Hooker Furnishings Corporation (NASDAQ: HOFT) – Q2 2026 Earnings

Hooker Furnishings Corporation (NASDAQ: HOFT) – Q2 2026 Earnings

Earnings Release Date: Sep. 11, 2025

Stock Price: $10.98

Market Cap: $116.5 million

Q2 2026 sales of $82.1 million vs $95.1 million in the prior year

Q2 2026 EPS of ($0.31) vs ($0.19) in the prior year

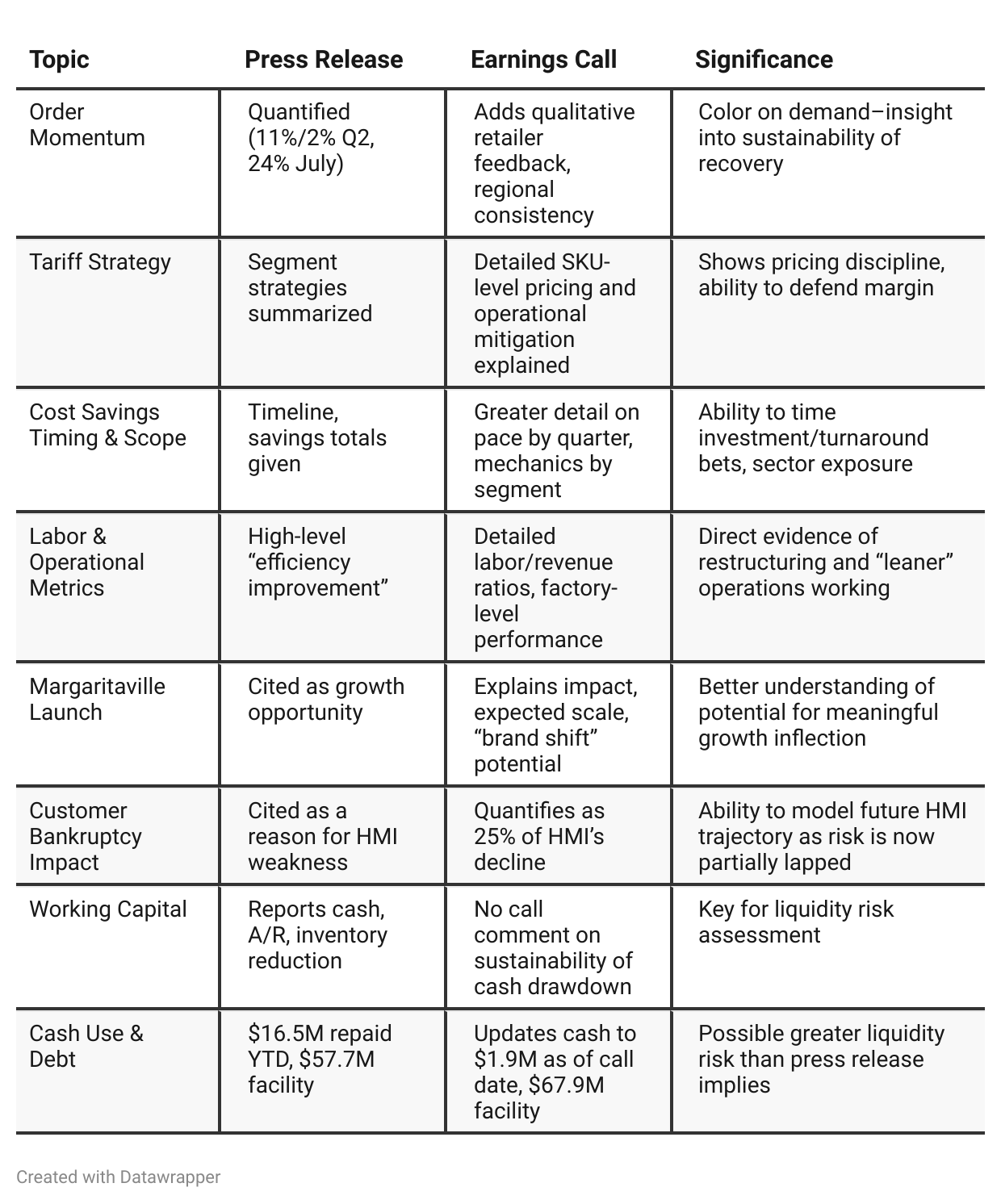

Press Release vs Call Transcript Comparison

Segment Divergence is a Key Story: While Hooker Branded and Domestic show order and operational improvements, HMI remains a material risk and drag; call gives more sense of path out via cost cuts and demand stabilization.

Sustainability of Profitability: Both documents tout path to profitability at today’s revenue; call gives more conviction (and caveats, e.g., “barring additional disruptive events”).

Catalytic Events are Near-Term: Major cost savings and expense structure overhaul mostly effective by end of Q3; Margaritaville launch in Q4; next 2 quarters are pivotal for sentiment reset.

Liquidity and Cash Burn: Press release details the reliance on inventory/workdown for cash generation. Call highlights capital allocation continuing but doesn’t address how sustainable non-earnings cash generation is.

Tariff and Supply Chain Execution is an X-Factor: New tariffs material, but more importantly, variable by segment. Strong execution here will differentiate the outcome.

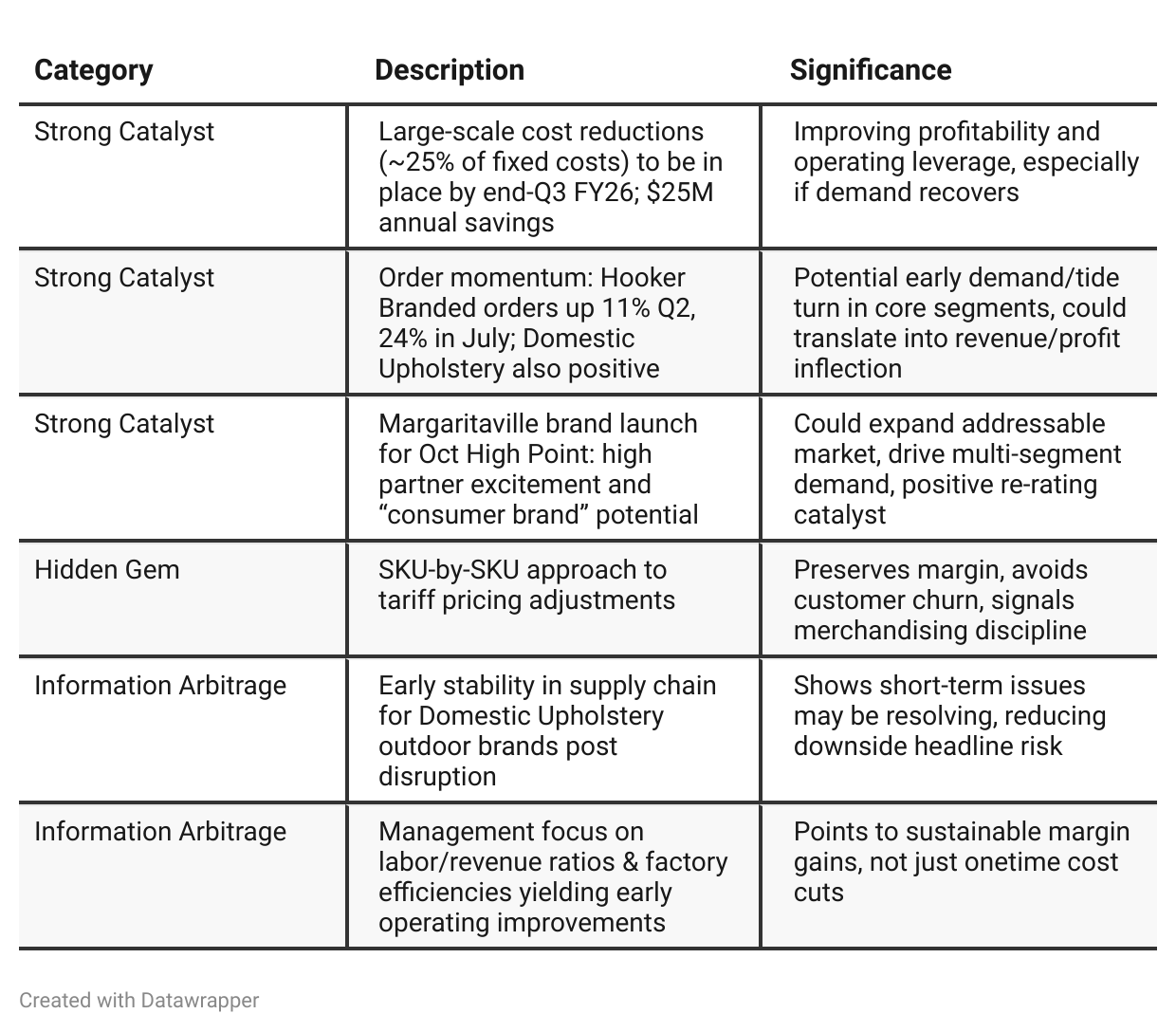

Positive Insights

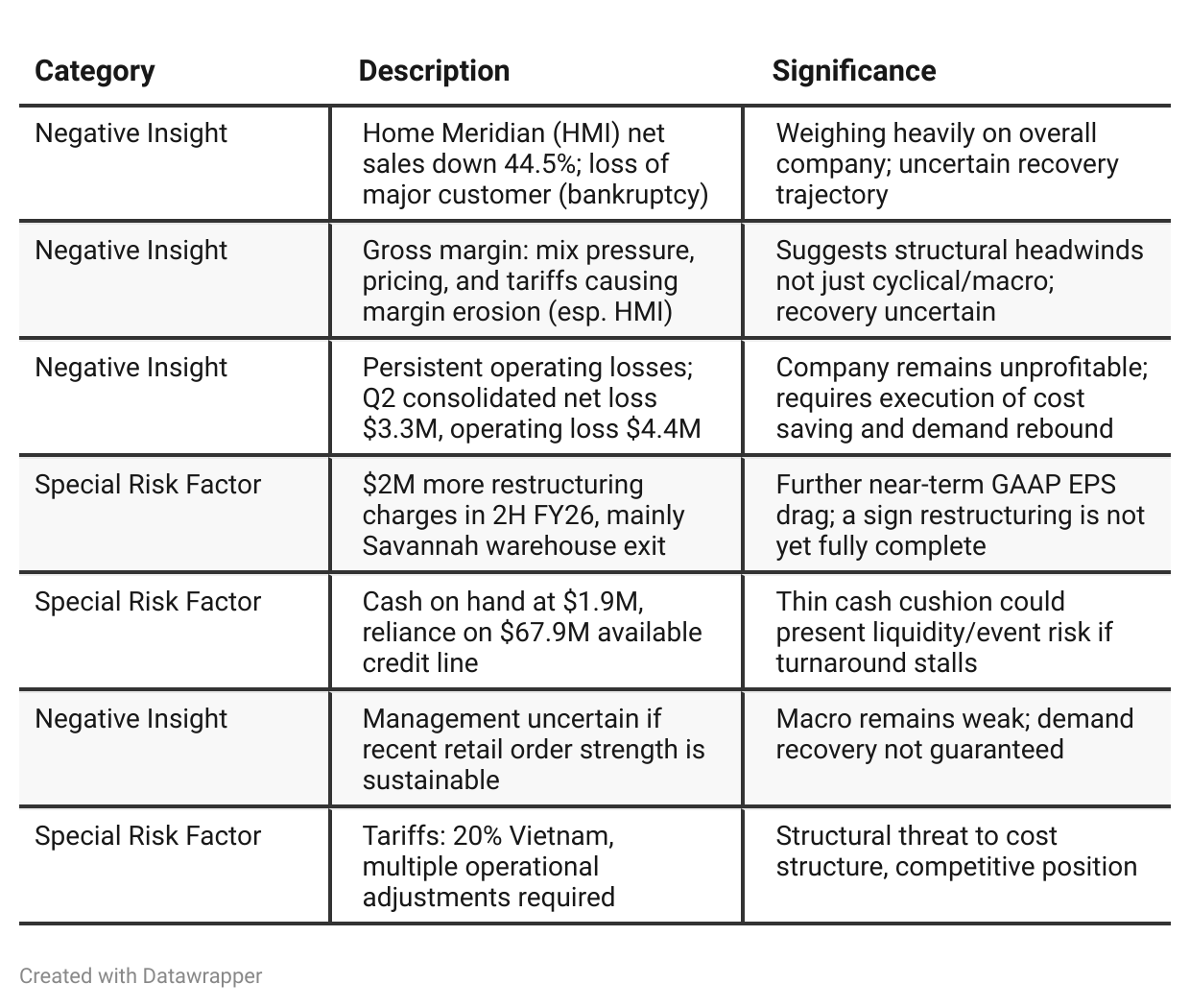

Negative Insights

Tariff Risk

Management devoted meaningful commentary to US tariff risks:

20% Tariff on Vietnam imports (effective 8/1/2025):

Impact: Raises costs for furniture and component imports. Particularly disrupts HMI and Domestic Upholstery supply chains.

Mitigation:

Domestic Upholstery: Incremental measures (e.g., new sourcing for fabrics/components).

Hooker Branded: SKU-by-SKU pricing adjustment instead of broad price hikes, aiming to protect merchandising edge and customer relationships.

HMI: Focus on mitigating value perception in highly price-sensitive channels, balancing product flow and margin.

Strategic Response: Management indicates no major customer attrition or margin hit yet, and believes mitigation is “in hand,” but acknowledges market is volatile and future adjustments may be needed.

Forward Look: If tariffs rise further, or if mitigation lags, margin or share loss risks could re-emerge, especially for price-sensitive segments.

Competitive Impact: Not explicitly discussed, but tiered mitigation suggests risk of competitive squeeze for HMI and potential pricing power at core brands.

Summary: Tariffs remain a central, ongoing threat to both cost structure and pricing flexibility. Management’s granular strategy (SKU-level) is smart, but long-term competitive pressure and the potential for further governmental trade actions demand close monitoring.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2026: Hooker Furnishings presented itself as a company in the midst of a cost and operational overhaul. The tone was one of cautious optimism, with management trying to stabilize operations, make margin progress, and emphasize strategic pivots (Vietnam warehouse, digital and product innovations). Macro and tariff uncertainties loomed large, but the business was not yet feeling acute pain outside of HMI. Orders were perking up, and management expressed hope for a traditional second-half sales ramp.Q2 2026: The narrative is now more about confronting hard realities—major cost cuts, dramatic HMI underperformance, and real impacts from finalized tariffs. Management has moved from simply planning to actively executing big, structural changes. There is early evidence of momentum (order upticks, progress in cost structure), but a sense of urgency and operational focus has replaced some of the optimism from Q1. The team is pragmatic about risk, especially liquidity and the sustainability of demand, and investors are warned to expect continued restructuring drag before seeing the hoped-for profitability inflection.

Year-over-year comparison

Q2 FY25: Hooker Furnishings was in the initial stages of cost transformation, focusing on weathering sector-wide challenges while emphasizing margin progress, new merchandising, and operational flexibility. The company was still relatively financially strong and expecting to benefit from macro stabilization.

Q2 FY26: A year later, the narrative is more somber but decisive—facing reality that headwinds are lasting longer and cutting deeper, especially for HMI. The company has doubled down on cost reduction (from $10M to $25M), forced to confront severe macro and segment-specific issues, and is in the thick of executing a high-stakes restructuring. Cash has become much tighter. However, new catalysts like product launches and warehouse/operational changes provide the possibility of a turnaround, provided cost savings and early order momentum prove durable.

Final Takeaway

Hooker Furnishings Corporation is in a deep restructuring phase, focusing on aggressive cost reduction, operational streamlining, and new growth catalysts (e.g., Margaritaville). While early order momentum and improving efficiency offer promise, the company remains hampered by persistent losses, a vulnerable HMI segment, and macro/tariff headwinds. Execution on cost cuts and demand recovery is critical. Verdict: HOLD, with the possibility of upside if revenue sustains and profitability inflects; however, near-term caution is warranted due to ongoing execution and liquidity risks.