Koil Energy Solutions, Inc. (OTCQB: KLNG) – Q2 2025 Earnings

Koil Energy Solutions, Inc. (OTCQB: KLNG) – Q2 2025 Earnings

Earnings Release Date: Aug. 14, 2025

Stock Price: $1.20

Market Cap: $14.5 million

Q2 2025 sales of $5.18 million vs $5.78 million in the prior year

Q2 2025 EPS of $0.01 vs $0.08 in the prior year

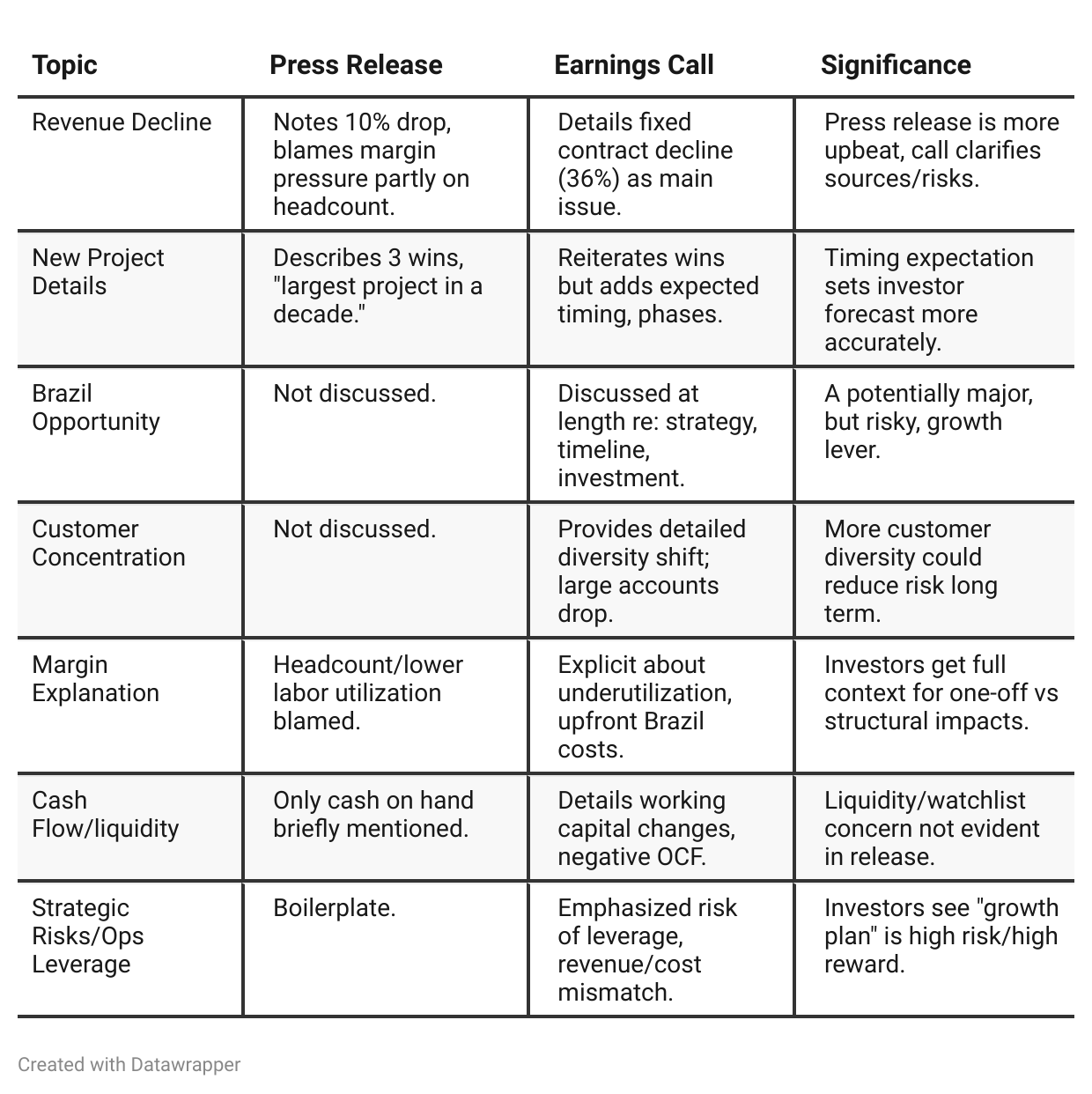

Press Release vs Call Transcript Comparison

The press release focuses on momentum, downplays risk, and accentuates growth language for Wall Street/investor confidence.

EBITDA/net income cited, but not related to cash flow or working capital volatility.

Implies contracted revenue pipeline is more certain than it may be (execution/timing challenges acknowledged more on the call).

The earnings call is more transparent about ‘why’ Q2 missed.

Explains volatility in project cycles and what will need to go right for a rebound.

Discusses up front risk in Brazil, customer concentration swing, and high operating leverage as both risk and potential reward.

Significant ‘difference’ for investors:

The call’s further granularity on project mix, customer concentration, and Brazil investment could identify meaningful risks or opportunities (for example, if Brazil fails, costs could drag; if Brazil succeeds, transformation is possible).

The headcount ramp, only partially covered in the release, is both a capacity enabler AND a current profitability drag, with future outcome dependent on project execution.

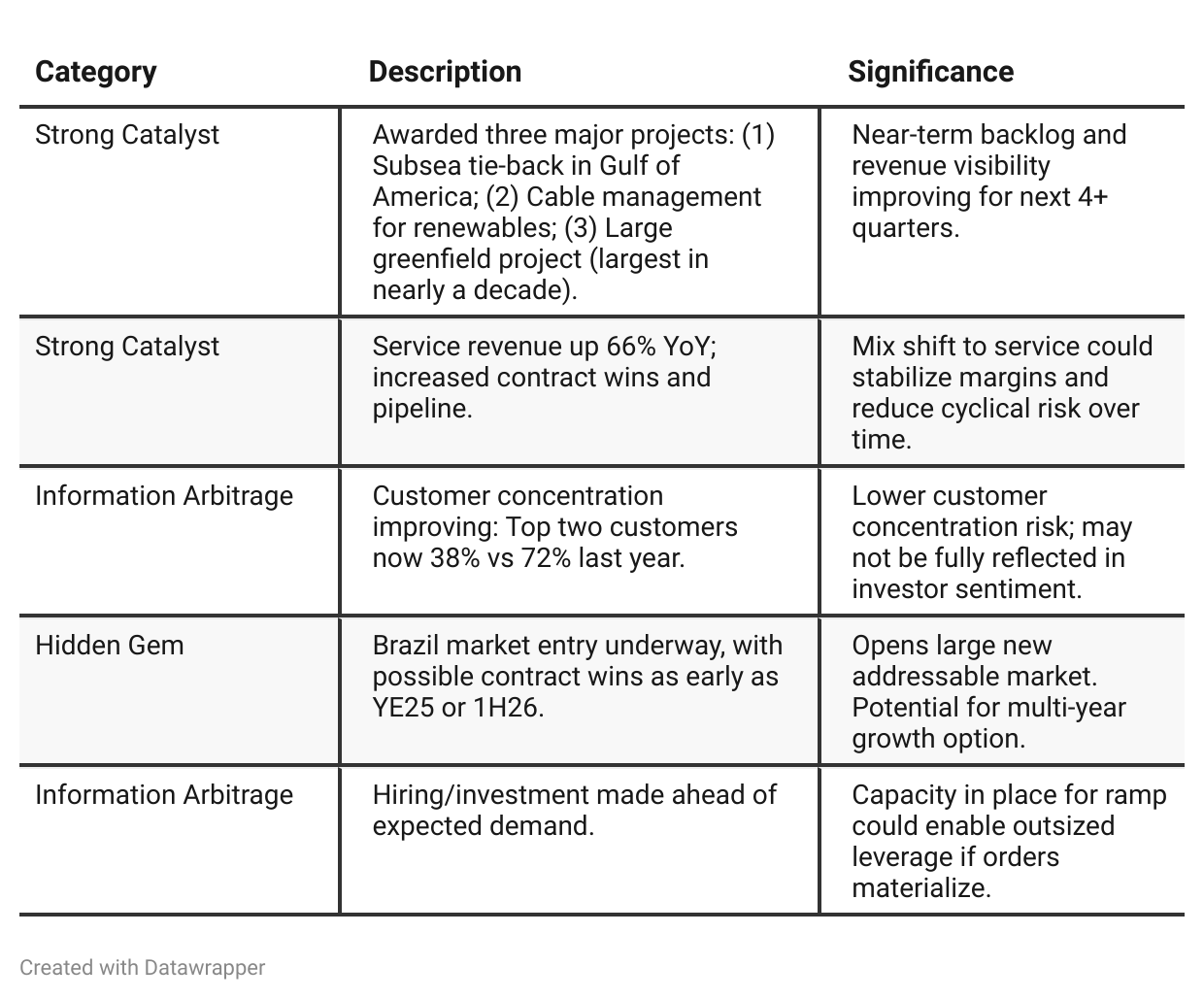

Positive Insights

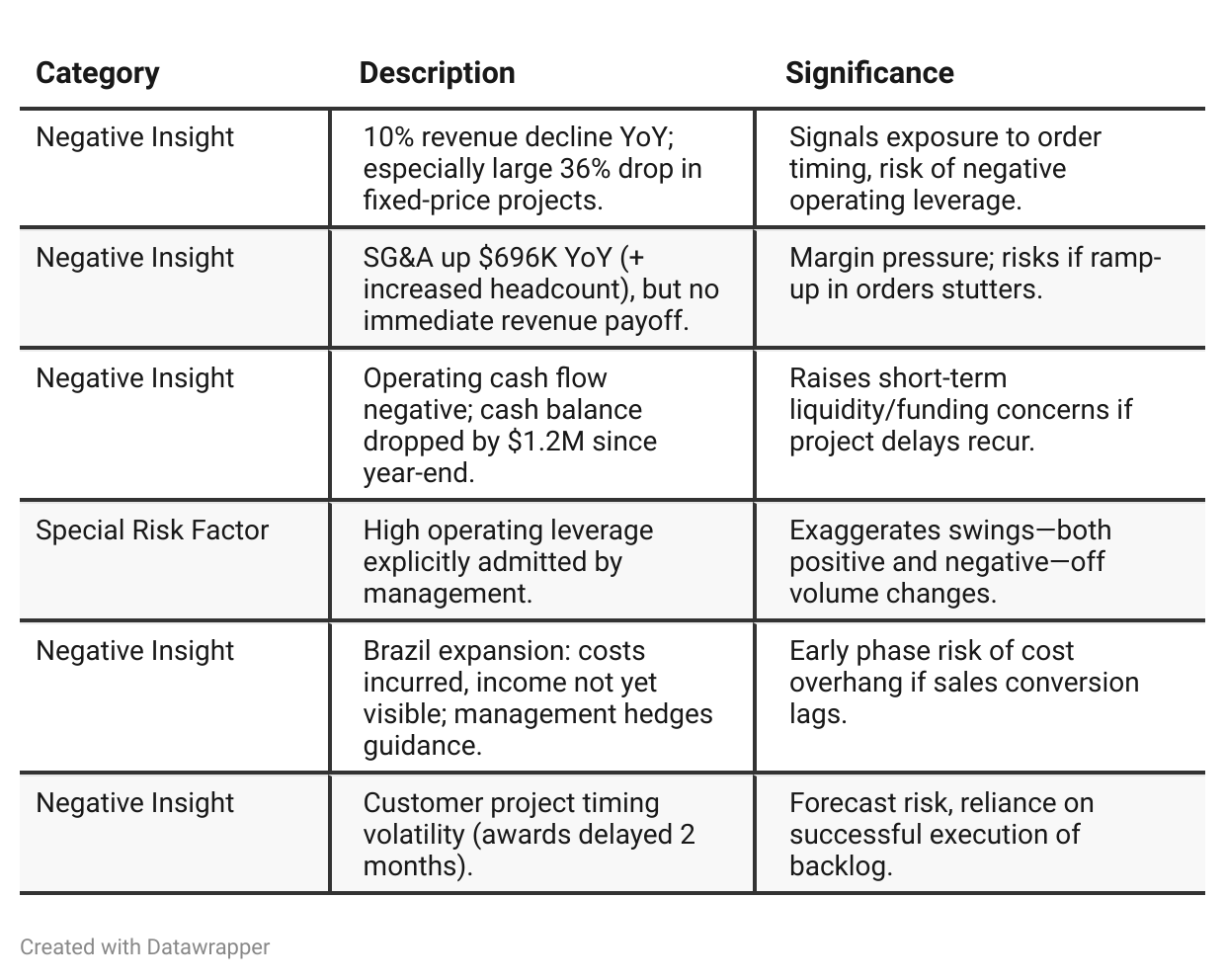

Negative Insights

Tariff Risk

Tariff/Trade Policy Section:

No explicit mention of U.S. tariffs, trade policy, or direct impact on supply chain or operations in the call.

No discussion of mitigation actions, supply chain shifts, or pricing responses to tariffs.

For now, no signals that tariffs or U.S. trade policies are affecting Koil’s reported revenues, profitability, or competitive stance. Investors should check future filings and calls, especially if Brazil- or U.S.-sourced content becomes more influential, for updates on this front.

Previous Earnings Call

Quarter-over-quarter comparison

Narrative Arc:Q1 2025: Koil Energy is open about growing pains—investing ahead of scale, dealing with the cost of underutilization, and having faith that their bets on capacity, especially SG&A and operational buildout, will pay off if order flow improves. Management strikes an explanatory, almost defensive posture but maintains belief in long-term positioning (citing specific contract wins and client satisfaction).

Q2 2025: The “wait” for revenue inflection appears to be giving way—fresh contract wins are tangible evidence that buildout was (potentially) the right move. Messaging is less about apologizing and more about capitalizing on existing momentum. Risk factors shift from “why aren’t we growing yet?” to “can we now execute against a large backlog and turn improved order intake into margins, cash flow, and sustainable growth?” Customer concentration risk falls, the Brazil gamble starts to look nearer to payoff, and assertiveness replaces caution in tone.

Year-over-year comparison

Koil Energy’s journey from Q2 2024 to Q2 2025 traces a classic cycle:

2024 was about acceleration, market validation, and harvesting returns from earlier bets.

Management crowed about high growth, margin expansion, major contract wins, and flawless execution.

Narrative: “We are executing our growth strategy and the market is responding.”

2025 represents a pause and recalibration.

Macro tailwinds and opportunity still exist, but are now countered by internal execution struggles, cost pressures, and delays.

The messaging moves from triumph to realism: “We’ve invested for growth and have tangible wins, but short-term pain and delayed gratification are the new reality.”

Management tries to reassure investors that structural changes (diverse customers, new backlog, bigger service footprint, Brazil entry) will eventually deliver returns once the project and macro cycle becomes more favorable.

Narrative: “We’re weathering short-term headwinds, have built the muscle for more growth, and are positioned to rebound.”

Final Takeaway

Koil Energy is in a transition/growth phase with elevated volatility. Major new project wins signal improved momentum, and international expansion (notably Brazil) could set the stage for multi-year upside. Yet, operating leverage is acute, the company is burning cash, and evidence of sustained order-to-revenue conversion is still pending. Hold rating is appropriate: upside potential is clearly present, but prudent investors should seek further confirmation in upcoming quarters—especially on cash flow stabilization and execution in new markets.