Jacobs Solutions Inc. (NYSE: J) – Q3 2025 Earnings

Jacobs Solutions Inc. (NYSE: J) – Q3 2025 Earnings

Earnings Release Date: Aug. 5, 2025

Stock Price: $139.92

Market Cap: $16802.1 million

Q3 2025 sales of $3,031.8 million vs $2,883.4 million in the prior year

Q3 2025 EPS of $1.56 vs $0.66 in the prior year

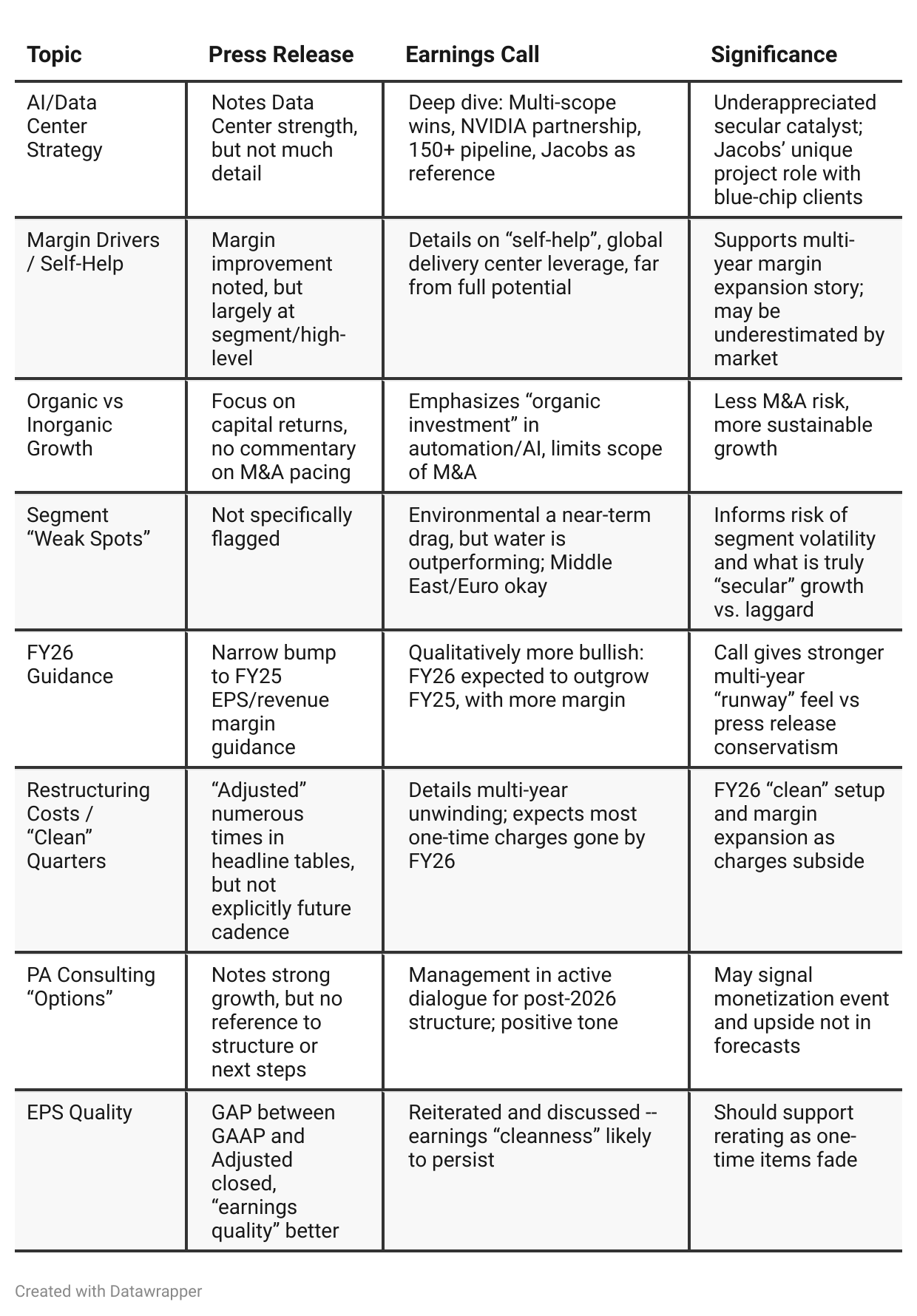

Press Release vs Call Transcript Comparison

Earnings Call is More Forward-Looking: The call provides stronger and more granular forward commentary (AI/data, Europe/ME, PA Consulting, digital focus, backlog mix), making the investment case more robust.

Capital Returns Not Just Talk: Transcript surfaces consistent buybacks, above 100% FCF payout, subtracting 4% of shares YTD—management views shares as attractively priced.

FY26 Set-up Appealing: With separation cost roll-off, organic growth/margin levers, and robust backlog, Jacobs appears to have a multi-year pathway for double-digit EPS growth and cash returns.

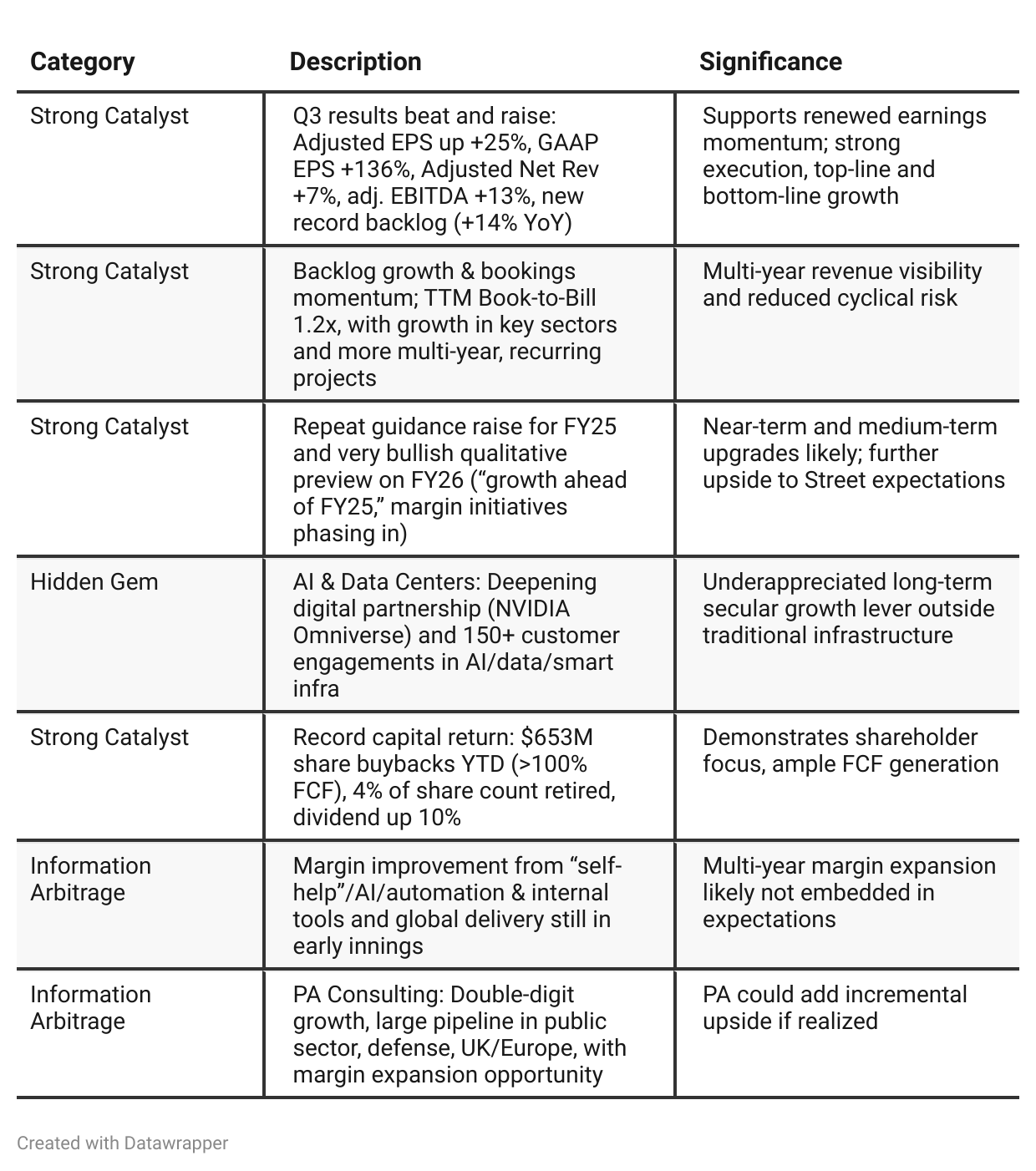

Positive Insights

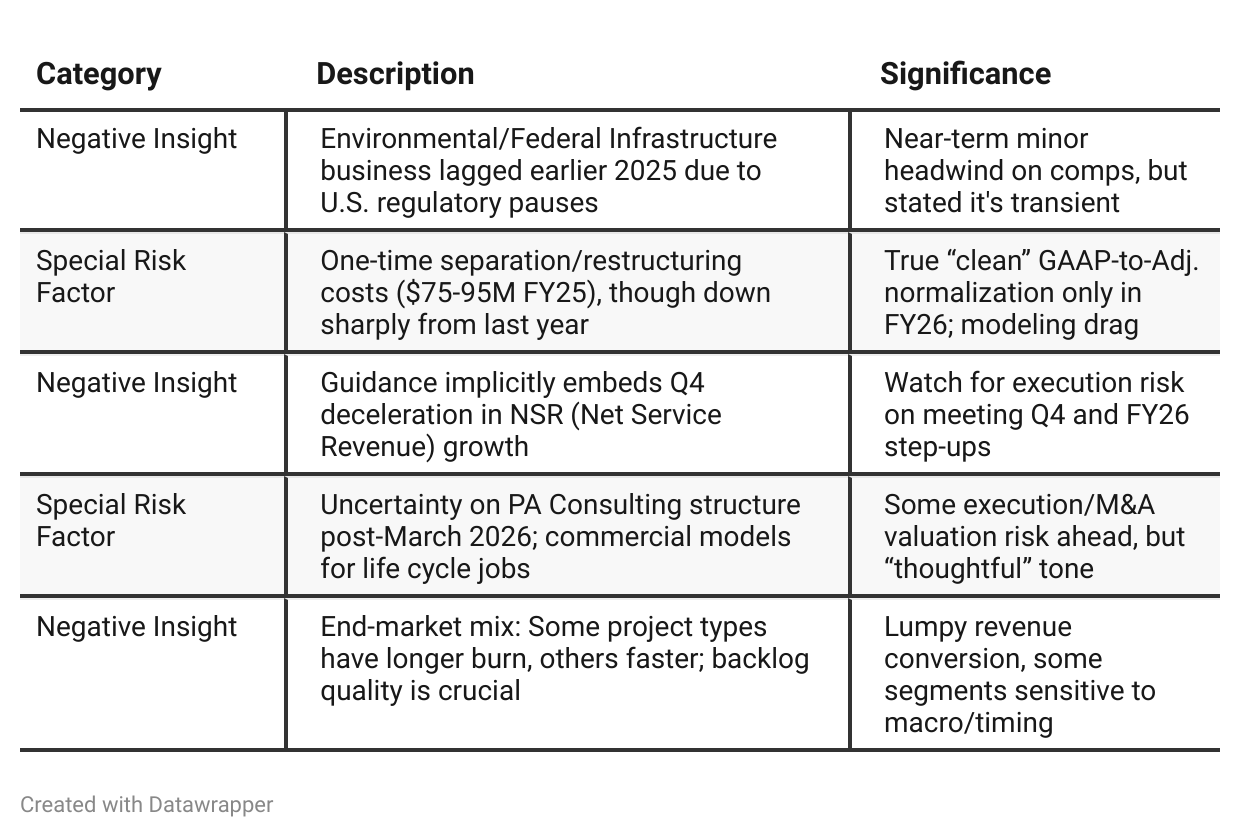

Negative Insights

Tariff Risk

Tariffs/Trade Discussion in Transcript: There are only brief, generic references to tariffs or trade policy in the management’s risk statements and no segment or regional color during Q&A or prepared remarks.

Findings:

In prepared disclosures, management names tariffs/trade policies as a broad legislative risk.

No explicit commentary on recent or expected tariff impacts, import content, supply chain shifts, or pricing actions.

No discussion of shifting production or margin headwinds/tailwinds from tariffs.

Implications for Investors:

Management does not see material tariff risk to guidance or outlook, or their exposure is modest and diversified across geographies and supply chains.

Investors should monitor future filings for updates in case U.S. or cross-border trade policy changes accelerate.

No evidence of current adverse or positive effect on market share or innovation path.

Summary: Tariffs do not present a quantifiable risk for Jacobs at this time per transcript content. Investors should, however, remain vigilant for changes in global trade policy, especially around infrastructure, digital/AI hardware, and energy markets.

Previous Earnings Call

Quarter-over-quarter comparison

Jacobs’ narrative has transitioned from a posture of resilience and operational cleanup (Q2), dealing with one-time challenges (legal reserve, separation costs), and relying on backlog quality to “weather the storm,” to an assertive growth story (Q3) with upgraded guidance, strong execution, and new secular tailwinds—particularly in digital infrastructure and AI/data centers.PA Consulting and strategic wins (NVIDIA partnership, global digital/AI engagements, energy transformation) are now center-stage in the narrative, with sustained margin expansion and capital returns underpinning the shareholder thesis. Q3’s tone is far more confident, growth-centric, and forward-looking, signaling that Jacobs is not just defensive, but positioning itself as a platform for multiyear secular growth.

Year-over-year comparison

Jacobs in Q3 2024 was a story in transition—navigating a major spin-off, absorbing headline costs, and emphasizing a mix shift to higher margin, higher value consulting and science-based work as the platform for its future. Management was disciplined but still defensive, and while operational and capital return discipline were clear, the company was keen to reassure investors that the transition would pay off.

By Q3 2025, Jacobs has fully turned the corner. The company is characterized by strong, margin-led growth, record and qualitatively robust backlog, and now targets secular growth markets such as AI data centers, digital/AI transformation, and resilient infrastructure. Management is no longer focused on “fixing” or “separating,” but on “winning” and “expanding” its global platform and innovation pipeline; the narrative is more growth-centric, assertive, and multi-year in scope.

Final Takeaway

Jacobs (J) is in a leadership growth phase following separation, powered by secular tailwinds (AI/data, water, life sciences), record backlog, and self-funded capital return. While short-term segment cyclicality and residual one-time costs pose minor risks, management’s disciplined execution and bullish FY26 margin/revenue outlook support rerating potential. Execution on digital partnerships, margin initiatives, and segment resiliency are the key to unlocking further shareholder value. Verdict: Buy, with upside as market digests multi-year earnings and cash generation inflection.