IRIDEX Corporation (NASDAQ: IRIX) - Q2 2025 Earnings

IRIDEX Corporation (NASDAQ: IRIX) - Q2 2025 Earnings

Earnings Release Date: Aug. 12, 2025

Stock Price: $1.30

Market Cap: $21.8 million

Q2 2025 sales of $13.6 million vs $12.6 million in the prior year

Q2 2025 loss per share of ($0.06) vs ($0.16) in the prior year

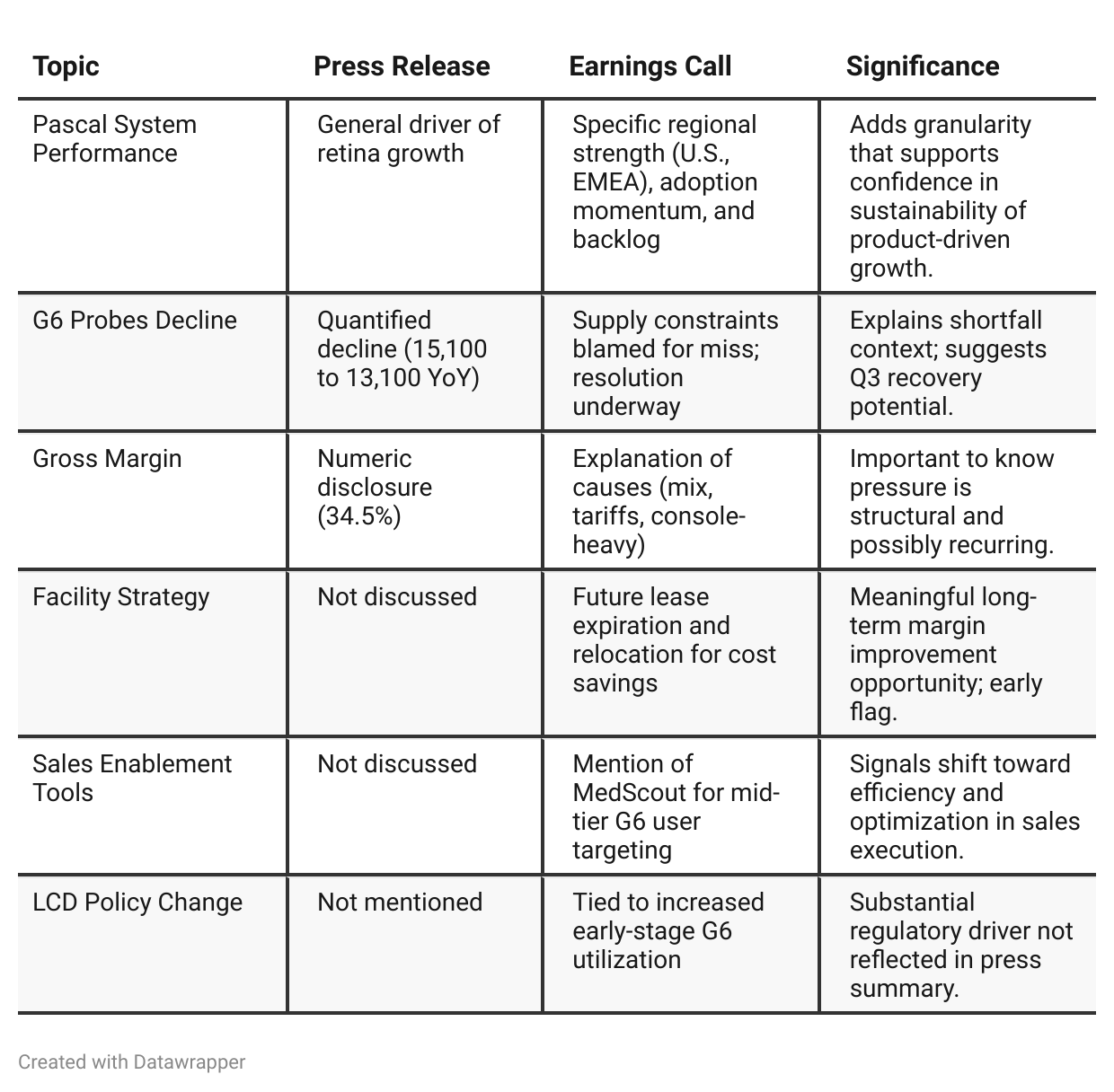

Press Release vs Call Transcript Comparison

The press release presents a clean, progress-focused financial update centered on revenue growth and expense control, but it omits several operational and strategic insights that emerged on the earnings call. The call highlights regional market complexity, outlines margin improvement tactics (e.g., facility move, contract manufacturing), and discloses operational tools like MedScout and new reimbursement tailwinds for the G6 system.

These distinctions matter—while the press release supports a turnaround story, the call enhances investor confidence by illustrating how management is executing tactically. For investors weighing IRIDEX’s momentum and sustainability, the earnings call offers more actionable depth.

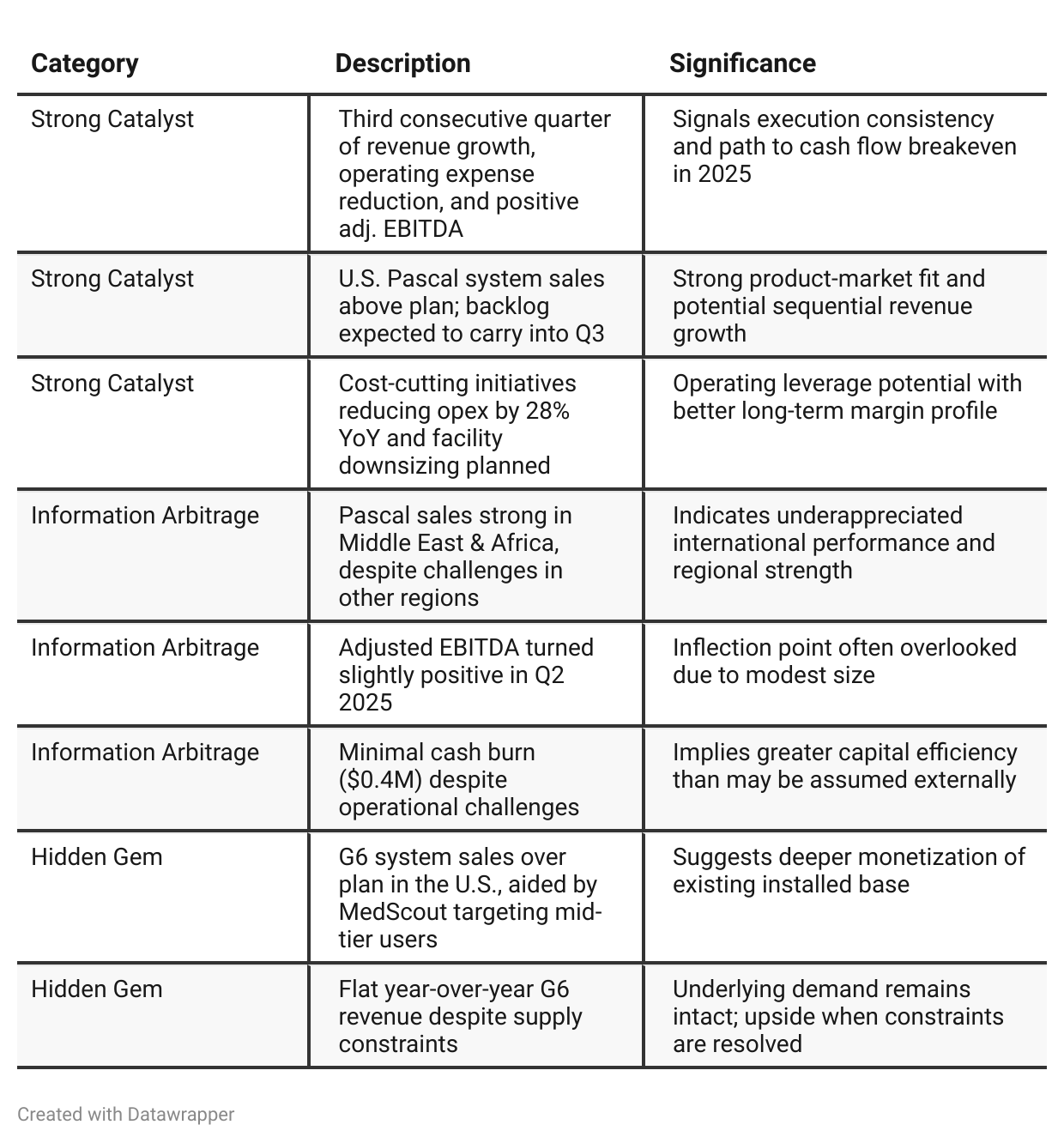

Positive Insights

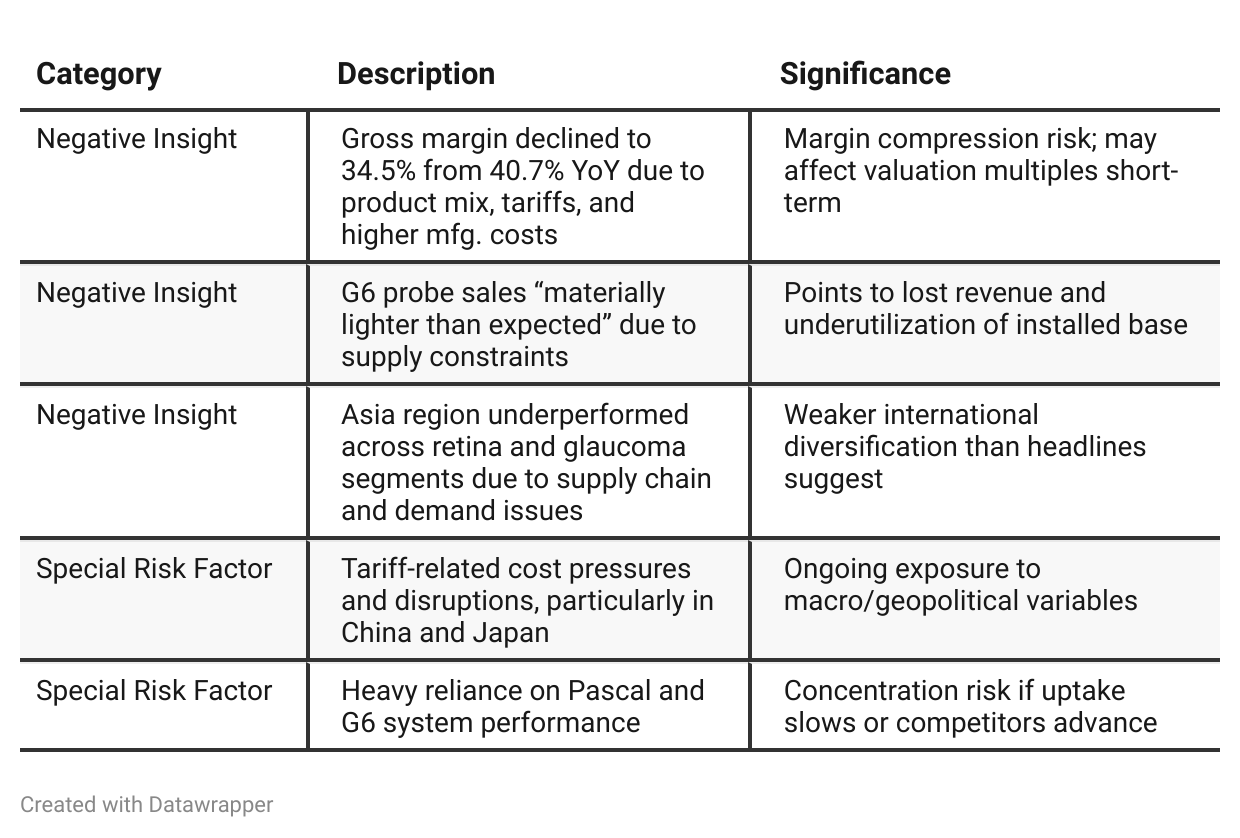

Negative Insights

Tariff Risk

Mentions & Impact:

Management explicitly noted tariff-related disruptions in Asia, particularly impacting Q2 orders and potential future quarters.

Tariffs contributed to margin compression, increasing manufacturing costs alongside inflation.

Mitigation Actions:

No direct mention of supply chain reorientation; however, negotiations with contract manufacturers and a facility relocation in 2026 suggest a medium-term shift to lower-cost structures.

Risks to Watch:

Potential for further strain in international sales if U.S.-China trade issues escalate.

Market share vulnerability if delays persist in Asia and Japan, particularly for Pascal and G6 systems.

Forward-Looking Commentary:

Management believes challenges are now “identified” and “mitigation plans” are in place, but timelines were vague.

Conclusion:

Tariffs remain a significant wildcard. Their influence on both costs and revenue timing could delay full financial recovery. Progress on supply diversification and localization strategies should be closely monitored.

Previous Earnings Call

Quarter-over-quarter comparison

IRIDEX entered 2025 in stabilization mode, focused on cutting costs and reversing EBITDA losses. Q1 marked its first adjusted EBITDA-positive quarter in recent history, boosted by stronger MP3 probe sales, cost discipline, and a $10M strategic infusion from Novel Inspiration.

By Q2, the tone shifted to confident execution, with three quarters of operating progress and a clear roadmap for continued margin and cost optimization—including relocation plans and supplier renegotiations. While Q2 gross margins slipped due to unfavorable mix and inflation-related costs, revenue growth was solid, and probe supply issues—though disruptive—were addressed quickly.

International expansion remains a core focus, but operational friction (e.g., MDR delays, pricing pressure) highlights the complexity of the global push. Overall, IRIDEX is emerging as a leaner, more targeted operator with a credible glidepath to profitability by year-end 2025.Year-over-year comparison

Between Q2 2024 and Q2 2025, IRIDEX’s narrative shifts from one of cautious stabilization under legacy leadership to structured transformation under new management. The 2024 call emphasized recovering probe sales and capital equipment trends, while reiterating dependence on unlocking shareholder value through a strategic review.

By 2025, with Patrick Mercer as CEO, the story pivots toward internal execution, operational discipline, and incremental margin improvement. The company positions itself as leaner, more efficient, and more in control of its own destiny—moving away from financial lifelines and toward operational self-reliance.

While the strategic review remains in the background, the 2025 call suggests that IRIDEX is no longer waiting for a transaction to define its future.

Final Takeaway

IRIDEX is in a restructuring phase, having made tangible progress on its cost structure, product efficiency, and adjusted EBITDA.

While U.S. sales—particularly Pascal and G6—show strength, international headwinds and gross margin deterioration pose near-term risk. Execution on cost containment, probe availability, and product utilization will be critical for sustained profitability.

Verdict: HOLD, with moderate upside if margin recovery and operational momentum continue through Q3–Q4.