Ituran Location and Control Ltd. (NASDAQ: ITRN) – Q2 2025 Earnings

Ituran Location and Control Ltd. (NASDAQ: ITRN) – Q2 2025 Earnings

Earnings Release Date: Aug. 19, 2025

Stock Price: $40.28

Market Cap: $801.3 million

Q2 2025 sales of $86.8 million vs $84.9 million in the prior year

Q2 2025 EPS of $0.68 vs $0.66 in the prior year

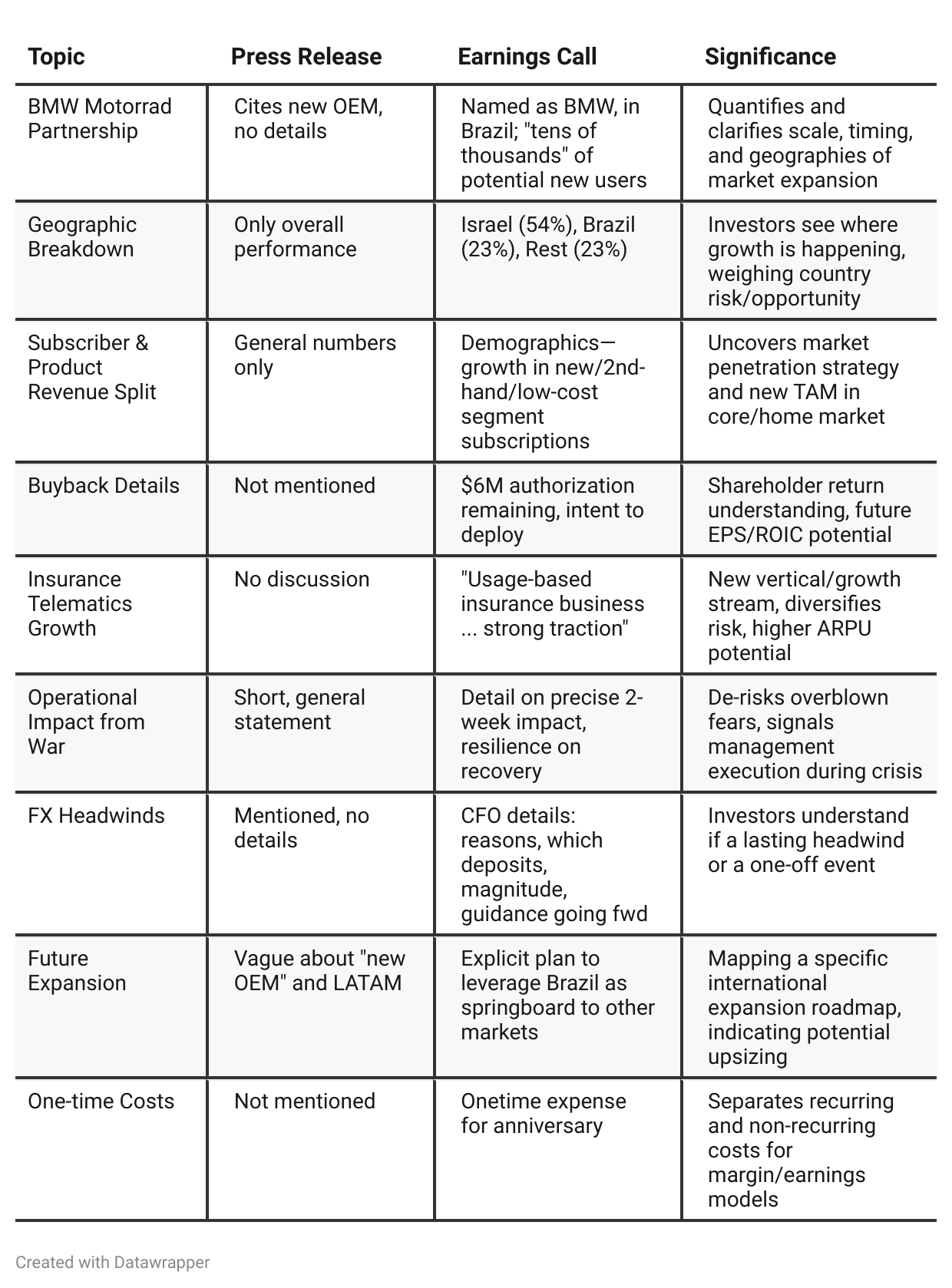

Press Release vs Call Transcript Comparison

Tone & Color: The call delivers affirmation of resilience (quick rebound after war), cultural strength and employee loyalty (30th anniversary), and strong management/shareholder alignment (dividend and buyback focus).

Guidance: Management reaffirms subscriber growth forecast (220k-240k for FY25), even after conflict, lending credibility to prior guidance.

Cyclical or Transitory vs. Structural: Product sales dip and OpEx rise are positioned as one-offs, while recurring revenue and new market segments/offerings (motorcycles, insurance telematics) signal ongoing core strength.

Currency Sensitivity: Both documents highlight FX risk but only the call provides context and relative magnitude, aiding modeling for international investors.

Cash Flow & Balance Sheet Strength: Both note strong cash generation and net cash position but the—call’s buyback discussion—puts a finer point on possible capital allocation moving forward.

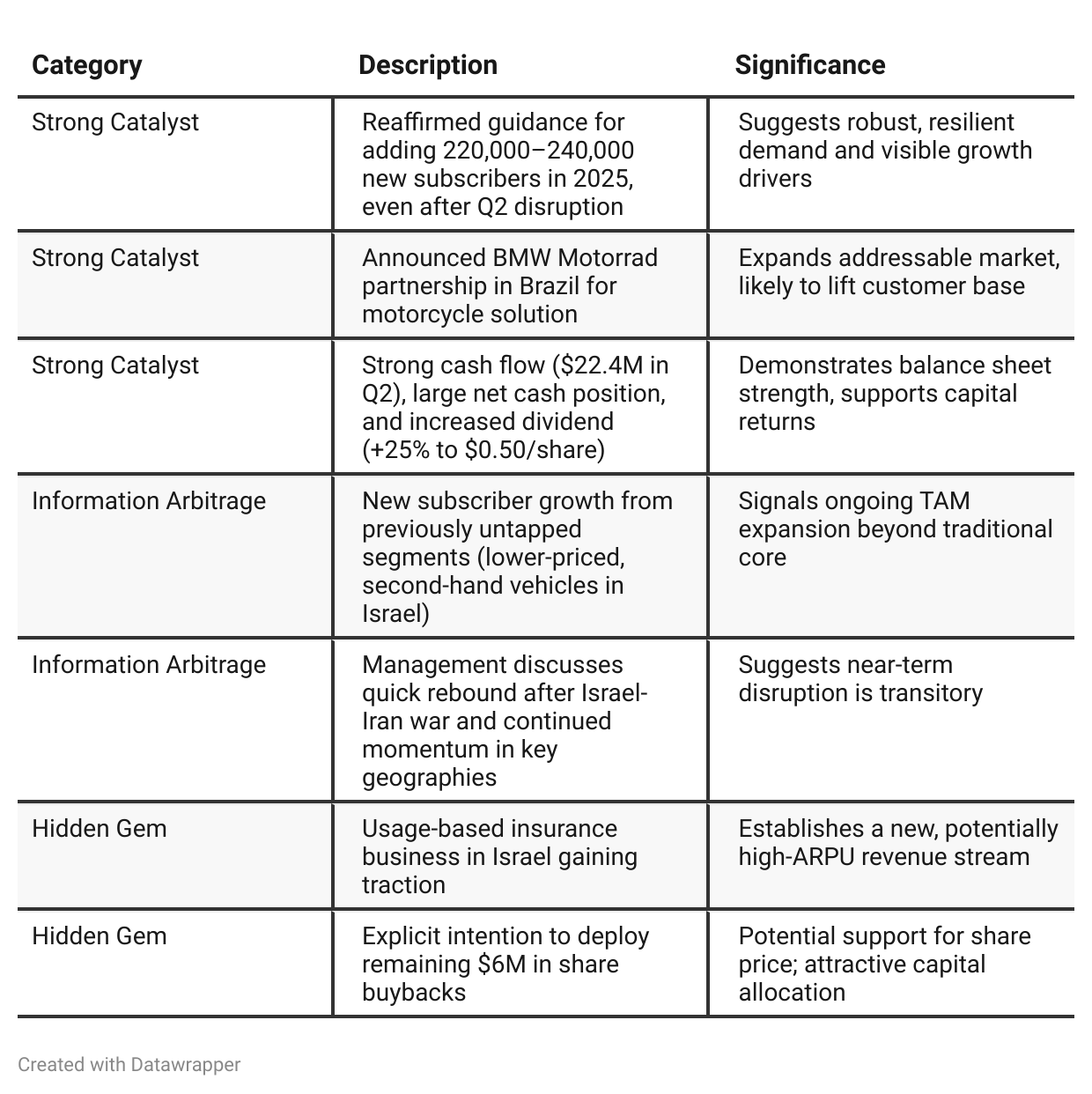

Positive Insights

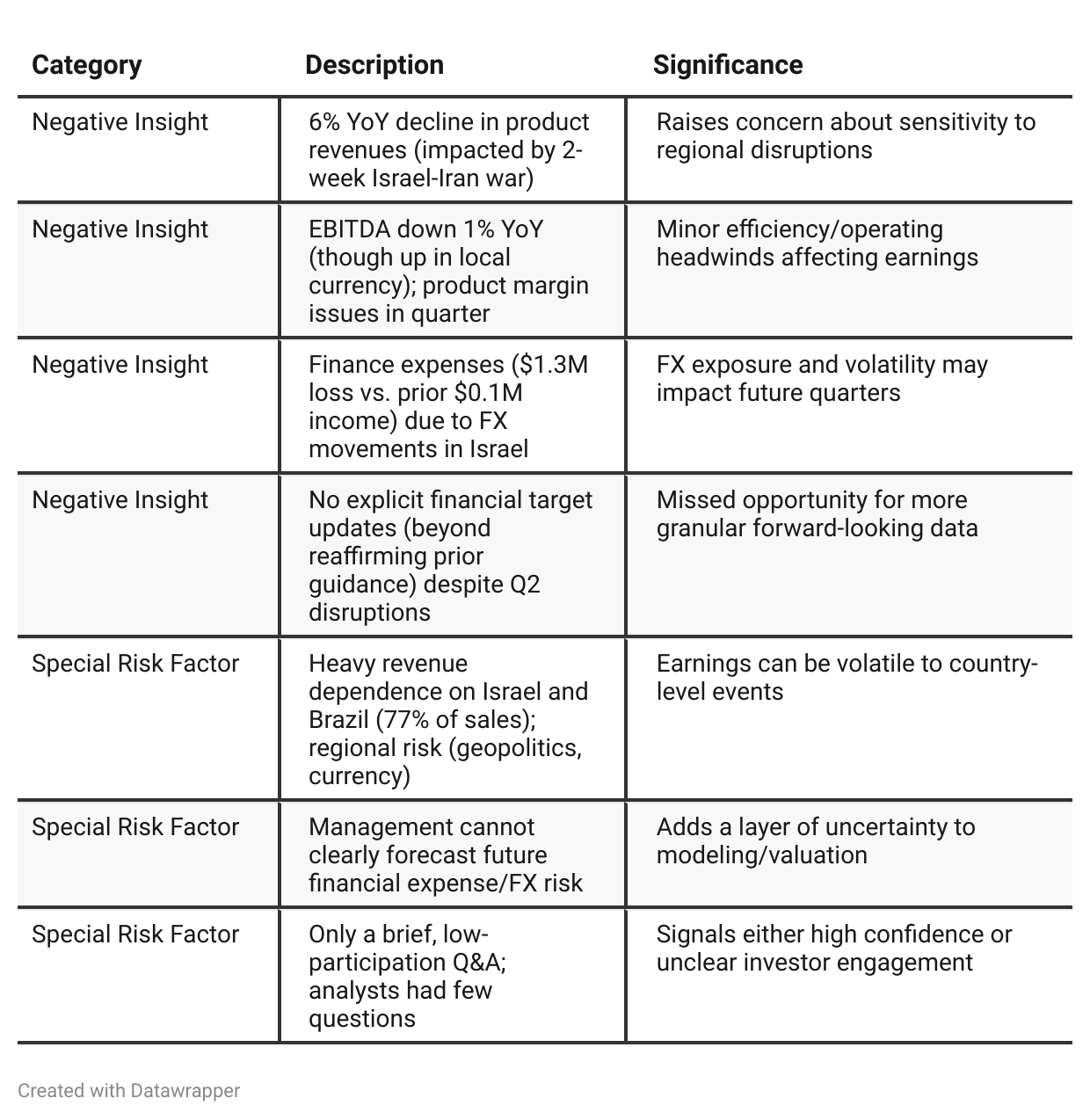

Negative Insights

Tariff Risk

Mentions: The transcript contains no discussion of U.S. tariffs or trade policy. There are no stated impacts, risk mitigations, or strategic responses regarding tariffs, nor any forward-looking statements about trade policy effects.

Implications: As Ituran operates in technology/telematics (mainly in Israel and Latin America), tariffs do not appear to be a current, material risk per management’s commentary. For investors concerned about trade exposure, review subsequent filings and monitor for mention of supply chain/geopolitical changes in future calls.

Sentiment Analysis

The overall sentiment toward Ituran Location and Control Ltd. ($ITRN) is bullish. Investors are expressing confidence in the stock, frequently citing its increased dividend, healthy revenue and net margin growth, consistent subscriber expansion, and trust in management. Several classify the stock as undervalued or a “buy” at current levels, with one noting the recent share price dip as a buying opportunity despite an EPS miss, due to strong fundamentals and prospects from new markets. Few, if any, concerns or negative views are presented, supporting a positive outlook.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q1 2025 painted a story of acceleration, with management celebrating record subscriber growth, a key new Stellantis OEM relationship, and increased guidance for the year. The focus was on topline momentum, long-term OEM strategy, and preparing investors for a normalization in “bulk” subscriber additions. Financial commentary was optimistic, with improvements across most metrics, without any external disruptions clouding the outlook.Q2 2025 reveals a company tested by significant external headwinds for the first time in a while (regional conflict, unfavorable FX movement), but the narrative remains confident and steadfast. Management’s messaging shifts subtly—less about headline growth, more about resilience, stability, cash flow, and new routes for expansion (notably the BMW motorcycle partnership). The company leans into its diversified subscriber base, recurring revenue streams, and capital-return policies, while transparently acknowledging temporary setbacks and the uncertainties of the operating environment.

Year-over-year comparison

From Q2 2024 to Q2 2025, Ituran’s narrative has shifted from one of confident innovation and expansion to one emphasizing durability, shareholder friendliness, and flexibility amidst global headwinds. In 2024, management’s story was about driving new verticals, pursuing strategic partnerships, and building an innovation pipeline, with recurring revenue growth making potential FX “noise” secondary. By 2025, the company had delivered on key OEM deals (notably BMW in Brazil), but found itself tested by geopolitical shocks and sharp FX moves. The messaging adjusted accordingly: while growth initiatives continue, the primary tone now is one of resilience, focus on stable dividends, maintaining operating momentum despite adversity, and disciplined capital allocation.

Management’s evolution in communication moves from “look at our growth engine and innovation pipeline” to “see our stability and reliable execution, even through unexpected crises.” The consistent thread is a dedication to growing subscribers and recurring revenues, but with a more pronounced emphasis on managing risk, rewarding shareholders, and prudent, defensive stewardship of the business.

Final Takeaway

Ituran is in a growth phase, leveraging core recurring revenue and expanding via new product categories (e.g., motorcycle telematics) and markets (notably in Latin America). Despite regional disruption (Israel-Iran), the company maintained guidance and highlighted resilience and operational discipline. FX and regional concentration risks remain, but strong cash flow, a rising dividend, and an active buyback provide support and downside protection. Execution in new segments (OEM, insurance telematics) and geographic expansion will be the swing factor for outsized future returns. Verdict: Buy, with upside as growth catalysts play out and risks are managed.