Hudson Global, Inc. (NASDAQ: HSON) – Q2 2025 Earnings

Hudson Global, Inc. (NASDAQ: HSON) – Q2 2025 Earnings

Earnings Release Date: Aug. 8, 2025

Stock Price: $9.12

Market Cap: $27.3 million

Q2 2025 sales of $35.5 million vs $35.7 million in the prior year

Q2 2025 EPS of $0.12 vs $0.04 in the prior year

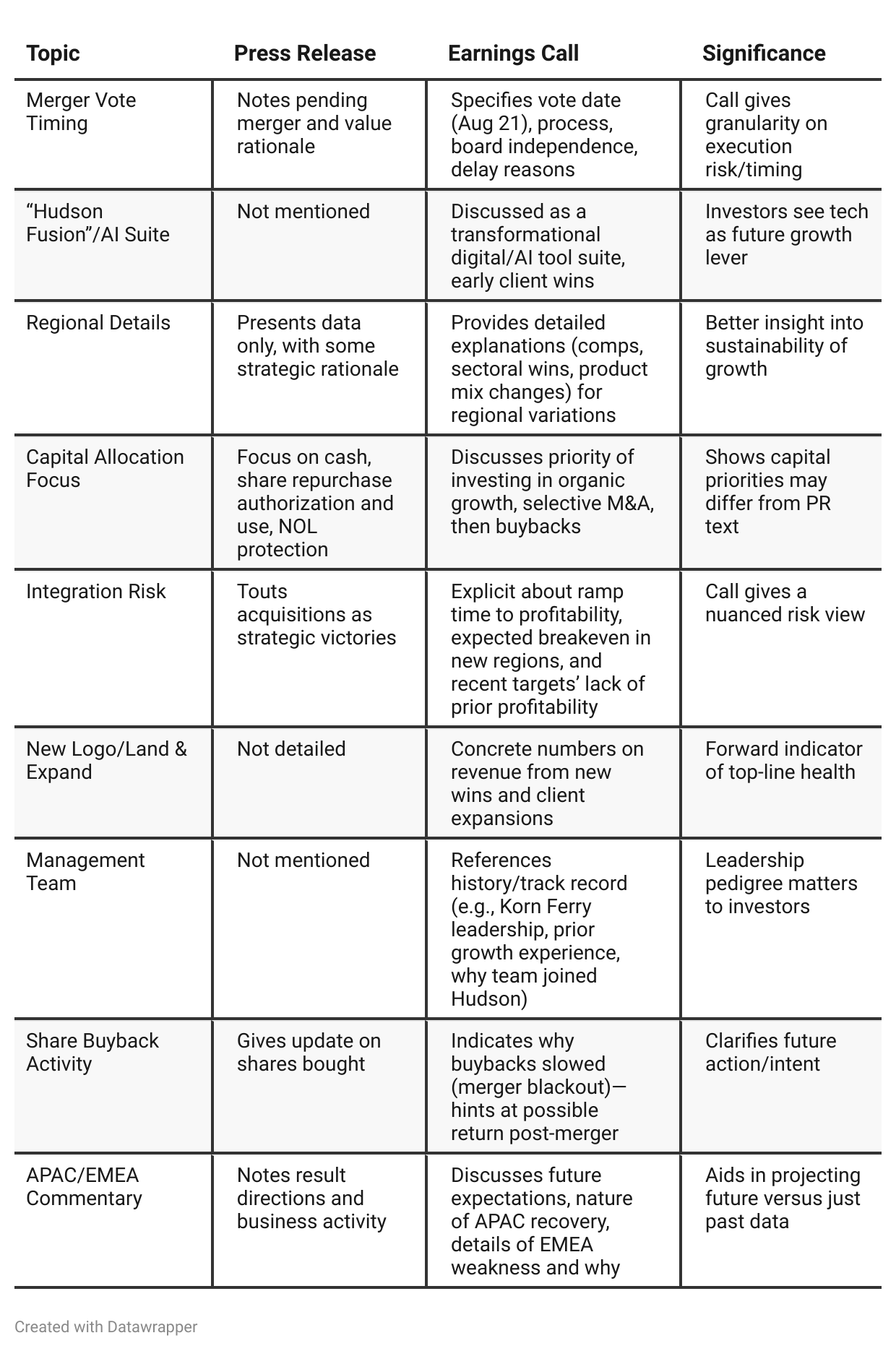

Press Release vs Call Transcript Comparison

Tone: Press release is fact-based and optimistic, with little emphasis on near-term challenges; earnings call gives a more realistic, nuanced context and forward-looking color.

Share Repurchases: Ongoing but paused due to merger process; expected to resume, giving a potential share price floor.

M&A Philosophy: Preference for organic growth and “team hires” over large M&A, but will use acquisitions opportunistically to plug geographic and service gaps.

NOL Tax Shield: Major NOL asset could offset profits, enhancing future earnings quality if company turns sustainably profitable post-merger.

Client Diversification: Discusses expansion of both global footprint and services (from “geographic holes” to digital/brand/exec search), hinting at both growth opportunity and execution complexity.

Long-term Targets: Management seems confident in high teens growth rates post-merger, regardless of macro improvement, based on new business and strategy.

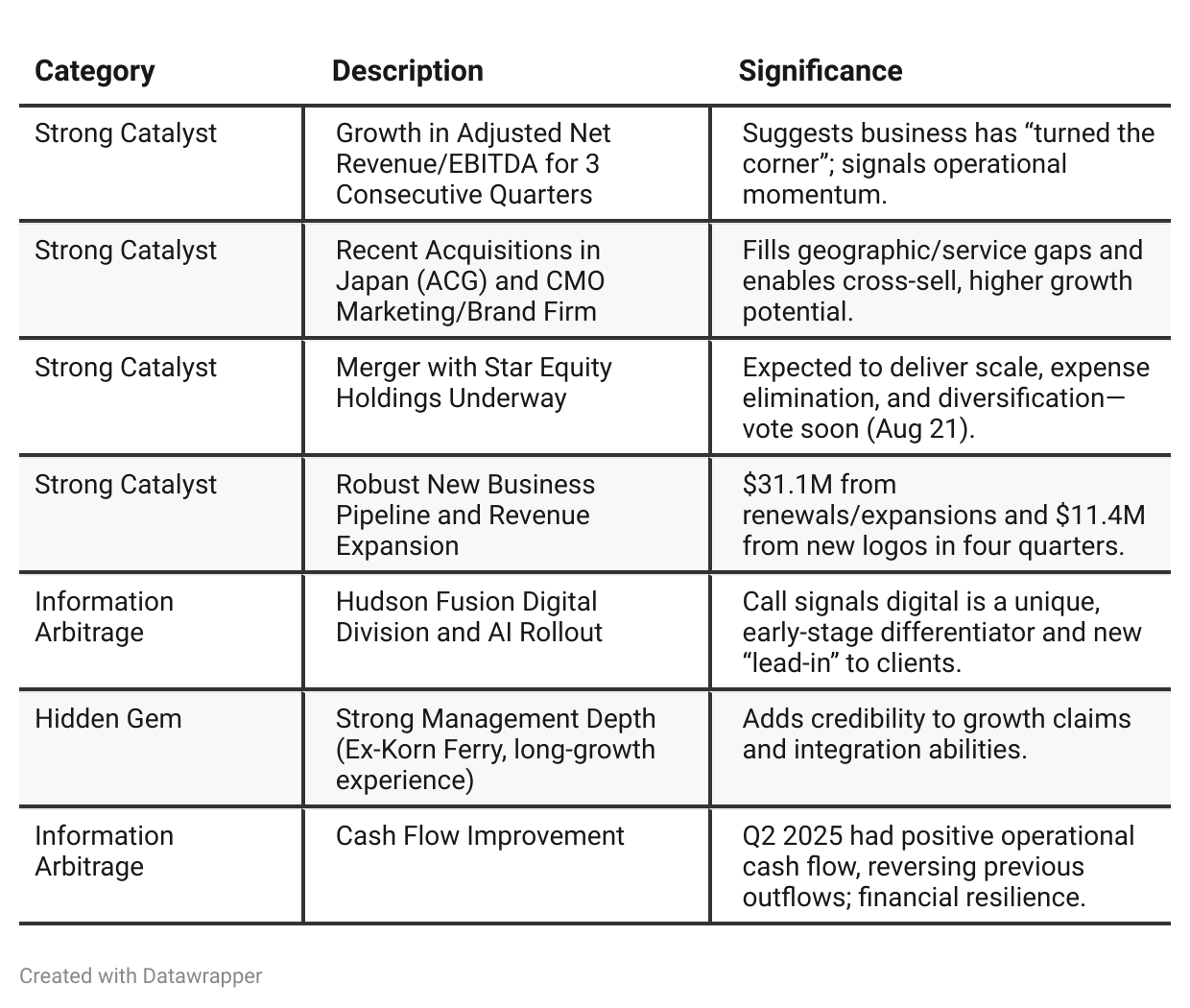

Positive Insights

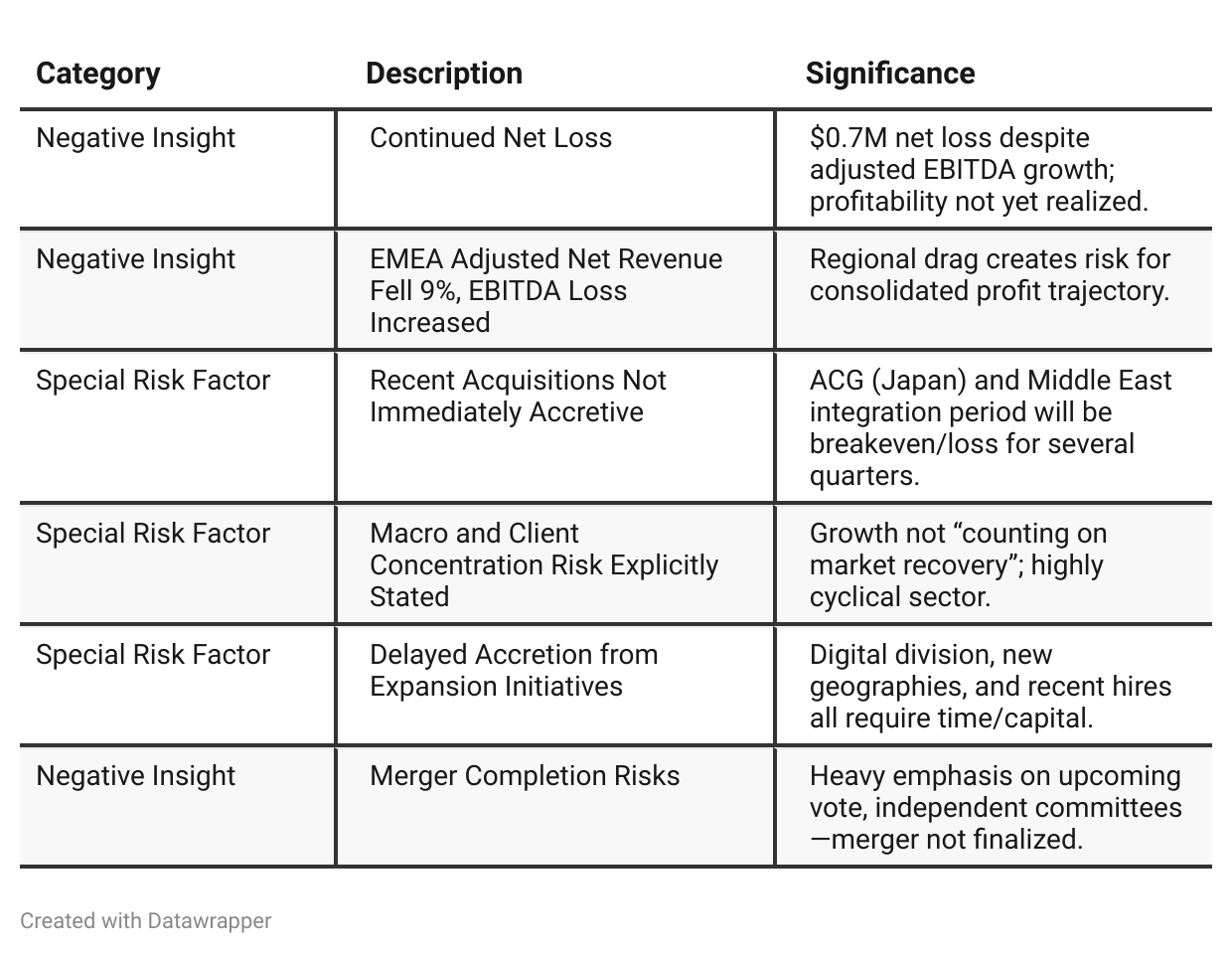

Negative Insights

Tariff Risk

No direct or indirect mentions of U.S. tariffs, trade policies, or international trade risk (including China or U.S. import/export) appeared in the Q2 2025 earnings call transcript.

No discussion regarding the impact of tariffs on revenue, supply chain, or profitability was surfaced.

No actions described relating to tariff mitigation (e.g., supply chain shift, contract renegotiation, price adjustments).

Sentiment Analysis

The overall sentiment toward Hudson Global (HSON) is bullish. Investors and commentators express excitement about the completed merger with Star Equity Holdings, highlight the company's entry into Japan and new board appointments, and mention insider and institutional buying. Some see HSON as an under-the-radar microcap with high breakout/reversal potential due to its low float, high insider ownership, and recent corporate actions, all suggesting optimism about future growth and profitability.

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Earlier Call (Q1 2025): Hudson Global described itself as a company in transition—recovering from a tough external environment, rebuilding after underinvestment, and focusing on the foundational steps of leadership hiring, digitization, and plugging service gaps. Management emphasized the importance of stabilizing results, assembling the right team, and preparing the company to capitalize when market conditions inevitably improve.Latest Call (Q2 2025): The narrative advances decisively. Hudson now presents itself as past the inflection point—delivering multiple quarters of improving operational results, already commercializing its digital investment, securing substantial new business, and executing on strategic deals. The upcoming Star Equity merger represents a credible next phase—moving from foundational work to unlocking scale and diversification. Management’s tone is more confident, shifting from hope to delivery.

Year-over-year comparison

Q2 2024 → Q2 2025: Hudson Global’s narrative transitions from defense to offense. In 2024, the company was weathering a downturn, with client hesitancy, shrinking deal scopes, and a need to tighten costs to defend the bottom line. Progress was centered on rebuilding relationships and moving quickly to survive.

By Q2 2025, the company presents a story of renewed operational momentum and execution: consecutive growth quarters, new regional and digital initiatives now driving commercial wins, and a potentially transformational merger in the works. Management confidence is higher, the focus is on scaling ambitious strategies, and the language shifts from “survive and optimize” to “grow and lead.”

Final Takeaway

Hudson Global is in a transformation and expansion phase, leveraging recent acquisitions, a robust digital offering, and a pending merger to ignite growth. The company has returned to steady adjusted net revenue/EBITDA gains and is building a more diversified geographic and product base. However, continued net losses, execution risk on new initiatives, and a not-yet-certain merger present clear risks. Execution on digital rollout, EMEA turnaround, and merger completion will be critical for future upside. Verdict: HOLD, with strong potential for upgrade upon confirmed progress.