Genasys Inc. (NASDAQ: GNSS) – Q3 2025 Earnings

Genasys Inc. (NASDAQ: GNSS) – Q3 2025 Earnings

Earnings Release Date: Aug. 14, 2025

Stock Price: $1.64

Market Cap: $73.8 million

Q3 2025 sales of $9.9 million vs $7.2 million in the prior year

Q3 2025 loss per share of ($0.14) vs ($0.15) in the prior year

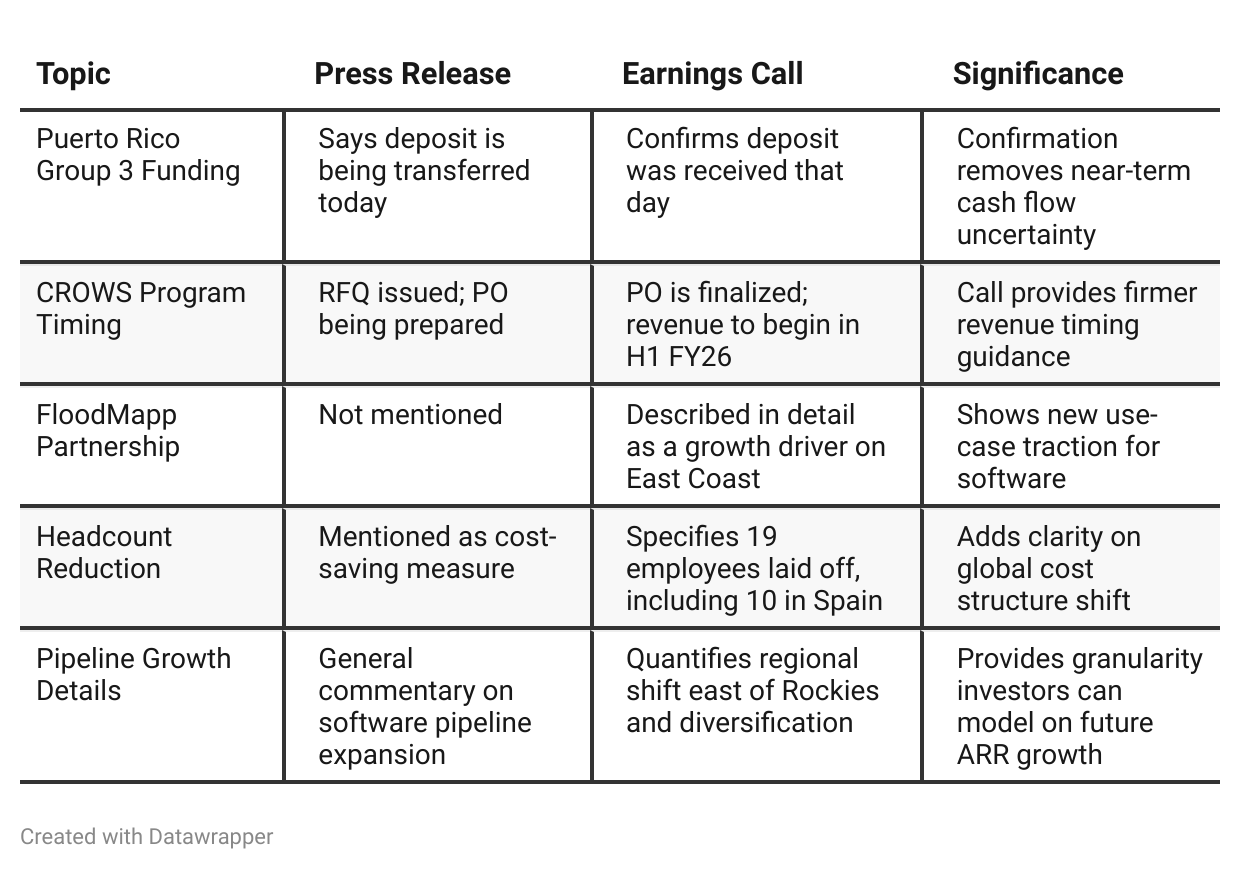

Press Release vs Call Transcript Comparison

While the press release highlights headline results and high-level business trends, the earnings call delivers real-time confirmations, contextual detail, and deeper strategic insight—especially around the status of Puerto Rico deposits, timing of CROWS revenue, and the traction of new product features like FloodMapp.

These differences are crucial from an investment perspective, as they de-risk cash flow assumptions and validate future growth levers not yet reflected in the financials. The call paints a more confident and clearer picture of operational execution and positioning heading into FY26.

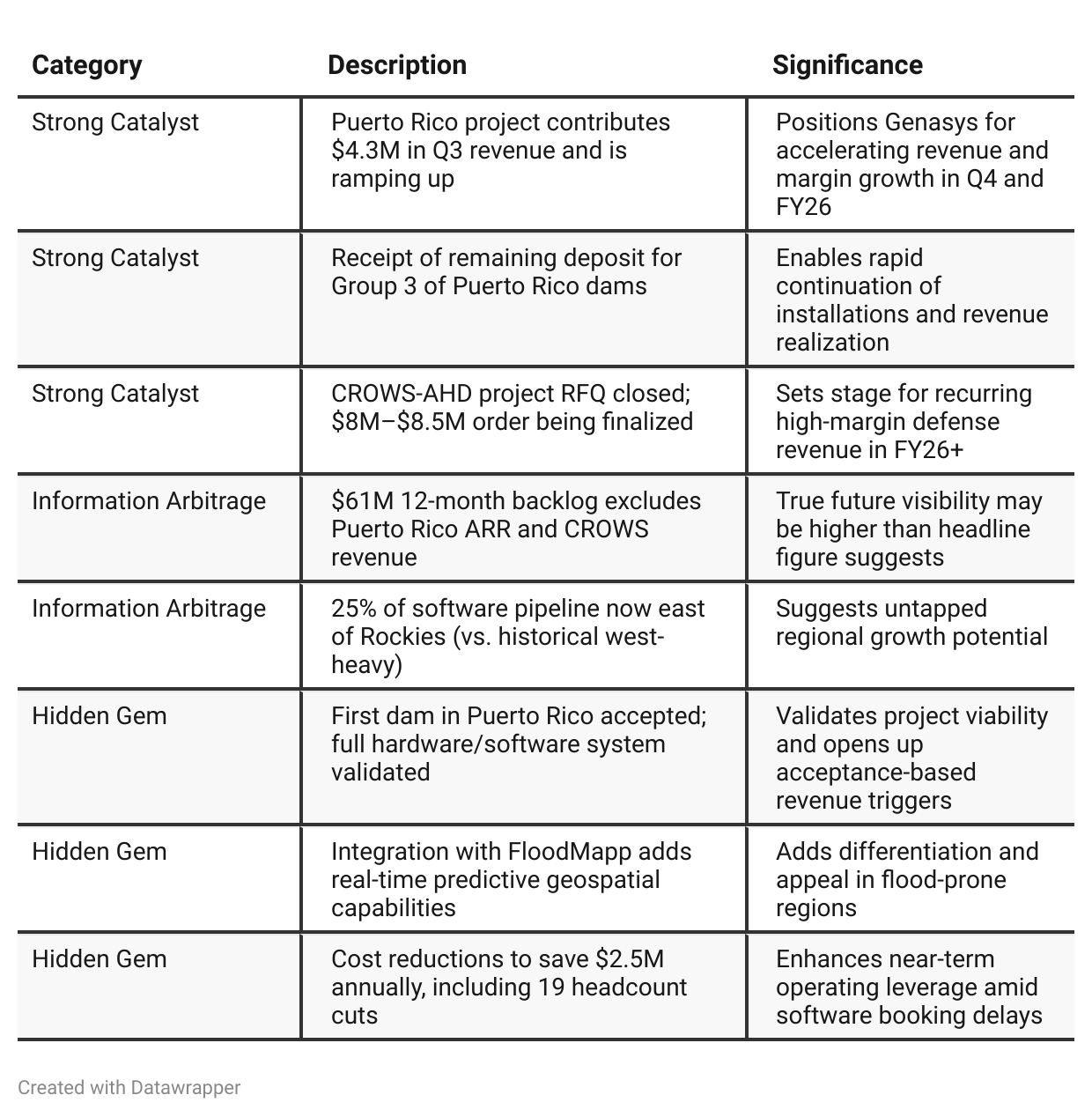

Positive Insights

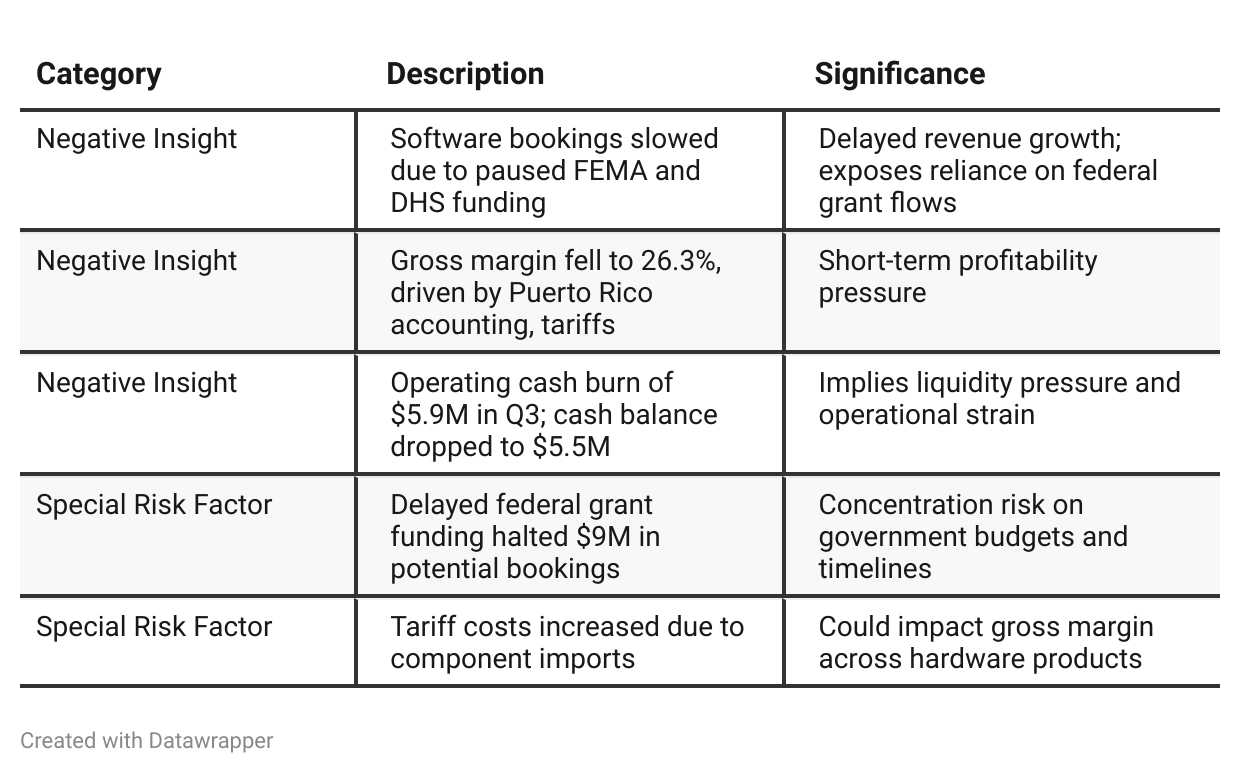

Negative Insights

Tariff Risk

Tariffs on imported components were explicitly cited as a reason for lower Q3 margins.

No direct commentary on mitigation efforts such as supplier shifts or pricing adjustments.

Management did not forecast future tariff impacts, indicating potential risk exposure remains unhedged.

No mention of impact on competitiveness or sourcing flexibility—an area investors should monitor closely.

Previous Earnings Call

Quarter-over-quarter comparison

From Q2 to Q3 2025, Genasys transitioned from a defensive stance—managing cash flow, awaiting key payments, and addressing public concerns—to an execution-oriented and strategically proactive posture. The company resolved the Puerto Rico funding bottleneck, recorded the first accepted installation, and positioned itself to recognize higher-margin revenue in Q4.

While federal grant freezes continued to constrain short-term software revenue, the sales pipeline reached record highs, aided by a geographic expansion and new feature sets. Cost control measures, including layoffs, were initiated to protect margins and cash runway. Additionally, progress on the CROWS program materialized into a pending $8M+ order, offering multiyear tailwinds.

The company now appears better positioned for profitable growth, though reliant on operational execution and continued stabilization in public sector funding.Year-over-year comparison

Between Q3 2024 and Q3 2025, Genasys has shifted from setting up strategic foundations to executing on those opportunities.

In Q3 2024, management emphasized multi-year visibility into record bookings via Puerto Rico and Army CROWS, highlighting strong ARR growth and software-driven transformation. By Q3 2025, that vision is partially realized — with Puerto Rico now contributing revenue and CROWS orders materializing — but real-world execution challenges have surfaced: federal funding delays, lower-than-expected margins, and cash burn issues.Despite these setbacks, the company continues to push growth through expanded geographic software reach and new feature sets (e.g., FloodMapp). The overall narrative is maturing from promise to proof — Genasys is now being judged on how well it can deliver on its backlog and monetize its differentiated platform.

Final Takeaway

Genasys is in a growth phase, anchored by major long-term contracts (Puerto Rico, CROWS) and a rapidly expanding software pipeline.

Despite short-term margin pressure, funding delays, and liquidity challenges, the company is reducing costs, improving operating leverage, and advancing contract execution. Execution on Puerto Rico buildout and CROWS delivery will be pivotal in determining near-term investor sentiment.

Verdict: Hold, with upside potential if funding constraints ease and gross margins rebound in Q4 and FY26.