Lakeland Industries, Inc. (NASDAQ: LAKE) – Q2 2026 Earnings

Lakeland Industries, Inc. (NASDAQ: LAKE) – Q2 2026 Earnings

Earnings Release Date: Sep. 9, 2025

Stock Price: $15.00

Market Cap: $142.9 million

Q2 2026 sales of $52.5 million vs $38.5 million in the prior year

Q2 2026 EPS of $0.08 vs ($0.19) in the prior year

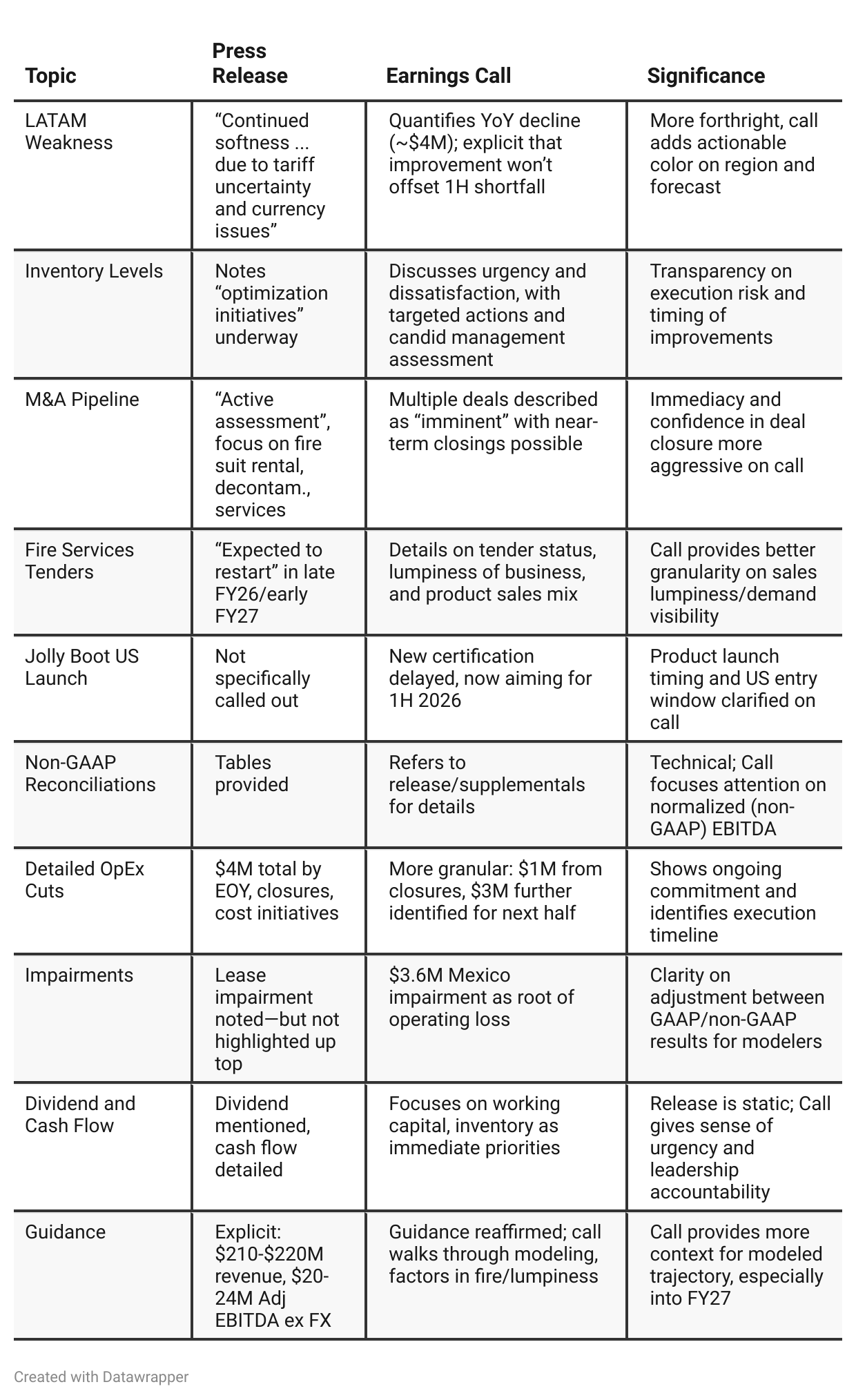

Press Release vs Call Transcript Comparison

Management Candor: The call expresses direct dissatisfaction with current inventory and margin levels, showing willingness to accept near-term pain for longer-term gain.

Imminent M&A: The level of confidence and immediacy about upcoming, service-related acquisitions is higher on the call—these could contribute to future recurring revenue streams, a strategic pivot.

Cash Flow Watch: The transition from negative operating cash flow to improvement in H2 is a key theme; any setbacks here would be a red flag.

Lumpy Revenue Profiles: Fire service tenders and large orders complicate quarterly forecasting; positive for upside, but riskier for misses.

Non-GAAP Is Key: Given large asset impairments and purchase accounting, investors should focus on Non-GAAP/adjusted metrics for normalized performance trends.

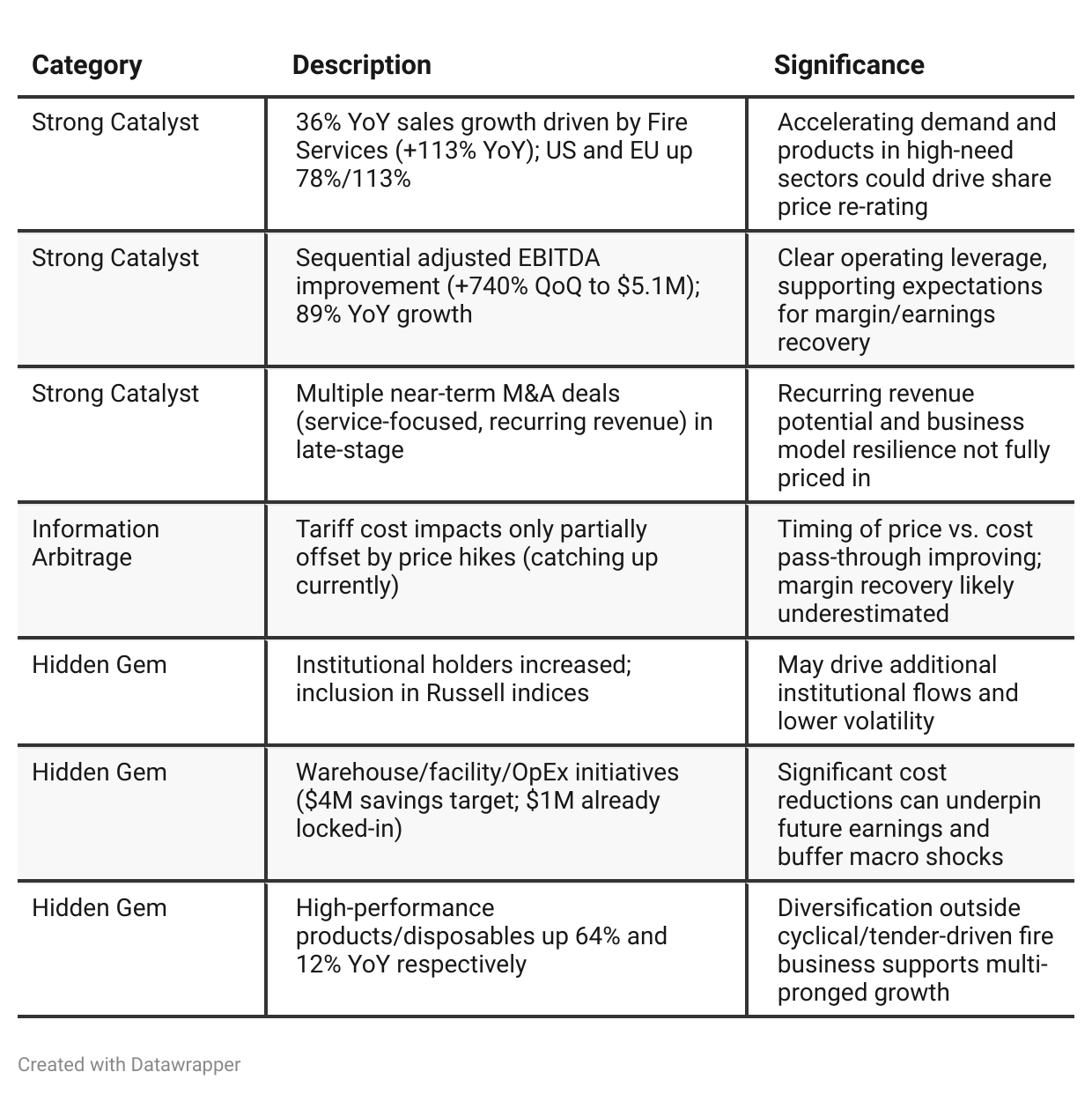

Positive Insights

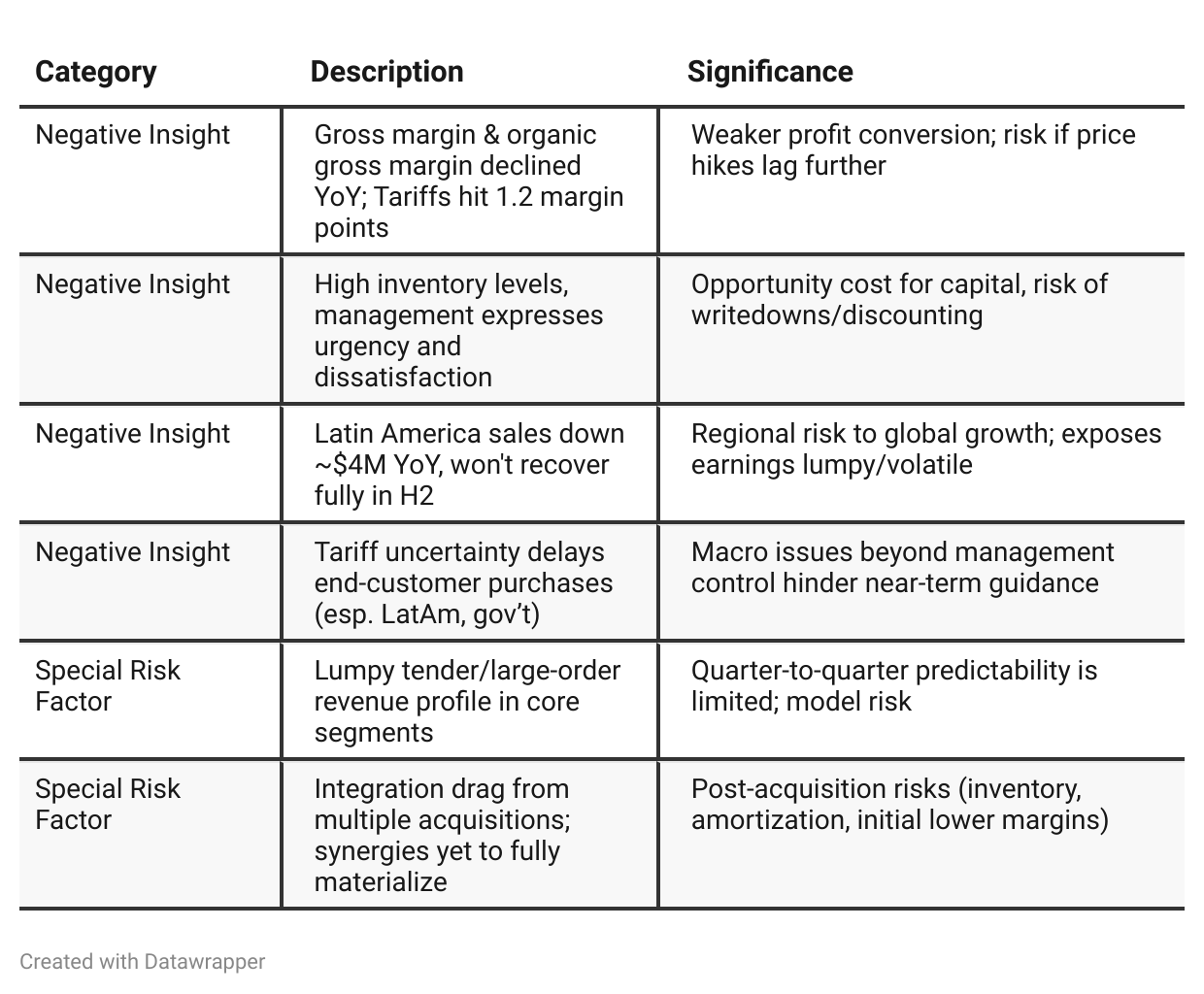

Negative Insights

Tariff Risk

Tariffs & Trade Policies:

Explicit Impact: Tariffs reduced gross margin by ~1.2 percentage points for the quarter; LATAM business especially impacted by delayed purchasing and currency volatility.

Mitigation Actions:

Management implementing price increases (starting to catch up with cost pressures).

Inventory pre-stocking in anticipation of tariff swings.

Productivity and OpEx initiatives ($4M targeted savings).

Supply chain diversification to increase resilience/flexibility.

“Tariff-free” sales promotions to boost short-cycle product sales.

Market Impact:

Customer demand timing lumpy (“let’s wait for tariff news”)—especially pronounced among government and LATAM buyers.

Short-term negative for cash flow and inventory, but seen as transitory by management (“light at the end of the tunnel”).

Forward-Looking Statements:

Management expects margin improvement as price/cost alignment stabilizes and global tariff “normalizes.”

Continued vigilance and diverse supply chains help buffer future shocks; expect further gross margin and operating income recovery in H2/FY27.

Summary: Tariffs are a material risk, but management is proactive; future margin expansion depends on successful offsetting of cost by pricing and operational savings. Execution is key.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2026: Lakeland’s leaders were on the defensive, explaining a quarter where operational disruptions (especially tariffs and acquisition integration) hit margins and profitability. The message revolved around the transitory nature of these setbacks, and the call was as much about educating the market on “why things went wrong” as on celebrating robust fire services top-line growth. Cost discipline and inventory management were promises, not yet progress; margin recovery was theoretical, pegged to accounting reversals and normalization.Q2 2026: The narrative shifts from defense to offense. With sequential improvement in margins and profits, management leans into growth—both organic and via M&A—while candidly acknowledging inventory and regional shortfalls. The tone is more transparent and even urgent regarding areas that need fixing, but the momentum message is clear. Tariffs evolve from being a disruptive force to a managed risk; integration is still ongoing, but the story now orbits future opportunities (institutional ownership, imminent smaller M&A, recurring services revenue). The company’s story is one of transition: from margin and cash flow repair toward a more sustainable, scalable, and higher-value growth model.

Year-over-year comparison

Q2 2025: Lakeland’s story was one of integration, transition, and managing disruption. The call was detail-heavy, excusing margin setbacks and setting the table for future margin and profitability improvement. The company was optimistic, but explanations outpaced execution, and management was focused on laying the foundations and hiring the right team.

Q2 2026: The narrative shifts to execution and operational discipline. Having absorbed integration setbacks and accounting noise, Lakeland pivots to driving results: record revenue, improving margins, and clear plans for cost control, margin repair, and working capital reduction. The company is no longer just promising improvement—it’s delivering sequential numbers and spelling out operational urgency, while continuing the long-term vision for service-driven, recurring-revenue fire business dominance. The message is less about weathering storms and more about building sustainable, scalable growth with a mature, results-driven operating tempo.

Final Takeaway

Lakeland Industries is in a growth and margin-recovery phase with strong top-line drivers, notably in fire services and international markets, and a robust M&A/services pipeline. While recent revenue and EBITDA growth are promising, key risks include elevated inventories, lumpy customer demand, and ongoing margin pressure from tariffs and acquisition integration. Execution on inventory normalization and margin improvement will be critical moving forward. Verdict: HOLD (positive bias); potential upside if management delivers on cost discipline and sustained demand, but investors should monitor working capital and margin trends closely.