IZEA Worldwide, Inc. (NASDAQ: IZEA) – Q2 2025 Earnings

IZEA Worldwide, Inc. (NASDAQ: IZEA) – Q2 2025 Earnings

Earnings Release Date: Aug. 12, 2025

Stock Price: $3.73

Market Cap: $63.2 million

Q2 2025 sales of $9.1 million vs $9.1 million in the prior year

Q2 2025 EPS of $0.07 vs ($0.13) in the prior year

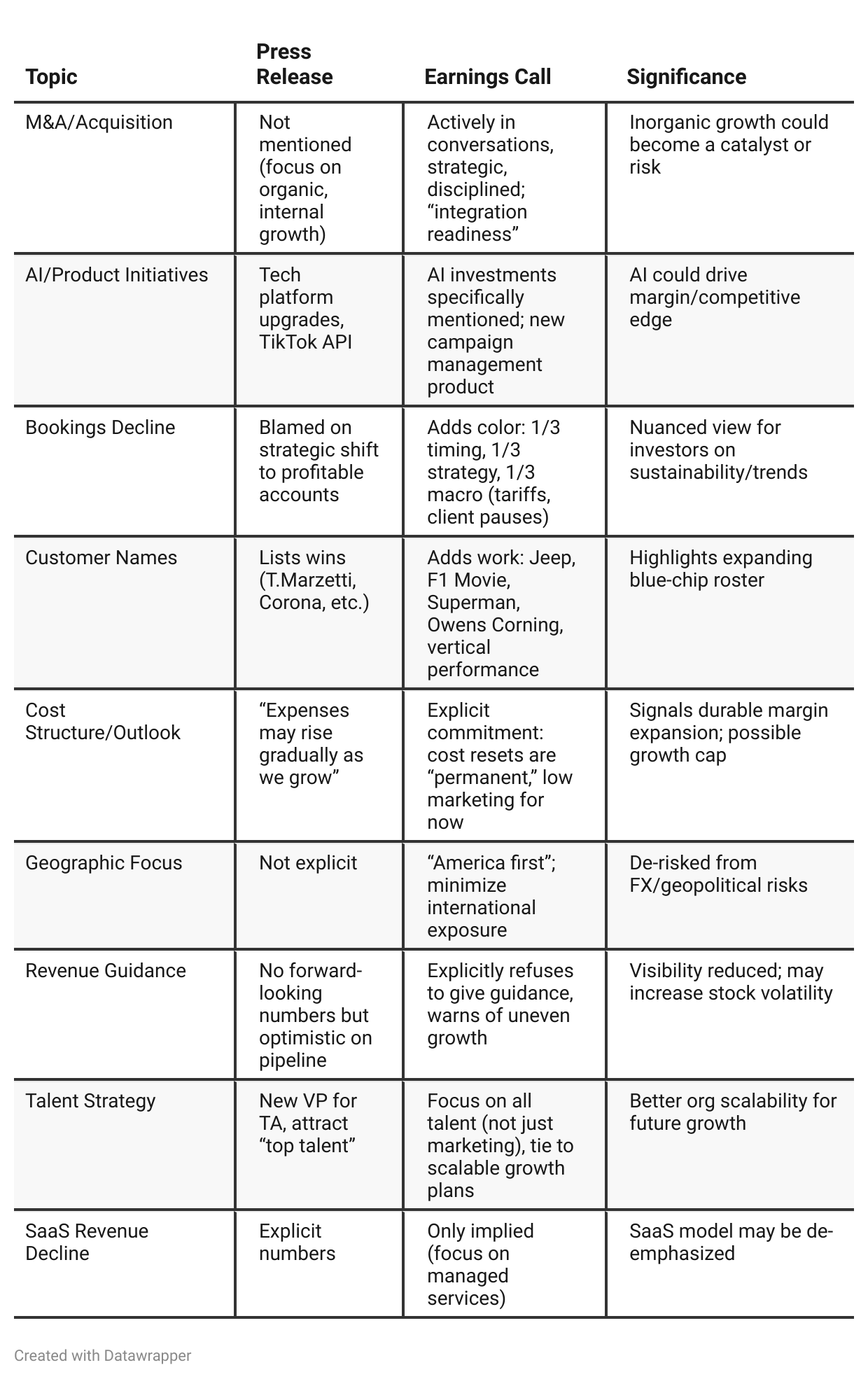

Press Release vs Call Transcript Comparison

Transformation in Business Model: Both documents stress transformational changes, but the call makes it evident that this means not just improved margin but a complete reset of how IZEA pursues accounts, measured investments, and long-term vision.

M&A Readiness and Discipline: The call’s focus on not overpaying, having integration systems ready, and being strategic with acquisitions signals a thoughtful, less risky approach to inorganic growth compared to many microcaps.

Technology Investment Intent: The emphasis on AI and technology enhancements is more explicit on the call, suggesting future automation, better margins, and possibly product differentiation.

Cautious optimism: While both documents are upbeat, the call is careful to hedge against uneven growth—this realism helps investors calibrate expectations but also signals prudent management.

Exposure to Macro/Economic Uncertainty: The earnings call narrative adds texture to what “client pauses” and “vertical outperformance” actually mean, highlighting both risk and opportunity due to sectoral strategies.

Liquidity and Balance Sheet Strength: Consistent message: high cash, no debt, share buybacks, and readiness for both organic and inorganic initiatives—this balance sheet strength is a safety net for additional bets if opportunities arise or macro turns negative.

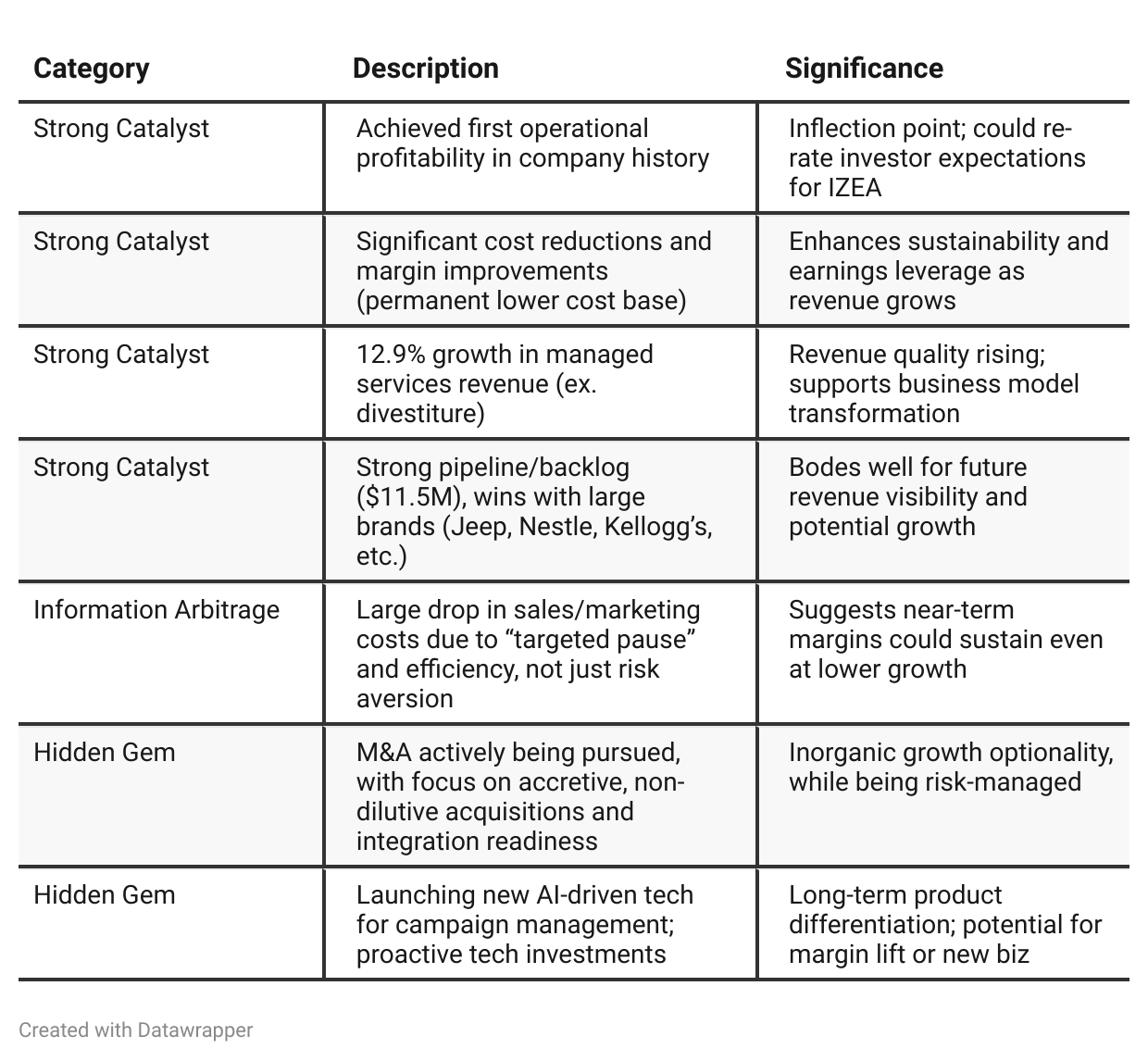

Positive Insights

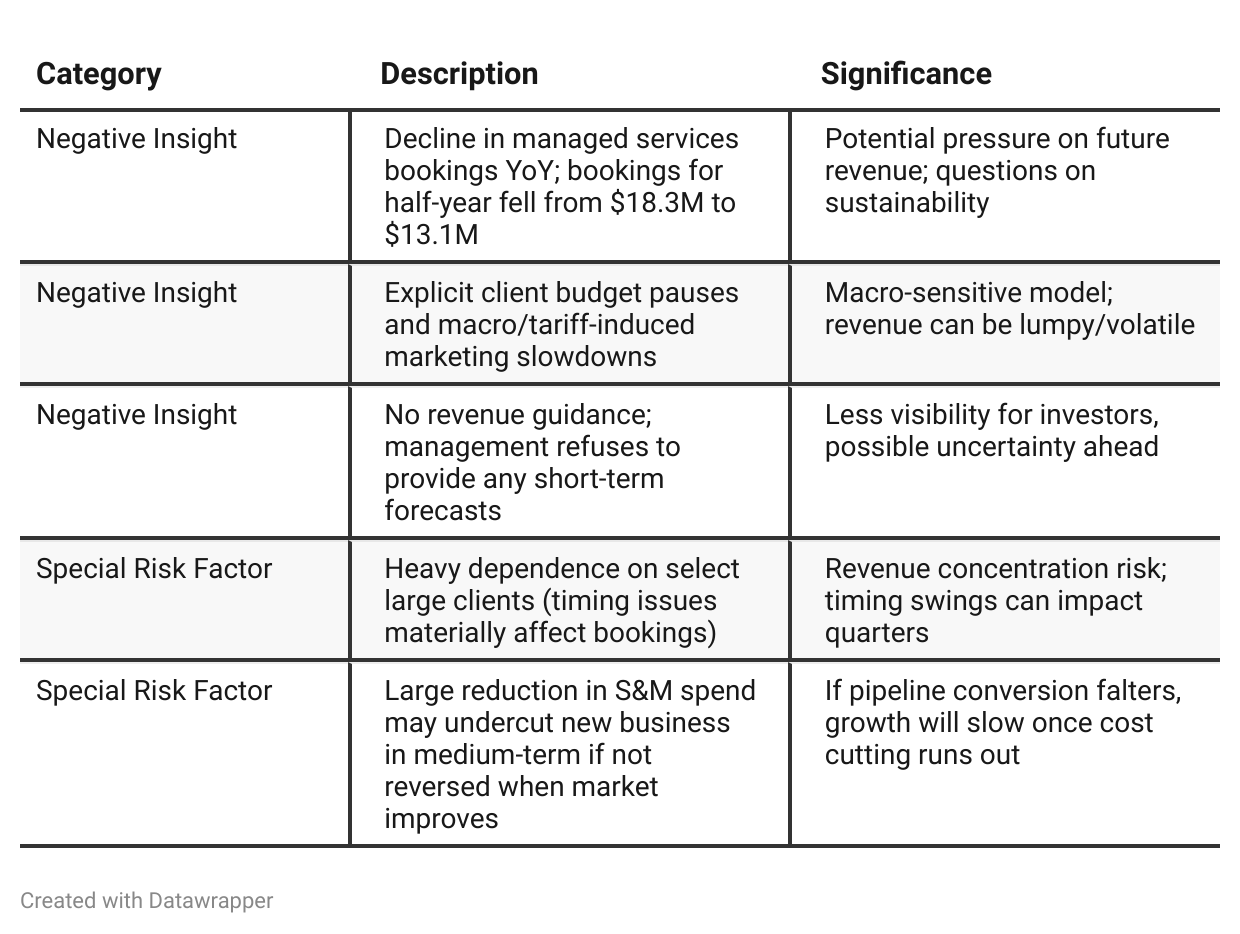

Negative Insights

Tariff Risk

Tariff Effects Mentioned:

Management specifically attributes part of the bookings decline and budget pausing to “tariff-related uncertainties affecting certain industries.”

No quantification or direct mitigation steps provided on the call.

CEO emphasized “America first” model, implying a strategy to reduce international exposure and possibly avoid tariff impacts on the supply/cost side.

Mitigating Actions:

Strategic focus on domestic (‘America first’) and higher-quality customers may be a deliberate hedge to avoid international/trade-related volatility.

Forward-Looking Statements:

Acknowledgement that macro conditions, including tariffs, produce uncertainty. Management says some client verticals have been strong, but this is not a comprehensive offset.

Conclusion on Tariff Risks: While IZEA is feeling the effects of tariffs via customer budget caution, its business model shift may partially insulate against future shocks. However, without more detail, the durability of this strategic adjustment remains to be proven, and investors should watch for additional macro/trade commentary in company filings and future calls.

Previous Earnings Call

Quarter-over-quarter comparison

At Q1 2025, IZEA projected the story of a company in active turnaround—bold moves to simplify the business, slash costs, and refocus strategy on the US market and higher-quality opportunities were front and center. While revenue growth was strong and losses narrowed dramatically, the tone was about “nearly” achieving profitability and about foundational work for future results.By Q2 2025, this groundwork pays off: the company proudly reports its first operational profit ever, signaling a tangible inflection that validates the prior quarter’s strategy. The messaging shifts from aspiration to accomplishment, with an eye on sustaining and scaling efficiency, technological investment (especially in AI), and disciplined M&A to fuel the next phase of growth. Still, Q2 reflects more caution around macro headwinds and visibility (“uneven” growth expected), signaling continued discipline and realism as the company moves forward.

Year-over-year comparison

In Q2 2024, IZEA was a company in transition:

Management candidly described a tough period after losing a major customer and operating at a loss, but pointed to booming bookings, tech/AI-driven efficiency, and a healthy cash position as reasons for optimism. The tone was one of rebuilding—focused on diversifying customers, leveraging technology, integrating small acquisitions, and returning to growth.

By Q2 2025, the narrative matures into one of milestone achievement and newfound discipline:

The company achieves its first ever operational profit, validates its cost and account-quality resets, and touts an efficient, focused business model. The tone is confident but more measured, recognizing macro/tariff-driven risks and calling out disciplined expense management over unchecked growth. Where 2024 was about “when we turn the corner,” 2025 is “we’ve turned it—but must sustain it.” Execution, focus, and risk management are recurring motifs, and the playbook calls for scaling efficiently, expanding high-margin relationships, and making selective M&A moves.

Final Takeaway

IZEA is in a transformation phase, having reached operational profitability for the first time while executing strategic cost reductions and shifting to higher-quality contracts. Strong cash reserves and a buyback provide downside protection. However, sequential bookings declines, macro headwinds (including tariff effects), and a lack of forward guidance introduce uncertainty. Execution on pipeline conversion and sustaining client demand are key for the next leg up. Verdict: Hold, with upside if secular tailwinds or bookings rebound; downside if demand continues to soften.