Goldman Sachs BDC (NYSE: GSBD) – Q2 2025 Earnings

Goldman Sachs BDC (NYSE: GSBD) – Q2 2025 Earnings

Earnings Release Date: Aug. 7, 2025

Stock Price: $11.23

Market Cap: $1317.2 million

Q2 2025 sales of $91.0 million vs $108.6 million in the prior year

Q2 2025 EPS of $0.38 vs $0.57 in the prior year

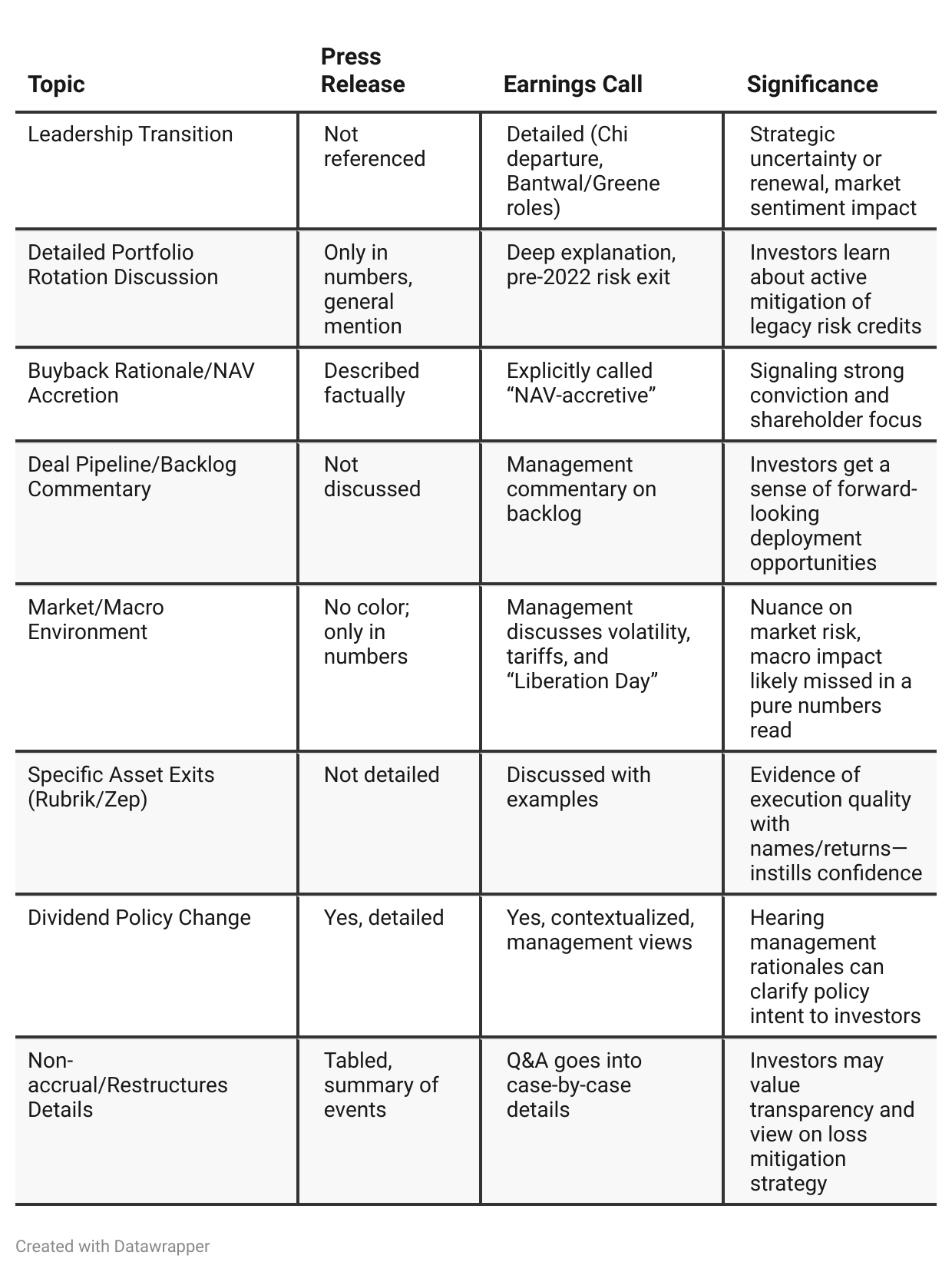

Press Release vs Call Transcript Comparison

Supplemental non-GAAP measures are explained in far more detail in the press release; the call just points to the document. The approach to present adjusted metrics after accounting for special dividends may create confusion unless investors read both.

The press release is backward-looking and quantitative, the call provides forward-looking tone, strategic context, and specific rationale for actions.

The press release omits macro/market outlook commentary, sector rotation strategy, emphasis on lead positions in new originations, examples of success stories (e.g., Rubrik)—all featured prominently on the call.

Q&A section in the call addresses points that could concern institutional investors (non-accruals, leverage trajectory), which are only stated at surface-level in the release.

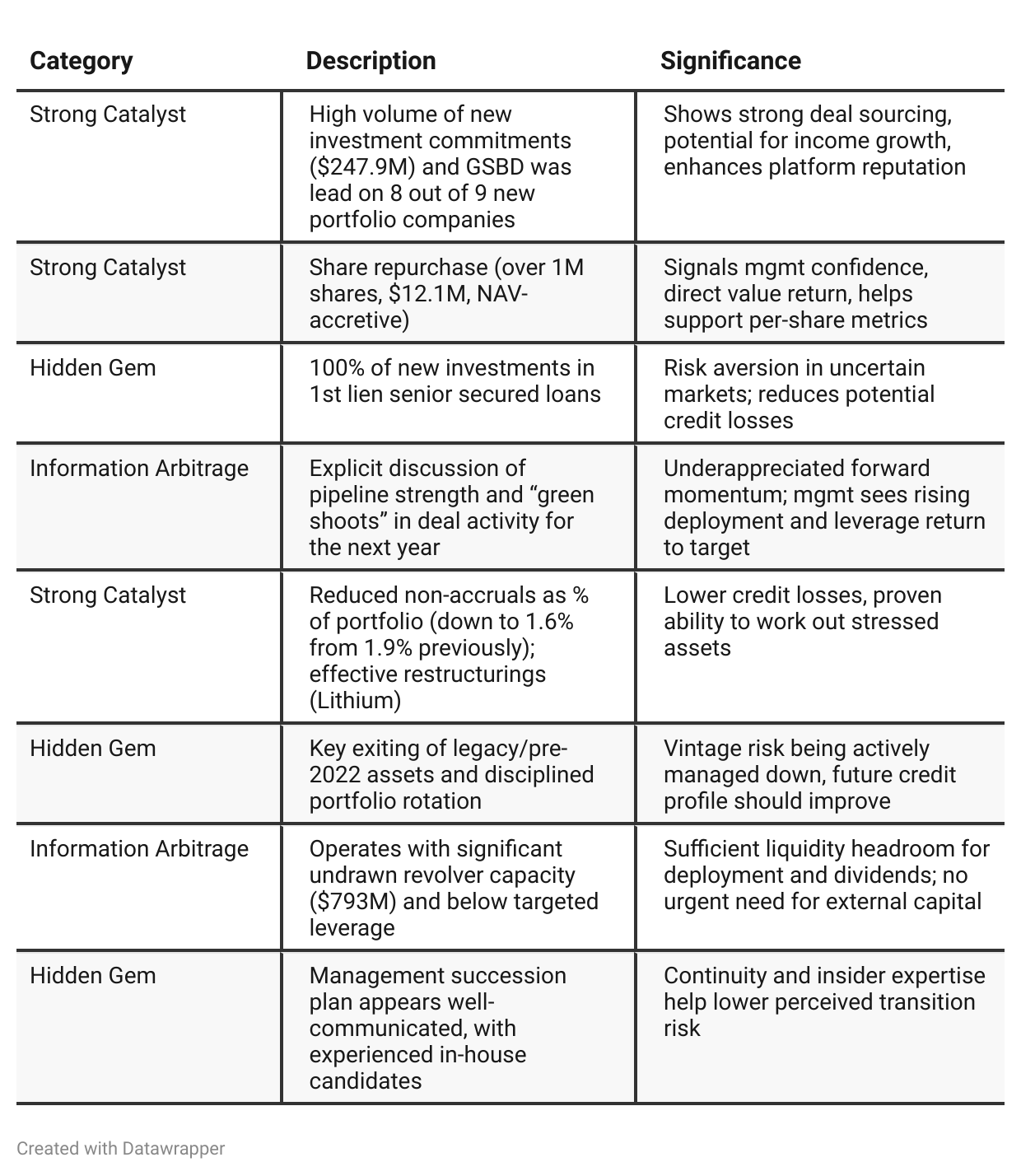

Positive Insights

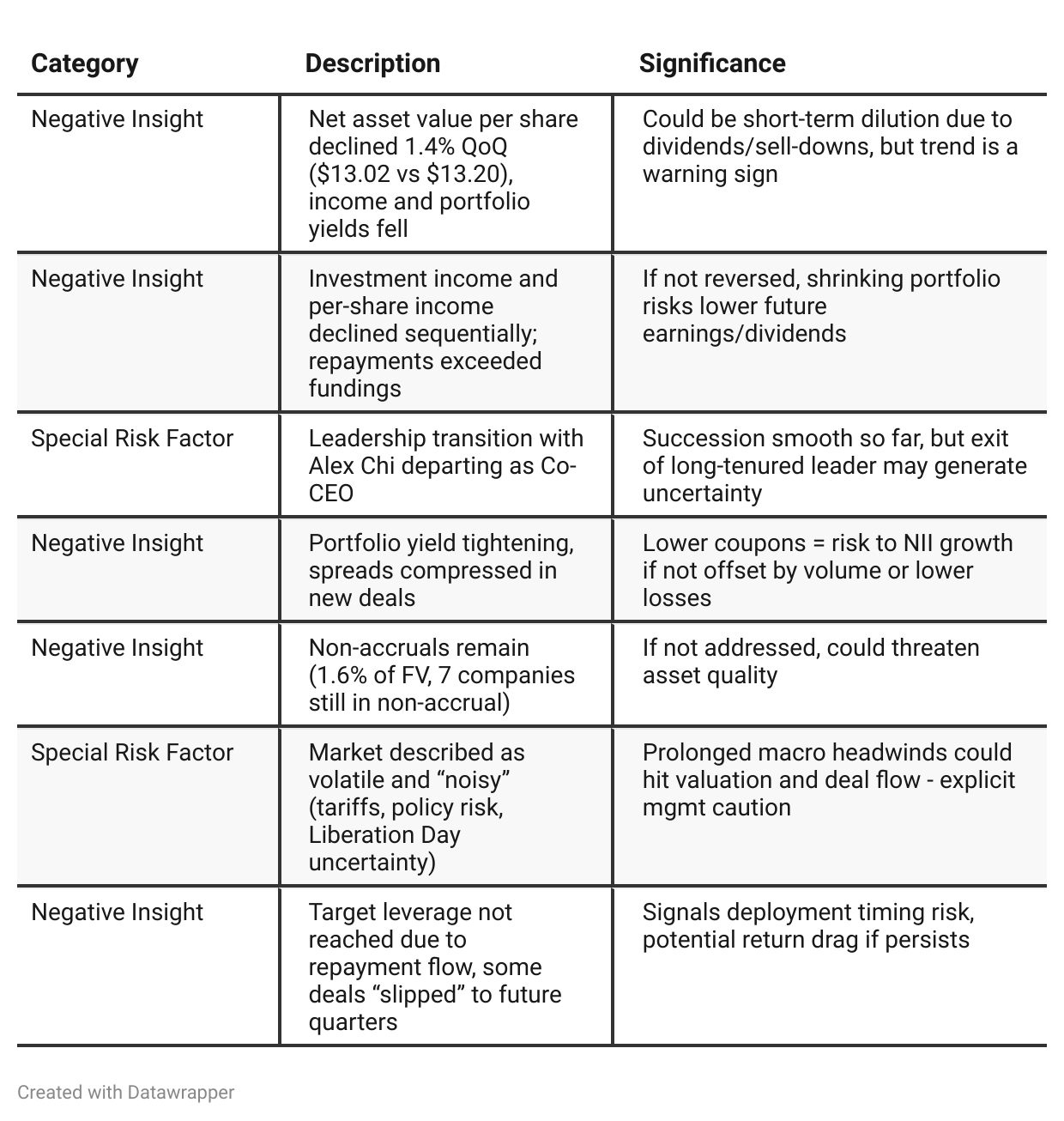

Negative Insights

Tariff Risk

Tariffs were mentioned several times as a key macro risk:

Management cited “policy volatility,” “tariff-sensitive industries,” and the lasting “noise” from recent tariff developments (e.g., hint at “Liberation Day”).

Explicit statement: “Uncertainty will persist, particularly in the tariff-sensitive industries,” but also noted increased activity in less-sensitive sectors (software, domestic services, financial services, digital infrastructure).

Public market hesitation following April tariff announcements, yet equity markets remain strong due to successful IPO activity.

GSBD’s approach—pivoting exposure towards low-tariff-impact sectors, rotating out of higher-risk sectors—is a core part of its credit discipline.

No direct mention of supply chain shifts, production relocations, or contract renegotiations at the BDC level (as they are a lender, not an operator), but GSBD is clearly emphasizing selective, tariff-resilient deal origination.

Forward-looking: Management sees ongoing volatility but a robust M&A pipeline as companies re-evaluate portfolios in light of tariffs. GSBD is positioned to benefit by focusing on sectors buffered from direct tariff impact. No earnings guidance adjustment for tariffs noted, but future quarters may see greater impact if policies worsen or trickle through to secondary industries.

Previous Earnings Call

Quarter-over-quarter comparison

Q1 2025 Narrative: GSBD is navigating a tough macro environment marked by tariff noise, sluggish M&A, and persistent yield pressure. Management is laser-focused on de-risking the portfolio, maintaining a first-lien bias, and weathering volatility with strong balance sheet discipline. The company is awaiting a pickup in deal activity, maintaining cautious optimism, and positioning itself for an eventual upturn.Q2 2025 Narrative: GSBD transitions from a mode of defense and waiting into action: ramping up new investments, accelerating portfolio rotation, and executing on buybacks—all underpinned by confidence in management continuity post-CEO transition. The tone is more constructive about the future, with actual evidence of increasing deal flow, active portfolio management, and visible shareholder return initiatives. Macro risks remain, but GSBD’s messaging shifts toward leveraging its competitive edge and focusing on growth opportunities rather than primarily risk containment.

Year-over-year comparison

Q2 2024: GSBD is “battle-tested”—candid about credit blemishes, but demonstrating origination momentum and portfolio resilience. The story is about handling existing pain points while leveraging Goldman’s platform to grow and upgrade the book. The dividend is solid, but risk is acknowledged.

Q2 2025: The narrative is one of maturity, succession, and operational momentum. The big story shifts from firefighting individual credits to shaping the next phase—exiting legacy positions, doubling down on quality leads, and using buybacks as a signal of confidence. Leadership change is handled with a forward-looking, team-based message. Macro worries persist, but GSBD sees itself as well-placed to navigate volatility and capture opportunity, as the M&A market revives and their competitive edge sharpens.

Final Takeaway

Goldman Sachs BDC is in a strategic portfolio rotation and stabilization phase, focusing on high-quality, senior secured lending and pruning legacy assets. While management succession and market volatility pose risks, strong capital access, healthy deal flow, and a disciplined credit outlook offer offsets. Execution on deployment and yield stabilization are critical for future upside. Verdict: Hold with a positive outlook, but with watchful eye on leverage rebuild and credit quality.