Intellicheck, Inc. (NASDAQ: IDN) – Q2 2025 Earnings

Intellicheck, Inc. (NASDAQ: IDN) – Q2 2025 Earnings

Earnings Release Date: Aug. 12, 2025

Stock Price: $5.03

Market Cap: $99.6 million

Q2 2025 sales of $5.1 million vs $4.7 million in the prior year

Q2 2025 loss per share of ($0.01) vs ($0.01) in the prior year

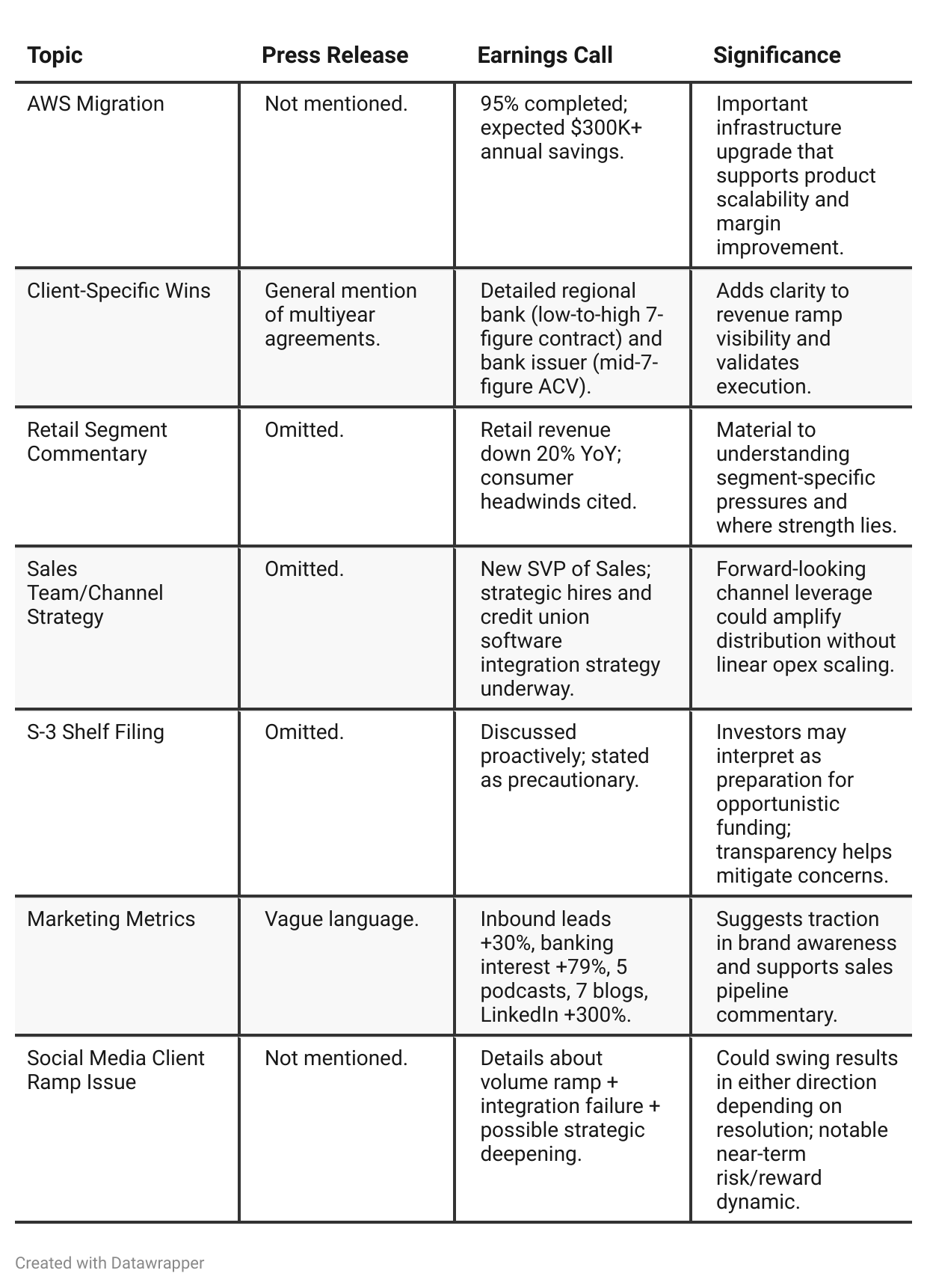

Press Release vs Call Transcript Comparison

While the press release provides a clean financial overview and headline achievements, the earnings call reveals deeper operational dynamics, including strategic pivots, technical setbacks, and more granular customer-level data. The absence of key developments—like the AWS migration, social media client issue, and evolving channel strategy—in the press release means investors relying solely on it might miss both upside optionality and downside risks. For a well-rounded investment thesis, the call provides essential forward-looking color that materially affects the near-term narrative and long-term trajectory.

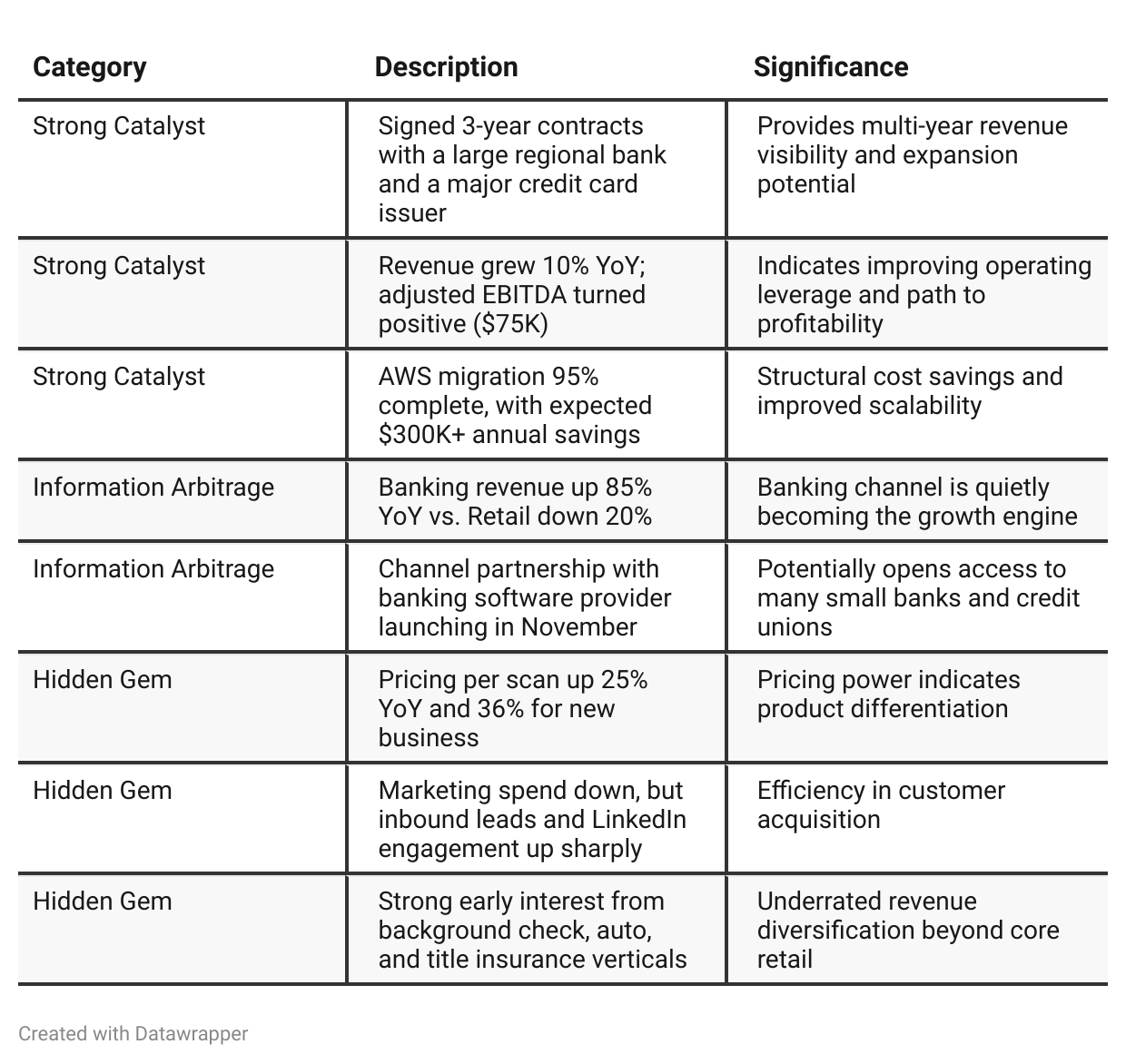

Positive Insights

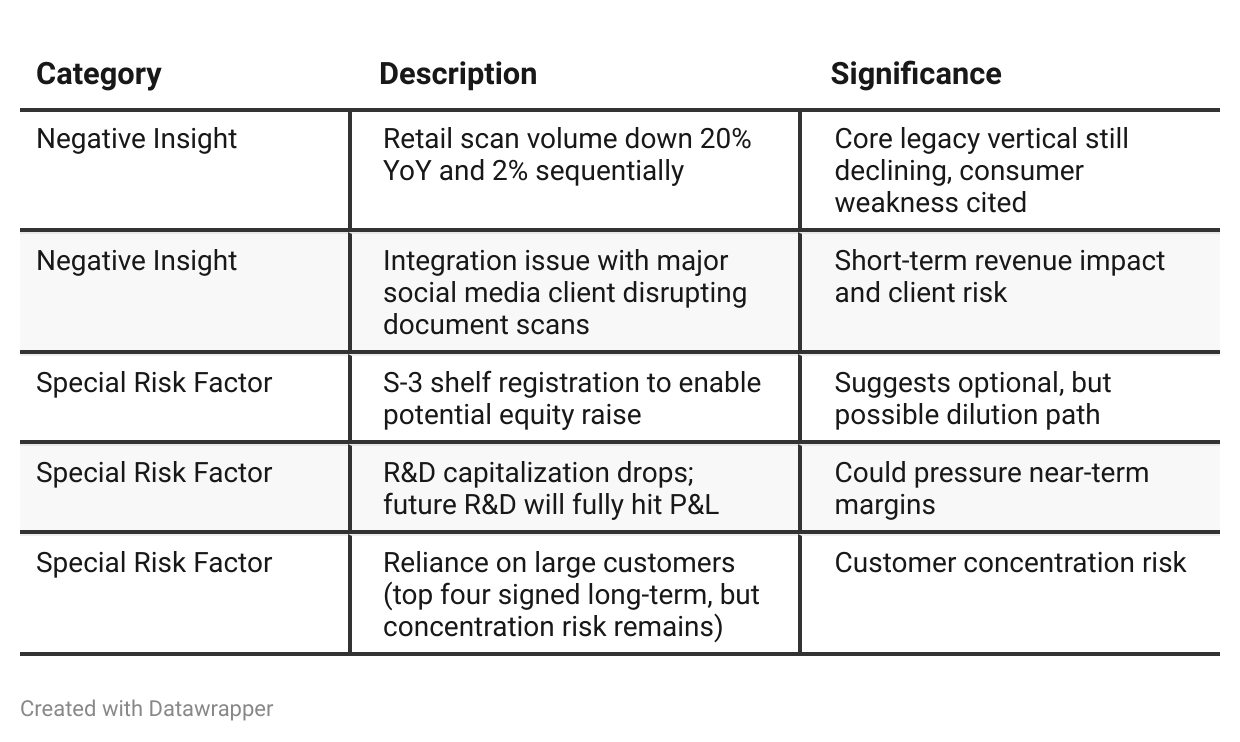

Negative Insights

Tariff Risk

Mentions of Tariffs:

– Retail segment volatility was attributed in part to “tariff concerns” alongside inflation and consumer confidence.

→ While not deeply explored, management acknowledged macro sensitivity of retail vertical to trade policies.

Mitigation Actions:

– No specific tariff-related actions (e.g., sourcing shifts or pricing adjustments) were discussed.

Impact:

– Tariffs are indirectly contributing to retail sector weakness, but company is already de-emphasizing this vertical in favor of more resilient banking and SaaS clients.

Forward-Looking Statements:

– No projections tied to tariff shifts; strategic pivot toward less tariff-sensitive markets underway.

Previous Earnings Call

Quarter-over-quarter comparison

Intellicheck’s Q1 call was framed as a turning point—refuting the “old Intellicheck” label and laying the groundwork for a diversified, modern SaaS identity platform. Q2 built on that foundation with clear proof points: major contract wins, expanded client relationships, successful AWS migration, and growing traction in high-value verticals.

The social media hiccup was a minor setback, but overall, the company’s messaging shifted from “redefining perception” to “executing against plan.”

The narrative now emphasizes predictability, multi-vertical opportunity, and operational discipline, supported by clear financial progress and strategic partnerships.Year-over-year comparison

Between Q2 2024 and Q2 2025, Intellicheck’s narrative evolved from one of defensive repositioning to execution-led expansion. In 2024, management was trying to offset serious declines in its core retail vertical through diversification and internal restructuring.

One year later, the company is benefiting from those moves—landing major banks, signing multi-year SaaS contracts, growing new verticals, and launching high-leverage marketing campaigns.

The tone is more forward-looking and metrics-backed, signaling that Intellicheck has transitioned from survival mode to strategic growth mode.

Final Takeaway

Intellicheck is in a scaling phase, leaning into banking and SaaS opportunities while reducing dependence on retail.

Long-term contract wins, pricing power, and cost reduction via AWS migration support the bull case. Yet, execution risk remains on ramping new verticals and resolving the social media client issue. Retail softness and potential near-term margin pressure due to R&D hitting the P&L also warrant caution.

Verdict: HOLD, with upside if the social media integration is resolved and banking channel continues to expand.