Key Tronic Corporation (NASDAQ: KTCC) – Q4 2025 Earnings

Key Tronic Corporation (NASDAQ: KTCC) – Q4 2025 Earnings

Earnings Release Date: Aug. 27, 2025

Stock Price: $2.98

Market Cap: $32.1 million

Q4 2025 sales of $110.5 million vs $126.6 million in the prior year

Q4 2025 adjusted loss per share of ($0.35) vs ($0.06) in the prior year

Full year sales of $467.9 million vs $566.9 million is the prior year

Full year adjusted loss per share of ($0.47) vs ($0.02) in the prior year

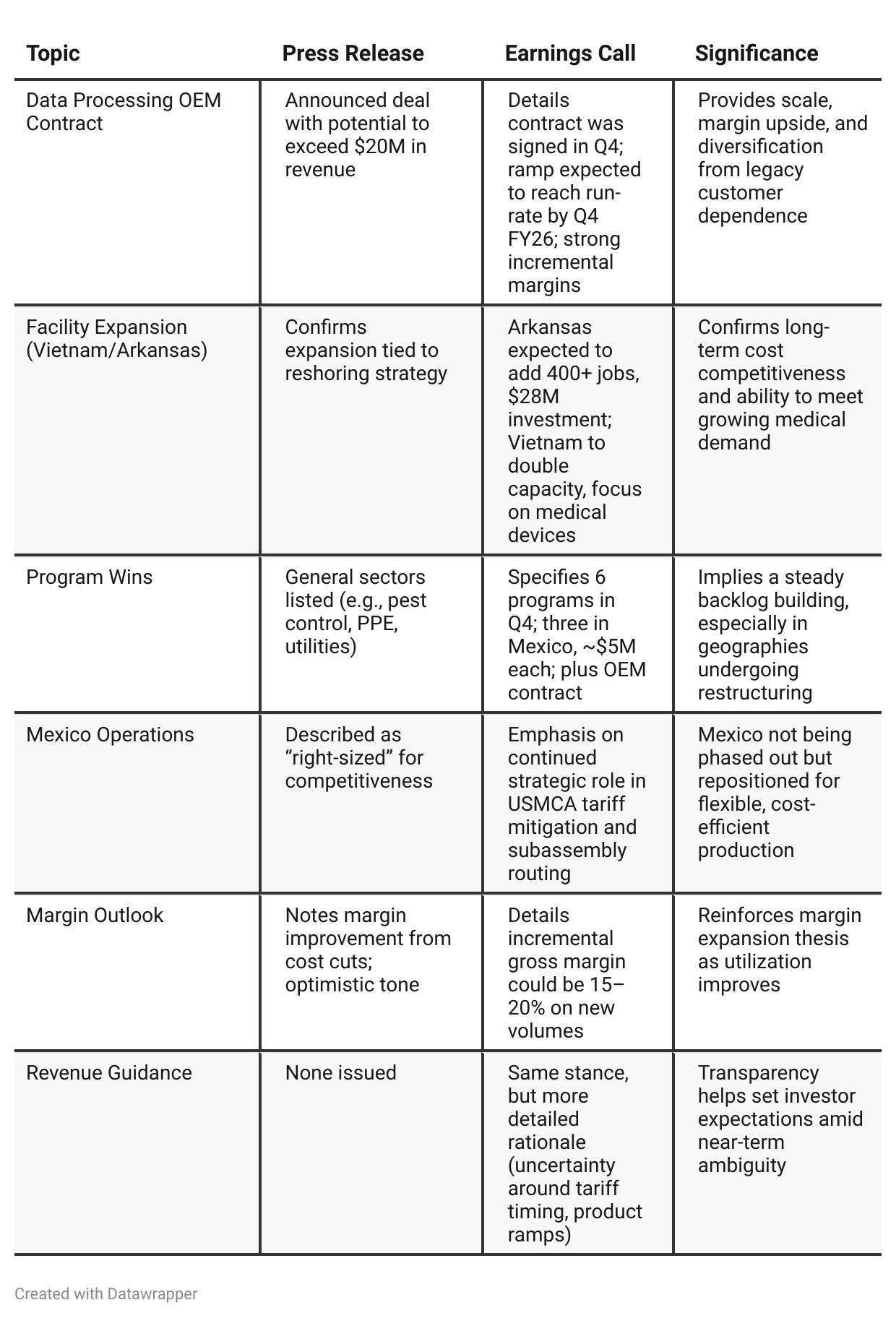

Press Release vs Call Transcript Comparison

The press release delivers a measured summary of results and outlines operational changes, but the earnings call adds critical context for investors. It highlights new contract wins with margin implications, expansion scale, and customer motivations behind reshoring interest. The call also provides a clearer view into execution challenges (e.g., tariff-driven delays) and risk management efforts like cost reductions and footprint optimization.

For investors, these differences are crucial: the press release alone might signal continued weakness, while the call reveals underappreciated levers for a turnaround—particularly as tariff uncertainties stabilize and new programs begin to ramp.

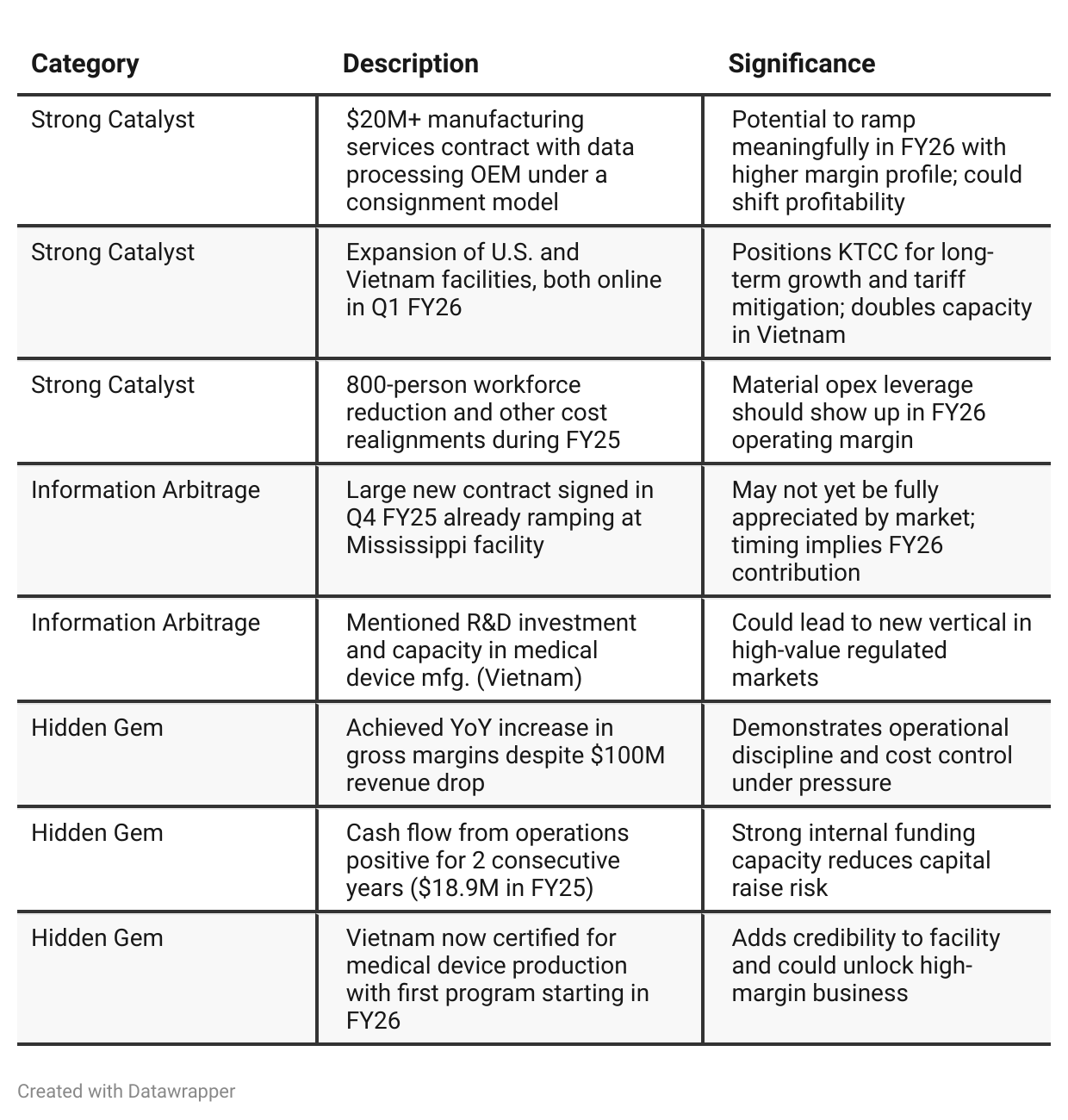

Positive Insights

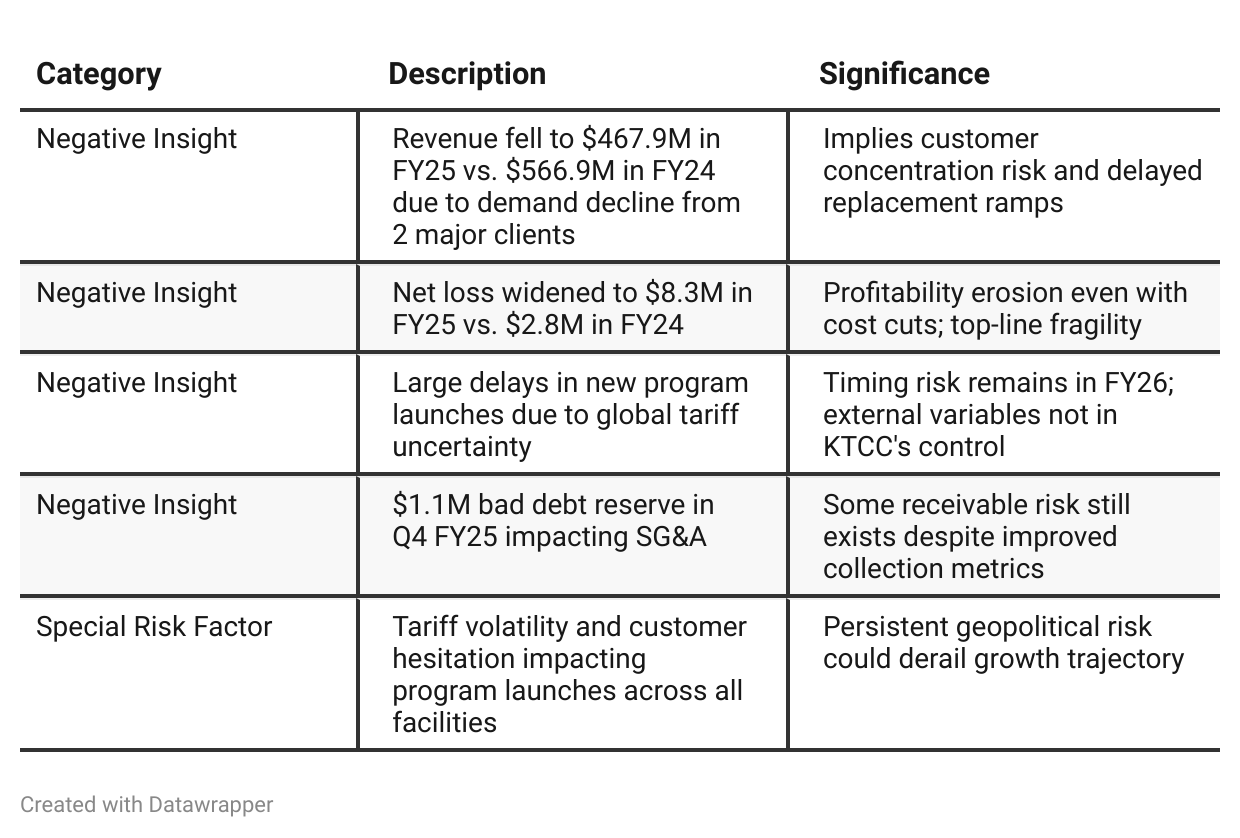

Negative Insights

Tariff Risk

Tariffs were cited multiple times as a key cause of program launch delays and customer hesitation, especially in FY25. The company:

Took steps to mitigate risks by expanding U.S. and Vietnam production

Rebalanced global manufacturing to diversify away from China

Highlighted Vietnam as a low-cost China alternative and Mexico as a USMCA tariff shield

Stated customer demand is shifting in favor of nearshoring and dual sourcing due to tariff volatility

Forward-Looking Statements: Management expects the new footprint will enable them to better absorb future tariff shocks. No numerical sensitivity or scenario analysis was provided, but mitigation is a core strategic driver.

Previous Earnings Call

Quarter-over-quarter comparison

Between Q3 and Q4 FY2025, Key Tronic’s narrative evolved from tactical survival to strategic re-positioning. In Q3, the company was still weathering the brunt of lost revenue and struggling with tariff-induced delays, focusing on operational cost cuts and efficiency gains to stabilize performance.

By Q4, the tone shifted: KTCC framed FY2025 as a transition year, with major structural moves (facility expansion, automation, headcount reduction) setting the stage for a ramp in FY2026. The announcement of a high-margin, consignment-style $20M OEM contract and a medical device manufacturing initiative in Vietnam suggests that the groundwork is yielding tangible growth vectors.

The leadership's messaging also signaled that their cost base and capacity expansions now position them to reclaim margin and scale—particularly as customers resume decision-making amid ongoing geopolitical uncertainty.Year-over-year comparison

In Q4 2024, Key Tronic was navigating short-term disruptions (cyberattack, winter storms) but appeared poised for a rebound, buoyed by cost cuts, margin recovery, and an expanding customer base. Management framed these disruptions as temporary setbacks with recoverable revenue and emphasized operational momentum and margin expansion heading into FY25.

By Q4 2025, however, the narrative shifted toward deeper structural challenges: two legacy customers pulled back significantly, global tariff volatility stalled new launches, and margins compressed despite continued cost reductions. The tone was more cautious, with management focused on stabilizing operations, rebalancing capacity across geographies, and investing in long-term footprint expansion (Arkansas and Vietnam). Strategic optimism remains, but it is tempered by operational losses, muted revenue, and deferred program ramps.

The story evolved from a short-term rebound thesis (Q4 2024) to a long-term repositioning effort (Q4 2025) as unexpected macroeconomic shifts—especially tariffs—derailed near-term recovery.

Final Takeaway

Key Tronic is in a transition phase, absorbing the impact of major customer losses and tariff-related delays while repositioning itself through aggressive cost cuts, U.S./Vietnam expansions, and a meaningful new contract win.

While management is clearly building capacity for recovery, near-term execution and macro volatility remain key swing factors.

Verdict: Hold, with potential upside if new programs ramp on schedule and margin recovery materializes in FY26.