross margin expansion (+4 points YoY) in both documents, but call makes explicit that tariff management and improved sales mix are drivers.

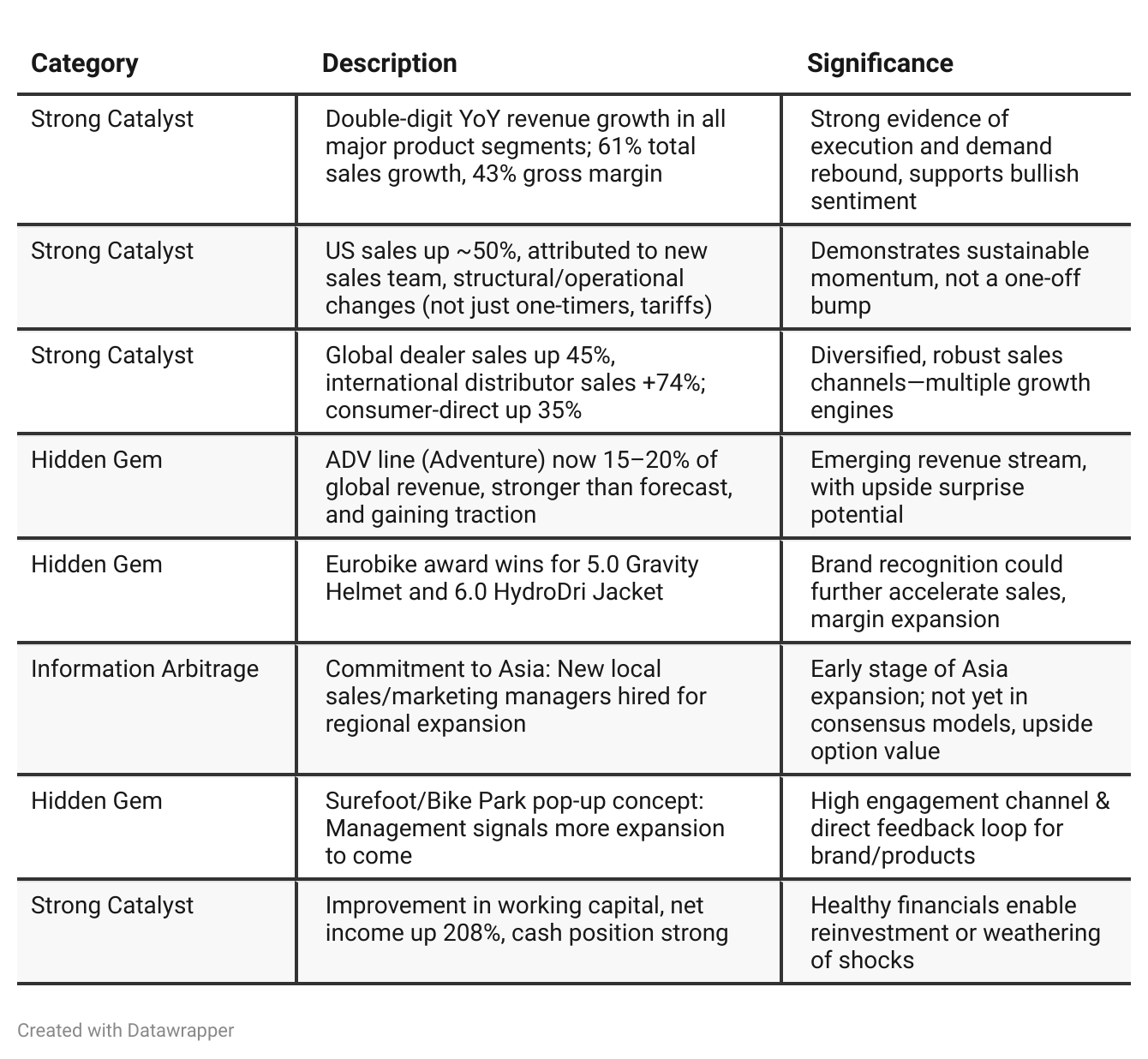

Positive Insights

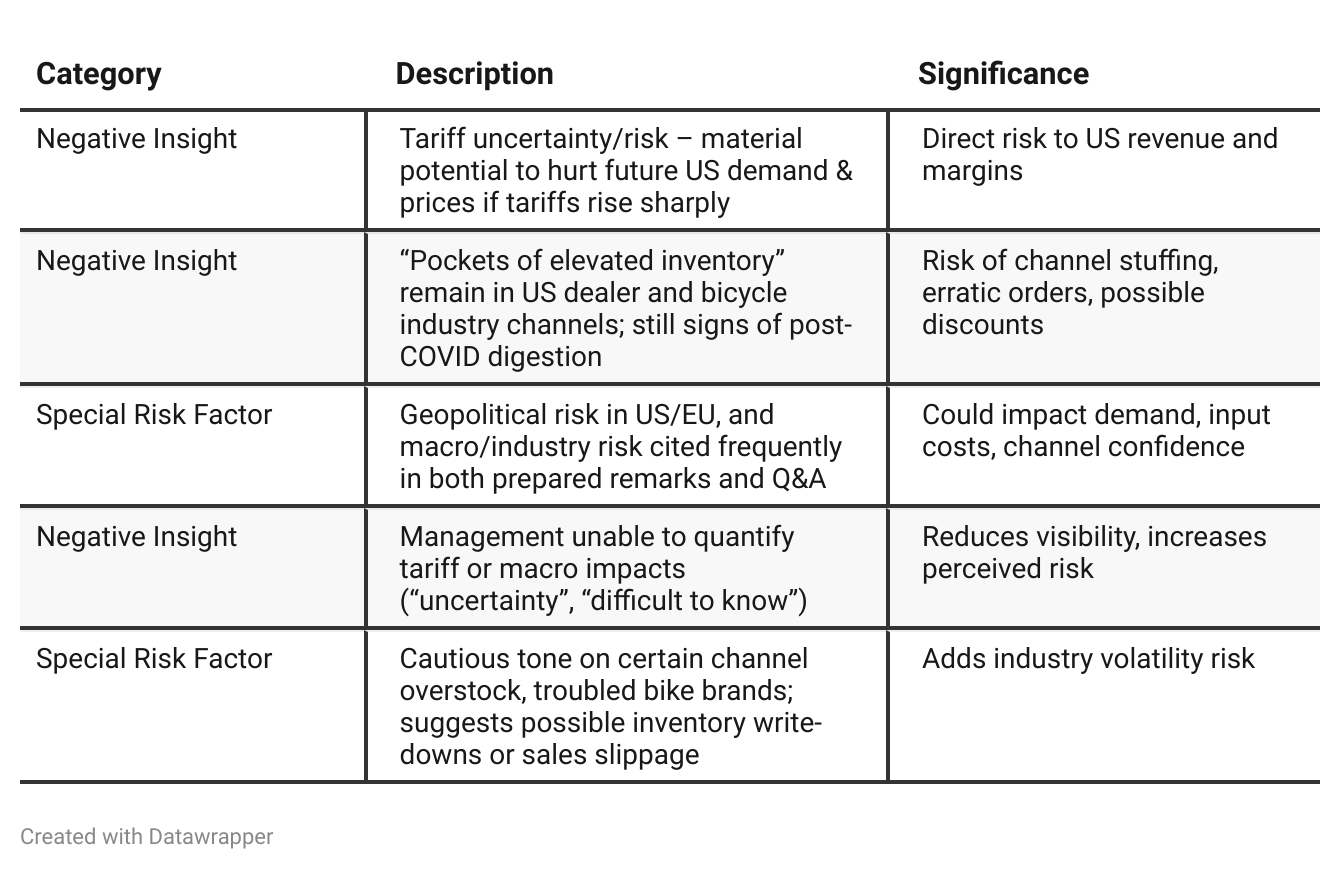

Negative Insights

Tariff Risk

Mentions & Analysis:

Management discussed tariffs as a real uncertainty with possible negative impact on US revenue and demand, mainly via potential inflation and cautiousness at the dealer/consumer level.

The CEO stated that everyone in the space (competitors included) is equally exposed. Hence, competitive position isn't uniquely threatened unless there's a large, outsized tariff move.

Concrete mitigations include: close supplier relationships, pass-through pricing (to a degree), and adjusting ordering patterns.

Management could not quantify the precise impact but feels it should be manageable barring extreme new tariffs.

No evidence of major supply chain restructuring (e.g., relocating manufacturing) at this time.

CEO is watchful, but the current scenario is not yet sharply negative.

Forward-looking comments: As long as tariffs stay at current levels or only modestly increase, Leatt expects to manage through, but high double-digit tariffs would present demand risk in the US.

Summary: Tariff risk is present, actively monitored, but not existential at current levels. Material escalation by policymakers would require close watch, and could shift the investment case quickly. Continue to track US/Asia trade signals in industry and macro news.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025: Leatt’s narrative centers around a strong return to growth after post-pandemic contraction, with double-digit gains across all categories—but also a strong recognition of persistent macro, inventory, and US channel risks. The company focuses on building a foundation for future expansion: investing in talent, refining sales structures (especially in the US), efficient inventory management, and developing new product lines like ADV. Optimism is measured; financial discipline and operational leverage are recurring themes.Q2 2025: The company’s story shifts to celebratory execution. The operational changes discussed in Q1 have directly translated to record sales and profitability, especially in the US, and momentum is now self-reinforcing across channels and geographies. Operational discipline is still present, but the risk tone has softened; new themes of brand/channel innovation (pop-up retail, Asia hires) surface, and management projects confident, sustained growth. The ADV line has become a material pillar. The overall narrative has evolved from cautious optimism (based on a foundation being set) to high conviction in a new phase of robust growth and competitive advantage, with risks acknowledged but perceived as increasingly under control.

Year-over-year comparison

In Q2 2024, Leatt’s narrative was about weathering a tough industry cycle: falling revenues, inventory clear-outs, unpredictable distributor ordering, and margin pressure from promotions. The messaging was about laying the groundwork for future recovery through inventory actions, pipeline building, and brand investment. Operations were defensive; risks were ever-present; optimism was a prospect, not a reality.

By Q2 2025, the story is one of validated execution and inflection-point growth. The investments in people, brand, and product have paid off in record revenue, profit, and margin expansion. The company speaks with conviction about global demand, brand strength, and competitive execution (“momentum” is the mantra). Channels are now aligned and firing, the ADV segment has become a material growth engine, and previously cited macro/inventory risks, while still mentioned, are downgraded in urgency. Strategic new bets—like Asia expansion and pop-up retail—move from conceptual to tangible, reinforcing Leatt as an innovation- and execution-driven brand in a state of renewed acceleration, rather than mere cyclical recovery.

Final Takeaway

Leatt Corporation is in a growth phase, fueled by operational changes, strong brand performance, and multiple product/channel innovations. Key drivers are robust US and international sales, strategic moves in ADV and Asia, and awards/brand recognition. While tariff and industry risks could disrupt the outlook, current financial health and management execution suggest continued upside. Watch delivery on Asia, channel normalization, and tariff policies. Verdict: Buy, while monitoring external volatility and tariff impacts.