Karat Packaging Inc. (NASDAQ: KRT) – Q3 2025 Earnings

Karat Packaging Inc. (NASDAQ: KRT) – Q3 2025 Earnings

Earnings Release Date: Nov. 06, 2025

Stock Price: $25.36

Market Cap: $508.7 million

Q3 2025 sales of $124.5 million vs $112.8 million in the prior year

Q3 2025 EPS of $0.36 vs $0.45 in the prior year

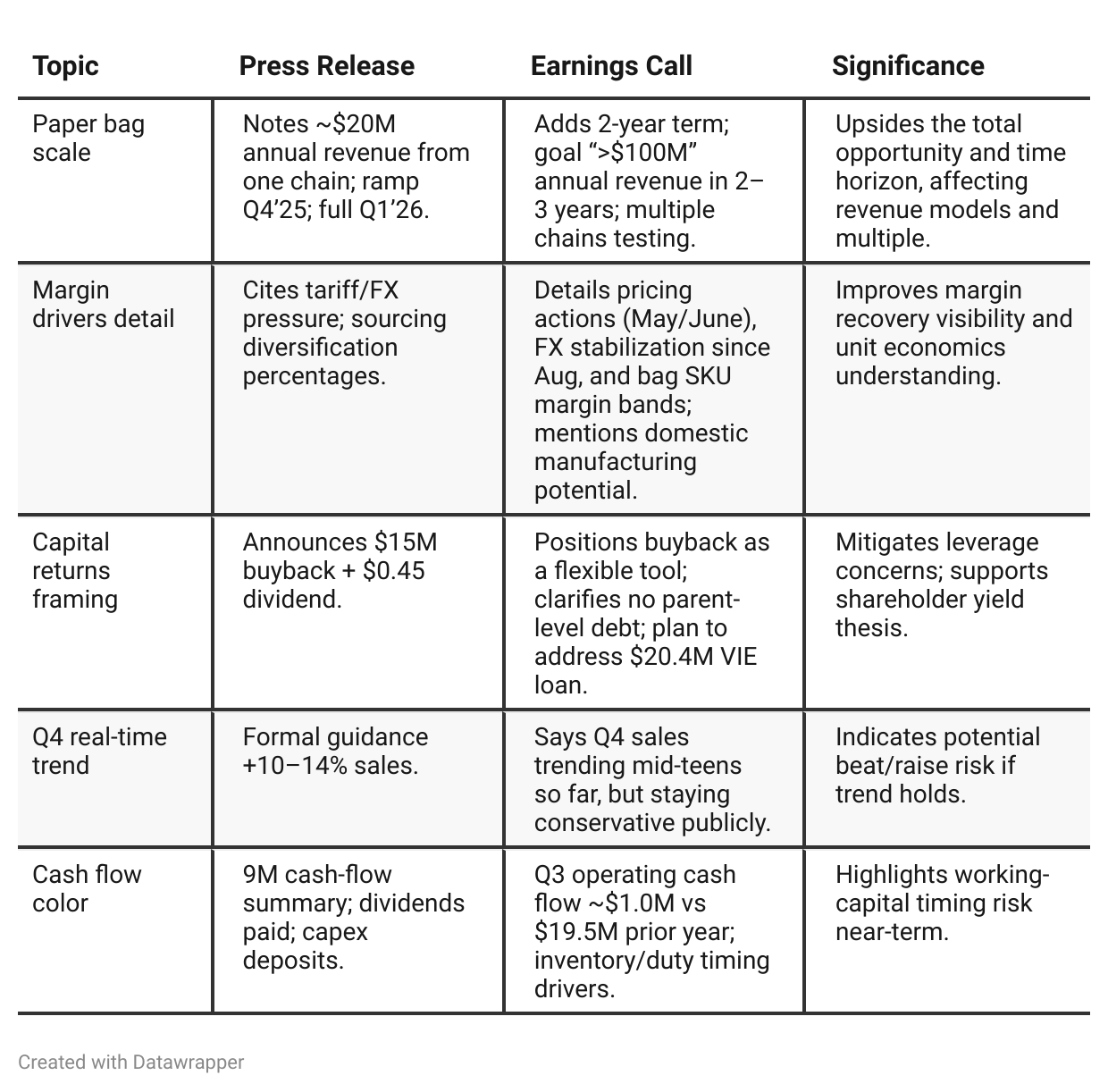

Press Release vs Call Transcript Comparison

Channel mix continues to favor chains/distributors; online grows modestly; retail under pressure. This supports a strategy skewed to enterprise wins and DTC optimization, with less reliance on retail recovery.

Sourcing shifts (higher U.S., lower Taiwan) are a structural hedge against tariffs—and could shorten lead times, aiding working-capital turns over time.

Management’s commentary implies pipeline breadth beyond the named chain (multiple tests), de-risking customer concentration in the new category.

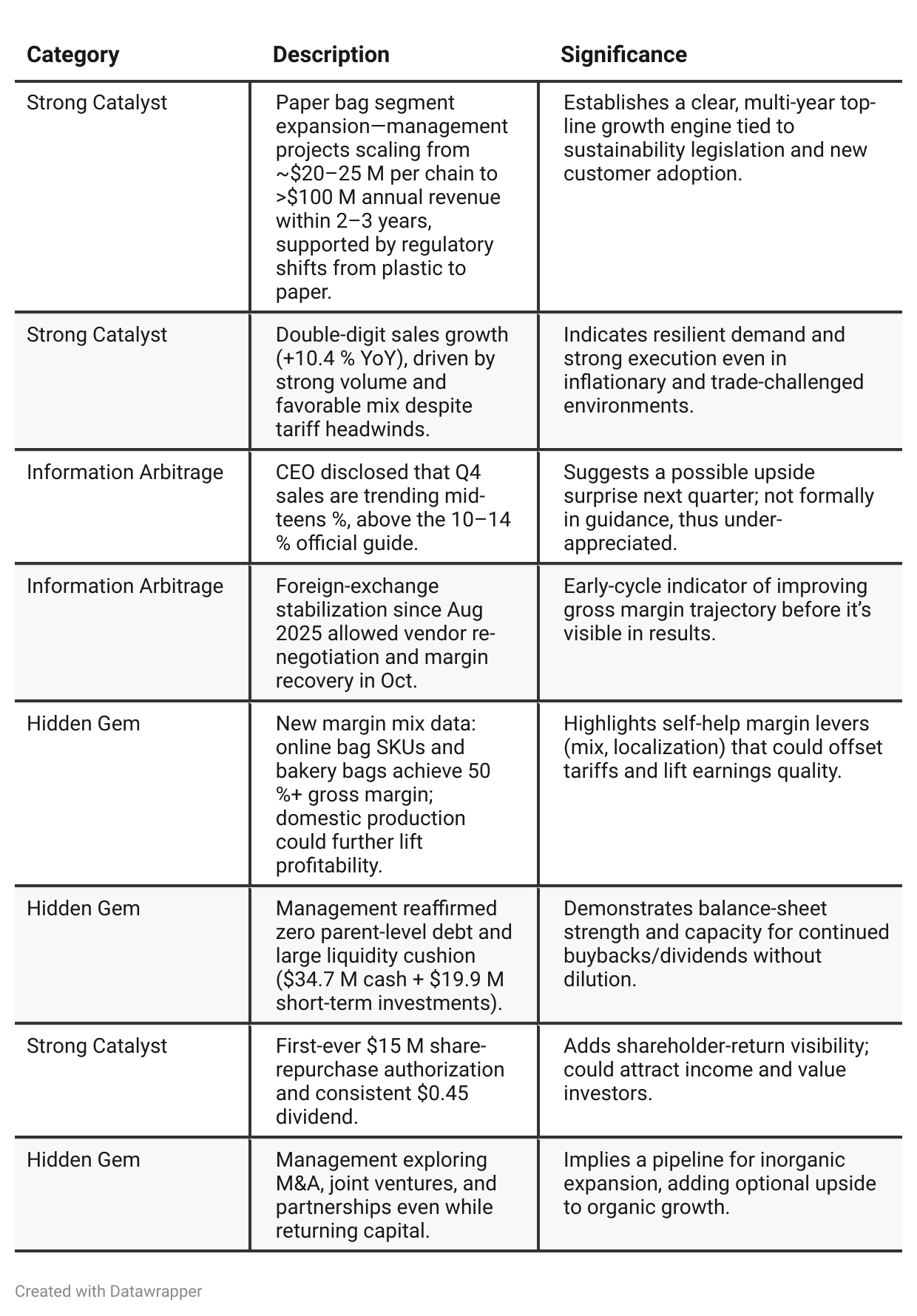

Positive Insights

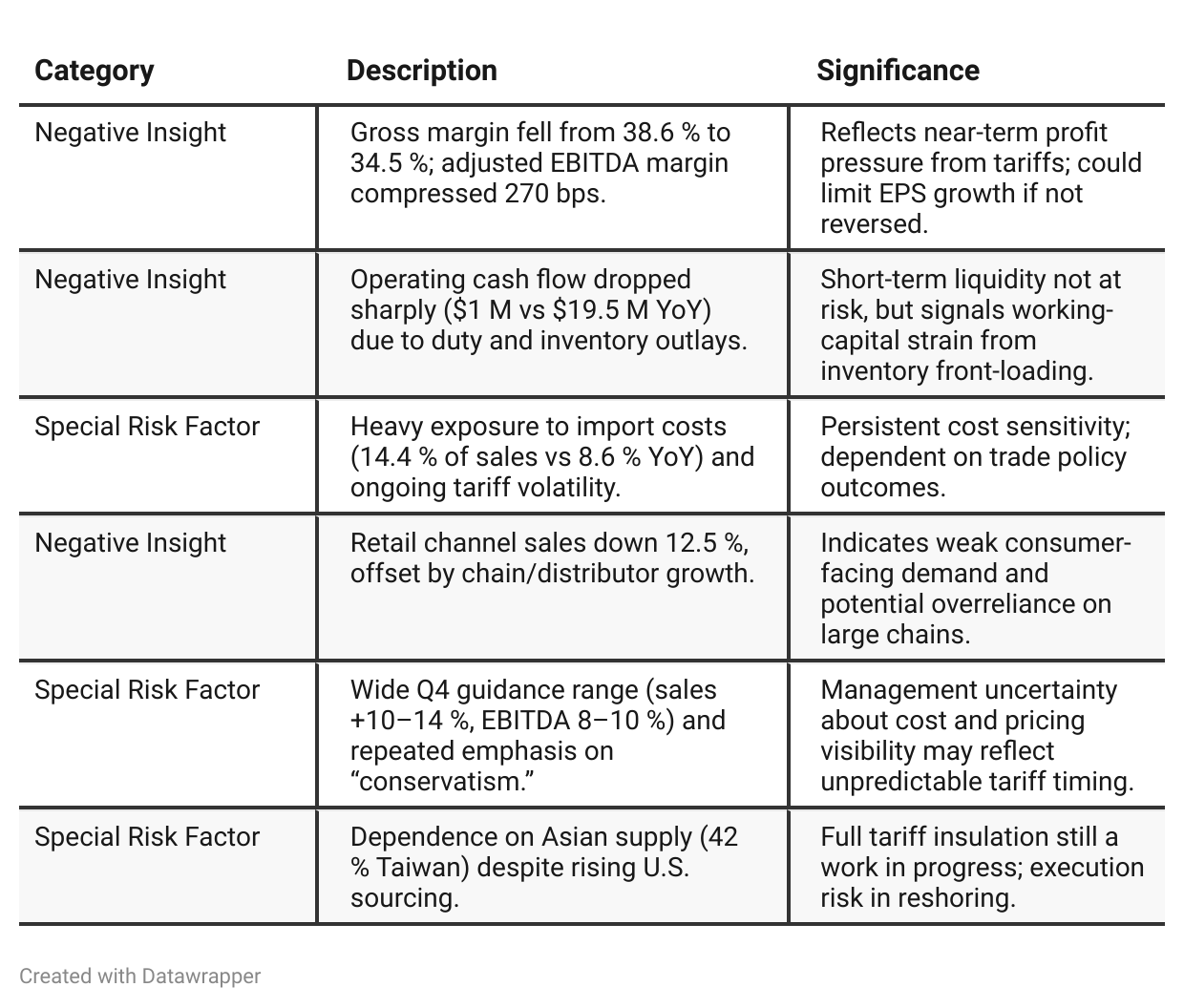

Negative Insights

Tariff Risk

Impact: Import costs rose > 60 % YoY; now 14.4 % of sales, compressing gross margin to 34.5 %.

Mitigation: Domestic sourcing raised to 20 %; Taiwan share cut to 42 %. Company plans further supply-chain relocation and may shift part of production to the U.S. to control costs.

Management View: FX stabilization and pricing actions since May/June expected to restore margins gradually.

Forward Outlook: If tariffs persist or worsen, upside limited; if eased, could trigger meaningful margin recovery and EPS re-rating.

Summary: Tariffs are the largest exogenous variable—company is actively adapting but remains exposed.

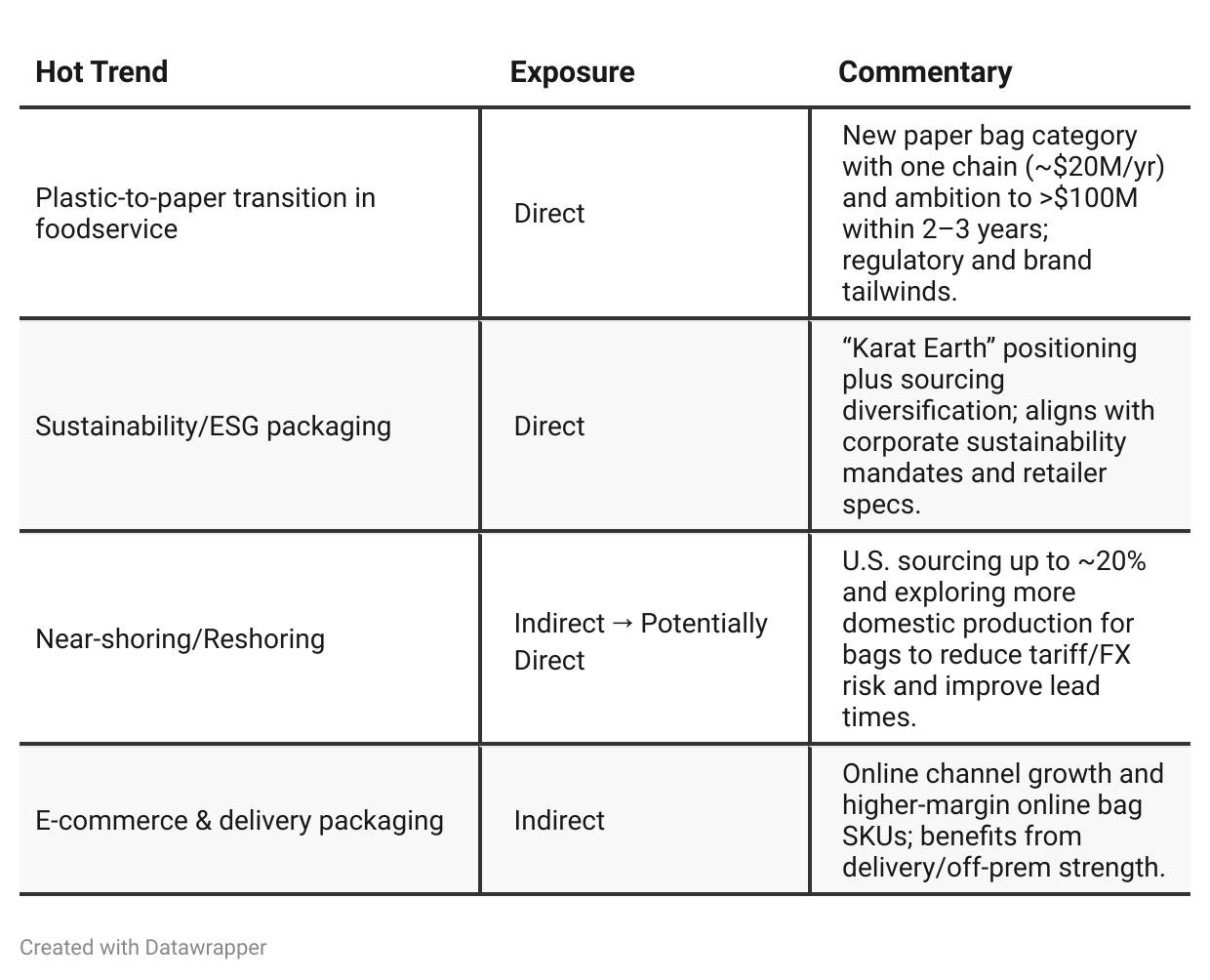

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2-25 → Q3-25: The story advances from “preparing the springboard” (diversified sourcing, DC live, pricing set, pipeline building) to “the jump has started” (paper-bag contract inked, shipments underway, multi-year >$100M scale target) while transparently showing the tariff hit to margins and cash flow. Management tempers margin optimism with conservatism, but offsets it with FX stabilization, vendor re-pricing, and a capital-return layer (dividend + buyback). Net-net: the growth narrative broadened and de-risked on demand, even as costs/macros remain the gating factor for near-term profitability.Year-over-year comparison

Karat Packaging’s story evolved from “profitable expansion” (Q3 2024) to “strategic resilience and capital return” (Q3 2025).

The company’s tone now reflects a balance between growth optimism and cost realism. Despite tariff-driven margin compression, management demonstrates operational agility (domestic sourcing, pricing actions) and confidence via buybacks and new product scaling.

Investors should view this as a transition year—moving from margin peak to diversified, cash-generative stability with optional upside in sustainable paper packaging.

Final Takeaway

Karat Packaging (NASDAQ: KRT) is in a growth phase, leveraging sustainability trends (paper-bag expansion) while navigating tariff-driven margin pressure. Management demonstrates operational discipline, debt-free balance sheet, and shareholder-return initiatives. While short-term profitability is dampened, medium-term outlook is strong if margin recovery follows FX stability and tariff moderation.

Verdict: BUY (Moderate Risk) – Upside from 2026 margin normalization and bag-segment scaling; downside tied to tariff persistence and execution pace.