Harrow, Inc. (NASDAQ: HROW) – Q3 2025 Earnings

Harrow, Inc. (NASDAQ: HROW) – Q3 2025 Earnings

Press release and earnings call link

Earnings Release Date: Nov. 10, 2025

Stock Price: $33.93

Market Cap: $1248.3 million

Q3 2025 sales of $71.6 million vs $49.3 million in the prior year

Q3 2025 EPS of $0.03 vs ($0.12) in the prior year

Overview: Harrow (Nasdaq: HROW) provides ophthalmic (eye-care) therapeutics across branded, generics, compounded and (future) biosimilars in North America. Products target dry eye disease, retina disorders, surgical settings, glaucoma and ocular surface disease.

Revenue drivers (what they do): Near-term growth is concentrated in VEVYE (cyclosporine for dry eye) and IHEEZO (ocular anesthetic for procedures), with TRIESENCE (triamcinolone acetonide) re-accelerating via an expanded indication push (ocular inflammation).

Main customer/end markets: U.S. eye-care ecosystem (ophthalmologists, retina specialists, surgery centers, optometrists) managing front- and back-of-eye conditions.

Positioning: Emerging platform player aiming to be a “next great U.S. ophthalmic company” with a broad portfolio and access programs; management emphasizes scalable commercial infrastructure.

Recent financial trajectory: Q3’25 revenue $71.6m (+45% y/y); GAAP net income $1.0m; Adj. EBITDA $22.7m; cash $74.3m.

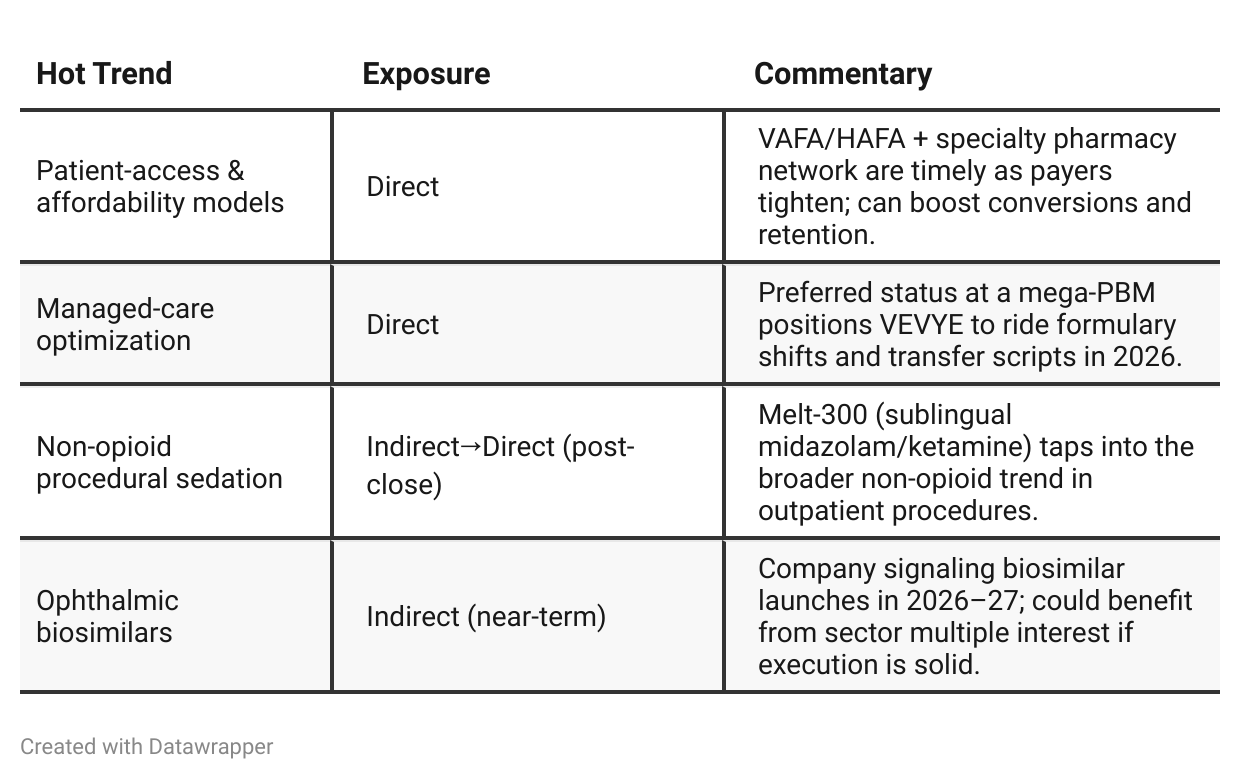

Key near-term themes: Broad payer coverage wins for VEVYE effective Jan 1, 2026 (PBM = pharmacy benefit manager), expansion of access programs (VAFA/HAFA), and strategic pipeline/M&A (Melt Pharmaceuticals).

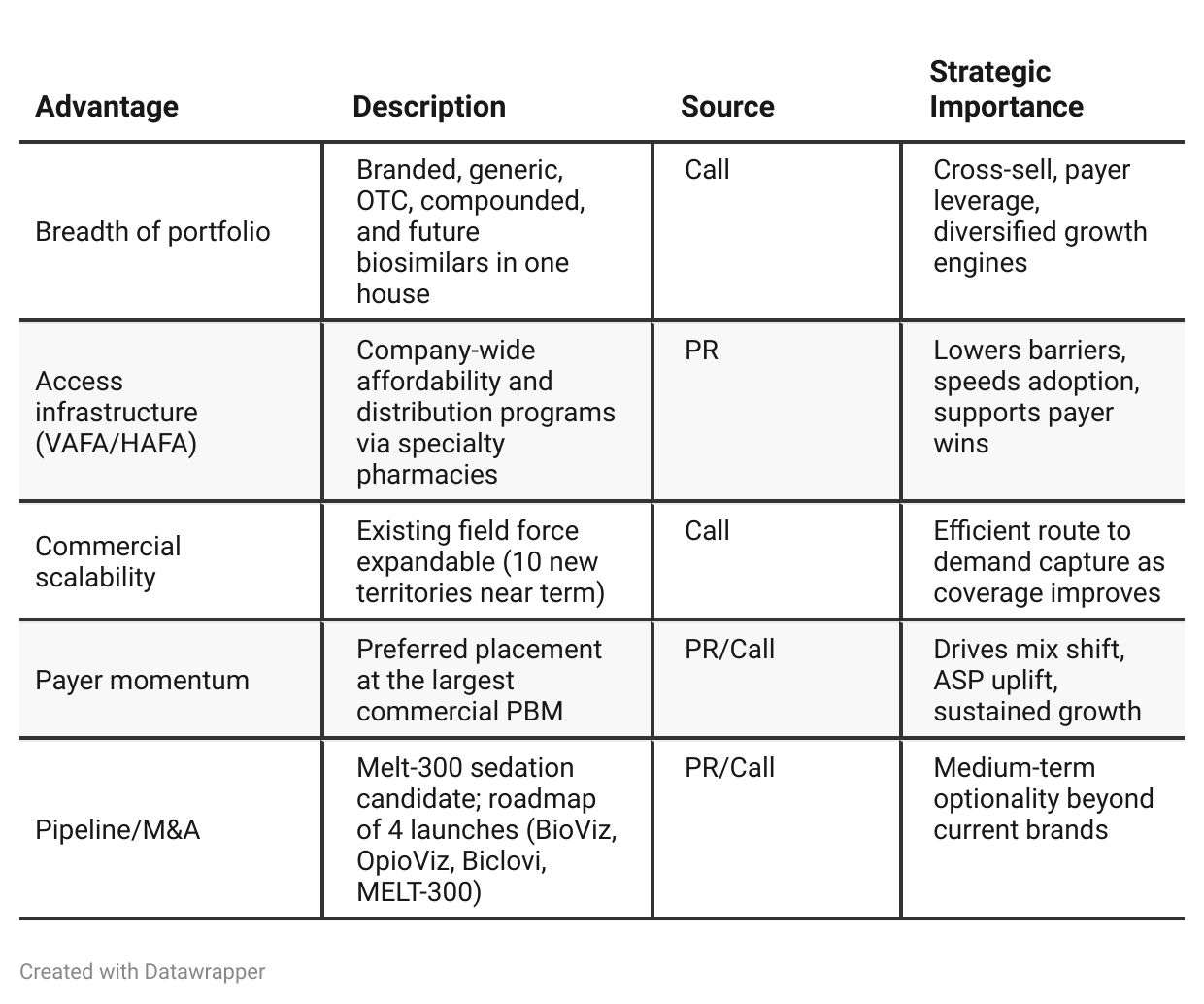

Competitive Advantage Insights

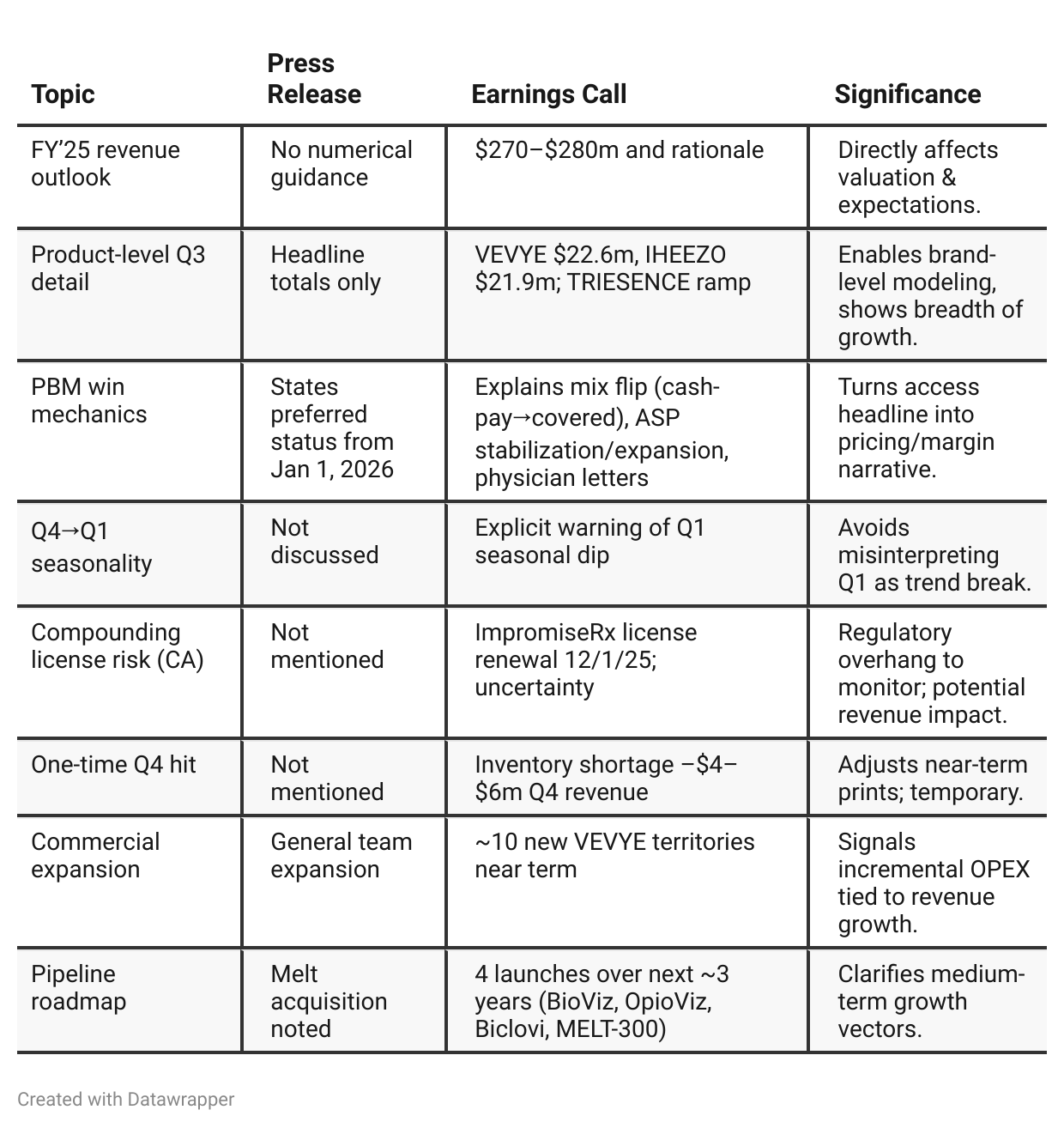

Press Release vs Call Transcript Comparison

The PR gives confirmation of growth and strategic highlights (coverage, access programs, Melt). The call supplies the how/when that moves models: guidance, seasonal cadence, brand splits, and conversion math from PBM wins. Together, they imply 2026 could see unit growth + ASP uplift in VEVYE—i.e., volume and price working at once.

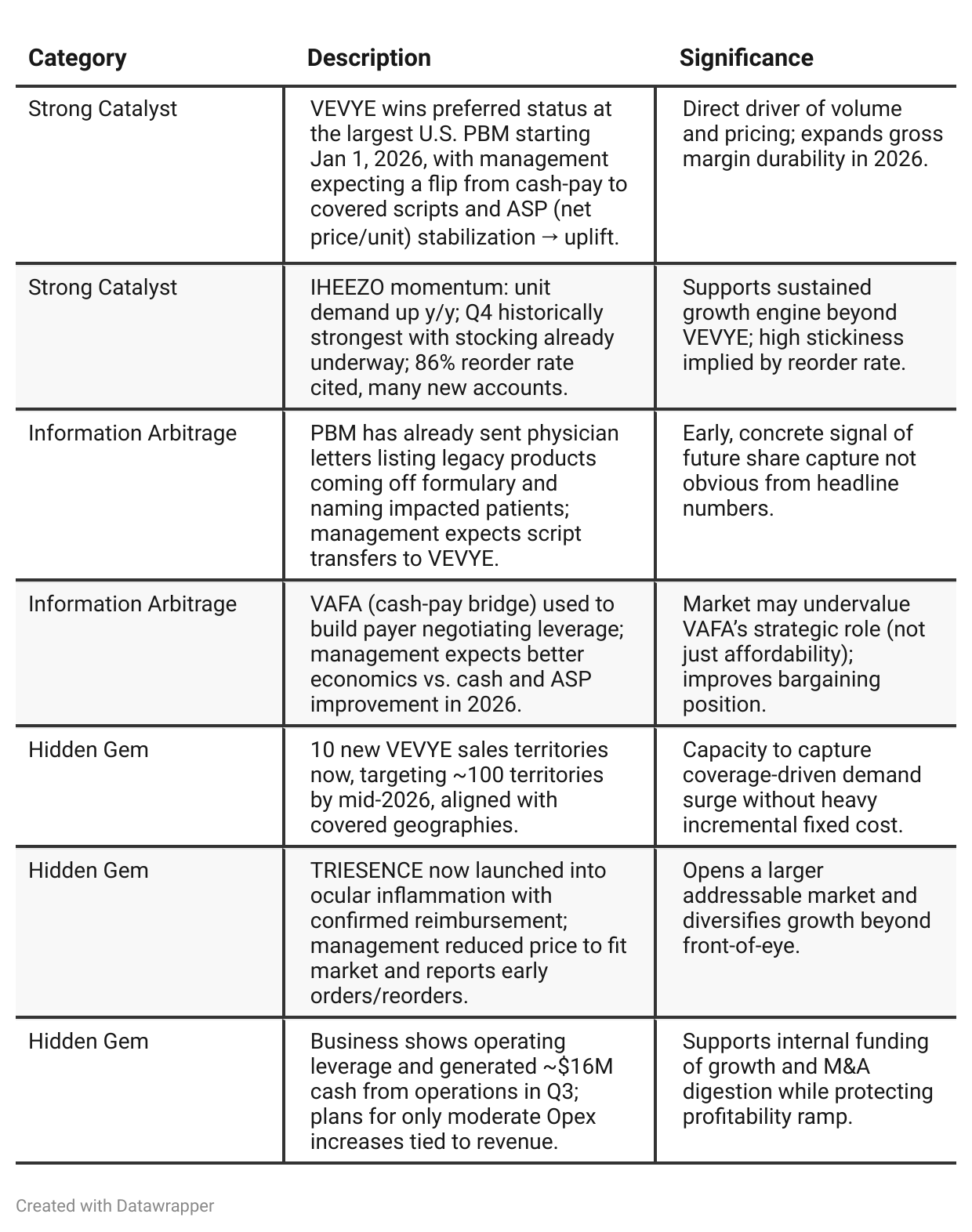

Positive Insights

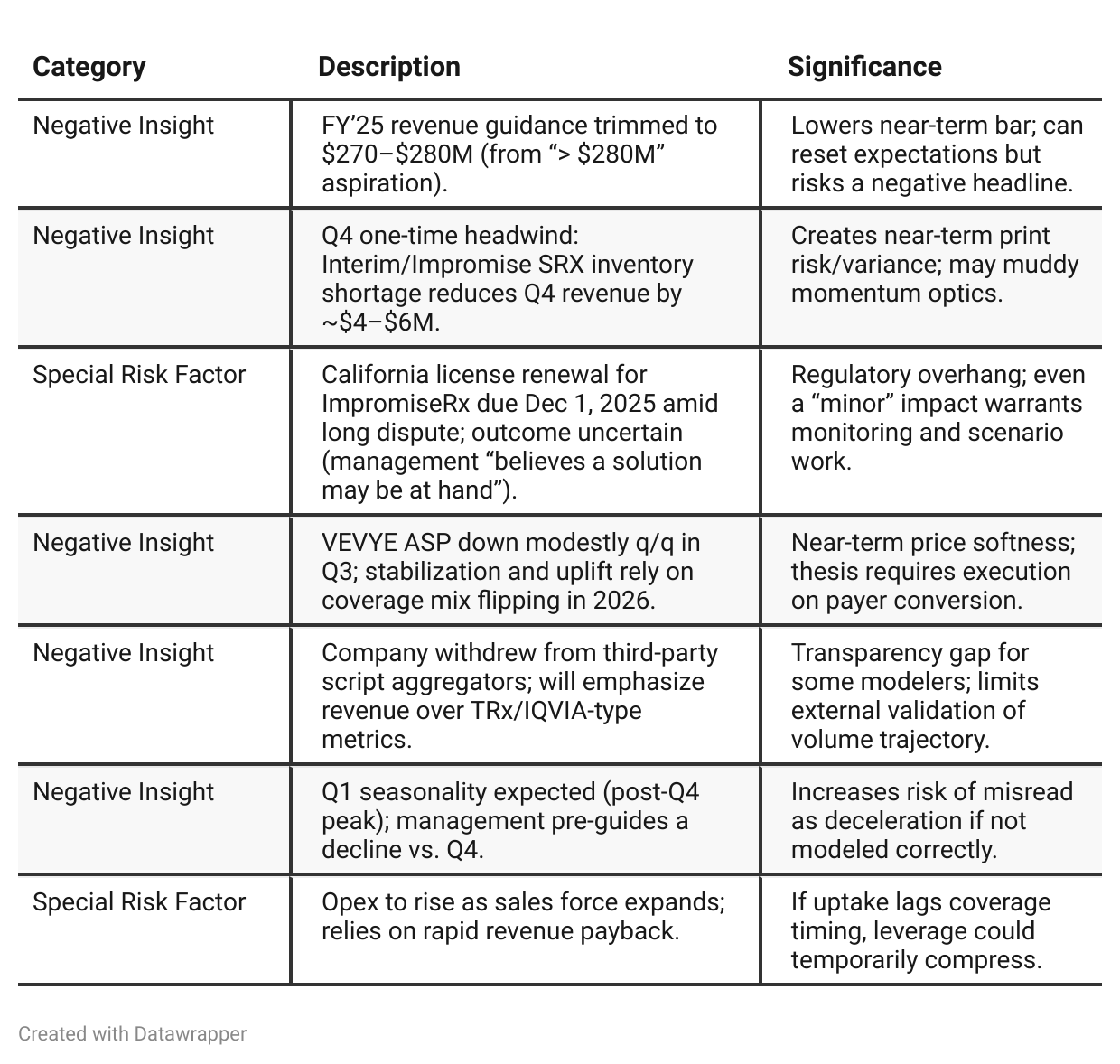

Negative Insights

Investor Underappreciation Signals

✅ VEVYE Coverage Win — Transformative reimbursement shift taking effect Jan 1, 2026. Investors may be overlooking how Harrow’s deal with the largest U.S. PBM immediately flips most VEVYE prescriptions from cash-pay to covered, lifting ASP and margins; as doctors receive formal plan-change notices, sentiment should shift from cautious to bullish once early Q1 data confirm the pricing uptick.

✅ TriEssence Relaunch — Entry into ocular inflammation unlocks the brand’s largest market. With confirmed reimbursement, strong surgeon enthusiasm, and a 53% new-customer mix in Q3, this expansion could sharply accelerate growth, yet many models still assume flat specialty revenue; evidence of sustained reorder momentum in Q4 should correct that gap.

✅ Operating Leverage Inflection — SG&A growth now trailing revenue growth. Core infrastructure investments are largely complete, so incremental sales now convert efficiently to EBITDA; the Street may not be pricing in how quickly cash generation can compound as commercial hires become revenue accretive within one quarter.

✅ Rare & Specialty Portfolio Rebuild — New leadership and “Access for All” could revive a $10M/quarter business. This segment represents less than 1% of addressable volume today, but management is re-staffing and reactivating physician engagement; early traction in Q4 would signal a return to growth that consensus models likely omit.

✅ Melt Pharmaceuticals Acquisition — Non-opioid sedation platform adds an overlooked optionality layer. The MELT-300 asset offers a scalable entry into procedural anesthesia without IV or opioid risk, a narrative underweighted by ophthalmic-focused investors but likely to attract attention as clinical milestones or hospital partnerships emerge.

✅ VEVYE Sales Force Expansion — Ten new territories ready for coverage-aligned rollout. Management’s decision to open new territories ahead of 2026 payer coverage suggests confidence in ROI from each incremental rep; investors may underappreciate how this geographic leverage can accelerate market share capture once formulary access broadens.

✅ HAFA Program Expansion — Extending affordability model across the full portfolio. The new Harrow Access for All initiative goes beyond VEVYE, reducing friction and boosting patient retention for multiple brands; consensus likely treats this as a marketing cost rather than a structural volume driver, a view that will shift as refill rates improve in Q4–Q1.

Tariff Risk

No explicit mentions of U.S. tariffs or trade policy impacts in the call. There’s no discussion of tariff-driven COGS pressure, supply chain rerouting, pricing actions, or market-share shifts attributable to tariffs. Conclusion: Tariff risk not addressed; investors should assume neutral tariff exposure until filings or management commentary indicate otherwise.

Hot Stock Trends Analysis

Previous Earnings Call

Quarter-over-quarter comparison (Previous Analysis)

Q2 2025:

Harrow’s narrative centered on momentum and market entry. Management emphasized rapid growth across VEVYE, IHEEZO, and TRIESENCE, supported by M&A-driven pipeline expansion (Biclovi, Samsung biosimilars). The story was aspirational: Harrow as the next great U.S. ophthalmic company building scalable infrastructure and chasing share gains. Risks were de-emphasized; tone was almost promotional.Q3 2025:

The company’s narrative matured into one of execution discipline and structural validation. Harrow began to show proof that earlier investments were translating into stable margins, repeatable revenues, and cash generation. The PBM coverage win gives tangible proof of payer traction, while leadership additions bring operational credibility. Management introduced risk transparency (license renewal, inventory issue) and more specific, data-backed commentary.Year-over-year comparison

Q3’24 → “Proving product-market fit.” Management highlights rapid VEVYE adoption/refills, leans into retina pivot for IHEEZO, and relaunches TRIESENCE with reimbursement clarity; tone is aspirational and momentum-centric.

Q3’25 → “Converting access into durable economics.” Management codifies guidance, surfaces risks, quantifies brand revenue, and details the PBM preferred win that should flip mix and lift ASP in 2026; commercial leadership and territory plans are aligned to capture that conversion.

Final Takeaway

Harrow is in a growth phase, focusing on coverage-driven VEVYE expansion, IHEEZO account growth, and TRIESENCE’s ocular-inflammation launch, with MELT adding optionality. While Q4 one-time and Q1 seasonality may cloud near-term optics, the Jan 1, 2026 PBM catalyst sets up volume + ASP expansion. Execution on coverage→conversion, sales-force scale-up, and license resolution will be critical. Verdict: BUY, with upside hinging on proof of conversion and stable product economics through 1H’26.