Intermap Technologies Corporation (OTCQB: ITMSF) – Q2 2025 Earnings

Intermap Technologies Corporation (OTCQB: ITMSF) – Q2 2025 Earnings

Earnings Release Date: Aug. 14, 2025

Stock Price: $2.17

Market Cap: $121.4 million

Q2 2025 sales of $3.0 million vs $3.6 million in the prior year

Q2 2025 EPS of $0.01 vs $0.01 in the prior year

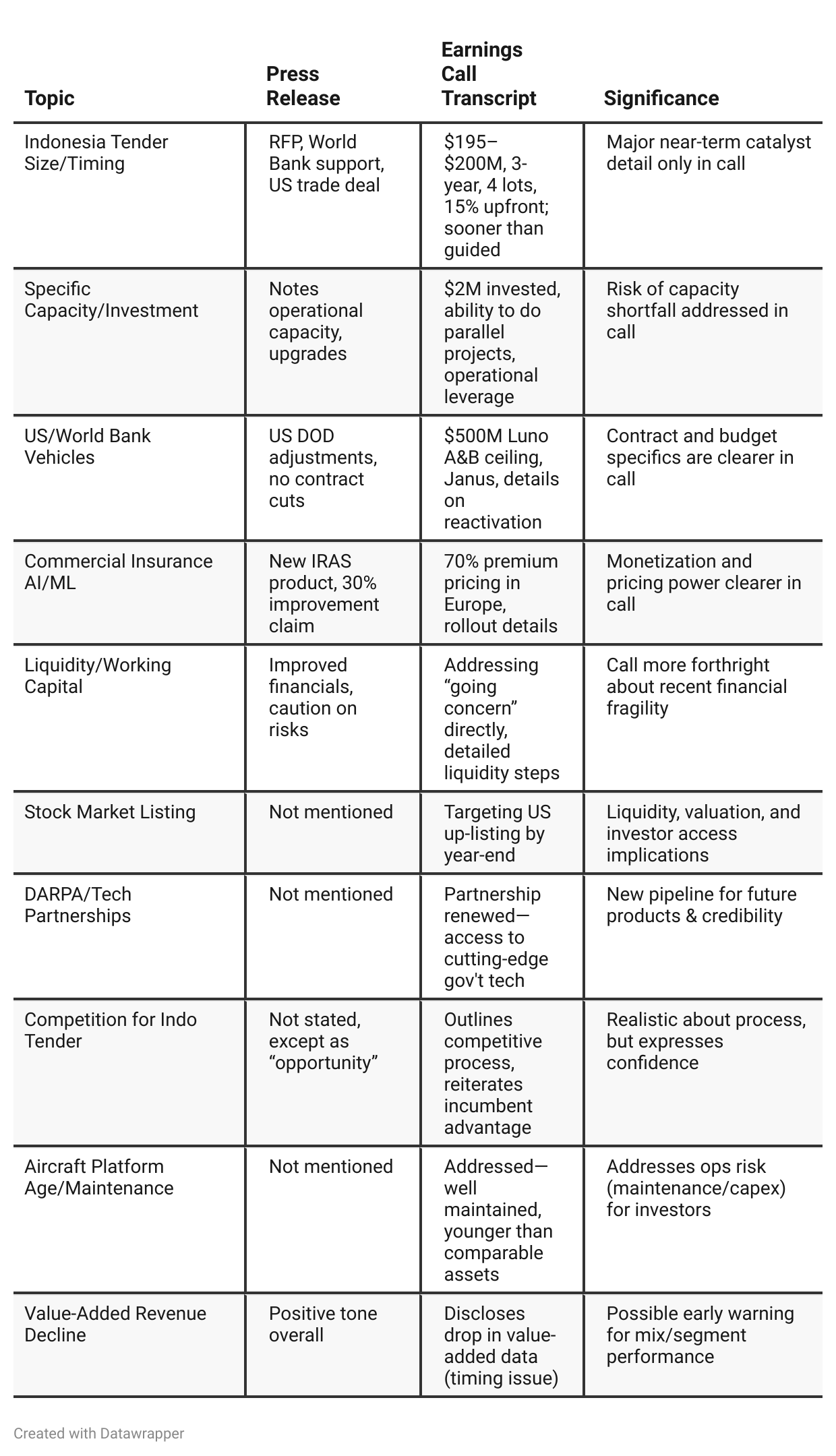

Press Release vs Call Transcript Comparison

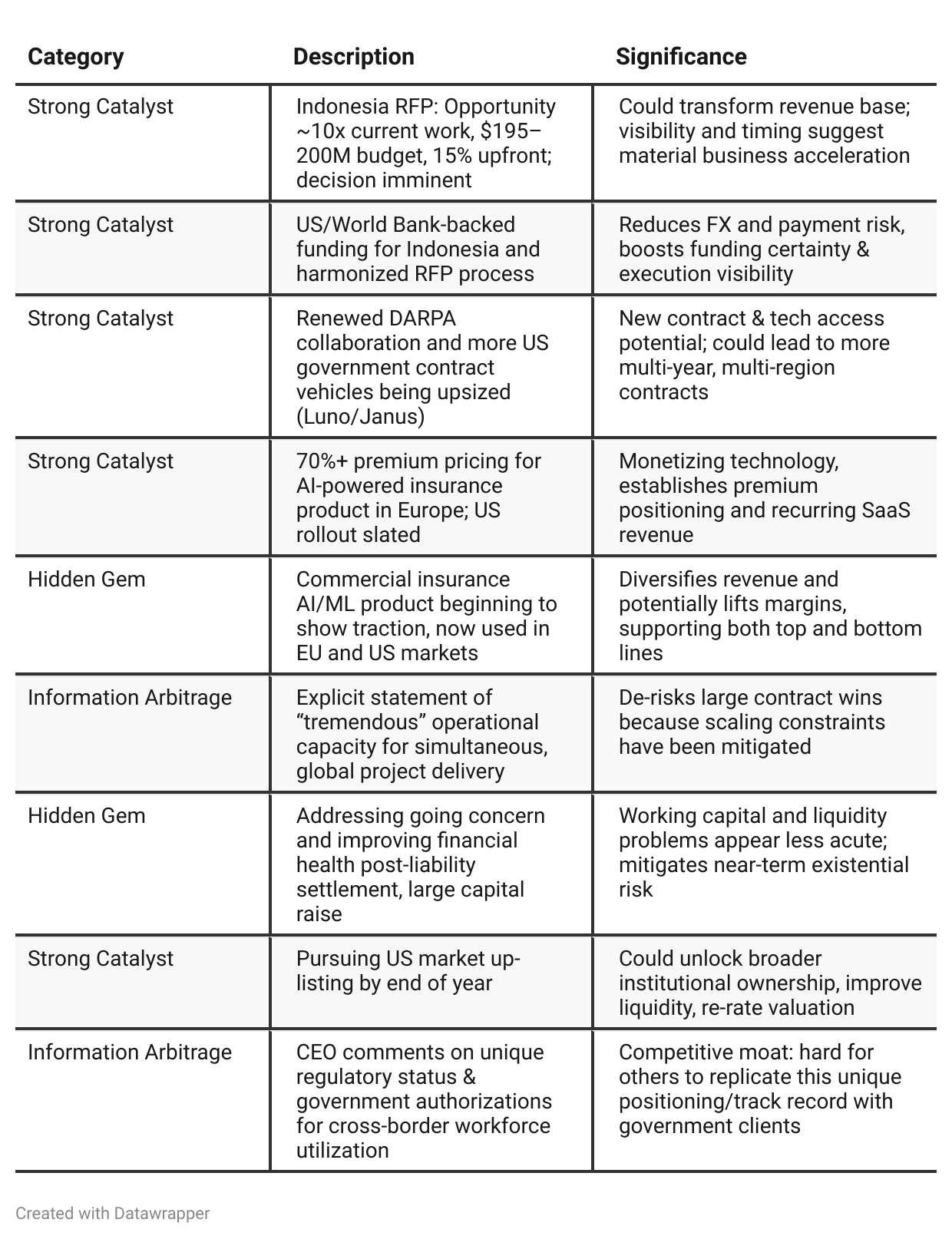

Market Expansion: The call makes it clear the addressable market (especially for mapping and risk) is tied to ongoing global instability—so demand fundamentals aren’t just cyclical, but potentially secular.

Operational Leverage: Investments in platforms and processing mean new contracts could yield high drop-through to profit/cash.

Segment Performance Transparency: The call provides revenue by geography/segment and is clear on where shortfalls are timing-related, de-risking but not eliminating top-line misses.

Incumbency and Technology Moat: The call’s explicit discussion of custom platforms, rare US government carveouts, and deep roots in Indonesia reinforce that barriers to entry are high, though not insurmountable.

Product Diversification: The expansion into insurance uses the same tech base but provides an independent, potentially recurring revenue stream.

Management Forthrightness: Willingness to address frontally issues of competition, risk, and capacity is a positive governance signal.

Positive Insights

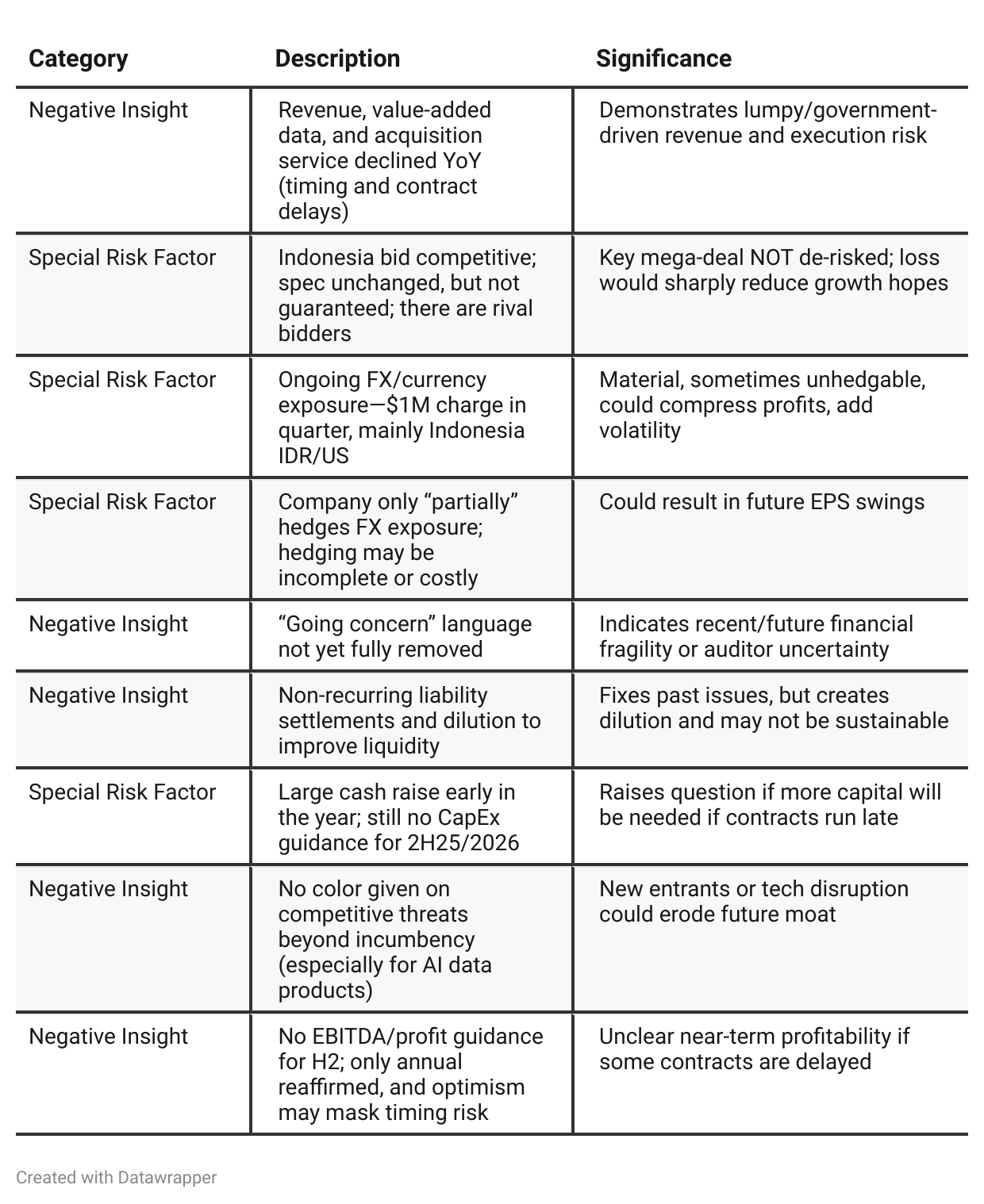

Negative Insights

Tariff Risk

Direct Impact: Intermap states it is not affected by recent cross-border tariffs because it does not source hardware or materials from Canada or tariff-exposed regions.

Currency Volatility: The company took a $1M currency charge, partly due to macroeconomic factors including tariffs affecting the IDR-USD exchange rate.

Mitigation: Future Indonesia contracts will be funded in USD via the World Bank, significantly reducing FX and tariff-related risk going forward.

Competitive/Operational Impact: No supply chain pressure or loss of market share related to tariffs; digital services focus and international agreements further insulate the business.

Bottom Line: Tariffs do not present a material risk to Intermap’s revenue, supply chain, or ability to compete; investors should monitor currency volatility, not direct tariff exposure.

Previous Earnings Call

Quarter-over-quarter comparison

From Q1 to Q2, Intermap Technologies’ narrative has evolved from steady, well-disciplined execution, careful risk management, and incremental growth in niche financial and strategic technology markets, to a company intensely focused on securing transformational, contract-driven growth opportunities on the world stage. While operational upgrades, liquidity improvements, and new AI/ML product successes are encouraging, the company’s fate is increasingly tied to the outcome of a handful of large government tenders—most notably the imminent Indonesia megaproject. Management’s tone has shifted toward ambitious, opportunity-driven messaging, but with bluntness about the associated risks and competitive landscape.Year-over-year comparison

—

Final Takeaway

Intermap Technologies is in a turnaround/growth phase, focusing on large government mapping contracts (notably Indonesia) and expansion of its insurance AI/ML SaaS platform. While the imminent Indonesia contract, US government re-acceleration, and improved liquidity represent strong upside catalysts, the company remains exposed to execution risk (especially competition for the Indonesia deal), FX volatility, and historical financial fragility (going concern language not fully eliminated). Execution on major contract awards and continued diversification into commercial insurance will be critical for value realization. Verdict: HOLD—with significant potential upside if Indonesia or other large contract wins materialize in H2 2025.