Harrow, Inc. (NASDAQ: HROW) – Q1 2025 Earnings

Harrow, Inc. (NASDAQ: HROW) – Q1 2025 Earnings

Earnings Release Date: May 8, 2025

Stock Price: $24.59

Market Cap: $880.5 million

Q1 2025 sales of $47.8 million vs $34.6 million in the prior year

Q1 2025 EPS of -$0.50 vs -$0.38 in the prior year

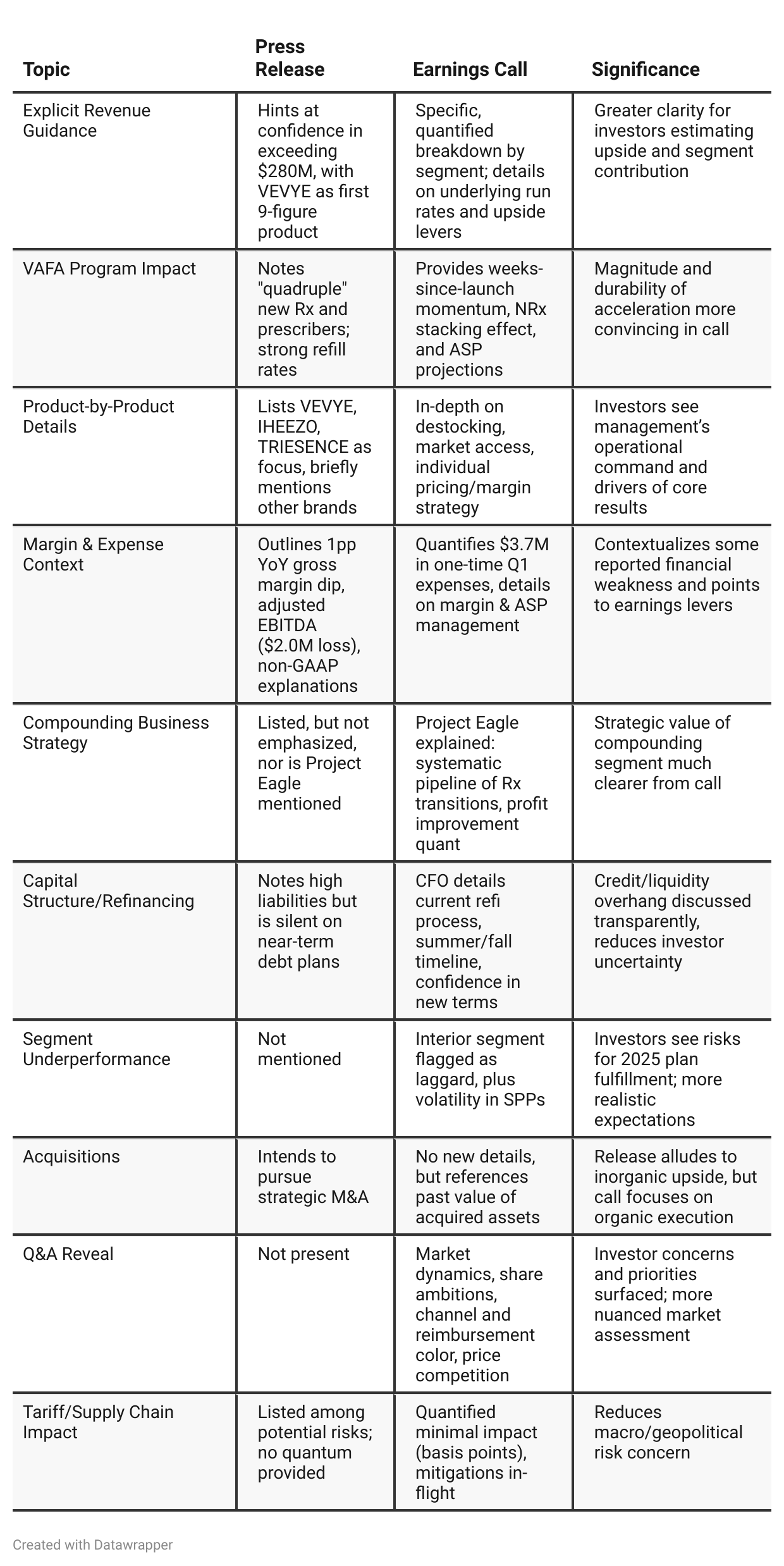

Press Release vs Call Transcript Comparison

Tone & Openness: The call features candid dialogue about both strengths and weaknesses, offering a more nuanced (and investable) view than the press release. The CEO’s “never satisfied” theme and willingness to call out what’s not working will reassure investors focused on execution risk.

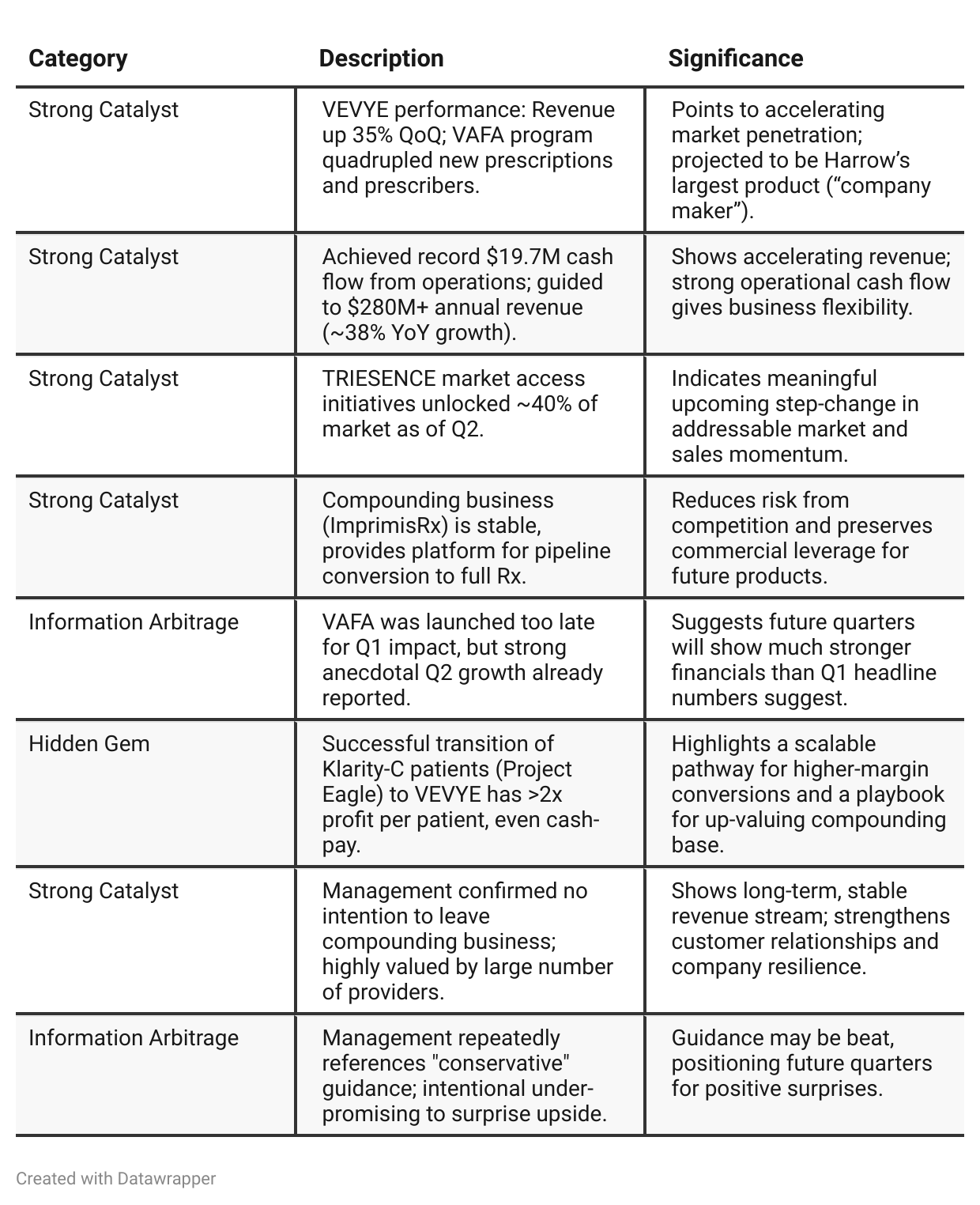

Product Transition as a Playbook: The detail around moving Klarity-C patients to VEVYE hints at a repeatable strategy for migrating compounded users to full Rx products, with clear margin improvement.

Profitability Path: While headline losses are significant, both documents make clear that the business is in investment mode with several inflection points on visibility for margin expansion (through scale, margin management, and one-off items dropping out).

Market Share Ambitions: The call outlines leadership aspirations in dry eye and anti-inflammatory categories, setting up potential for future positive market-share surprises.

Transparency on Risks: The earnings call uniquely tackles critical investor questions (debt, margin swings, reimbursement challenges, etc.) head-on, positioning Harrow as unusually transparent in its communications.

Strategic Leverage of Compounding: Whereas the press release downplays this area, the call describes a flywheel effect where compounding acts as a launchpad for the Rx pipeline and commercial leverage.

Positive Insights

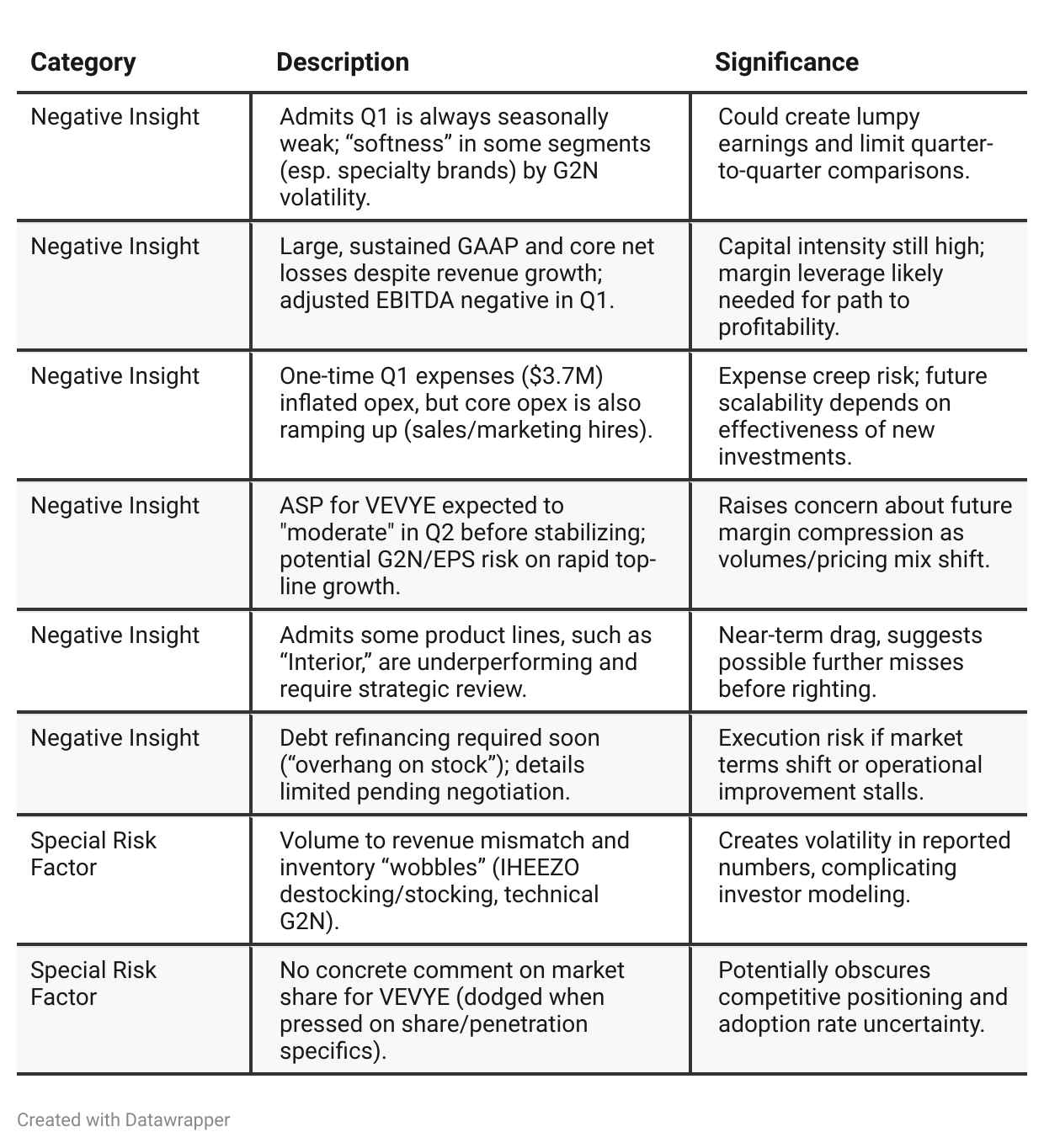

Negative Insights

Tariff Risks

Tariff impacts on Harrow are currently negligible—only ~50 basis points in gross margins, per CFO/CEO.

Noted that even sharply higher tariffs on key products (IHEEZO is manufactured ex-US) would only modestly impact margin; current sourcing and cost structure are robust against headline tariff changes.

The company is also working to localize its supply chain, bringing more excipients/APIs from domestic sources, which will potentially decrease exposure further.

No mention of tariffs as a material risk to competitive advantage, market share, or innovation in current operations.

No forward-looking “tariff risk” flagged to future guidance; management's tone is measured and confident.

Previous Analysis

Quarter-over-quarter comparison (Previous Analysis)

At the end of 2024, Harrow, Inc. presented itself as a company in the midst of a breakthrough—riding the momentum of record revenue and margin expansion, rolling out bold new access strategies (VAFA), and celebrating operational wins. The focus was on capturing market share quickly and driving adoption with an energized commercial team.

Fast-forward to Q1 2025, the company’s narrative has matured. While still optimistic about long-term potential, management is more transparent about near-term challenges, operational headwinds, and the rigor required for sustained growth. The messaging now emphasizes a “blocking and tackling” approach: executing on transformative market access programs, monitoring real-world traction, and proactively addressing segment underperformance while keeping a close eye on margin discipline and funding needs. The company’s story has shifted from initial exuberance and disruption to disciplined execution, measured optimism, and a recognition that ongoing success will demand continuous improvement and adaptability.

Year-over-year comparison

In early 2024, Harrow’s narrative was one of resilience and expansion—the company was bouncing back from industry-wide disruptions, successfully launching new products, hiring proven commercial leaders, and celebrating surging refill rates, coverage wins, and expanding customer relationships. Optimism about the future was high, with little focus on operational or financial risk.

By Q1 2025, the narrative matured significantly. Management still expresses confidence but tempers this with candor about seasonal headwinds, technical challenges in revenue recognition, margin volatility, and the need to “do better” in weaker segments. The focus has shifted to disciplined execution, data-driven product launches, and maximizing the impact of access initiatives such as VAFA. Debt and refinancing needs are discussed transparently as critical inputs to guidance certainty. The story has evolved from one of high-growth enthusiasm to one of scaling the business responsibly, managing complex externalities, and laying the groundwork for sustainable, margin-expanding long-term growth.

Final Takeaway

Harrow, Inc. is in a growth phase, leveraging its core ophthalmic drug suite and a unique compounding-to-branded migration model. While near-term catalysts—from the VEVYE VAFA program and TRIESENCE market access upgrades—are strong, bottom-line losses, debt refinancing needs, and some execution volatility create a wait-and-see scenario. Execution on migration metrics, successful debt refinancing, and margin stabilization will be critical to unlocking further upside. Verdict: Hold—with positive bias, as delivery on key milestones could quickly alter the risk/reward profile.